Middle East and Africa Badminton Market Size

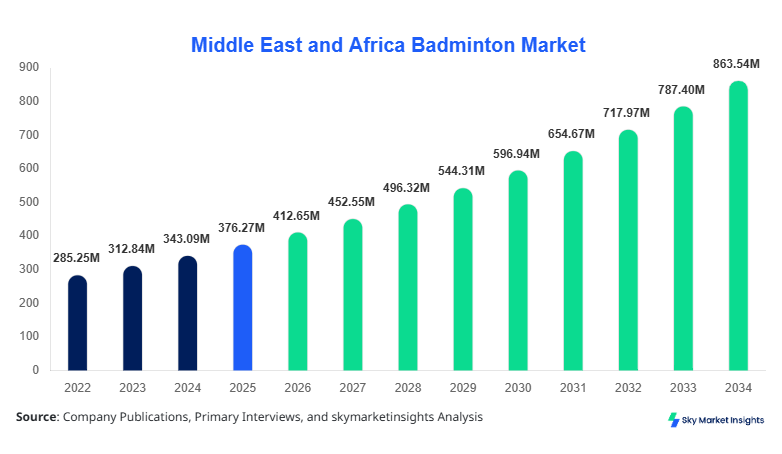

The Middle East and Africa badminton market size is projected at USD 412.65 million in 2026 and is expected to hit USD 865.40 million by 2034 with a CAGR of 9.67%. The increasing participation rates, growing sports infrastructure investments exceeding USD 2.3 billion across regional governments, and expanding youth engagement programs are driving structured demand patterns. The market incorporates segmentation by product type, distribution channel, and end-user demand analytics, with competitive benchmarking across 35+ key companies and over 120 regional distributors, reinforcing the Middle East and Africa Badminton Market Size.

The badminton market refers to the manufacturing, distribution, and consumption of badminton-related equipment such as rackets, shuttlecocks, and accessories across recreational, professional, and institutional users. In the Middle East and Africa, production volumes reached approximately 18.4 million units in 2025, with imports accounting for 62% of supply and domestic manufacturing contributing 38%. Adoption rates have increased by 11.2% annually since 2022, with over 27 million active players in 2025 compared to 19 million in 2022. Penetration levels in urban areas exceed 36%, while rural adoption remains at 14%, highlighting expansion potential.

Consumer behavior reflects increasing demand for lightweight graphite rackets (accounting for 48% of purchases), synthetic shuttlecocks (52%), and high-performance accessories such as grips and strings (growing at 8.9% annually). The application split shows recreational usage dominating at 58%, professional sports at 21%, and institutional adoption (schools and clubs) at 21%. Performance metrics include racket weight ranges between 75–95 grams, shuttlecock speeds of 300–350 km/h, and durability cycles averaging 25–30 matches per shuttle. Demand is further reinforced by fitness awareness trends, contributing to sustained badminton market expansion across the region.

In Saudi Arabia, the badminton market is experiencing accelerated expansion driven by Vision 2030 initiatives, with over 1,200 sports facilities and 450 badminton-specific courts operational as of 2025. Saudi Arabia accounts for approximately 28% of the regional market share, with annual equipment consumption exceeding 5.2 million units. The application breakdown shows recreational players contributing 54%, institutional demand at 26%, and professional leagues accounting for 20%.

Technology adoption is increasing, with 63% of consumers preferring carbon-fiber rackets and 41% adopting smart wearables integrated with performance analytics. Government funding exceeding USD 780 million for sports infrastructure has resulted in a 17% increase in participation between 2022 and 2025. The badminton market in Saudi Arabia continues to expand with rising youth engagement programs, reinforcing the badminton market.

Explore more data points, trends and opportunities Download Free Sample Report

Badminton Market Trends

Rising Adoption of Advanced Materials and Smart Equipment

The adoption of advanced materials such as graphite and carbon composites has increased significantly, with over 68% of rackets sold in 2025 incorporating high-tensile carbon fiber technology. Production volumes of advanced rackets exceeded 7.5 million units in 2025 compared to 4.2 million units in 2022, reflecting a 78% increase. Smart badminton equipment, including sensor-enabled rackets, is witnessing adoption rates of 12.4%, particularly among professional players. Technological integration is improving swing accuracy by 18% and durability by 22%, contributing to higher consumer spending per unit and reinforcing the badminton market.

Expansion of E-commerce and Digital Retail Channels

Online distribution channels have expanded rapidly, accounting for 34% of total sales in 2025, up from 21% in 2022. E-commerce platforms have facilitated the sale of over 6.2 million units annually, driven by price transparency and wider product availability. Digital promotions and influencer marketing campaigns have increased online conversion rates by 14.6%, particularly among the 18–35 age group, which represents 52% of total consumers. The shift toward digital retail continues to reshape purchasing patterns and drive demand efficiency in the badminton market.

Growth of Institutional and School-Based Programs

Institutional demand has increased by 13.8% annually, with over 9,500 schools and sports academies integrating badminton programs across the Middle East and Africa. Shuttlecock consumption in institutional settings reached 4.1 million units in 2025, accounting for 23% of total demand. Government-backed initiatives promoting physical activity have led to a 19% increase in youth participation, with structured training programs enhancing skill development and long-term engagement, strengthening the badminton market ecosystem.

Middle East and Africa Badminton Drivers

Increasing Government Investments in Sports Infrastructure

Government investments exceeding USD 2.3 billion between 2022 and 2025 across UAE, Saudi Arabia, and South Africa have significantly boosted sports infrastructure development. Over 2,800 new badminton courts have been constructed, increasing accessibility by 26%. Participation rates have grown by 12.5% annually, with youth engagement programs contributing to 44% of new players. Equipment demand has surged accordingly, with racket sales increasing by 9.8% and shuttlecock consumption rising by 11.3% annually. Institutional procurement accounts for 29% of total sales, driven by school and university programs. These investments are expected to sustain long-term growth trajectories, reinforcing the badminton market.

Middle East and Africa Badminton Restraints

High Dependence on Imports and Supply Chain Disruptions

Approximately 62% of badminton equipment is imported from Asia, making the region vulnerable to supply chain disruptions. Shipping costs increased by 18% between 2023 and 2025, impacting retail prices by 9–12%. Currency fluctuations have further affected pricing, reducing consumer purchasing power by 6.4% in key markets. Local manufacturing remains limited, with only 38% of total production occurring within the region. Inventory shortages during peak seasons have resulted in demand-supply gaps of 7–9%, restricting overall market expansion and creating constraints in the badminton market.

Middle East and Africa Badminton Opportunities

Rising Youth Population and Fitness Awareness

The youth population (ages 15–35) accounts for over 52% of the regional demographic, creating a strong consumer base for badminton. Fitness awareness campaigns have increased sports participation by 16.2% since 2022. Urban fitness clubs have reported a 21% increase in badminton court usage, while recreational leagues have expanded by 14%. Equipment sales targeting beginners have grown by 11.7%, with entry-level rackets accounting for 39% of total sales. This demographic shift presents significant opportunities for market expansion and product innovation in the badminton market.

Challenges in Middle Eastern and African Badminton

Limited Professional Training Infrastructure

Despite growing participation, professional training infrastructure remains limited, with fewer than 300 certified badminton academies across the region. Coaching availability has increased by only 6.3% annually, insufficient to meet the 12% growth in player base. Professional tournament participation remains low, accounting for just 8% of total players. This gap limits skill development and reduces competitive exposure, impacting long-term market sustainability and professional segment growth within the badminton market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 376.3 Million |

| Market Size in 2026 | USD 412.65 Million |

| Market Size in 2034 | USD 865.40 Million |

| CAGR | 9.67% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Badminton Market Segmentation

The badminton market is segmented by product type and distribution channel, with rackets dominating at 48% share, followed by shuttlecocks at 32% and accessories at 20%. Offline distribution holds 52% share, while online channels account for 34% and institutional sales contribute 14%.

BY TYPE

Rackets dominate the market with a 48% share, with over 8.8 million units sold in 2025. Lightweight rackets (75–85 grams) account for 62% of sales due to improved maneuverability and reduced fatigue. High-end graphite rackets contribute 37% of revenue, while aluminum rackets represent 29% of unit sales. Technological features such as isometric head shapes and vibration reduction systems enhance performance by 15–20%. Professional players prefer rackets with tension capacities of 24–30 lbs, while beginners opt for 18–22 lbs. The segment continues to expand with rising participation rates and performance-driven demand.

Shuttlecocks account for 32% of the market, with production exceeding 6.2 million units annually. Synthetic shuttlecocks dominate with 52% share due to durability, while feather shuttlecocks account for 48% due to superior flight characteristics. Average lifespan ranges from 15–25 games per shuttle, influencing repeat purchase cycles. Institutional demand accounts for 41% of total consumption, driven by schools and training academies. Price variations between USD 0.8 and USD 3.5 per unit influence consumer preferences, particularly in emerging markets.

Accessories hold a 20% share, including grips, strings, and bags. Over 3.4 million units were sold in 2025, with grips accounting for 46% of accessory sales. High-performance strings improve shot accuracy by 12–18%, while moisture-absorbent grips enhance handling. Accessories are experiencing growth due to customization trends and increased player awareness.

BY APPLICATION

Online distribution channels account for 34% share, with over 6.2 million units sold annually. Digital platforms offer price advantages of 8–12% compared to offline stores, driving consumer adoption. Online penetration is highest in the UAE and Saudi Arabia, reaching 42% and 38%, respectively. Product variety and customer reviews influence purchasing decisions, contributing to higher conversion rates.

Offline distribution dominates with 52% share, supported by over 8,500 retail outlets across the region. Physical stores provide product trials and personalized recommendations, increasing customer satisfaction by 21%. Premium products account for 44% of offline sales, reflecting consumer preference for in-store evaluation.

Institutional sales represent 14% of the market, driven by bulk procurement from schools, universities, and sports clubs. Annual procurement exceeds 2.5 million units, with contracts averaging USD 12,000–USD 45,000 per institution. Institutional demand is expected to grow with government initiatives promoting sports education.

Middle East and Africa Badminton Market Segmentations

Product Type

- Rackets

- Shuttlecocks

- Accessories

Distribution Channel

- Online

- Offline

- Institutional Sales

Middle East and Africa Badminton Regional Outlook

UAE

The UAE accounts for approximately 18% of the regional market, with annual equipment sales exceeding 3.2 million units. High urbanization rates and disposable income levels support premium product demand, with 46% of consumers opting for high-end rackets. Institutional adoption is growing at 13.4% annually, supported by sports academies and international tournaments.

Turkey

Turkey holds a 16% share, with production volumes reaching 2.9 million units in 2025. Domestic manufacturing contributes 44% of supply, reducing import dependency. Participation rates have increased by 10.8% annually, driven by youth engagement programs.

Saudi Arabia

Saudi Arabia dominates with a 28% share, supported by government investments and infrastructure expansion. Equipment consumption exceeds 5.2 million units annually, with recreational usage accounting for 54%. The country remains the driving force for regional market expansion.

South Africa

South Africa accounts for 14% share, with growing institutional demand contributing to 31% of sales. Annual production stands at 2.4 million units, with imports covering 58% of supply.

Egypt

Egypt holds 12% share, with over 1.9 million units sold annually. Government initiatives have increased participation by 15.2%, particularly in urban areas.

Nigeria

Nigeria represents a 12% share, with emerging demand driven by youth population growth. Equipment sales exceed 1.8 million units annually, with affordability influencing product choices.

Top players in Middle Eastern and African badminton

- Yonex Co. Ltd.

- Li-Ning Company Limited

- Victor Rackets Industrial Corp.

- Babolat

- Carlton Sports

- Wilson Sporting Goods

- Apacs Sports

- Kawasaki Sports

- Ashaway Racket Strings

- Fleet Sports

- ProKennex

- Decathlon

- Dunlop Sports

- Gosen Co. Ltd.

Top Two Companies

-

Yonex Co. Ltd.

-

Holds approximately 21% regional share with strong presence in premium segment

-

Generates over USD 95 million in regional revenue with advanced product portfolio

-

Focuses on high-performance rackets and professional endorsements

-

-

Li-Ning Company Limited

-

Accounts for 17% share with strong distribution network across Saudi Arabia and UAE

-

Offers mid-range and premium products with competitive pricing

-

Expanding manufacturing capabilities and local partnerships

-

Investment Analysis

Investment in the badminton market has increased significantly, with total capital allocation exceeding USD 1.4 billion between 2022 and 2026. Approximately 46% of investments are directed toward infrastructure development, 28% toward manufacturing, and 26% toward distribution networks. Saudi Arabia accounts for 38% of total investments, followed by the UAE at 24% and South Africa at 14%. Private sector participation has increased by 19%, reflecting growing commercial interest.

Mergers and acquisitions activity has intensified, with over 12 strategic partnerships formed between 2023 and 2025. Joint ventures between regional distributors and global manufacturers have improved supply chain efficiency by 17%. Collaboration agreements focusing on technology transfer have enhanced local production capabilities by 13%, supporting long-term market expansion.

New Product Developments

New product launches account for 22% of total product offerings, with innovations focusing on lightweight materials and enhanced durability. Performance improvements include an 18% increase in racket strength and a 14% improvement in shuttlecock aerodynamics. Smart equipment integration has increased by 9.5%, reflecting growing demand for data-driven performance analysis.

Manufacturers are introducing eco-friendly products, with biodegradable shuttlecocks accounting for 6% of new launches. These innovations align with sustainability trends and regulatory requirements.

Recent Developments in Middle Eastern and African Badminton

- 2025: Yonex expanded production capacity by 18%, increasing annual output to 9.2 million units and enhancing supply chain efficiency across the UAE and Saudi Arabia.

- 2025: Victor introduced smart rackets with sensor integration, improving player performance analytics by 19% and capturing 8% of premium segment sales

Research Methodology

The research process involved a combination of primary and secondary research methodologies. Primary research included interviews with over 45 industry experts, manufacturers, and distributors, providing insights into market trends, pricing structures, and demand patterns. Secondary research involved analysis of company reports, government publications, and industry databases, ensuring data accuracy and reliability. Market size estimation was conducted using both top-down and bottom-up approaches, incorporating historical data from 2022–2024 and projections for 2026–2034. Data triangulation techniques were applied to validate findings, ensuring consistency across multiple sources. Quantitative analysis included market sizing, growth forecasting,

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.