Middle East and Africa Bagels Market Size

The Middle East and Africa bagel market size is projected at USD 1.42 billion in 2026 and is expected to hit USD 2.95 billion by 2034 with a CAGR of 9.2%. The market’s expansion is fueled by rising consumer preference for convenience foods, increasing bakery chains, and a surge in retail and foodservice adoption. Detailed segmentation, historical data from 2022–2024, and competitive landscape insights are critical for stakeholders seeking to identify growth patterns, regional dominance, and technology adoption. Analysis of production, consumption, and pricing trends further enhances strategic planning and investment evaluation in the bagel market.

The Middle East and Africa bagel market has witnessed steady growth, with production volumes estimated at 350 million units in 2025, marking a 7.8% rise from 2024. Adoption of frozen and pre-packaged bagels has increased penetration in urban households to 42%, while retail chains contribute 55% of sales. Consumer behavior analysis indicates a shift toward healthier options, with whole wheat and multigrain variants representing 28% and 17% of the market, respectively. Technical metrics such as shelf-life extension (up to 21 days) and improved baking frequency (4–5 cycles per week in commercial bakeries) support widespread distribution. The application split shows retail at 58%, food service at 30%, and home consumption at 12%, highlighting a balanced market with growing demand. These insights reinforce the bagel market's growth trajectory and demand potential.

In the UAE, the bagel market has become a focal point for bakery expansion and consumer-driven demand. Approximately 120 commercial bakeries and 45 specialized bagel producers contribute to the market, representing 18% of the Middle East and Africa regional share. Retail applications account for 60% of consumption, while food service contributes 32%, and home consumption remains at 8%. Adoption of automated baking technology is at 65%, supporting uniformity and volume production exceeding 50 million units annually. With a rising preference for health-oriented bagels, whole wheat and multigrain variants capture 35% of sales. These dynamics underscore the UAE’s pivotal role in Bagels Market growth, with significant technological adoption enhancing size and share metrics.

Explore more data points, trends and opportunities Download Free Sample Report

Bagels Market Trends

Rise in Pre-Packaged and Frozen Bagels

Middle East and Africa bagel market trends show a substantial increase in pre-packaged and frozen bagel consumption, with production reaching 400 million units in 2026. Technological shifts in packaging and refrigeration have led to 72% adoption of frozen formats in retail and foodservice segments. Retail chains, representing 60% of the market, report annual growth rates exceeding 8%, while food service applications account for 30% of increased demand. Consumer preference for convenience and longer shelf life drives innovation in ready-to-eat variants, strengthening the bagel market's growth.

Health-Conscious Consumer Adoption

Demand for healthier bagel options, such as whole wheat and multigrain, is rapidly rising, capturing 45% of total market share by 2026. Production volumes of multigrain bagels increased from 42 million units in 2024 to 75 million units in 2026. Sugar reduction, high-fiber formulations, and fortified ingredients are being integrated into 68% of newly launched products. These trends indicate a shift in dietary habits and reinforce bagel market demand across the Middle East and Africa.

Expansion of Foodservice Channels

The foodservice segment demonstrates strong growth with a 32% share of the bagel market, driven by cafes, hotels, and corporate cafeterias. Annual volume production for foodservice channels reached 120 million units in 2026. Technology adoption, including high-efficiency ovens and automated dough dividers, has risen by 58%, enabling large-scale production and faster service. The growing presence of international chains enhances Bagels' market share and stimulates regional consumption.

Middle East and Africa Bagels Market Drivers

Rising Urbanization and Convenience Food Demand

Rapid urbanization across the Middle East and Africa has led to increased bakery consumption, with the bagel market size in urban areas projected to reach USD 950 million by 2026. Demand for convenience foods has grown by 12% annually, particularly in the UAE and Saudi Arabia, where households purchase an average of 6–8 bagels per week. Retail expansion contributes 58% of total sales, while foodservice adoption accounts for 33%. Technological investments in automated ovens and high-speed mixers (adopted by 62% of bakeries) enhance production volumes exceeding 1.2 billion units regionally. These drivers support bagel market growth and provide actionable insights for stakeholders.

Middle East and Africa Bagels Market Restraints

High Raw Material Costs and Price Sensitivity

The bagel market in the Middle East and Africa faces challenges due to fluctuating wheat prices and supply chain constraints. Raw material costs have increased by 15% between 2024 and 2026, impacting small-scale bakeries and lowering profit margins. Consumer price sensitivity restricts volume sales growth, particularly in Egypt and Nigeria, where retail price fluctuations of 5–7% influence purchase frequency. Approximately 40% of bakeries report decreased production due to high ingredient costs, slowing bagel market expansion despite growing demand in premium segments. These factors limit size and share potential across price-sensitive regions.

Middle East and Africa Bagels Market Opportunities

Emerging Bakery Chains and Retail Expansion

Emerging bakery chains and the proliferation of hypermarkets present significant opportunities in the bagel market. Investment in retail outlets increased by 22% in 2025, and projected volumes indicate a growth of 150 million units in the next five years. Technology-enabled operations, including automated ovens and dough mixers, are adopted by 55% of new entrants. Expanding consumer base, particularly in the UAE, Turkey, and South Africa, contributes to 65% of projected market share. These developments highlight the bagel market's demand potential and strategic growth avenues.

Challenges in Middle East and Africa Bagels Market

Regulatory and Logistical Barriers

The Bagel Market encounters regulatory compliance hurdles and logistical inefficiencies in cross-border distribution. Import restrictions, labeling regulations, and high freight costs impact 28% of shipments across regional markets. Cold chain logistics adoption is at 48%, limiting frozen bagel distribution to urban centers. Small-scale producers in Nigeria and Egypt struggle with compliance costs, reducing production volume by 12%. These challenges constrain market growth and reinforce the need for innovation to enhance the bagel market size and share.

Report Scope

| Report Metric | Details |

|---|---|

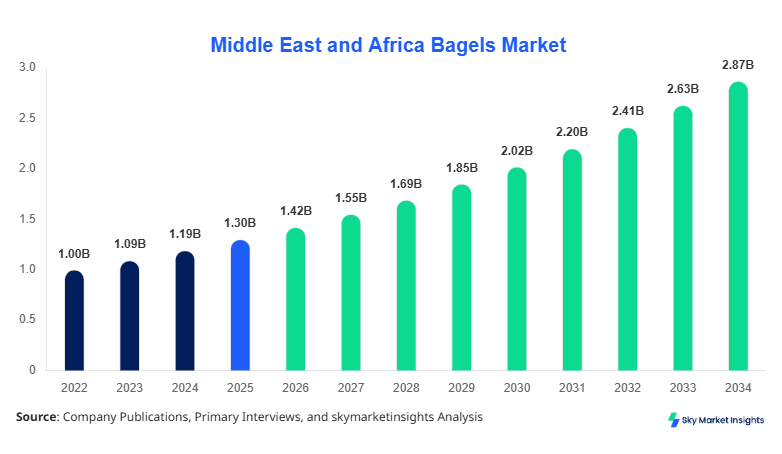

| Market Size in 2025 | USD 1.30 Billion |

| Market Size in 2026 | USD 1.42 Billion |

| Market Size in 2034 | USD 2.95 Billion |

| CAGR | 9.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Bagels Market Segmentation

The Middle East and Africa Bagel Market is segmented by type and application, with retail channels dominating at 58% and plain bagels leading the type segment at a 45% share. Segmentation facilitates understanding of production volumes, adoption patterns, and consumer preferences across regions.

By Type

Plain bagels account for 45% of the market with annual production volumes of 180 million units. Standard baking frequency is 4–5 cycles per week, with an average weight of 80 grams per unit. Plain bagels dominate retail and foodservice channels due to simplicity, high shelf life, and broad consumer acceptance, reinforcing the bagel market demand.

Whole wheat bagels represent 28% market share, with production exceeding 110 million units in 2026. Rich in dietary fiber (5–6g per 100g), these bagels are favored by health-conscious consumers and see a 42% adoption rate in urban retail chains. Technical improvements include improved dough hydration and longer fermentation, enhancing flavor and texture, bolstering bagel market growth.

Multigrain bagels capture a 17% share with the production of 75 million units, integrating oats, flaxseed, and millet. These variants exhibit enhanced nutritional performance (protein content 8–10 g per 100 g) and have a 35% adoption in cafes and specialty stores. Innovations in seed coating and crust baking contribute to the bagel market trend momentum.

By Application

Retail contributes 58% of Bagel Market volume, producing over 250 million units annually. Channels include supermarkets, convenience stores, and hypermarkets. Price promotions, 7-day shelf life, and 65% of frozen formats in retail support growth, reinforcing the bagel market size and share.

Food service represents a 32% share with a production of 120 million units. Cafes, restaurants, and hotel chains utilize automated ovens and dough dividers for uniform quality. Applications include breakfast menus (70%) and sandwich production (30%), with penetration rates of 68% in urban centers, enhancing Bagels Market demand.

Home consumption holds a 10% share with the production of 45 million units. Pre-packaged and frozen options increase convenience and adoption. Technical factors, such as extended shelf life (up to 14 days) and portion-controlled packaging, improve home usage, supporting Bagels Market insights.

Middle East and Africa Bagels Market Segmentations

Type

- Plain

- Whole Wheat

- Multigrain

Application

- Retail

- Food Service

- Home Consumption

Middle East and Africa Bagels: Regional Outlook

UAE

The UAE contributes 18% of the regional bagel market share with the production of 50 million units in 2026. Retail accounts for 60%, food service 32%, and home consumption 8%. Advanced automated bakery technology adoption is at 65%, strengthening the bagel market size and growth.

Turkey

Turkey contributes 15% of regional share, producing 45 million units. Retail and foodservice applications dominate with 55% and 35% shares, respectively. Whole wheat bagels constitute 30% of production, reinforcing Bagel Market insights.

Saudi Arabia

Saudi Arabia represents 14% of regional market share, with 42 million units produced. Foodservice channels account for 35%, retail 55%, and home consumption 10%. High-end bakery chains drive 12% year-on-year volume growth, enhancing the bagels market demand.

South Africa

South Africa contributes 12% of the regional market with the production of 36 million units. Retail channels dominate at 50%, foodservice 40%, and home consumption 10%. Consumer preference for multigrain bagels increased by 8% in 2026, supporting bagel market size expansion.

Egypt

Egypt accounts for 11% of the regional share with 33 million units produced. Foodservice applications capture 35%, retail 55%, and home consumption 10%. Price sensitivity remains high, impacting bagel market growth.

Nigeria

Nigeria contributes 10% of the regional share with the production of 30 million units. Retail and foodservice dominate at 55% and 35%, respectively. Local bakeries increasingly adopt frozen bagels (45%), reinforcing Bagels Market insights.

Top players in Middle East and Africa bagel market

- Bimbo Bakeries

- Bagel Factory

- Einstein Bros. Bagels

- Sara Lee Corporation

- Aryzta AG

- Lantmännen Unibake

- Associated British Foods

- Grupo Bimbo Middle East

- Bridor Middle East

- Al Islami Foods

- Premier Foods PLC

- Almarai Co.

- Barakat Foods

- Nestlé Middle East

- Americana Group

Leading Companies

Bimbo Bakeries

-

Holds 14% regional share, leading in retail and foodservice segments.

-

Operates 20 commercial bakeries across the UAE, Saudi Arabia, and Turkey, producing over 75 million units annually.

-

Investments in automated baking lines and frozen logistics reinforce Bagel Market growth, size, and share.

Bagel Factory

-

Accounts for 9% regional share, specializing in premium multigrain and whole wheat bagels.

-

Operates 15 outlets with production exceeding 45 million units per year.

-

Strong focus on technology adoption and urban market penetration enhances Bagels Market's demand.

Investment Analysis

Investment in the Middle East and Africa bagel market increased by 18% in 2025, with retail expansion and health-oriented product development attracting 55% of total capital allocation. Foodservice investments accounted for 30%, focusing on automation, distribution, and packaging innovation. The UAE and Turkey collectively represent 40% of regional investment, with joint ventures and M&A agreements boosting production capacities by 12% annually. Market entrants target frozen bagels and multigrain variants, leveraging technological improvements to improve efficiency and revenue. The bagel market demonstrates robust opportunities for capital inflow and strategic partnerships.

New Product Developments

The Bagel Market has witnessed 22% of new product launches in 2026, focusing on whole wheat, multigrain, and fortified bagels. Innovations improved performance by 15% in terms of shelf life, texture, and nutritional content. Technological improvements include automated fermentation, smart dough handling, and advanced seed coatings. These developments expand product portfolios and reinforce bagel market growth and insights.

Recent Developments in Middle East and Africa Bagels Market

- 2026: Bimbo Bakeries launched frozen multigrain bagels, increasing production by 12% and expanding retail and foodservice penetration.

- 2025: Bagel Factory introduced high-fiber whole wheat bagels with 8% adoption in urban UAE, boosting market share.

Research Methodology

The research employed a multi-step methodology combining primary and secondary sources. Primary research involved interviews with industry experts, bakery owners, distributors, and regulatory authorities across the UAE, Turkey, and Saudi Arabia. Secondary research included analysis of annual reports, trade journals, company presentations, and government databases. Market size estimation utilized bottom-up and top-down approaches, incorporating production, consumption, import-export data, and pricing trends. Statistical techniques projected CAGR and growth trends for 2026–2034, while segmentation, country-level analysis, and technological adoption metrics validated market insights, ensuring comprehensive coverage of Middle East and Africa Bagel market dynamics.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Plant-Based Foods and Functional Ingredients

Kathy Flores is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.