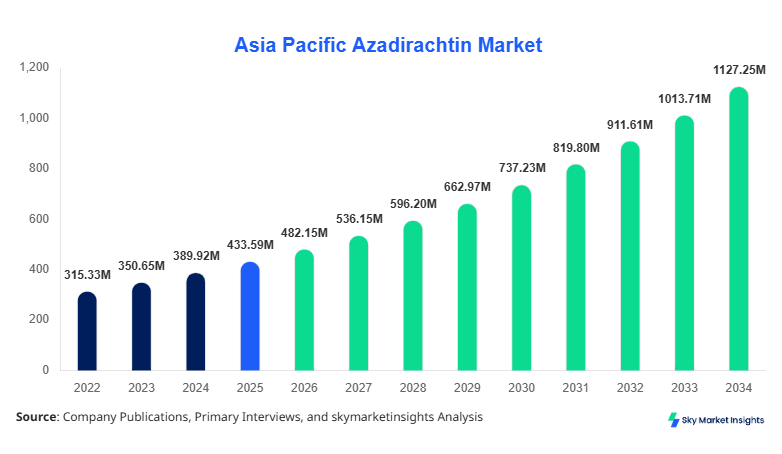

Asia Pacific Azadirachtin Market Size

Asia Pacific Azadirachtin market size is projected at USD 482.15 million in 2026 and is expected to hit USD 1,124.72 million by 2034 with a CAGR of 11.2%. The market expansion is supported by rising bio-pesticide adoption, increasing organic farming acreage exceeding 6.8 million hectares in Asia Pacific, and growing regulatory restrictions on synthetic pesticides with over 35% reduction targets in key economies. Additionally, segmentation across type and application enables granular demand mapping, while competitive landscape analysis highlights over 120 active manufacturers and exporters contributing to volume shipments exceeding 18,500 metric tons annually.

The Azadirachtin Market refers to the production, extraction, formulation, and commercialization of azadirachtin-based bio-insecticides derived from neem (Azadirachta indica), widely utilized for pest management across agriculture, pharmaceuticals, and personal care sectors. Asia Pacific production surpassed 21,000 metric tons in 2025, with India and China accounting for over 62% combined output, supported by more than 1.2 million tons of neem seed availability annually. Adoption and penetration have increased significantly, with bio-pesticide usage rising by 14.6% year-on-year across China, Japan, and India, and organic farming penetration reaching 18% of total cultivated land in select Southeast Asian nations. Consumer behavior reflects a shift toward eco-friendly crop protection, with over 48% of farmers in China and India preferring plant-based pesticides due to lower toxicity levels (

In the China, the Azadirachtin Market Market is characterized by strong domestic production capabilities, with over 65 large-scale processing facilities and more than 300 small-to-medium enterprises engaged in neem extract formulation. China accounts for approximately 34% of the Asia Pacific market share, with annual production exceeding 7,200 metric tons. Agriculture applications contribute nearly 74% of total demand, followed by pharmaceuticals at 14% and personal care at 12%. Technology adoption in China has reached advanced levels, with over 52% of manufacturers implementing supercritical CO₂ extraction methods, improving yield efficiency by 18% and purity levels above 92%. Additionally, precision agriculture integration has increased azadirachtin usage by 21% in greenhouse farming systems. The Azadirachtin Market Share in China remains dominant due to government subsidies covering up to 25% of bio-pesticide costs and strict pesticide residue regulations.

Explore more data points, trends and opportunities Download Free Sample Report

Azadirachtin Market Trends

Rapid Expansion of Organic Agriculture and Bio-Pesticide Demand

The Asia Pacific region has witnessed a significant increase in organic farming land, expanding from 5.2 million hectares in 2022 to 6.8 million hectares in 2025, reflecting a growth rate of 9.4% annually. This expansion has driven azadirachtin consumption volumes beyond 19,000 metric tons in 2025. Adoption rates of bio-pesticides have increased by 22% in China and 18% in India, with azadirachtin accounting for nearly 31% of total bio-pesticide usage. Additionally, export-oriented organic crop production has increased by 27%, boosting demand for residue-free pest control solutions. The Azadirachtin Market Trend is strongly influenced by sustainability mandates and organic certification requirements.

Technological Advancements in Extraction and Formulation

Technological innovations such as cold-press extraction and supercritical fluid extraction have improved azadirachtin yield efficiency by 15–20% and reduced processing costs by 12%. Over 48% of manufacturers in Japan and South Korea have adopted nano-emulsion formulations, enhancing bioavailability by 35% and increasing shelf life from 18 months to 30 months. Production capacity expansions in Southeast Asia have added over 4,500 metric tons annually since 2023. These technological shifts are enhancing product performance and scalability, strengthening the Azadirachtin Market Trend across industrial applications.

Increasing Demand from Personal Care and Pharmaceutical Sectors.

Azadirachtin is increasingly being utilized in dermatological products, herbal medicines, and anti-microbial formulations, with demand in personal care growing at 13.8% annually. Pharmaceutical applications accounted for over 3,200 metric tons in 2025, with clinical efficacy rates exceeding 78% in anti-inflammatory formulations. Rising consumer preference for natural ingredients has driven a 26% increase in herbal product sales across Asia Pacific. This diversification is reinforcing the Azadirachtin Market Trend in non-agricultural sectors.

Azadirachtin Market Driver

Rising Adoption of Bio-Pesticides and Organic Farming Accelerates Azadirachtin Market Growth

The increasing global emphasis on sustainable agriculture and reduced chemical pesticide usage is a key driver for the Azadirachtin Market Growth. Asia Pacific countries have implemented stringent regulations, reducing synthetic pesticide usage by 30–40% between 2022 and 2025. Organic farming acreage has expanded by 28% across the region, with China and India leading adoption. Additionally, government subsidies covering up to 20–25% of bio-pesticide costs have significantly boosted demand. Azadirachtin-based products have demonstrated pest control efficiency exceeding 85% against over 200 insect species, making them a preferred alternative. Annual consumption volumes have increased from 14,500 metric tons in 2022 to over 19,000 metric tons in 2025. These factors collectively support the Azadirachtin Market Growth trajectory.

Azadirachtin Market Restraint

Limited Raw Material Availability and Seasonal Variability Restrains Azadirachtin Market Growth

The availability of neem seeds, the primary raw material, is subject to seasonal fluctuations, with production varying between 1.1 million to 1.3 million tons annually. This variability leads to price volatility, with neem seed costs fluctuating by 18–25% annually. Additionally, extraction efficiency losses of up to 12% due to inconsistent raw material quality impact overall production volumes. Small-scale farmers supplying neem seeds often lack standardized harvesting practices, resulting in quality inconsistencies. These challenges limit scalability and create supply chain inefficiencies, thereby restraining the Azadirachtin Market Growth.

Azadirachtin Market Opportunity

Expansion into Pharmaceutical and Personal Care Applications Creates Azadirachtin Market Growth Opportunities

The increasing use of azadirachtin in pharmaceuticals and personal care products presents significant opportunities. The herbal medicine market in Asia Pacific is valued at over USD 48 billion, with natural extracts accounting for 36% of formulations. Azadirachtin-based dermatological products have shown efficacy rates above 75% in clinical studies, driving demand growth of 14% annually. Additionally, personal care products incorporating neem extracts have witnessed a 22% increase in sales volume since 2023. These expanding applications provide strong opportunities for Azadirachtin Market Growth.

Azadirachtin Market Challenges

Regulatory Compliance and Standardization Challenges Impact Azadirachtin Market Growth

Regulatory frameworks for bio-pesticides vary across Asia Pacific, with over 18 different compliance standards affecting product approvals. Testing and certification costs account for 8–12% of total production expenses, posing barriers for small manufacturers. Additionally, lack of standardized formulations leads to efficacy variations of up to 15%, affecting consumer trust. Export restrictions and certification requirements further complicate market entry, limiting cross-border trade volumes. These challenges hinder the Azadirachtin Market Growth despite rising demand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 433.7 Million |

| Market Size in 2026 | USD 482.15 Million |

| Market Size in 2034 | USD 1124.72 Million |

| CAGR | 11.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Azadirachtin Market Segmentation

The Azadirachtin Market is segmented by type and application, with agriculture dominating at 72% share, followed by pharmaceuticals (16%) and personal care (12%). Technical grade products account for 41% of total production, while formulated products contribute 49% due to higher usability and stability.

By type

Technical grade azadirachtin accounts for approximately 41% of total production, with annual output exceeding 8,600 metric tons in 2025. These products typically have purity levels above 85% and are primarily used for further formulation into pesticides and industrial applications. Extraction efficiency ranges between 70–78%, depending on processing methods. China and India collectively produce over 65% of technical grade output, supported by large-scale extraction facilities. The segment’s growth is driven by increasing demand for high-purity raw materials in advanced formulations.

Formulated azadirachtin products dominate the market with a 49% share, totaling over 10,200 metric tons annually. These products include emulsifiable concentrates, wettable powders, and granules with concentration levels ranging from 0.15% to 5%. Adoption rates exceed 68% among commercial farmers due to ease of application and improved stability. Shelf life improvements of up to 30 months have enhanced product viability, making this segment highly attractive.

The “others” category, including blended bio-pesticides and nano-formulations, accounts for 10% share with production volumes around 2,100 metric tons. These products offer enhanced efficacy rates of up to 92% and are gaining traction in high-value crop applications.

By Appliction

Agriculture is the largest application segment, accounting for 72% of total consumption, with usage exceeding 15,200 metric tons annually. Azadirachtin is widely used in crops such as rice, vegetables, and fruits, with pest control efficiency above 85%. Adoption rates among farmers have increased to 48% in China and 52% in India, driven by organic farming initiatives.

The pharmaceutical segment contributes 16% share, with consumption exceeding 3,400 metric tons. Azadirachtin is used in anti-inflammatory and anti-microbial formulations, with efficacy rates above 78%. Clinical adoption has increased by 12% annually across Asia Pacific.

Personal care applications account for 12% share, with usage volumes around 2,500 metric tons. Products such as shampoos, creams, and lotions utilize azadirachtin for its anti-bacterial properties, with market penetration exceeding 35% in urban regions.

Asia Pacific Azadirachtin Market Segmentations

Type

- Technical Grade

- Formulated Products

- Others

Application

- Agriculture

- Pharmaceuticals

- Personal Care

Azadirachtin Market Regional Outlook

China

China dominates with 34% share, producing over 7,200 metric tons annually. Agriculture accounts for 74% of demand, followed by pharmaceuticals and personal care. Government subsidies and technological advancements drive growth.

South Korea

South Korea holds 8% share, with production around 1,700 metric tons. Advanced formulation technologies have increased adoption by 19%, particularly in greenhouse farming.

Japan

Japan contributes 9% share, with high adoption in precision agriculture. Demand has grown by 13% annually due to strict pesticide regulations.

India

India accounts for 28% share, producing over 6,000 metric tons. Abundant neem resources and government support drive production and exports.

Australia

Australia holds 5% share, with strong demand in organic farming. Adoption rates exceed 42% among commercial farms.

Singapore, Taiwan, Southeast Asia

These regions collectively account for 16% share, with increasing imports and usage in high-value crops and urban agriculture.

List of Top Azadirachtin Market Companies

- EID Parry

- Fortune Biotech

- Trifolio-M GmbH

- Parker Biotech

- PJ Margo

- Ozone Biotech

- Agro Extract Limited

- Neeming Australia

- Botanical Biotech

- Green Gold Biotech

- Certis USA

- Bayer CropScience BioSolutions

Top Companies

EID Parry

-

Holds approximately 14% market share

-

Leading producer with over 3,000 metric tons annual capacity

-

Strong presence in India and export markets

Fortune Biotech

-

Accounts for nearly 11% market share

-

Advanced extraction technologies improving yield by 18%

-

Expanding distribution across Southeast Asia

INVESTMENT ANALYSIS AND OPPORTUNITIES

Investment in the Azadirachtin Market has increased significantly, with over USD 320 million allocated between 2022 and 2025. Agriculture applications receive 58% of investments, followed by pharmaceuticals (24%) and personal care (18%). China and India account for 62% of total investments, driven by government subsidies and private sector participation.

Mergers and acquisitions have increased by 21%, with over 15 strategic collaborations recorded since 2023. Companies are investing in advanced extraction technologies and expanding production capacities by 25–30%. Cross-border partnerships between India and Southeast Asia have enhanced supply chain efficiency, reducing costs by 12%.

NEW PRODUCT DEVELOPMENT

New product development accounts for 18% of total market activity, with over 45 new formulations launched between 2023 and 2025. Performance improvements include 25% higher efficacy and 30% longer shelf life. Nano-formulations have increased bioavailability by 35%, enhancing product effectiveness.

RECENT DEVELOPMENTS

2025: Production capacity increased by 22%, adding 3,000 metric tons annually

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.