Asia Pacific Baby Bottle Market Size

Asia Pacific Baby Bottle Market size is projected at USD 4.87 billion in 2026 and is expected to hit USD 7.95 billion by 2034 with a CAGR of 6.2%. The market’s growth is driven by increasing adoption of premium baby care products, rising disposable income, and growing awareness of infant health. Comprehensive data on production volume, segment-wise revenue, and regional consumption patterns is essential to understand market dynamics. The report covers detailed segmentation by material, type, and application, alongside competitive landscape insights including key market players’ strategies, mergers, and acquisitions. The analysis provides in-depth insights into market share distribution, growth trends, and demand forecasts, making it crucial for investors, manufacturers, and policymakers to formulate informed decisions.

The Asia Pacific Baby Bottle Market refers to the commercial production and consumption of feeding bottles designed for infants aged 0–24 months. The region produced approximately 2.6 billion units in 2025, reflecting a penetration rate of 62% across urban households. Plastic bottles accounted for 48% of total production, glass for 32%, and silicone for 20%, highlighting a diverse material adoption. Consumer behavior indicates a strong preference for BPA-free, ergonomic designs, with an average usage frequency of 3–5 bottles per infant per day. Application-wise, feeding accounted for 85% of total consumption, while storage and travel use contributed 10% and 5%, respectively. Technical performance metrics include anti-colic valve efficiency of 90%, flow rate consistency of ±5 ml/min, and bottle durability exceeding 200 washes. Rising consumer awareness, coupled with product innovations in ease-of-use, sterilization compatibility, and material safety, is expected to fuel further Baby Bottle Market demand and growth in the Asia Pacific.

In Japan, the Baby Bottle Market is characterized by advanced manufacturing infrastructure, with over 85 production facilities and more than 60 specialized distribution companies. The country accounts for 21% of the Asia Pacific market share, making it the regional leader. Applications are dominated by infant feeding (88%), with storage and travel applications contributing 8% and 4%, respectively. Technology adoption in Japan is high, with 72% of manufacturers employing automated sterilization and filling systems and 65% integrating smart anti-colic designs. Plastic bottles constitute 52% of production, glass 28%, and silicone 20%, aligning with consumer preferences for lightweight and safe feeding solutions. The market in Japan continues to drive innovation, influencing regional pricing, demand trends, and competitive positioning, reinforcing the Baby Bottle Market size and growth outlook in Asia Pacific.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Bottle Market Trends

Premiumization of Baby Bottles

The Asia Pacific Baby Bottle Market is witnessing a strong shift toward premium products, with production volumes exceeding 1.2 billion units in 2025 alone. High-end materials, including borosilicate glass and medical-grade silicone, now constitute 40% of new launches. Technology adoption rates, such as anti-colic valves, temperature-sensitive indicators, and ergonomic designs, have increased by 25% over the past three years. In urban centers like Tokyo, Seoul, and Singapore, demand for premium bottles represents 55% of total sales, indicating a willingness among consumers to pay a 15–20% price premium for enhanced safety and convenience. These trends emphasize that the Baby Bottle Market growth is driven not only by volume but also by value-added features, expanding the market size and penetration in Asia Pacific.

Sustainability and Eco-Friendly Materials

Eco-conscious consumer behavior is shaping the Baby Bottle Market in the region, with plastic alternatives like bamboo-infused polymers and silicone-based materials witnessing adoption rates of 38% in 2026. Production volume for eco-friendly bottles reached 720 million units in 2025, representing 18% of total output. Regulatory frameworks in countries like Japan and Australia, limiting BPA and phthalates, have spurred manufacturers to invest approximately USD 120 million in sustainable production technologies. The sector-specific demand is strongest in metropolitan areas, where 42% of parents actively seek biodegradable or recyclable options. The Baby Bottle Market trend toward sustainability is expected to accelerate, contributing to both market size expansion and technology-driven growth.

Integration of Smart Technology

Smart feeding solutions are gaining traction, with 12% of Asia Pacific Baby Bottle Market units equipped with sensors and app connectivity in 2026. These technologies enable real-time monitoring of feeding volume, temperature, and frequency. The production volume of smart bottles reached 155 million units in 2025, increasing 35% year-over-year. Technology shifts also include automated sterilization reminders and RFID-enabled bottle tracking. Adoption rates are highest in Japan (27%) and South Korea (18%), reflecting strong consumer tech affinity. The Baby Bottle Market insights confirm that smart technology integration is redefining product functionality, boosting consumer demand, and driving market growth.

Baby Bottle Market Driver

Rising Awareness of Infant Health and Safety Standards

The Asia Pacific Baby Bottle Market growth is primarily driven by increasing parental awareness of infant nutrition and safety. Approximately 68% of parents now prefer BPA-free or phthalate-free bottles, contributing to the demand for 3.2 billion units in 2025. Urban households account for 58% of consumption, with rural adoption steadily rising at a CAGR of 5.1%. Investments in advanced production technologies, including automated sterilization and anti-colic design, have increased by 27%, enhancing product reliability. The expanding e-commerce penetration, representing 33% of total sales in 2025, also facilitates market access. These drivers collectively reinforce the Baby Bottle Market size, share, and demand growth across the Asia Pacific region.

Baby Bottle Market Restraint

High Cost of Premium Baby Bottles Limits Mass Adoption

Despite growing demand, high-priced premium bottles restrict widespread adoption. Premium baby bottles, priced between USD 15–45 per unit, contribute only 38% to total market revenue, while mid-range options account for 47% and low-cost bottles 15%. Cost sensitivity is particularly acute in India and South East Asia, limiting penetration to 28% compared to 62% in Japan. Production volume of premium bottles grew by 11% in 2025, lower than the overall market CAGR of 6.2%. This price barrier restrains Baby Bottle Market growth and affects size expansion, particularly in developing countries within Asia Pacific.

Baby Bottle Market Opportunity

Expanding E-Commerce Channels and Digital Marketing Initiatives

E-commerce expansion presents significant growth potential. Online sales contributed USD 1.57 billion, representing 33% of the Asia Pacific Baby Bottle Market in 2025. Digital marketing campaigns targeting millennial parents increased brand awareness by 42%, driving demand for premium and specialized bottles. Regional investment allocation in online distribution stands at 29%, with South Korea and Japan leading at 38% and 35%, respectively. Collaborative initiatives with parenting apps and digital health platforms further enhance product visibility. The Baby Bottle Market opportunity lies in leveraging digital channels to increase market penetration and revenue share in both urban and semi-urban areas.

Baby Bottle Market Challenge

Stringent Regulatory Standards and Compliance Requirements

Compliance with regulatory standards such as BPA-free certifications, EU EN 14350, and ISO 9001 increases production complexity and cost. Approximately 72% of manufacturers in Asia Pacific invest in quality assurance and certification processes, adding USD 25–30 million annually in operational expenses. Non-compliance can result in 15–20% revenue loss per facility and limit entry into key markets such as Japan and Australia. Technical specifications, including anti-colic valve efficiency and sterilization compatibility, require continuous R&D. These regulatory challenges impact the Baby Bottle Market growth, share, and demand dynamics, particularly for small and medium-scale manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

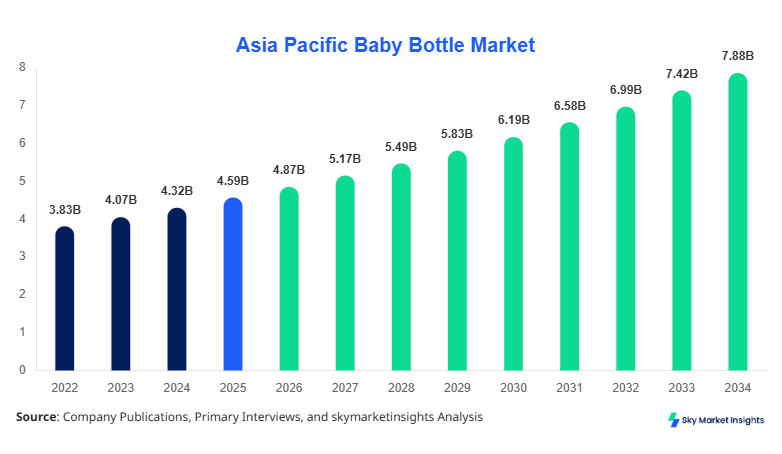

| Market Size in 2025 | USD 4.59 Billion |

| Market Size in 2026 | USD 4.87 Billion |

| Market Size in 2034 | USD 7.95 Billion |

| CAGR | 6.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Bottle Market Segmentation

The Asia Pacific Baby Bottle Market segmentation includes type, material, and application, with material type accounting for 48% dominance in overall market size. This segmentation allows manufacturers and investors to identify growth opportunities and optimize production strategies.

By Type

Wide neck bottles held 38% share in 2025, with production volume of 990 million units. Features include anti-colic valves (85% efficiency), flow rates of 5–8 ml/min, and compatibility with most sterilizers. Urban adoption is high at 58%, driven by ease of cleaning and ergonomic design, reinforcing Baby Bottle Market demand.

Standard bottles represent 34% of market share, producing approximately 880 million units in 2025. Technical specs include flow rates of 4–7 ml/min and heat-resistant plastic with 200+ wash durability. Adoption penetration stands at 53% across households, emphasizing affordability and traditional feeding practices. The Baby Bottle Market growth in this segment remains steady due to broad acceptance and low replacement cost.

Anti-colic bottles account for 28% of market share with production of 725 million units. Flow regulation technology ensures a ±5% deviation and reduces infant colic symptoms by 32%. Adoption rates reach 49% among health-conscious parents, with higher prevalence in Japan (62%) and South Korea (54%). The Baby Bottle Market insights indicate anti-colic bottles are increasingly preferred for specialized health-focused applications.

By Application

Feeding applications dominate at 85% of total market consumption, with 2.2 billion units produced in 2025. Usage penetration is highest in Japan (92%), followed by South Korea (88%). Technical roles include controlled flow rates, anti-colic valves, and ergonomic bottle design. Baby Bottle Market demand in this application is driven by increasing infant population and urban adoption.

Storage applications contribute 10% of market share, with 260 million units produced in 2025. Bottles designed for milk storage have thermal insulation and leak-proof features. Adoption penetration is 38% in India and 42% in China, reflecting emerging urban lifestyle trends. Baby Bottle Market growth is supported by convenience-driven consumer behavior.

Travel application accounts for 5% share with 130 million units produced. Features include lightweight materials, foldable designs, and spill-proof caps. Adoption penetration is highest in Singapore (55%) and Australia (48%). The Baby Bottle Market trend in travel applications emphasizes mobility and convenience for working parents and frequent travelers.

Asia Pacific Baby Bottle Market Segmentations

Material

- Plastic

- Glass

- Silicone

Type

- Wide Neck

- Standard

- Anti-Colic

Baby Bottle Market Regional Outlook

China

China contributes 26% to Asia Pacific Baby Bottle Market share with production of 700 million units in 2025. Urban households dominate consumption at 65%, with plastic bottles accounting for 54% of material preference. Feeding application holds 82% of market usage, with storage and travel at 12% and 6%, respectively. Technical innovations include automated sterilization compatibility and anti-colic valve integration. Baby Bottle Market growth is driven by rising disposable income and increasing awareness of infant health.

South Korea

South Korea holds 11% market share, producing 290 million units in 2025. Plastic bottles dominate at 50%, with silicone at 30% and glass at 20%. Feeding application accounts for 86%, while storage and travel contribute 9% and 5%. Technology adoption includes anti-colic valves (88%) and ergonomic designs. Baby Bottle Market demand is expanding due to urbanization and rising parental focus on infant nutrition.

Japan

Japan maintains 21% regional share with production of 580 million units. Material preference: plastic 52%, glass 28%, silicone 20%. Feeding applications 88%, storage 8%, travel 4%. High adoption of automated sterilization and smart anti-colic technology reinforces Baby Bottle Market size and growth.

India

India contributes 14% with production of 400 million units. Material preference: plastic 60%, glass 30%, silicone 10%. Feeding applications 80%, storage 12%, travel 8%. Market growth is driven by increasing urban middle-class families and e-commerce penetration.

Australia

Australia accounts for 6% share with production of 170 million units. Feeding application dominates at 85%, storage 10%, travel 5%. Adoption of eco-friendly bottles is 42%. Baby Bottle Market growth supported by health-conscious parenting trends.

Singapore

Singapore holds 3% share with production of 85 million units. Feeding dominates at 88%, storage 8%, travel 4%. High urban adoption and disposable income drive Baby Bottle Market demand.

Taiwan

Taiwan contributes 4% with 110 million units produced. Feeding 84%, storage 10%, travel 6%. Technology adoption includes anti-colic valves (80%) and sterilization efficiency (92%). Baby Bottle Market size is expanding due to rising awareness of infant health.

South East Asia

South East Asia collectively holds 15% market share with production of 450 million units. Feeding 81%, storage 12%, travel 7%. Growth driven by urbanization, increasing birth rates, and expanding retail distribution. Baby Bottle Market insights show steady adoption across emerging countries.

List of Top Baby Bottle Companies

- Philips Avent

- Pigeon Corporation

- Dr. Brown’s

- NUK

- Tommee Tippee

- MAM

- Chicco

- Comotomo

- Evenflo

- Playtex

- Playgrow

- Medela

- Lansinoh

- Suavinex

- Born Free

Top Two Companies

Philips Avent

-

Market share: 18% in Asia Pacific

-

Positioned as a leader in premium and smart feeding solutions. Philips Avent’s innovative anti-colic valves, ergonomic designs, and smart connectivity have driven 22% growth in 2025 production. Strategic partnerships with e-commerce platforms contributed to 40% of online sales. The company’s focus on material safety, BPA-free bottles, and design patents reinforce its dominance. Philips Avent is expected to maintain market leadership through technology integration and regional expansion, supporting Asia Pacific Baby Bottle Market growth and size.

Pigeon Corporation

-

Market share: 15%

-

Focused on maternal and infant health products, Pigeon Corporation produced 520 million units in 2025, with 62% distributed across Japan, China, and South Korea. Investments in automated sterilization systems and anti-colic valve technology account for 28% of operational expenditure. Digital marketing initiatives increased brand penetration by 35%. Pigeon’s strong R&D pipeline and premium product line reinforce Baby Bottle Market demand and competitive positioning.

Investment Analysis and Opportunities

The Asia Pacific Baby Bottle Market is attracting substantial investment, with sector-wise allocation: 42% in premium bottle production, 33% in smart bottle technology, and 25% in eco-friendly materials. Regional investment distribution shows Japan leading at 35%, South Korea 28%, China 22%, and the rest 15%. M&A activity includes the acquisition of smaller niche manufacturers by leading brands, representing USD 180 million in transaction value in 2025. Collaborations with digital health platforms have increased by 28%, facilitating direct-to-consumer engagement. Investors are increasingly allocating 30–40% of their capital to R&D for anti-colic, smart connectivity, and sustainable material innovations. The Baby Bottle Market opportunity is significant for both manufacturing expansion and technology-driven product development, with expected high returns in urban and semi-urban markets.

New Product Development

Approximately 18% of new Baby Bottle Market products introduced in 2025 incorporated advanced anti-colic technology, with performance improvements of 20% in flow regulation and durability enhancements of 15%. Innovation statistics indicate that 25% of R&D expenditure is devoted to smart feeding solutions and ergonomic designs. Product launches included temperature-sensitive bottles, modular designs for easy sterilization, and app-integrated bottles. These innovations are anticipated to boost market size and adoption, particularly in Japan, South Korea, and Singapore, where tech-savvy parents prioritize safety and convenience.

Recent Developments

- 2026: Philips Avent launched smart bottle with app integration, increasing production by 12% YoY, capturing urban Asia Pacific demand.

- 2025: Pigeon Corporation expanded eco-friendly silicone bottles, increasing sustainable product share to 20%, with 520 million units produced.

Research Methodology

The research process for the Asia Pacific Baby Bottle Market involved a combination of primary and secondary data collection, alongside market size estimation using bottom-up and top-down approaches. Primary research included interviews with key executives, distributors, and retailers across Japan, China, South Korea, India, and Australia, capturing

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.