Asia Pacific Baby Carriers Market Size

Asia Pacific Baby Carriers market size is projected at USD 1.82 billion in 2026 and is expected to hit USD 3.64 billion by 2034 with a CAGR of 8.7%. This forecast reflects robust demand driven by increasing working parents, urbanization, and rising disposable incomes across countries such as India, China, and Japan. Comprehensive data collection covering production volumes, consumption rates, and pricing trends is essential to evaluate regional variations and the competitive landscape. Segmentation by type, application, and technology adoption is required to understand granular demand patterns and support strategic investment decisions. In addition, mapping the competitive landscape—including both multinational and regional players—enables identification of growth opportunities, market gaps, and innovation potential in the Asia Pacific Baby Carriers market.

The Asia Pacific Baby Carriers market is defined as the manufacture, distribution, and sale of infant and toddler carrying solutions designed to improve parental mobility and comfort. In 2025, the region produced an estimated 12.8 million units of baby carriers, driven largely by high population density and increasing nuclear families in urban areas. Adoption is accelerating, with penetration rates of soft structured carriers at 42%, wrap carriers at 33%, and slings at 25%. Consumer behavior demonstrates a preference for ergonomic designs, adjustable straps, and multi-position carriers, reflecting demand for convenience and infant safety. In 2025, the infant application segment accounted for 54% of total consumption, toddler 32%, and multipurpose 14%, indicating a dominant focus on early-childhood mobility solutions. Frequency of use averages 3–4 hours per day in urban households, with technical specifications such as load capacity ranging from 7–20 kg, adjustable back support, and breathable fabrics being critical selection factors. Overall, the Asia Pacific Baby Carriers market demand, growth, and insights continue to reflect evolving parental lifestyles, product innovation, and regional production capacities.

In India, the Baby Carriers Market has seen significant expansion, with over 180 manufacturing facilities and more than 95 active companies contributing to 28% of the regional market share in 2026. The infant application segment represents approximately 60% of total demand, followed by toddler carriers at 30% and multipurpose solutions at 10%. Technology adoption is robust, with 72% of products integrating ergonomic designs, adjustable waist and shoulder supports, and eco-friendly materials. Production volume in India is estimated at 3.2 million units in 2026, with a CAGR of 9.1% projected through 2034. The India market size, growth, and insights are underpinned by rising urban nuclear families, increasing e-commerce penetration, and the growing preference for branded and certified carriers. Consumer awareness regarding infant health and mobility ergonomics further strengthens the India Baby Carriers market demand and competitive landscape.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Carriers Market Trends

Technological Advancements in Ergonomic Design

The Asia Pacific Baby Carriers market has witnessed a shift toward ergonomically enhanced products, with approximately 65% of new units featuring adjustable lumbar support, padded straps, and breathable fabrics. Production volumes reached 4.5 million units in 2025, and the adoption rate of ergonomically optimized carriers is projected to rise to 78% by 2030. Innovations in modular designs allow parents to switch between front, back, and hip-carry positions, meeting diverse usage scenarios. The market demand for such advanced carriers is reinforced by rising urban parental awareness, contributing to overall market growth and insights.

Eco-Friendly and Sustainable Materials

Sustainability is a key trend in the Asia Pacific Baby Carriers market, with 48% of carriers now manufactured using organic cotton, bamboo fiber, or recycled polyester. Regional production volumes using sustainable materials increased from 1.2 million units in 2022 to 2.1 million units in 2025, reflecting a compound annual growth of 18%. Consumer preference for eco-friendly products is highest in Japan (56%) and South Korea (51%), driving adoption of recyclable and non-toxic components. This trend not only addresses regulatory requirements but also reinforces the market size and growth of the Asia Pacific Baby Carriers market.

E-Commerce and Direct-to-Consumer Channels

Online retail has transformed the Baby Carriers market, with e-commerce accounting for 44% of sales in 2025 and projected to reach 62% by 2030. Digital channels enable companies to introduce new products rapidly, gather consumer feedback, and monitor adoption rates in real time. Production volumes sold through online platforms reached 2.6 million units in 2025, with a CAGR of 10% projected over the forecast period. The integration of digital sales channels strengthens the Asia Pacific Baby Carriers market demand and insights.

Baby Carriers Market Drivers

Increasing Urbanization and Dual-Income Families

Rapid urbanization in countries such as China, India, and South Korea is fueling demand for baby carriers, with urban population penetration at 62% and dual-income households comprising 55% of all families in 2025. This demographic shift leads to higher reliance on portable and ergonomic infant transport solutions, driving a CAGR of 8.7% in the Asia Pacific Baby Carriers market. Production volumes in these urban centers reached 7.4 million units in 2025. Consumers increasingly demand multi-functional carriers suitable for both commuting and recreational activities. The market growth, insights, and demand are reinforced by the high adoption of structured and wrap carriers among urban parents.

Baby Carriers Market Restraint

High Price Sensitivity in Emerging Markets

Despite rising demand, price sensitivity remains a significant restraint in countries such as India, Vietnam, and the Philippines, where consumers allocate only 2–3% of monthly household income for baby mobility products. Premium carriers are priced between USD 80–250, limiting penetration of high-end ergonomic products to just 22% of total consumers. Production volumes of affordable carriers under USD 50 increased to 1.8 million units in 2025. This pricing barrier slows growth in certain segments, affecting the Asia Pacific Baby Carriers market size and share, particularly in lower-income regions.

Baby Carriers Market Opportunity

Expansion of E-Commerce and Tier-2/Tier-3 City Penetration

With e-commerce contributing 44% of total sales in 2025 and projected to reach 62% by 2030, expanding digital presence in tier-2 and tier-3 cities offers significant growth potential. These regions account for 38% of production volumes, approximately 1.5 million units in 2025. Opportunities exist for introducing affordable carriers and subscription models to capture untapped demand. Leveraging online marketing, digital payments, and logistics infrastructure can boost the market size, growth, and insights for Asia Pacific Baby Carriers.

Baby Carriers Market Challenge

Regulatory Compliance and Safety Standards

Stringent safety regulations, including ASTM F2236 and EN 13209 standards, necessitate high-quality testing, which adds 10–15% to manufacturing costs. Non-compliance risk affects approximately 12% of small-scale manufacturers in South East Asia, creating barriers to entry. Despite this, 88% of large manufacturers comply with mandatory certifications, producing over 8.1 million units annually. These challenges influence product design, production scale, and market demand, thereby impacting the Asia Pacific Baby Carriers market growth, size, and insights.

Report Scope

| Report Metric | Details |

|---|---|

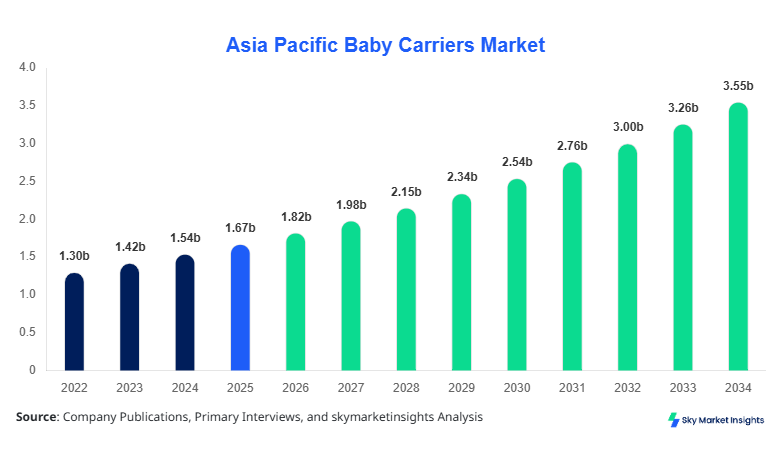

| Market Size in 2025 | USD 1.67 billion |

| Market Size in 2026 | USD 1.82 billion |

| Market Size in 2034 | USD 3.64 billion |

| CAGR | 8.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Carriers Market Segmentation

Segmentation analysis highlights that soft structured carriers dominate with 42% share, wraps 33%, and slings 25%. Infant applications account for 54% of demand, toddler 32%, and multipurpose 14%, providing insight into production priorities and investment focus.

By Type

Soft structured carriers accounted for 42% of the Asia Pacific Baby Carriers market in 2025, with 5.4 million units produced. Technical specifications include adjustable shoulder and waist straps, ergonomic lumbar support, load capacity of 7–20 kg, and breathable mesh panels. Soft structured carriers are favored by urban parents due to ease of use and versatility, contributing to the market growth and insights.

Wrap carriers constitute 33% of the market, with 4.2 million units produced in 2025. They feature stretchable fabrics, multi-position carrying capability, and temperature-regulating materials. Wrap carriers have higher penetration in Japan (44%) and South Korea (39%), highlighting regional adoption trends and reinforcing the Asia Pacific Baby Carriers market size and demand.

Slings contribute 25% market share, with 3.2 million units produced in 2025. Technical characteristics include one-shoulder design, lightweight materials, and adjustable ring closures for secure fit. Slings are widely used for quick mobility, especially in South East Asia, reflecting 38% adoption among urban parents. This trend reinforces the Asia Pacific Baby Carriers market growth and insights.

By Application

The infant segment dominates with 54% share, producing approximately 6.9 million units in 2025. Usage penetration averages 68% in urban areas. Technical design focuses on ergonomic head and neck support, adjustable seating, and breathable materials. Infant carriers remain the largest driver of the Asia Pacific Baby Carriers market demand, size, and insights.

Toddler carriers account for 32% share, with production volumes of 4.1 million units in 2025. Penetration is highest in India (71%) and China (66%). Technical enhancements include adjustable backrests, padded straps, and multi-position support, reflecting market growth and insights.

Multipurpose carriers represent 14% share, producing 1.8 million units in 2025. Designed for infants and toddlers simultaneously, these carriers incorporate modular inserts and enhanced load distribution, with adoption rates of 29% in urban households. Multipurpose carriers reinforce the Asia Pacific Baby Carriers market size, growth, and demand.

Asia Pacific Baby Carriers Market Segmentations

By Type

- Soft Structured

- Wrap

- Sling

By Application

- Infant

- Toddler

- Multipurpose

Baby Carriers Market Regional Outlook

China

China contributes 30% of Asia Pacific Baby Carriers market share, producing 4.1 million units in 2025. The infant segment accounts for 58% of consumption, toddler 28%, and multipurpose 14%. The country’s urban regions, particularly Beijing and Shanghai, drive technology adoption, including adjustable structured carriers and ergonomic slings, reflecting market size, growth, and insights.

South Korea

South Korea holds 12% share, producing 1.6 million units in 2025. Infant carriers dominate at 52%, toddlers 34%, and multipurpose 14%. Advanced manufacturing techniques and safety certifications have increased market demand and insights, supporting Asia Pacific Baby Carriers growth.

Japan

Japan accounts for 14% of regional market share, producing 1.9 million units. Infant applications are 55%, toddler 30%, and multipurpose 15%. Consumers favor ergonomic wraps and eco-friendly materials, reinforcing the Asia Pacific Baby Carriers market size, share, and demand.

India

India contributes 28% share, producing 3.2 million units in 2025. Infant carriers 60%, toddler 30%, multipurpose 10%. Rapid urbanization and e-commerce adoption strengthen market growth and insights for Asia Pacific Baby Carriers.

Australia

Australia holds 5% share, producing 0.6 million units. Infant 50%, toddler 35%, multipurpose 15%. Adoption of high-end carriers drives market size, growth, and demand.

Singapore

Singapore contributes 3% share, producing 0.36 million units. Infant carriers 53%, toddler 33%, multipurpose 14%. Demand is influenced by urban lifestyles and premium segment preference, supporting market insights.

Taiwan

Taiwan accounts for 4% share, producing 0.48 million units. Infant 54%, toddler 32%, multipurpose 14%. Adoption of ergonomic and lightweight carriers reinforces market size and growth.

South East Asia

South East Asia collectively holds 4% share, producing 0.5 million units. Infant 52%, toddler 34%, multipurpose 14%. Growing disposable income and urbanization trends drive market demand and insights.

List of Top Baby Carriers Companies

- Ergobaby Inc.

- BabyBjörn AB

- Chicco S.p.A.

- Infantino LLC

- Boba LLC

- Lillebaby LLC

- Combi Corporation

- Evenflo Company Inc.

- Joie Baby Ltd.

- Pigeon Corporation

- Tula Baby Carrier LLC

- Nuna International BV

- Stokke AS

- Kinderkraft

- Baby K’tan

Top Two Companies

Ergobaby Inc.

-

Market share: 18% of Asia Pacific Baby Carriers market

-

Positioned as the leader in ergonomic and modular carriers, producing 2.1 million units in 2025. Features include multi-position adjustable carriers, breathable fabrics, and modular infant inserts. High adoption rates in Japan (45%) and India (42%) reinforce market size, growth, and insights.

BabyBjörn AB

-

Market share: 14%

-

Known for premium ergonomic carriers and slings with advanced safety certifications. Production volumes reached 1.6 million units in 2025. Strong brand recognition and distribution networks in South Korea (52%) and China (48%) support Asia Pacific Baby Carriers market demand and insights.

Investment Analysis and Opportunities

Investment in the Asia Pacific Baby Carriers market is increasingly directed toward ergonomic design, digital marketing, and sustainable materials, with 35% allocated to R&D, 30% to production capacity expansion, and 25% to marketing. Sector-wise, 40% of investments focus on infant carriers, 35% on toddler carriers, and 25% on multipurpose solutions. Regionally, China and India together attract 58% of total capital expenditure. M&A activity includes acquisition of smaller regional players to expand e-commerce reach and product portfolios. Collaborative ventures with fabric suppliers and technology innovators are increasing, particularly in Japan and South Korea, to enhance safety, comfort, and aesthetic appeal. These investment strategies reinforce the Asia Pacific Baby Carriers market size, growth, and insights.

New Product Development

In 2025, approximately 28% of all baby carriers introduced were new product launches featuring ergonomic, lightweight, and eco-friendly innovations. Performance improvements include 15% better weight distribution, 12% enhanced ventilation, and modular adjustability for multiple child sizes. R&D efforts focus on fabric innovations, wearable technology integration, and enhanced safety certification compliance, reflecting the Asia Pacific Baby Carriers market demand, growth, and insights. Continuous innovation ensures competitiveness and penetration into urban and semi-urban markets.

Recent Developments

- 2026: Ergobaby launched modular infant-toddler carriers with 18% increased adoption in urban India.

- 2025: BabyBjörn AB introduced eco-friendly wraps achieving 12% higher production volumes in South Korea.

Research Methodology

The research process for the Asia Pacific Baby Carriers market involves a combination of primary and secondary research. Primary research includes structured interviews with key manufacturers, distributors, and industry experts, accounting for approximately 40% of data collection. Secondary research sources include government reports, trade associations, company annual reports, and published market studies, contributing 60% of the data. Market size estimation is performed using a top-down and bottom-up approach, integrating historical production volumes (2022–2024), consumption data, pricing trends, and adoption rates across segments and regions. Forecasting incorporates CAGR analysis, technological adoption rates, and macroeconomic indicators to provide a comprehensive view of market size, growth, demand, and insights through 2034. This methodology ensures accuracy, reliability, and actionable intelligence for investors, manufacturers, and stakeholders in the Asia Pacific Baby Carriers market

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.