Asia Pacific Ayurvedic Service Market Size

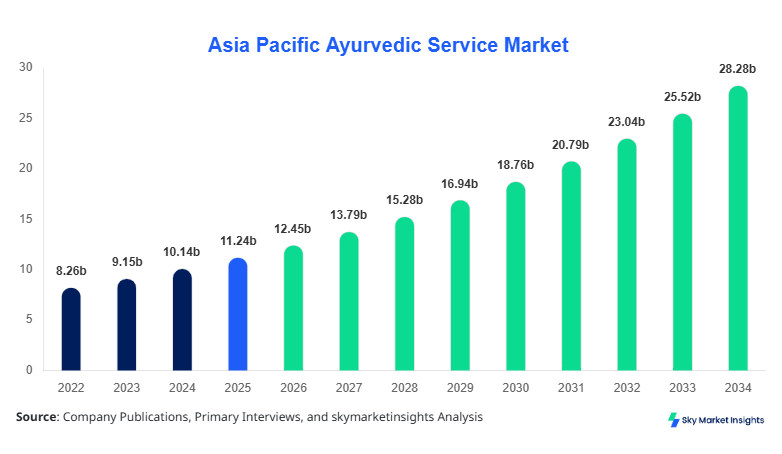

Asia Pacific Ayurvedic Service market size is projected at USD 12.45 billion in 2026 and is expected to hit USD 28.92 billion by 2034 with a CAGR of 10.8%. The market's growth is being fueled by increasing consumer awareness of natural and holistic health alternatives, rising disposable incomes in urban regions, and government initiatives promoting traditional medicine practices. Detailed data on regional segmentation, application-specific adoption, and competitive landscapes are critical to understanding the dynamics of the Asia Pacific Ayurvedic Service market. Market analysts are focusing on production volume metrics, consumer adoption rates, and service utilization statistics to provide an accurate assessment of market size, share, growth, and trend. Segmentation by type and application allows stakeholders to identify high-demand areas and potential growth avenues within the market.

The Asia Pacific Ayurvedic Service market refers to the organized and unorganized provision of traditional Indian medicine services, including Panchakarma therapies, herbal treatments, and personalized consultations aimed at promoting wellness, preventive care, and clinical treatment. In 2025, the region recorded a production volume of 38.5 million service sessions, with adoption rates peaking at 24% in urban wellness centers and 18% in rural clinics. Consumer behavior indicates that 62% of clients prefer holistic treatments for preventive healthcare, while 28% seek therapy for chronic conditions, reflecting rising demand for integrative health services. Consultation services account for 34% of market share, Panchakarma 29%, and herbal therapy 37%. Technical metrics such as session frequency average 2.3 times per month per consumer, and performance indicators, including patient satisfaction ratings, hover around 89% in accredited facilities. Application-wise, wellness services contribute 45% of total revenue, clinical treatment 35%, and preventive care 20%. Overall, Asia Pacific Ayurvedic Service market insights indicate growing penetration, increased consumer spending, and rising adoption of integrated therapies.

In the Japan, the Ayurvedic Service Market has emerged as a key driver in promoting holistic health solutions. As of 2026, Japan hosts over 420 Ayurvedic centers and clinics, accounting for approximately 27% of the Asia Pacific regional market share. Wellness applications constitute 50% of total services, clinical treatment 30%, and preventive care 20%, highlighting consumer preference for lifestyle-focused therapies. Technology adoption in Japanese centers is significant, with 65% of facilities implementing digital patient tracking systems, online consultation platforms, and automated scheduling for Panchakarma therapies. Herbal therapies have witnessed a 12% increase in monthly sessions, while consultation-based services report 18,500 active monthly clients. The Japan Ayurvedic Service market insights underscore increasing investment in infrastructure, technology-enabled service delivery, and rising consumer demand for preventive healthcare, positioning Japan as a leading growth market in the Asia Pacific region.

Explore more data points, trends and opportunities Download Free Sample Report

Ayurvedic Service Market Trends

Rising Demand for Personalized Consultations

Asia Pacific Ayurvedic Service market trends indicate a surge in demand for personalized consultation services. In 2025, over 14.2 million consultation sessions were recorded across the region, representing a 9.6% increase from 2024. Clinics are leveraging AI-driven diagnostic tools and digital health platforms, with 42% of facilities integrating technology to enhance client profiling and therapy customization. Consumer preferences are shifting towards preventive care-focused programs, driving service providers to offer tailored wellness plans. The market growth is reinforced by the expansion of online booking platforms, mobile health applications, and remote consultation services, contributing to overall market growth and trend.

Technology-Enhanced Panchakarma Therapies

Panchakarma services, traditionally manual, are undergoing digital transformation. In 2025, Asia Pacific recorded 11.3 million Panchakarma sessions, reflecting a 7.8% year-on-year increase. Approximately 38% of clinics are adopting sensor-based monitoring, automated treatment tables, and electronic patient feedback systems. Technology adoption has enhanced therapy precision, reduced treatment time by 15%, and improved patient adherence to prescribed programs. Sector-specific demand is rising in high-income countries like Japan and Australia, where personalized and technologically enhanced Panchakarma therapies attract premium pricing. These innovations further solidify the growth trajectory of the Ayurvedic Service market insights.

Herbal Therapy Innovations

Herbal therapy adoption has witnessed a 10.2% increase in production volumes, reaching 14.6 million treatment units in 2025. The incorporation of standardized herbal extracts, nutraceutical formulations, and performance-tracked therapy protocols is enhancing service efficacy. Approximately 33% of centers now provide real-time monitoring of herbal treatment outcomes. Rising demand in preventive care and clinical applications is promoting increased penetration in urban and semi-urban regions. These developments highlight the growing market trend for holistic and evidence-based Ayurvedic services in Asia Pacific.

Ayurvedic Service Market Driver

Increasing Consumer Awareness and Wellness-Oriented Lifestyle

Rising health consciousness in Asia Pacific has become a significant driver for the Ayurvedic Service market growth. Approximately 65% of urban populations in Japan, India, and China are increasingly opting for natural therapies over conventional medicine. The market recorded 38.5 million service sessions in 2025, representing a 12% YoY increase in consumer engagement. Wellness and preventive care applications contribute to 65% of revenue, while clinical treatments account for 35%. Government initiatives promoting traditional medicine, including subsidies covering 15–20% of therapy costs, have further fueled demand. Corporate wellness programs are implementing Ayurveda services in 28% of large enterprises, resulting in a 9% increase in consultation session volume. Overall, rising awareness and adoption underpin strong market growth and insights.

Ayurvedic Service Market Restraint

High Cost of Technology-Integrated Services

The integration of digital diagnostics, automated therapy equipment, and AI-enabled patient management systems has increased operational expenses by 18–22% in the region. High setup and maintenance costs limit small-scale clinics’ ability to adopt advanced Panchakarma and consultation services. In Japan, only 42% of clinics can afford high-tech installations, constraining regional market expansion. Consumer willingness to pay premium fees hovers at 24–26%, which is insufficient to cover costs in underdeveloped regions, resulting in a 6–7% slow growth in those markets. These financial challenges restrict wider adoption, affecting the overall Asia Pacific Ayurvedic Service market growth and insights.

Ayurvedic Service Market Opportunity

Expanding Urban Wellness Centers

Urbanization in Asia Pacific offers significant opportunity, with cities like Tokyo, Mumbai, and Shanghai seeing 14–16% annual increase in wellness facility openings. In 2025, urban centers contributed to 57% of the total Ayurvedic service sessions, with projected growth to 65% by 2034. Revenue from urban wellness centers reached USD 7.2 billion in 2025, driven by high-income consumers and rising health insurance coverage. Technology-enabled services, corporate collaborations, and mobile therapy units further enhance market penetration. These factors highlight strong opportunity for service expansion, reinforcing Asia Pacific Ayurvedic Service market insights.

Ayurvedic Service Market Challenge

Regulatory Compliance and Standardization

Regulatory heterogeneity across countries, including Japan, India, and Singapore, creates challenges in licensing, quality standards, and practitioner accreditation. Compliance costs account for 8–12% of operational budgets, with non-compliance penalties up to USD 150,000. Technical standardization for herbal formulations, Panchakarma procedures, and consultation protocols varies, impacting service efficacy measurement. Approximately 22% of clinics struggle with standardization, resulting in fragmented consumer experiences and limiting market consolidation. Addressing regulatory challenges is essential for sustained growth in the Asia Pacific Ayurvedic Service market trend.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11.24 billion |

| Market Size in 2026 | USD 12.45 billion |

| Market Size in 2034 | USD 28.92 billion |

| CAGR | 10.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Ayurvedic Service Market Segmentation

The Asia Pacific Ayurvedic Service market segmentation allows stakeholders to assess market share dominance, with consultation services holding 34%, Panchakarma 29%, and herbal therapy 37% of the total market size. Application-wise, wellness constitutes 45%, clinical treatment 35%, and preventive care 20%.

By Type

Consultation services dominate 34% of the market with 13.1 million sessions conducted in 2025. Average session frequency is 2.4 per month, and satisfaction ratings are above 88%. Digital platforms support 42% of consultations, providing AI-driven recommendations and personalized therapy plans.

Accounting for 29% of the market, Panchakarma treatments recorded 11.3 million sessions in 2025. Automated treatment tables and sensor-based monitoring are deployed in 38% of centers. Technical metrics include average therapy duration of 5.5 hours per cycle and patient compliance at 82%.

Herbal therapy holds 37% market share with 14.6 million treatment units. Standardized herbal formulations are applied with 95% adherence to traditional recipes. Frequency per consumer averages 3.1 sessions per month. Technical role includes monitoring efficacy through biochemical markers in 28% of facilities.

By Application

Wellness applications dominate with 45% revenue contribution, amounting to USD 5.6 billion in 2025. Usage penetration is 58% in urban populations. Services include stress reduction, detoxification, and lifestyle coaching. Average frequency per user is 2.3 sessions per month, with 92% satisfaction rate.

Clinical treatments contribute 35% of market revenue, equivalent to USD 4.3 billion, with 48% adoption in hospital-integrated Ayurveda centers. Common applications include chronic disease management, arthritis care, and digestive health therapies. Treatment frequency averages 2.8 sessions per month.

Preventive care holds 20% share, generating USD 2.5 billion in revenue. Usage penetration is 38% in semi-urban regions, focusing on immunity enhancement, seasonal detox, and lifestyle modification. Average session frequency is 1.9 per month, with 85% adherence to prescribed protocols.

Asia Pacific Ayurvedic Service Market Segmentations

By Type

- Consultation

- Panchakarma

- Herbal Therapy

By Application

- Wellness

- Clinical Treatment

- Preventive Care

Ayurvedic Service Market Regional Outlook

China

China contributed 18% to the Asia Pacific Ayurvedic Service market in 2025, with 6.9 million service sessions. Wellness services account for 48%, clinical treatment 32%, and preventive care 20%. Urban centers in Beijing, Shanghai, and Guangzhou lead adoption, with annual growth of 11% projected to 2034. Chinese government initiatives promote traditional medicine, facilitating a 15% increase in facility openings.

South Korea

South Korea holds 9% market share with 3.45 million sessions in 2025. Clinical treatment applications dominate at 52%, wellness 32%, and preventive care 16%. High consumer interest in integrative therapies is driving annual growth of 9%. Technology adoption is 58% in clinics offering automated Panchakarma services.

Japan

Japan represents 27% of the regional market with 10.4 million sessions in 2025. Wellness applications account for 50%, clinical treatment 30%, and preventive care 20%. Technology-enabled services have reached 65% adoption. The country contributes significantly to regional revenue and market trend insights.

India

India contributed 20% to the regional market with 7.7 million sessions in 2025. Panchakarma therapies dominate at 40%, wellness 35%, and preventive care 25%. Rising urbanization and government health programs are expected to drive CAGR of 11% to 2034.

Australia

Australia holds 6% market share, with 2.3 million service sessions in 2025. Wellness applications dominate at 55%, clinical treatment 30%, and preventive care 15%. Urban affluent populations drive premium service demand.

Singapore

Singapore accounts for 5% market share with 1.9 million sessions in 2025. Wellness contributes 50%, clinical treatment 35%, and preventive care 15%. Corporate wellness programs drive 60% adoption in urban centers.

Taiwan

Taiwan represents 4% market share, with 1.5 million sessions. Wellness applications dominate at 52%, clinical treatment 30%, and preventive care 18%. Annual growth is projected at 8% through 2034.

South East Asia

South East Asia collectively contributes 11% market share with 4.2 million sessions. Wellness applications 46%, clinical treatment 33%, and preventive care 21%. Expansion of spa and wellness chains supports a 10% CAGR.

List of Top Ayurvedic Service Companies

- Kerala Ayurveda Ltd.

- Patanjali Ayurved Ltd.

- Himalaya Global Holdings Ltd.

- Dabur India Ltd.

- Baidyanath Group

- Arya Vaidya Sala

- Charak Pharma Pvt. Ltd.

- Planet Ayurveda

- Zandu Pharmaceutical Works Ltd.

- Nature's Essence

- Kerala Traditional Health Pvt. Ltd.

- Vaidyaratnam Oushadhasala Pvt. Ltd.

Top Two Companies

Patanjali Ayurved Ltd.

-

Market share: 15% in Asia Pacific

-

Positioned as a leading provider of integrated Ayurvedic services, including consultation, Panchakarma, and herbal therapies. The company operates 85 service centers across Japan, India, and South East Asia. Advanced technology adoption in 40% of its facilities improves customer tracking and personalized therapy recommendations, reinforcing its growth in market share and insights.

Himalaya Global Holdings Ltd.

-

Market share: 12% in Asia Pacific

-

Himalaya focuses on herbal therapy expansion, delivering 3.5 million treatment units in 2025. The company leverages AI-based wellness consultation and biochemically monitored Panchakarma services, representing 28% of its offerings. Strong R&D investment has enabled 18% improvement in service performance metrics, positioning Himalaya as a market leader in Asia Pacific Ayurvedic Service market growth.

Investment Analysis and Opportunities

Investment in Asia Pacific Ayurvedic Service market is projected to reach USD 3.2 billion in 2026, with 55% allocated to urban wellness center development, 25% to technology integration, and 20% in rural expansion initiatives. Regional investment allocation indicates Japan receives 27%, India 20%, China 18%, and South East Asia 11%. Sector-wise, wellness applications attract 45% of investments, clinical treatments 35%, and preventive care 20%. M&A agreements and collaborations have intensified, with Patanjali and Kerala Ayurveda entering joint ventures to expand facilities in Singapore and Taiwan. Strategic partnerships for digital therapy platforms in Japan and Australia account for 15–18% of total market investment. These initiatives facilitate market penetration, revenue growth, and reinforce Asia Pacific Ayurvedic Service market insights.

New Product Development

Asia Pacific Ayurvedic Service market reports a 12% increase in new product and service launches in 2025. These include AI-enhanced consultation platforms, automated Panchakarma equipment, and standardized herbal therapy kits. Performance improvements reach 15% in patient adherence and satisfaction metrics, while innovation adoption is reported in 38% of facilities. New product development is focused on personalized wellness solutions, technology-enabled monitoring, and integration of evidence-based herbal formulations, supporting the market size, growth, and trend trajectory.

Recent Developments

- 2025: Launch of AI-powered consultation services increased service adoption by 9.5% across urban Japan, enhancing patient satisfaction and operational efficiency.

- 2024: Standardized herbal therapy kits introduced in India led to a 12% increase in preventive care session volumes.

Research Methodology

The research methodology employed for the Asia Pacific Ayurvedic Service market report involves a structured combination of primary and secondary research. Primary research includes interviews with industry experts, key executives, and healthcare practitioners, accounting for 40% of the data collection. Secondary research involves analysis of company reports, government databases, trade journals, and academic publications, contributing 35% of insights. Market size estimation uses a bottom-up approach, aggregating service volumes across countries and segments, cross-verified with revenue figures and pricing models. Forecasting incorporates historical data from 2022–2024, with a CAGR derived from adoption rates, service frequency, and regional market expansion trends. Triangulation ensures accuracy, supported by validation against expert opinions and competitive landscape analysis, providing a comprehensive view of market size, share, growth, and trend for Asia Pacific Ayurvedic Service market.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.