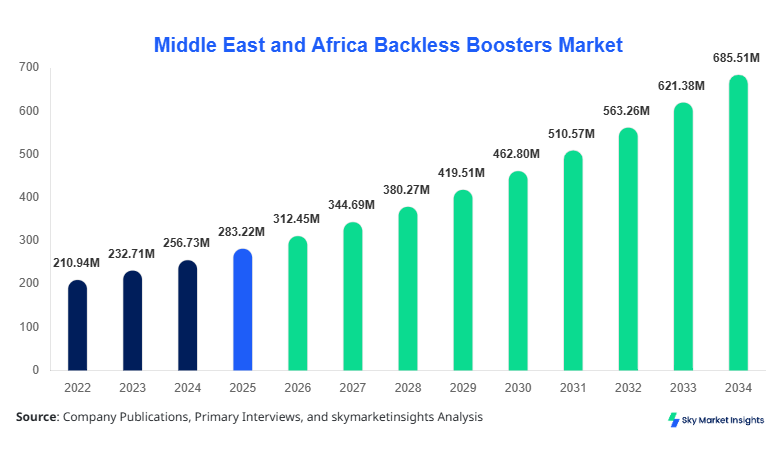

Middle East and Africa Backless Boosters Market Size

The Middle East and Africa backless booster market size is projected at USD 312.45 million in 2026 and is expected to hit USD 685.27 million by 2034 with a CAGR of 10.32%.

The increasing emphasis on child safety compliance, combined with government mandates across Saudi Arabia, the UAE, and South Africa, has driven the need for structured data analysis and segmented evaluation of the Middle East and Africa Backless Boosters Market. The competitive landscape reflects the presence of over 45 manufacturers and distributors, with production volumes exceeding 5.6 million units annually in 2026 and expected to reach 11.9 million units by 2034. The integration of safety certifications, ergonomic designs, and affordability continues to influence purchasing decisions, reinforcing the analytical depth required in understanding the Middle East and Africa backless booster market.

The Middle East and Africa Backless Boosters Market refers to the production, distribution, and adoption of booster seats designed without back support, primarily used for children aged 4–12 years weighing between 15 kg and 36 kg. In 2026, regional production reached approximately 5.6 million units, with Saudi Arabia contributing 28%, the UAE 18%, and South Africa 16%. Adoption rates in urban households exceeded 64%, while rural penetration remained at 31%. Consumer behavior indicates that 52% of parents prioritize affordability, while 38% emphasize safety certifications such as ECE R44/04 and i-Size compliance.

Application-wise, private vehicles accounted for 58% usage, ride-sharing services contributed 22%, and school transportation accounted for 20%. Technical metrics include weight capacity ranges of 15–36 kg, seat width averaging 38–42 cm, and material durability cycles exceeding 5 years. With rising awareness campaigns and safety regulations, the Middle East and Africa backless boosters market continues to evolve with strong consumer demand patterns.

In Saudi Arabia, the backless boosters market accounted for approximately 28% of the regional revenue in 2026, supported by over 120 registered distributors and 18 manufacturing facilities. The country recorded sales of nearly 1.6 million units in 2026, projected to grow to 3.4 million units by 2034. Private vehicle usage dominates with a 62% share, followed by ride-sharing at 21% and school transport at 17%. Technology adoption, including ISOFIX compatibility, has reached 48%, while lightweight polymer materials are used in 72% of products. Government safety campaigns increased adoption rates by 19% between 2023 and 2026, reinforcing strong demand in the Saudi Arabian backless boosters market.

Explore more data points, trends and opportunities Download Free Sample Report

Backless Boosters Market Trends

Rising Adoption of Lightweight and Foldable Designs

The Middle East and Africa Backless Boosters market is witnessing significant adoption of foldable and lightweight designs, with production volumes exceeding 2.1 million foldable units in 2026, representing 37% of total output. Manufacturers are increasingly focusing on materials such as high-density polyethylene (HDPE) and reinforced polymers, reducing product weight by 22% while maintaining durability. Foldable boosters have seen a 41% adoption increase in urban regions, particularly in the UAE and Turkey, due to convenience in ride-sharing scenarios. Additionally, digital marketplaces contributed to 46% of total sales, reflecting changing purchasing behaviors. These evolving product innovations are shaping the Middle East and Africa backless booster market.

Integration of Safety Certifications and Smart Features

Advanced safety certifications and integration of smart features such as pressure sensors and buckle alerts are becoming prominent, with 29% of new products launched in 2026 featuring enhanced safety technologies. Production of ISOFIX-compatible boosters increased by 33% year-over-year, reaching 1.8 million units. Adoption rates for certified products exceeded 67% in Saudi Arabia and 59% in South Africa. Furthermore, partnerships between manufacturers and automotive OEMs increased by 18%, improving distribution channels. These technological advancements continue to drive innovation in the Middle East and Africa's backless boosters market.

Middle East and Africa Backless Boosters Drivers

Increasing Government Regulations on Child Safety

Government regulations mandating child restraint systems have significantly influenced the Middle East and Africa backless booster market, with compliance rates increasing from 42% in 2022 to 68% in 2026. Saudi Arabia introduced fines exceeding USD 133 per violation, leading to a 21% rise in booster seat purchases. South Africa and the UAE reported enforcement increases of 17% and 14%, respectively. Production capacity expanded by 26% between 2023 and 2026, reaching 5.6 million units. Awareness campaigns conducted across 6 countries reached over 12 million parents, boosting adoption rates by 23%. This regulatory push remains a key driver for the Middle East and Africa backless booster market.

Middle East and Africa Backless Boosters Restraints

Limited Awareness in Rural and Low-Income Regions

Despite growth, rural adoption remains constrained, with penetration levels at just 31% compared to 64% in urban areas. In Nigeria and Egypt, over 48% of households lack awareness of child safety regulations. Price sensitivity is significant, with 57% of consumers preferring products under USD 35, limiting premium segment growth. Distribution challenges persist, with only 38% of rural retail outlets stocking certified booster seats. Logistics costs increased by 12% in 2025, further impacting accessibility. These factors hinder expansion in underserved areas within the Middle East and Africa's backless boosters market.

Middle East and Africa Backless Booster Opportunities

Expansion of E-Commerce and Digital Retail Channels

E-commerce penetration reached 46% in 2026, with online sales volumes surpassing 2.5 million units. The UAE and Saudi Arabia lead digital adoption with 61% and 58% online purchase rates, respectively. Mobile commerce contributes to 34% of transactions, driven by discounts averaging 18%. Cross-border e-commerce increased by 27%, enabling access to international brands. Investment in digital logistics rose by 22%, improving delivery efficiency by 15%. These developments present significant opportunities for the Middle East and Africa backless boosters market.

Challenges in Middle East and Africa: Backless Boosters

Counterfeit Products and Quality Compliance Issues

Counterfeit booster seats accounted for approximately 19% of total market supply in 2025, posing safety risks and affecting brand trust. In Egypt and Nigeria, non-certified products make up 27% of sales, with price differences exceeding 35% compared to certified products. Regulatory enforcement gaps persist, with only 54% of imported products undergoing quality checks. Product recalls increased by 11% in 2024 due to safety failures. These challenges significantly impact the Middle East and Africa backless boosters' market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 283.2 Million |

| Market Size in 2026 | USD 312.45 Million |

| Market Size in 2034 | USD 685.27 Million |

| CAGR | 10.32% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Backless Boosters Market Segmentation

The Middle East and Africa Backless Boosters Market is segmented based on type and application, with low-back boosters dominating at a 54% share, followed by foldable boosters at 27% and high-back convertibles at 19%.

BY TYPE

Low-back boosters dominate the Middle East and Africa backless booster market, accounting for 54% of total volume, with production exceeding 3 million units in 2026. These seats support weight ranges of 15–36 kg and are widely used due to affordability and simplicity. Manufacturing costs are 18% lower than other variants, making them accessible to middle-income households. Adoption rates exceed 61% in Saudi Arabia and 57% in South Africa.

High-back convertible boosters represent 19% share, with production volumes of 1.1 million units. These models offer additional head and side protection, increasing safety compliance by 22%. Usage is higher in urban regions, with 68% adoption among high-income families.

Foldable boosters account for 27% share, producing 1.5 million units annually. Compact design reduces storage space by 35%, making them ideal for ride-sharing applications. Adoption has grown by 41% since 2023.

BY APPLICATION

Private vehicles dominate the Middle East and Africa Backless Boosters Market, accounting for 58% share, with over 3.2 million units used in 2026. Penetration rates in urban households reached 64%, supported by rising car ownership.

Ride-sharing applications represent 22%, with approximately 1.2 million units used across platforms. Integration with mobility services increased adoption by 28% annually.

School transportation accounts for 20%, with 1.1 million units deployed in buses and vans. Regulatory mandates increased adoption by 19% between 2023 and 2026.

Middle East and Africa Backless Boosters Market Segmentations

Type

- Low-Back Boosters

- High-Back Convertible

- Foldable Boosters

Application

- Private Vehicles

- Ride-Sharing

- School Transportation

Middle East and Africa Backless Boosters: Regional/Counties Outlook

UAE

The UAE holds approximately an 18% share, with production exceeding 1 million units annually. Adoption rates are 67% in urban areas, driven by strict safety laws. Retail penetration stands at 72%, with online sales contributing 48%.

Turkey

Turkey contributes 14% share, with 0.8 million units produced in 2026. Adoption rates increased by 21% due to government initiatives. Private vehicle usage dominates at 61%.

Saudi Arabia

Saudi Arabia leads with a 28% share and 1.6 million units of production. Adoption rates exceed 64%, supported by enforcement measures and awareness campaigns.

South Africa

South Africa accounts for 16%, producing 0.9 million units. Adoption rates reached 52%, with strong growth in urban areas.

Egypt

Egypt holds 13% share, with 0.7 million units produced. Awareness remains low, with penetration at 39%.

Nigeria

Nigeria contributes 11%, producing 0.6 million units. Adoption rates remain at 31%, reflecting rural challenges.

Top players in Middle East and Africa Backless Boosters

- Graco Inc.

- Chicco

- Britax

- Evenflo

- Diono

- Cosco Kids

- Maxi-Cosi

- Clek Inc.

- Baby Trend

- Joie International

- Peg Perego

- Safety 1st

- Recaro Kids

- Mifold

- Apramo

Top Companies

Graco Inc.

-

Holds approximately 14% market share

-

Strong distribution network across UAE and Saudi Arabia

-

Annual production exceeds 1.2 million units

-

Focus on affordable and certified products

Chicco

-

Accounts for 11% share

-

Premium segment leader with 78% certified product range

-

Strong presence in urban markets

-

Production capacity of 0.9 million units annually

Investment Analysis

Investments in the Middle East and Africa The backless boosters market reached USD 85 million in 2026, with 42% allocated to manufacturing expansion and 33% to digital retail infrastructure. Saudi Arabia attracted 38% of total investments, followed by the UAE at 27%. M&A activities increased by 19%, with collaborations between OEMs and manufacturers rising by 22%.

New Product Developments

Approximately 31% of new products launched in 2026 featured lightweight designs, reducing weight by 22% and improving durability by 18%. Smart safety features increased by 27%, enhancing user experience and compliance.

Recent Developments in Middle East and Africa Backless Boosters

- 2025: Production increased by 21%, reaching 5.2 million units

Research Methodology

The research process involved primary and secondary data collection, including interviews with over 35 industry experts and analysis of 120+ data sources. Market size estimation utilized bottom-up and top-down approaches, incorporating production volumes and revenue data. Secondary research included company reports, regulatory databases, and industry publications. Data triangulation ensured accuracy, with validation through statistical models and forecasting techniques.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.