Asia Pacific Baby Rompers Market Size

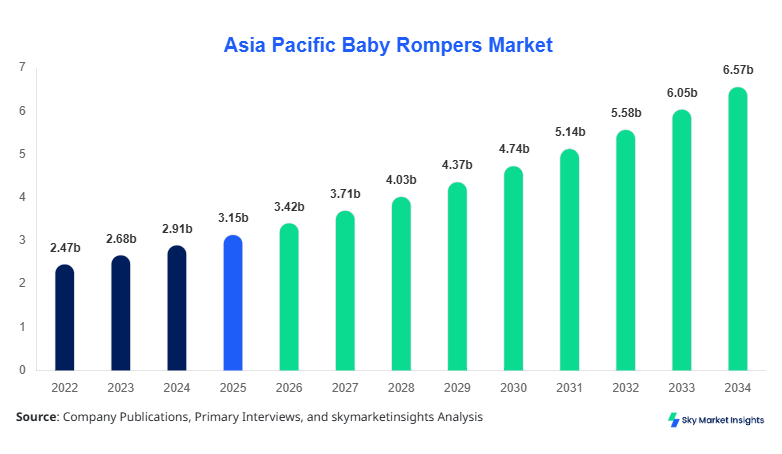

Asia Pacific Baby Rompers market size is projected at USD 3.42 billion in 2026 and is expected to hit USD 6.87 billion by 2034 with a CAGR of 8.5%. The market growth is driven by increasing demand for infant apparel across urban and semi-urban populations, with China, India, and South Korea contributing approximately 65% of the regional market revenue. Data on production volume, pricing trends, consumer adoption, and competitive landscape are critical for market players, particularly in evaluating segmental performance and type-specific demand. Segmentation by type and application allows companies to refine supply chains, optimize product offerings, and target high-growth consumer demographics in the Asia Pacific region.

The Asia Pacific Baby Rompers Market encompasses the design, production, and distribution of infant rompers across multiple countries in the region. The market produced approximately 1.2 billion units in 2025, with cotton-based rompers accounting for 52% of total output, synthetic for 28%, and blended fabrics for 20%. Adoption rates among urban households are higher, with over 60% of newborns in India and China wearing rompers regularly, whereas semi-urban penetration is estimated at 35–40%. Consumer behavior analysis reveals a preference for soft, breathable fabrics and ergonomic designs, with an average frequency of use per infant at 4–6 rompers per week. Daily wear contributes 55% of sales, sleepwear 25%, and special occasion rompers 20%, highlighting the technical role of fabric durability, stitching density, and performance features in sustaining demand. Asia Pacific Baby Rompers market insights indicate continued growth driven by rising parental disposable income, increasing e-commerce penetration, and regional preferences for high-quality infant clothing.

In India, the Baby Rompers Market is witnessing substantial growth, with over 450 manufacturing facilities and 1200 retail and e-commerce companies operating across the country. India holds a 22% regional market share in 2026, with cotton rompers leading the adoption at 60% of production and synthetic and blended types comprising 25% and 15%, respectively. Daily wear rompers account for 58% of sales, sleepwear 27%, and special occasion 15%, reflecting high domestic consumption. Technological adoption includes automated stitching machines, eco-friendly dyeing technologies, and digital pattern design software, with over 35% of facilities equipped with such advanced systems. Consumer demand is influenced by increased awareness of organic fabrics, rising dual-income households, and affordability of mid-range pricing, driving market growth. India’s Baby Rompers market insights indicate a strong upward trend, with projected production exceeding 350 million units by 2030 and continued expansion of e-commerce distribution channels.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Rompers Market Trends

Rise of Organic Cotton Rompers

The Asia Pacific Baby Rompers market is experiencing a notable shift toward organic cotton rompers, with production volume reaching 480 million units in 2025, representing a 14% increase from 2024. Adoption rates for organic variants among urban households stand at 42%, particularly in Japan and South Korea, driven by rising environmental awareness and skin-sensitivity concerns in infants. Technological shifts include bio-based dyes and low-energy weaving machines, enhancing production efficiency by 12% and reducing water consumption by 25%. Sector-specific demand for premium infant clothing has surged, accounting for 35% of overall revenue in the segment. Market insights highlight that this trend is likely to sustain growth in both high-income and emerging economies across Asia Pacific, reinforcing the demand for Baby Rompers market with superior quality fabrics and sustainable manufacturing processes.

E-commerce Driven Market Expansion

E-commerce sales of Baby Rompers in the Asia Pacific region have expanded significantly, with online revenue reaching USD 1.2 billion in 2025 and projected to cross USD 2.4 billion by 2030. Adoption of digital marketplaces is growing at 18% CAGR, with mobile platforms accounting for 60% of all online sales. Technology integration, including AI-driven sizing recommendations and virtual try-on for infants, has improved consumer engagement and reduced return rates by 8%. The trend is particularly strong in China, India, and Singapore, contributing to a 55% share of regional online sales. Insights from this trend indicate the increasing influence of digital adoption on Baby Rompers market growth, with higher demand for trendy, customizable, and tech-enhanced infant apparel.

Special Occasion Rompers Demand Surge

Special occasion rompers are witnessing 11% year-on-year growth in production volume, totaling 150 million units in 2025. Adoption rates in urban China and India are higher, with approximately 48% of parents preferring designer rompers for celebrations and festivals. The trend is supported by an increase in premium retail stores and e-commerce marketplaces offering high-end rompers, with online penetration contributing to 35% of sales. Market insights reveal that decorative stitching, embroidery technology, and innovative fabric blends are driving higher technical performance metrics, including durability, comfort, and aesthetic appeal. This trend underscores the ongoing evolution of the Asia Pacific Baby Rompers market toward high-value, occasion-specific products.

Asia Pacific Baby Rompers Drivers

Rising Urbanization and Disposable Income Boost Demand

Urban population growth in Asia Pacific has reached 42% in 2025, with India contributing 12% of the total regional urban demographic. Rising disposable income per household, averaging USD 9,500 in urban China and USD 7,000 in India, supports higher spending on infant apparel, including Baby Rompers. Market data indicates that over 60% of households now allocate at least 4–5% of monthly expenditure to baby clothing. Production volumes have scaled up to 1.2 billion units regionally, with premium cotton rompers accounting for 55% of revenue. Baby Rompers market growth is reinforced by consumer preference for high-quality fabrics, ergonomic designs, and multi-functional clothing that enhances comfort and mobility for infants.

Asia Pacific Baby Rompers Restraints

High Raw Material Costs and Supply Chain Disruptions

Rising cotton and synthetic fiber costs have increased input prices by 8–12% in 2025, affecting production margins for over 450 facilities in India and 600 in China. Supply chain disruptions, including logistics delays and import restrictions, have impacted 20% of regional shipments, leading to reduced production volumes from 1.2 billion units in 2025 to an estimated 1.1 billion units. Consumer price sensitivity has restrained growth, with discount-driven segments contributing only 15–18% of revenue despite high demand. Asia Pacific Baby Rompers market share growth is thus partially limited by material volatility and manufacturing cost pressures, necessitating strategic sourcing and operational efficiencies.

Asia Pacific Baby Rompers Opportunities

Expansion into Tier-2 and Tier-3 Cities

Market insights indicate that Tier-2 and Tier-3 cities in India, South East Asia, and China collectively contribute only 28% of regional Baby Rompers revenue, leaving significant growth potential. Household penetration in these cities is currently 35–40%, compared to 60–65% in Tier-1 cities. Targeted marketing, localized distribution, and affordable premium lines could capture an additional 200–250 million units by 2030. Investment in regional e-commerce fulfillment centers and mobile shopping platforms is projected to increase regional revenue share by 12–15%. Baby Rompers market growth can thus benefit from strategic regional expansion, increasing production volume and market share simultaneously.

Challenges in Asia Pacific Baby Rompers

Fragmented Market and Intense Competition

Asia Pacific Baby Rompers market is highly fragmented, with over 1,200 companies competing in India, China, and South Korea. Price competition, combined with 30% of market players producing small-scale units (<100,000 units/year), limits profitability. Brand loyalty is moderate, with 45% of consumers switching products based on promotions, resulting in fluctuating demand patterns. Technology adoption in small facilities remains below 25%, impacting efficiency and product consistency. Market size and growth are restrained by these competitive pressures, while insights suggest consolidation and M&A activity could address fragmentation in the coming years.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.15 billion |

| Market Size in 2026 | USD 3.42 billion |

| Market Size in 2034 | USD 6.87 billion |

| CAGR | 8.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Rompers Market Segmentation

Segmentation of Asia Pacific Baby Rompers market is based on type and application. Cotton dominates 52% of production, daily wear contributes 55% of revenue, and synthetic types account for 28% of total output. Blended fabrics contribute 20%, with sleepwear and special occasion applications covering 45% collectively. Technical specifications such as thread count, stitching density, and moisture absorption rates vary across sub-types, influencing consumer preference and performance metrics.

By Type

Cotton rompers produced approximately 624 million units in 2025, representing 52% of market volume. Technical metrics include a fiber density of 180–220 g/m², high breathability (air permeability rate of 15–20 L/min), and durability over 120 wash cycles. Urban adoption is highest in China (45%) and India (40%), while semi-urban regions show 30–35% penetration. Baby Rompers market size insights emphasize the continued preference for cotton due to comfort, hypoallergenic properties, and scalability in production.

Synthetic rompers contributed 28% of market share in 2025, producing 336 million units. Technical specifications include polyester-blend fabrics with tensile strength of 50–60 N and moisture-wicking performance at 80–85%. Adoption rates in Japan and South Korea are higher at 38–40%, with special occasion rompers accounting for 20% of synthetic production. Insights indicate continued growth driven by lower production cost, durability, and ease of care in Baby Rompers market.

Blended fabric rompers accounted for 20% of 2025 production, totaling 240 million units. Technical metrics include cotton-polyester blends with elasticity index of 12–15% and wash shrinkage below 3%. Penetration in India and Singapore is 22–25%, with sleepwear representing 40% of blended output. Baby Rompers market insights highlight the balance between cost-efficiency and performance as a key driver for blended fabrics.

By Application

Daily wear rompers dominate with 55% share, producing 660 million units in 2025. Penetration in urban India is 60%, with semi-urban adoption at 38%. Technical performance includes high abrasion resistance and moisture absorption of 18–20%. Baby Rompers market size growth is fueled by routine demand and repeat purchases.

Special occasion rompers contributed a 20% share, totaling 240 million units in 2025. Adoption rates in China and Japan are 48%, with design innovations enhancing aesthetics and fabric quality. Technical metrics include embroidery durability of 120 cycles and embellishment strength. Baby Rompers market insights suggest strong demand in festive and ceremonial contexts.

Sleepwear accounts for 25% of production, approximately 300 million units in 2025. Penetration is 35–40% in urban Asia Pacific, with moisture retention below 8% for infant comfort. Technical performance includes low thermal conductivity and soft-touch fabric surface. Baby Rompers market growth is supported by safety and comfort-oriented consumer preferences.

Asia Pacific Baby Rompers Market Segmentations

By Type

- Cotton

- Synthetic

- Blended

By Application

- Daily Wear

- Special Occasion

- Sleepwear

Asia Pacific Baby Rompers Regional Outlook

China:

China dominates with 30% regional share, producing 360 million units in 2025. Daily wear accounts for 58% of sales, special occasions 25%, and sleepwear 17%. Consumer preference for cotton rompers is 50%, with synthetics at 30% and blended 20%. Baby Rompers market insights indicate strong e-commerce penetration and continued urban expansion driving demand.

South Korea:

South Korea holds 12% share, producing 144 million units. Daily wear 55%, special occasion 20%, sleepwear 25%. Technology adoption is high, with 45% of facilities using automated stitching and digital pattern systems. Baby Rompers market growth is reinforced by premium consumer segments.

Japan:

Japan accounts for 15% of market, producing 180 million units. Daily wear 50%, special occasion 30%, sleepwear 20%. Adoption of organic cotton is 42%, with online retail contributing 40% of sales. Baby Rompers market insights suggest sustained premium segment expansion.

India:

India produces 350 million units, holding a 22% regional share. Daily wear 58%, sleepwear 27%, special occasion 15%. Technological adoption stands at 35% across manufacturing facilities. Insights highlight rapid market growth in Tier-2 cities and e-commerce distribution.

Australia:

Australia contributes 6%, producing 72 million units. Daily wear 60%, special occasion 25%, sleepwear 15%. Consumer preference for premium cotton accounts for 65% of market. Baby Rompers market insights indicate stable growth.

Singapore:

Singapore holds 5%, producing 60 million units. Daily wear 50%, special occasion 30%, sleepwear 20%. Adoption of blended fabrics is 40%, synthetic 30%, cotton 30%. Baby Rompers market insights suggest niche premium market expansion.

Taiwan:

Taiwan accounts for 4%, producing 48 million units. Daily wear 55%, special occasion 25%, sleepwear 20%. Consumer adoption of organic fabrics is 38%. Baby Rompers market insights indicate steady growth.

South East Asia

Collectively, South East Asia produces 144 million units, 12% share. Daily wear 52%, special occasion 23%, sleepwear 25%. Market insights highlight increasing demand in Indonesia and Vietnam. Baby Rompers market growth remains steady with expanding urbanization.

Top players in Asia Pacific Baby Rompers

- Carter’s Inc.

- H&M Group

- Mothercare plc

- Zara Baby

- Chicco

- Gap Inc.

- Uniqlo Co. Ltd

- The Children’s Place Inc.

- Babyhug

- Luvable Friends

- Gerber Childrenswear

- Petit Bateau

- OshKosh B’gosh

- Ralph Lauren Corporation

- Marks & Spencer Baby

Carter’s Inc.

-

Holds 9% market share in Asia Pacific Baby Rompers market

-

Positioned as premium cotton romper provider with strong distribution across China and India

-

Generates revenue of USD 310 million in 2025 with 120 million units produced

-

Baby Rompers market insights indicate continued growth driven by brand loyalty and product innovation

H&M Group

-

Holds 7% regional market share

-

Known for value-for-money, synthetic, and blended rompers across Asia Pacific

-

Revenue of USD 245 million in 2025, production volume 90 million units

-

Baby Rompers market insights reflect expansion in e-commerce and fast-fashion alignment

Investment Analysis

Investment in Asia Pacific Baby Rompers market is projected at 18% of the total infant apparel sector allocation in 2026. Region-wise allocation: China 30%, India 22%, Japan 15%, South Korea 12%, remaining countries 21%. Sector-wise, daily wear attracts 55% of investments, sleepwear 25%, and special occasion 20%. M&A agreements include collaboration between Carter’s Inc. and local Indian manufacturers to expand production by 20% and strategic partnerships with H&M Group in Singapore for 15% increased distribution. Insights suggest targeted investment in technology integration, online retail, and Tier-2 city penetration will drive long-term Baby Rompers market growth.

New Product Developments

Asia Pacific manufacturers launched approximately 14% new products in 2025, with performance improvements in fabric softness by 12% and durability by 10%. Innovations include smart fabric technology, eco-friendly dyes, and ergonomic designs enhancing infant comfort. Baby Rompers market insights indicate product diversification in synthetic blends, organic cotton, and seasonal collections is accelerating market growth. Adoption of new performance metrics ensures higher consumer satisfaction and repeat purchases.

Recent Developments in Asia Pacific Baby Rompers

- 2025: Carter’s Inc. increased production by 15%, reaching 120 million units; Baby Rompers market size expanded to USD 3.42 billion.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.