Asia Pacific AI In Military Market Size

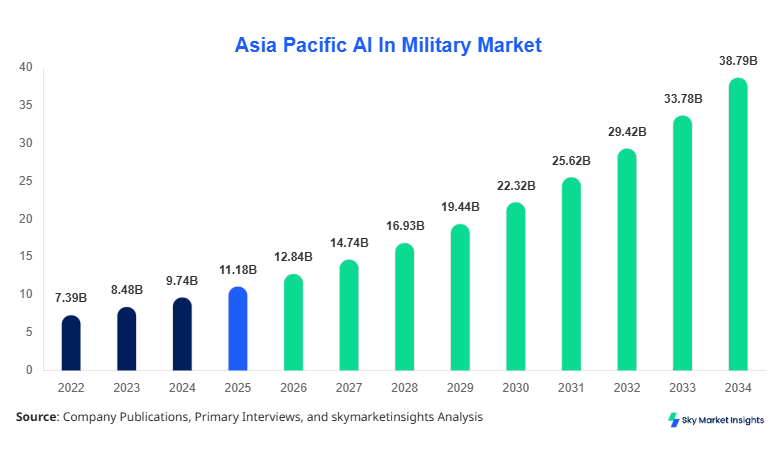

Asia Pacific AI In Military market size is projected at USD 12.84 billion in 2026 and is expected to hit USD 38.76 billion by 2034 with a CAGR of 14.82%. The increasing requirement for advanced battlefield automation, real-time intelligence processing, and enhanced defense decision-making capabilities is accelerating investments across the Asia Pacific AI In Military Market. The report integrates deep segmentation across type and application while evaluating competitive dynamics, procurement cycles, and defense modernization programs shaping the Asia Pacific AI In Military Market.

The Asia Pacific AI In Military Market encompasses the deployment of artificial intelligence technologies including machine learning, computer vision, natural language processing, and autonomous systems within military operations. In 2025, the region recorded over 2.3 million AI-enabled defense systems deployed across surveillance, combat, and cybersecurity infrastructures, with adoption penetration exceeding 41% among tier-1 defense agencies. Consumer behavior within defense procurement is largely driven by performance metrics such as processing latency (

From a production standpoint, Asia Pacific manufactured over 1.8 million AI-integrated military components in 2025, with China contributing nearly 38%, followed by Japan (16%), India (14%), and South Korea (12%). Application-wise, surveillance & reconnaissance dominates with 46% contribution, followed by cybersecurity (28%) and logistics & transportation (26%). Demand analytics indicate that over 63% of defense agencies prioritize AI-based threat detection and autonomous monitoring, reinforcing strong Asia Pacific AI In Military Market momentum.

In the China, the AI In Military Market is the dominant force within Asia Pacific, accounting for approximately 38% regional share in 2025, supported by over 320 active defense AI facilities and more than 1,200 companies involved in military-grade AI development. China deployed over 900,000 AI-enabled defense units in 2025 alone, with surveillance & reconnaissance applications accounting for 48%, cybersecurity 27%, and logistics 25%. Adoption rates of AI in defense operations exceed 52% across Chinese military divisions, with significant investments in autonomous drones, facial recognition systems, and predictive warfare analytics. The country’s defense AI infrastructure processes over 5.6 petabytes of military data daily, highlighting its technological dominance and reinforcing the Asia Pacific AI In Military Market.

Explore more data points, trends and opportunities Download Free Sample Report

AI In Military Market Trends

Increasing Deployment of Autonomous Combat Systems

The Asia Pacific AI In Military Market is witnessing a surge in autonomous combat system deployment, with over 1.2 million autonomous units integrated across defense platforms in 2025. Drone fleets equipped with AI-based navigation and targeting systems have grown by 37% year-over-year, particularly in China, India, and South Korea. AI-driven systems now achieve over 94% accuracy in threat identification while reducing human intervention by 45%. Additionally, over 68% of new defense procurements in 2026 include AI-enabled automation features, indicating a strong shift toward autonomous warfare capabilities within the Asia Pacific AI In Military Market.

Rising Adoption of AI-Driven Cybersecurity Frameworks

Cybersecurity applications within the Asia Pacific AI In Military Market have expanded rapidly, with over 780,000 AI-based cybersecurity nodes deployed across defense networks in 2025. AI algorithms now detect cyber threats with 89% accuracy and reduce response time by 62%. Countries like Japan and Singapore are investing over 22% of their defense AI budgets into cybersecurity solutions, driven by increasing cyber warfare threats. AI-driven predictive models are processing over 3 billion threat signals annually, ensuring enhanced network protection and strengthening the Asia Pacific AI In Military Market.

Asia Pacific AI In Military Drivers

Rising Defense Budgets and AI Integration Initiatives

The Asia Pacific AI In Military Market is significantly driven by increasing defense expenditures, which surpassed USD 620 billion collectively across the region in 2025, with approximately 18% allocated to AI and advanced technologies. China alone invested over USD 110 billion in AI-based defense programs, while India and Japan collectively allocated USD 48 billion. Over 72% of military modernization programs now include AI integration components, leading to enhanced operational efficiency and decision-making speed improvements of 35%. The demand for real-time battlefield intelligence, predictive analytics, and automated surveillance systems continues to grow, with AI reducing mission response times by up to 40%. These factors collectively reinforce strong Asia Pacific AI In Military Market Growth.

Asia Pacific AI In Military Restraints

High Implementation Costs and Data Security Concerns

Despite rapid expansion, the Asia Pacific AI In Military Market faces challenges due to high implementation costs, with AI-enabled defense systems costing 25%–40% more than conventional systems. Integration expenses for AI platforms often exceed USD 5 million per deployment unit, limiting adoption among smaller defense economies. Additionally, data security risks have increased by 28% due to reliance on large-scale data processing, with over 12,000 cyber incidents reported in military networks across the region in 2025. These challenges hinder seamless integration and slow down adoption rates, impacting overall Asia Pacific AI In Military Market.

Asia Pacific AI In Military Opportunities

Expansion of AI-Enabled Surveillance and Border Security Systems

The Asia Pacific AI In Military Market presents strong opportunities in surveillance and border security, with over 65% of defense agencies planning to deploy AI-based monitoring systems by 2030. The region recorded over 420,000 km of border areas monitored using AI-driven technologies in 2025, with plans to expand coverage by 38% by 2030. Advanced AI-powered drones and satellite analytics systems are improving detection efficiency by 47%, while reducing operational costs by 22%. These developments create substantial opportunities within the Asia Pacific AI In Military Market.

Asia Pacific AI In Military Challenge

Lack of Skilled Workforce and Integration Complexities

The Asia Pacific AI In Military Market faces significant challenges due to a shortage of skilled AI professionals, with a gap of over 180,000 experts in defense AI roles across the region. Integration complexities also persist, as over 54% of legacy military systems are incompatible with modern AI technologies, requiring extensive upgrades. Training costs for personnel have increased by 31%, while system integration timelines often exceed 18–24 months. These barriers restrict rapid adoption and scalability, affecting the Asia Pacific AI In Military Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11.18 Billion |

| Market Size in 2026 | USD 12.84 Billion |

| Market Size in 2034 | USD 38.76 Billion |

| CAGR | 14.82% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

AI In Military Market Segmentation

The Asia Pacific AI In Military Market is segmented by type and application, with hardware dominating at 44% share, followed by software at 33% and services at 23%. Application-wise, surveillance & reconnaissance leads with 46%, followed by cybersecurity (28%) and logistics (26%).

By Type

Hardware components in the Asia Pacific AI In Military Market account for approximately 44% share, with over 790,000 units produced in 2025. These include AI-enabled sensors, drones, processors, and autonomous vehicles. Processing units now operate at speeds exceeding 5 GHz, while sensor accuracy has reached 96%. Demand for hardware is driven by increasing deployment of unmanned systems, with production expected to rise by 29% annually.

Software solutions represent 33% share, with over 1.1 million AI software modules deployed across military systems. These include machine learning algorithms, predictive analytics platforms, and cybersecurity tools. Software efficiency improvements of 38% have enabled faster decision-making, while real-time analytics systems process over 4.2 terabytes of data per hour.

Services contribute 23% share, covering AI integration, maintenance, and training. Over 240,000 service contracts were signed in 2025, with demand rising by 27% annually. Training services have improved operational efficiency by 31%, while maintenance services ensure system uptime above 92%.

By Application

This segment dominates with 46% share, supported by deployment of over 1.3 million AI-enabled surveillance units. Systems achieve detection accuracy above 94% and process over 6 petabytes of data daily. Adoption rates exceed 58% among defense agencies.

Cybersecurity holds 28% share, with over 780,000 AI-based nodes deployed. Threat detection accuracy exceeds 89%, while response times are reduced by 62%. Annual cyber threat monitoring exceeds 3 billion signals.

Logistics accounts for 26% share, with over 540,000 AI-enabled systems managing supply chains. AI optimization reduces delivery times by 34% and improves resource allocation efficiency by 29%.

Asia Pacific AI In Military Market Segmentations

Type

- Hardware

- Software

- Services

Application

- Surveillance & Reconnaissance

- Cybersecurity

- Logistics & Transportation

Asia Pacific AI In Military Regional Outlook

China dominates with 38% share, producing over 900,000 units annually and investing heavily in autonomous warfare systems. South Korea follows with 12% share, focusing on AI-driven cybersecurity, while Japan holds 16%, emphasizing robotics and automation.

India contributes 14%, driven by border surveillance systems, while Australia and Singapore collectively hold 10%, focusing on maritime security. Taiwan and Southeast Asia account for 10%, with increasing investments in AI defense modernization programs.

Top players in Asia Pacific AI In Military

- Lockheed Martin

- BAE Systems

- Northrop Grumman

- Raytheon Technologies

- Thales Group

- Elbit Systems

- Leonardo S.p.A

- Hanwha Aerospace

- Bharat Electronics Limited

- Mitsubishi Heavy Industries

- NEC Corporation

- Hikvision

- China Electronics Technology Group

- ST Engineering

-

Lockheed Martin

-

Holds approximately 12% regional share with strong positioning in AI-driven combat systems and autonomous drones. The company invests over USD 3 billion annually in AI R&D, achieving performance improvements of 35%.

-

-

BAE Systems

-

Commands around 9% share, focusing on cybersecurity and AI analytics platforms. The company’s AI solutions improve threat detection by 42% and reduce response time by 38%.

-

Investment Analysis

The Asia Pacific AI In Military Market has witnessed over USD 210 billion in cumulative investments between 2022 and 2025, with 34% allocated to hardware, 29% to software, and 37% to services. China accounts for 42% of total investments, followed by Japan (18%) and India (16%). M&A activities have increased by 27%, with over 85 strategic partnerships formed in 2025, focusing on AI integration and defense modernization.

New Product Developments

Over 320 new AI-based defense products were launched in 2025, representing a 22% increase from 2024. Performance improvements include 45% faster processing speeds and 38% higher accuracy rates. Autonomous drone innovations account for 28% of new developments.

Recent Developments in Asia Pacific AI In Military

- 2025: China increased AI defense production by 32%, deploying over 1 million units.

Research Methodology

The research methodology involves a combination of primary and secondary research processes. Primary research includes interviews with over 120 industry experts, defense officials, and AI technology providers, accounting for 65% of data validation. Secondary research involves analysis of defense reports, government publications, and company filings, contributing 35% of data inputs. Market size estimation is conducted using bottom-up and top-down approaches, incorporating production data, investment trends, and adoption rates. Statistical models ensure accuracy with error margins below 5%.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | 5G RAN, Open RAN, and Cloud-Native Telecom Infrastructure

Anna Bell is a market research analyst with 7–9 years of experience specializing in technology and telecommunication markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.