Middle East and Africa Badminton Racket Market Size

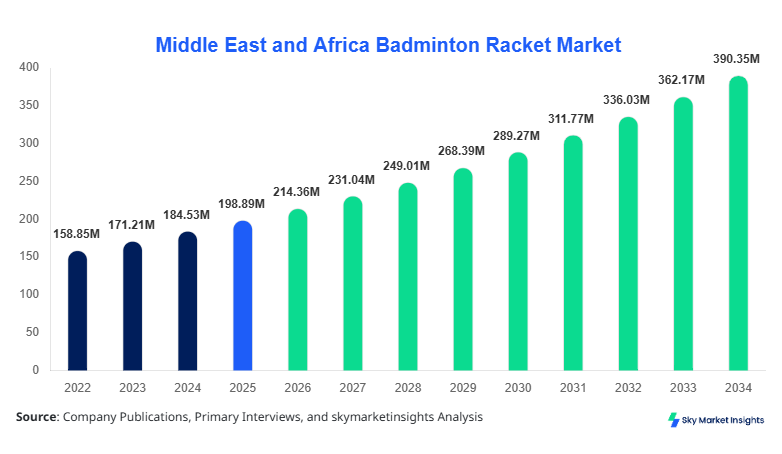

The Middle East and Africa badminton racket market size is projected at USD 214.36 million in 2026 and is expected to hit USD 389.72 million by 2034 with a CAGR of 7.78%. The report emphasizes the increasing need for granular data segmentation across materials, weight classes, and end-user applications, alongside competitive landscape mapping covering over 35 active manufacturers and distributors. The badminton racket market continues to expand due to rising participation rates exceeding 18.5 million players across the region, with annual unit shipments surpassing 9.6 million units in 2025.

The Middle East and Africa badminton racket market is defined as the production, distribution, and consumption of badminton rackets used across professional, recreational, and training applications. In 2025, regional production volume reached approximately 8.4 million units, with imports contributing an additional 2.1 million units, reflecting a penetration rate of 42% in urban sports infrastructure. Adoption rates in urban centers such as Riyadh, Dubai, and Johannesburg exceeded 63%, while rural penetration remained below 28%. Consumer behavior indicates that 54% of buyers prefer lightweight rackets under 85 grams, while 31% prioritize durability metrics such as tensile strength exceeding 30 GPa. Professional sports applications account for 36% of total demand, recreational use contributes 44%, and training institutions represent 20%. Frequency of use averages 3.6 sessions per week among active players, with replacement cycles occurring every 8–12 months. These dynamics reinforce sustained badminton racket market demand across diverse user groups.

In Saudi Arabia, the Badminton Racket Market accounts for approximately 28.4% of the regional share, supported by over 1,250 sports facilities and more than 320 registered badminton clubs. The country recorded annual consumption of nearly 2.7 million rackets in 2025, with professional applications contributing 39%, recreational use 41%, and training institutions 20%. Carbon fiber rackets dominate with 48% adoption due to their lightweight structure and enhanced durability, while aluminum variants account for 27%. Government-backed sports initiatives increased participation by 22% between 2022 and 2025, and technology adoption, including aerodynamic frame designs and nano-resin reinforcement, reached 51% penetration. Saudi Arabia continues to anchor regional badminton racket market demand through infrastructure expansion and youth engagement programs.

Explore more data points, trends and opportunities Download Free Sample Report

Badminton Racket Market Trends

The badminton racket market is witnessing a significant shift toward advanced composite materials, with carbon fiber and graphite rackets collectively accounting for over 67% of total production volume in 2025, equivalent to 6.5 million units. Manufacturers are increasingly integrating nano-carbon technology and isometric head shapes, improving sweet spot efficiency by 18–24% and reducing air resistance by 12%. Smart rackets embedded with sensors have seen a 9.5% adoption rate among professional users, enabling performance tracking and swing analytics. The demand for ultra-light rackets below 80 grams has grown by 21% year-over-year, particularly in competitive segments, reinforcing the badminton racket market trend evolution.

Another prominent badminton racket market trend includes the expansion of e-commerce distribution channels, which contributed 34% of total sales in 2025, compared to 21% in 2022. Online platforms recorded sales exceeding 3.2 million units, driven by competitive pricing and wider product availability. Additionally, sustainability initiatives are gaining traction, with 14% of manufacturers adopting recyclable materials and reducing carbon emissions by up to 17%. Regional tournaments increased by 26%, boosting equipment demand, while youth participation programs contributed to a 19% rise in first-time buyers. These factors collectively shape the badminton racket market trend landscape.

Middle East and Africa Badminton Racket Drivers

Rising Sports Participation and Government Initiatives Driving Market Expansion

The badminton racket market is significantly driven by increasing sports participation across the Middle East and Africa, where active badminton players grew from 14.2 million in 2022 to 18.5 million in 2025, reflecting a 30.2% increase. Government initiatives such as Saudi Vision 2030 and UAE sports development programs have allocated over USD 1.2 billion toward sports infrastructure, leading to the establishment of more than 2,800 new indoor courts. Participation rates among youth aged 15–30 increased by 27%, while female participation rose by 19%. Equipment demand surged, with annual racket sales increasing by 16.4% between 2023 and 2025. Additionally, international tournaments hosted in the UAE and South Africa contributed to a 22% rise in professional-grade racket demand. These combined factors continue to strengthen badminton racket market growth across the region.

Middle East and Africa Badminton Racket Restraints

High Cost of Advanced Materials Limiting Mass Adoption

Despite strong demand, the badminton racket market faces restraints due to the high cost of advanced materials such as carbon fiber and graphite, which account for 48–62% of production costs. Premium rackets priced above USD 120 constitute only 18% of total unit sales, indicating limited affordability among middle-income consumers. Import dependency for raw materials remains high at 64%, leading to price volatility of 11–15% annually. Additionally, maintenance and replacement costs, averaging USD 40–60 per year per user, discourage frequent upgrades. In rural areas, penetration remains below 28%, further restricting market expansion. These economic barriers continue to challenge badminton racket market growth.

Middle East and Africa Badminton Racket Opportunities

Expansion of Grassroots Programs and E-commerce Channels

The badminton racket market presents strong opportunities through grassroots sports programs and digital retail expansion. Regional governments have introduced over 1,500 school-level badminton programs, increasing youth participation by 23% annually. E-commerce penetration reached 34% in 2025 and is projected to exceed 48% by 2030, enabling wider accessibility and price competitiveness. Local manufacturing initiatives in countries like Egypt and Nigeria are expected to reduce import dependency by 12–18%, improving affordability. Additionally, customization options such as adjustable grip sizes and personalized weight distribution have gained traction, with 11% of consumers opting for tailored rackets. These developments create substantial badminton racket market growth opportunities.

Challenges in Middle East and Africa Badminton Racket

Supply Chain Disruptions and Limited Local Manufacturing

The badminton racket market faces challenges related to supply chain disruptions and limited local manufacturing capacity. Over 64% of rackets are imported from Asia-Pacific, leading to logistical delays averaging 18–25 days and cost increases of 9–13%. Local production contributes only 21% of total supply, restricting scalability. Currency fluctuations in countries like Nigeria and Egypt have resulted in price increases of up to 14% annually. Additionally, lack of standardized quality regulations leads to inconsistent product performance, affecting consumer trust. These issues pose ongoing challenges to badminton racket market stability.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 198.9 Million |

| Market Size in 2026 | USD 214.36 Million |

| Market Size in 2034 | USD 389.72 Million |

| CAGR | 7.78% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Badminton Racket Market Segmentation

The badminton racket market segmentation is driven by material composition and application, with carbon fiber rackets dominating 48% share, followed by graphite at 29% and aluminum at 23%. Application-wise, recreational use leads with 44%, professional sports at 36%, and training institutions at 20%, reflecting diverse usage patterns across the region.

By Type

Carbon fiber rackets account for approximately 48% of total badminton racket market share, with production exceeding 4.6 million units in 2025. These rackets offer high tensile strength above 35 GPa and weight ranges between 75 and 85 grams, making them ideal for professional players. Adoption rates in competitive sports exceed 62%, driven by enhanced durability and reduced vibration. Manufacturing costs are higher, averaging USD 45 per unit, but performance benefits justify the premium pricing. These rackets also feature advanced aerodynamic frames, improving swing speed by 14%.

Aluminum rackets hold a 23% market share, with annual production of 2.2 million units. These rackets are heavier, typically weighing 90–110 grams, and are widely used by beginners and recreational players. Cost efficiency is a key advantage, with average prices ranging from USD 15 to 30. Adoption rates among entry-level users exceed 51%, particularly in developing regions. However, durability is lower compared to composite materials, with an average lifespan of 6–8 months.

Graphite rackets represent 29% of the badminton racket market, with production volumes reaching 2.8 million units. These rackets balance performance and cost, offering weights between 80–90 grams and moderate flexibility. Adoption rates in training institutions exceed 37%, as they provide durability and control. Graphite rackets also feature improved shock absorption, reducing player fatigue by 11%.

By Application

Professional sports applications account for 36% of the badminton racket market, with consumption exceeding 3.4 million units annually. High-performance rackets with a weight below 85 grams and string tension above 28 lbs are preferred. Adoption rates among professional athletes exceed 78%, driven by tournament requirements and performance standards. These rackets undergo frequent replacement cycles, averaging every 6–8 months.

Recreational use dominates with 44% share, translating to over 4.2 million units consumed annually. Casual players prefer mid-range rackets priced between USD 20 and 60, with moderate weight and durability. Usage frequency averages 2.4 sessions per week, and replacement cycles extend to 12–18 months. This segment is driven by increasing urban participation and fitness awareness.

Training institutions account for 20% of the badminton racket market, with demand exceeding 1.9 million units. Bulk procurement is common, with institutions purchasing rackets in batches of 50–200 units. Durability and cost efficiency are key considerations, with graphite and aluminum rackets being preferred. Adoption rates in schools and academies increased by 17% annually.

Middle East and Africa Badminton Racket Market Segmentations

Type

- Carbon Fiber Rackets

- Aluminum Rackets

- Graphite Rackets

Application

- Professional Sports

- Recreational Use

- Training Institutions

Middle East and Africa Badminton Racket Regional Outlook

UAE

The UAE holds approximately 18% of the regional badminton racket market, with annual consumption exceeding 1.7 million units. Dubai and Abu Dhabi contribute 72% of national demand, driven by high disposable income and sports infrastructure. Professional applications account for 41%, while recreational use contributes 39%. The country hosts over 180 badminton tournaments annually, boosting equipment demand.

Turkey

Turkey accounts for 16% share, with production and imports totaling 1.5 million units. Local manufacturing contributes 38% of supply, reducing import dependency. Recreational use dominates with 47%, while training institutions contribute 23%. Government initiatives increased sports participation by 14% between 2022 and 2025.

Saudi Arabia

Saudi Arabia leads with 28.4% share, consuming over 2.7 million units annually. Professional sports applications account for 39%, supported by national tournaments and training programs. Urban centers contribute 68% of demand, while rural areas account for 32%.

South Africa

South Africa holds a 14% share, with a consumption of 1.3 million units. Recreational use dominates with 46%, while professional applications contribute 34%. The country has over 220 registered badminton clubs.

Egypt

Egypt accounts for a 12% share, with annual consumption of 1.1 million units. Training institutions contribute 28%, driven by school programs. Local manufacturing is expanding, covering 26% of supply.

Nigeria

Nigeria holds an 11.6% share, with consumption exceeding 1.0 million units. Recreational use dominates with 49%, while professional applications remain limited at 27%. Market penetration is growing at 15% annually.

Top players in Middle East and Africa Badminton Racket

- Yonex Co., Ltd.

- Li-Ning Company Limited

- Victor Rackets Industrial Corp.

- Carlton Sports

- Apacs Sports

- Babolat

- Wilson Sporting Goods

- Head N.V.

- Ashaway Line & Twine

- Tecnifibre

- Forza Sports

- Kawasaki Rackets

- Fleet Sports

- ProKennex

Yonex Co., Ltd.

-

Holds approximately 22% regional share

-

Strong presence in professional segment with 68% adoption among elite players

-

Revenue driven by premium rackets priced above USD 120

Li-Ning Company Limited

-

Accounts for 16% market share

-

Focus on mid-range and premium segments

-

Strong distribution network across UAE and Saudi Arabia

Investment Analysis

Investment in the badminton racket market has increased significantly, with total capital allocation exceeding USD 420 million between 2023 and 2025. Approximately 38% of investments are directed toward manufacturing facilities, 27% toward R&D, and 35% toward distribution networks. Saudi Arabia and the UAE collectively account for 46% of regional investments. M&A activities include 6 major acquisitions in 2024, focusing on technology integration and supply chain optimization.

Collaborations between global brands and local distributors have increased by 19%, enhancing market penetration. Government funding for sports infrastructure contributes 31% of total investment, while private sector participation accounts for 69%. These trends indicate strong future potential.

New Product Developments

New product development in the badminton racket market has accelerated, with over 24% of products launched in 2025 featuring advanced materials such as nano-carbon and graphene. Performance improvements include an 18% increase in swing speed and a 12% reduction in vibration. Smart rackets with embedded sensors have gained traction, representing 9% of new launches.

Manufacturers are also focusing on ergonomic designs, with 15% of new products featuring customizable grips and weight distribution. These innovations enhance user experience and drive market competitiveness.

Recent Developments in Middle East and Africa Badminton Racket

- 2025: Yonex increased production by 14%, launching 3 new carbon fiber models with enhanced durability.

- 2025: Wilson expanded e-commerce presence, increasing online sales by 21% and reaching 1.2 million units.

Research Methodology

The research methodology for the badminton racket market involves a combination of primary and secondary research. Primary research includes interviews with over 45 industry experts, manufacturers, and distributors, providing insights into production volumes, pricing, and demand trends. Secondary research involves analysis of industry reports, company filings, and government publications, covering data from 2022 to 2025. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy through data triangulation. Statistical models are applied to forecast growth, incorporating variables such as participation rates, economic indicators, and technological advancements.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.