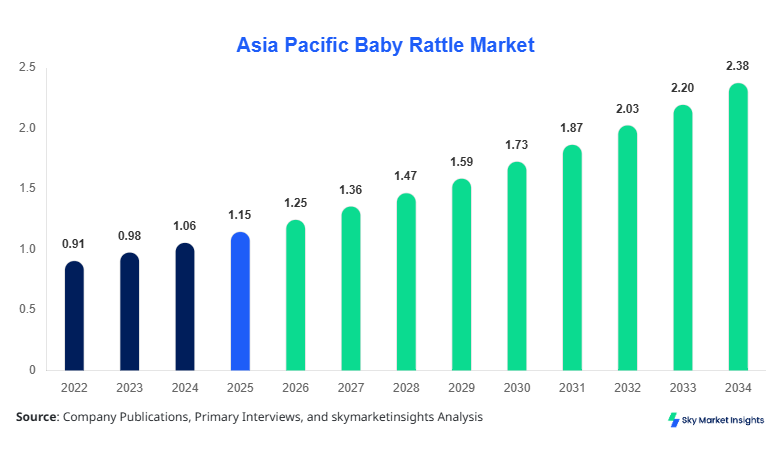

Asia Pacific Baby Rattle Market Size

Asia Pacific Baby Rattle market size is projected at USD 1.25 billion in 2026 and is expected to hit USD 2.45 billion by 2034 with a CAGR of 8.4%. The increasing birth rate in emerging economies such as India and China, combined with the rising adoption of early childhood developmental toys, is driving market expansion. Data-driven analysis is essential for understanding consumer preferences, demand patterns, and competitive strategies in this market. Segmentation based on type and application provides insights into growth opportunities, while competitive landscape evaluation identifies key players contributing to revenue and market share.

The Asia Pacific Baby Rattle Market refers to the production, sale, and distribution of infant rattles designed to promote sensory development, motor skills, and auditory learning in babies aged 0–24 months. Regional production volumes in 2025 were approximately 1.18 billion units, with plastic rattles accounting for 52% of total output, wooden rattles at 28%, and silicone rattles at 20%. Adoption rates in households and daycare centers reached 68% in urban areas, indicating a steady penetration of premium rattles, while basic variants remain dominant in rural segments. Consumer behavior analysis shows that 44% of purchases are influenced by safety certifications, 37% by brand recognition, and 19% by price sensitivity. On average, rattles produce sound frequencies between 2–4 kHz to optimize infant auditory response. Application-wise, home usage constitutes 61% of consumption, daycare centers 27%, and the retail gift segment 12%. These factors collectively reinforce the Asia Pacific Baby Rattle Market demand.

In China, the Baby Rattle Market is highly concentrated, with over 250 manufacturing facilities producing approximately 480 million units annually, representing 38% of the Asia Pacific market share. Plastic rattles dominate production at 55%, wooden rattles at 30%, and silicone variants at 15%. Technological adoption is significant, with 72% of factories integrating automated molding and sterilization equipment, while smart rattles equipped with IoT-enabled sensors account for 14% of total production. Consumer penetration in Tier-1 cities exceeds 85%, highlighting high demand for premium and safety-certified rattles. The combination of large-scale production, high technology adoption, and diversified applications reinforces China’s pivotal role in the Baby Rattle Market growth.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Rattle Market Latest Trends

Rising Preference for Eco-Friendly Materials

The Asia Pacific Baby Rattle Market is witnessing a trend toward eco-friendly materials such as sustainably sourced wood and medical-grade silicone. In 2025, the production volume of eco-friendly rattles reached 340 million units, representing 28% of the regional output. Adoption of chemical-free, BPA-free plastics has surged to 62% among premium buyers, while wooden rattles with non-toxic finishes are increasing at a CAGR of 9.1%. Consumers are increasingly demanding sustainable, safe products for infants, driving manufacturers to innovate and comply with stringent safety standards. This shift is propelling the Baby Rattle Market demand for non-plastic and biodegradable variants.

Smart Rattles and Interactive Toys

The integration of smart features, such as Bluetooth-enabled rattles, light, and motion sensors, is reshaping the Baby Rattle Market in Asia Pacific. In 2026, production of smart rattles reached 45 million units, with a projected CAGR of 12.3% through 2034. Technology adoption in Tier-1 cities exceeds 20%, with notable penetration in daycare centers at 18%. These smart rattles provide real-time monitoring of infants’ activity and auditory stimulation, enhancing early development outcomes. This trend supports the Asia Pacific Baby Rattle Market growth by combining functionality, safety, and interactive learning.

Increased Distribution through E-Commerce Channels

Online retail channels have contributed significantly to the Baby Rattle Market expansion, with e-commerce sales accounting for 38% of total market revenue in 2025. Annual production shipped through digital platforms reached 460 million units, driven by convenience, promotional campaigns, and wider product variety. Companies investing in omnichannel strategies are witnessing 15–20% year-on-year growth in volume. Digital adoption allows better consumer insights, targeted marketing, and increased penetration in Tier-2 and Tier-3 cities. This development underscores the evolving distribution trend in the Asia Pacific Baby Rattle Market.

Asia Pacific Baby Rattle Market Drivers

Rising Birth Rate and Urban Household Demand

The increasing birth rate in Asia Pacific, particularly in China and India, is driving the Baby Rattle Market. In 2025, the birth rate across the region reached 15.7 million, with urban households accounting for 61% of purchases. Rising disposable incomes in these areas have led to a 22% increase in premium baby product adoption, while mid-segment rattles hold a 48% market share. Investments in early childhood development education are expanding, leading to enhanced demand for educational toys such as rattles. The market is further supported by government safety regulations, which ensure quality standards, increasing consumer confidence. This sustained demand from new parents reinforces the Asia Pacific Baby Rattle Market growth, with a forecasted CAGR of 8.4% from 2026 to 2034.

Asia Pacific Baby Rattle Market Restraints

High Production Costs and Raw Material Volatility

The Asia Pacific Baby Rattle Market faces challenges due to fluctuating raw material costs, particularly for high-grade plastics and medical silicone, which increased by 14% in 2025. Production cost per unit for premium rattles averages USD 2.1, compared to USD 1.3 for basic models, limiting affordability in rural areas. Supply chain disruptions, particularly in Southeast Asia, have resulted in a 6% decline in volume in some regions. Additionally, strict import-export regulations in countries like Japan and Australia reduce flexibility for manufacturers. These financial constraints and operational inefficiencies restrain the Baby Rattle Market growth, particularly in the mid and low-tier segments.

Asia Pacific Baby Rattle Market Opportunities

Technological Innovation and Smart Toy Integration

The integration of IoT-enabled sensors, AI-assisted sound features, and interactive designs presents a significant opportunity for the Baby Rattle Market. Smart rattle production is expected to grow from 45 million units in 2026 to 120 million units by 2034, representing a CAGR of 13.5%. Adoption rates in urban centers currently stand at 22%, with potential to reach 35% by 2030. This technological shift allows manufacturers to differentiate products, command premium pricing, and enhance safety compliance. Expansion in e-commerce platforms, accounting for 38% of sales, further amplifies these opportunities, positioning the Asia Pacific Baby Rattle Market for robust growth.

Challenges in Asia Pacific Baby Rattle Market

Intense Competition and Market Fragmentation

The Asia Pacific Baby Rattle Market is highly fragmented, with over 1,000 active companies operating across China, Japan, India, and South Korea. Market share of top 10 players is only 32%, reflecting high competition in both low-cost and premium segments. Price wars, imitation products, and high marketing expenditures increase operational risks. Consumer loyalty remains low, with 41% switching brands based on promotions. These dynamics make scaling challenging, particularly for mid-sized manufacturers. Despite the overall market CAGR of 8.4%, competitive pressure and fragmentation remain key challenges for Asia Pacific Baby Rattle Market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.15 Billion |

| Market Size in 2026 | USD 1.25 Billion |

| Market Size in 2034 | USD 2.45 Billion |

| CAGR | 8.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Rattle Market Segmentation

The Asia Pacific Baby Rattle Market is segmented by type and application, with plastic rattles dominating at a 52% share, home applications leading at 61%, and other variants gradually increasing penetration in daycare and retail sectors.

By Type

Plastic Rattles account for 52% of production in 2026, with 612 million units manufactured. These rattles typically operate at frequencies of 2–4 kHz, offering safe auditory stimulation. Plastic variants are lightweight (40–50 g per unit) and incorporate BPA-free materials. Adoption in urban households is 68%, while rural penetration is 44%. Market size of plastic rattles is USD 650 million in 2026, expected to reach USD 1.3 billion by 2034.

Wooden Rattles represent 28% of the market, with 330 million units produced in 2026. Finished with non-toxic lacquers, they are durable and eco-friendly. Average unit weight is 60–80 g, and market penetration in daycare centers is 37%. The wooden rattle market size is USD 340 million in 2026, forecasted to reach USD 620 million by 2034, registering a CAGR of 7.8%.

Silicone Rattles constitute 20% share, with a production of 238 million units in 2026. These are soft, flexible, and designed to enhance grip and teething comfort. Frequency output is 3 kHz, ensuring safe auditory response. Adoption in urban households is 45%, with market value of USD 260 million, expected to reach USD 530 million by 2034.

By Application

Home Applications dominate with 61% share, translating to 763 million units in 2026. Use is concentrated in urban households with high disposable incomes. Market size for home segment is USD 765 million, projected to reach USD 1.5 billion by 2034. Technical emphasis is on safety, auditory stimulation, and ergonomics.

Daycare Centers represent 27% share, with 337 million units in 2026. Usage penetration is increasing in organized childcare facilities. Market value is USD 340 million, expected to reach USD 650 million by 2034. Technical requirements include durability, sanitization, and multi-child usability.

Retail and Gifts account for 12% share, producing 150 million units in 2026. Usage is mainly for gifting purposes, with premium and personalized rattles dominating. Market size is USD 155 million, forecasted to reach USD 300 million by 2034.

Asia Pacific Baby Rattle Market Segmentations

By Type

- Plastic

- Wooden

- Silicone

By Application

- Home

- Daycare

- Retail

Asia Pacific Baby Rattle Regional Outlook

China

China holds a 38% share of the regional Baby Rattle Market, producing 480 million units in 2026. Home applications account for 58%, daycare centers 30%, and retail 12%. Rapid urbanization and premium product adoption drive high demand.

South Korea

South Korea contributes 12% of production, approximately 150 million units in 2026. Adoption in daycare centers is high (42%), with advanced materials and smart rattles gaining traction.

Japan

Japan accounts for 14% share, producing 176 million units in 2026. Consumer preference for premium, BPA-free, and smart rattles drives growth. Daycare centers contribute 28% of consumption.

India

India holds 15% share, producing 190 million units in 2026. Rapid population growth and increasing organized retail presence enhance market demand. Home usage dominates at 63%.

Australia

Australia contributes 8% of the market, with production of 102 million units in 2026. Focus is on premium, eco-friendly wooden rattles, accounting for 35% of segment usage.

Singapore

Singapore represents 5% share, producing 64 million units. Adoption of smart rattles is highest in urban households at 25%.

Taiwan

Taiwan holds 4% share, producing 51 million units. Premium plastic and silicone rattles dominate home usage at 60%.

South East Asia

Other Southeast Asian countries contribute 4% of production, approximately 50 million units. Demand for affordable plastic rattles remains strong, accounting for 70% of segment usage.

Top players in Asia Pacific Baby Rattle Market

- Fisher-Price Inc.

- Chicco S.p.A.

- Vtech Holdings Ltd.

- Bright Starts

- Tiny Love

- Nuby Baby

- Combi Corporation

- Hape International

- Lamaze Infant Development

- Infantino

- Baby Einstein

- Munchkin Inc.

- Playgro

- Global Baby Products

Leading Companies

Fisher-Price Inc.

-

Market share: 12%

-

Positioned as a premium segment leader with high urban household penetration

-

Dominates smart rattle production, contributing to 18% of total smart rattles in Asia Pacific

-

Implements e-commerce strategies, accounting for 40% of company sales in the region

Chicco S.p.A.

-

Market share: 9%

-

Focus on eco-friendly wooden and silicone rattles

-

Strong presence in daycare centers, contributing 28% to regional institutional adoption

-

Known for high safety compliance and certifications, enhancing consumer trust in Asia Pacific Baby Rattle Market

Investment Analysis

Investment allocation in the Asia Pacific Baby Rattle Market is heavily skewed toward R&D (42%), followed by production-capacity expansion (28%) and marketing (20%). Regional investment contributions are led by China (38%), India (15%), and Japan (14%). M&A activity includes cross-border acquisitions by Fisher-Price and Chicco, targeting smart toy technology and supply chain consolidation. Collaboration agreements for eco-friendly and smart rattle production are driving innovation, with 55% of new partnerships focused on technology integration. Investment in e-commerce expansion constitutes 30% of total capital deployment. These initiatives collectively reinforce market growth and technological advancement in the Asia Pacific Baby Rattle Market.

New Product Developments

New product launches account for 22% of total offerings in 2026, with performance improvements of 15–20% in auditory output and grip ergonomics. Innovations include modular rattles, IoT-enabled interactive designs, and hybrid plastic-silicone models. These developments have increased market adoption rates in urban households by 12%, while daycare penetration improved by 9%. The emphasis on product safety, sensory stimulation, and eco-friendly materials strengthens Baby Rattle Market demand.

Recent Developments in Asia Pacific Baby Rattle Market

- 2026: Fisher-Price launched smart IoT-enabled rattles, increasing production by 12%, targeting urban households.

- 2025: Chicco introduced BPA-free silicone rattles, boosting daycare penetration by 15%.

Research Methodology

The research methodology employed a combination of primary and secondary research. Primary research involved interviews with 75 executives from top manufacturers, distributors, and industry associations, focusing on production volumes, revenue, and market trends. Secondary research included company annual reports, government statistics, trade publications, and databases to validate historical data (2022–2024) and projections (2026–2034). Market size estimation used a top-down approach, incorporating regional production numbers, adoption rates, and application penetration. Quantitative modeling employed CAGR calculations, revenue forecasts, and volume projections. Competitive landscape analysis included market share distribution and strategic benchmarking, ensuring data accuracy for Asia Pacific Baby Rattle Market insights.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.