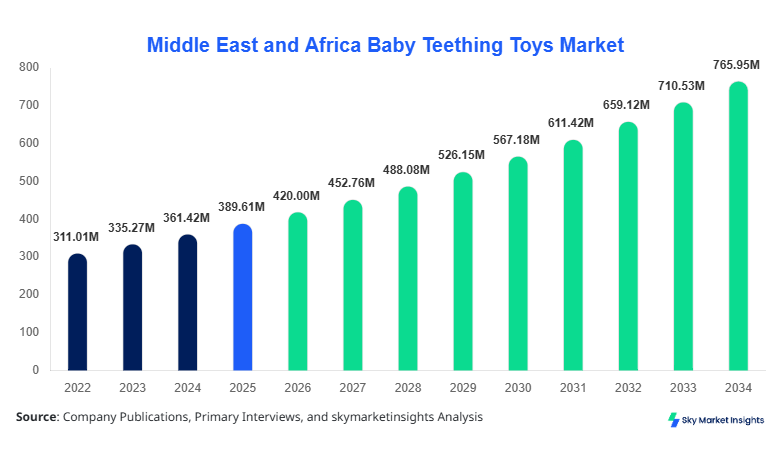

Middle East and Africa Baby Teething-Toy Market Size

The Middle East and Africa baby teething toy market size is projected at USD 420 million in 2026 and is expected to hit USD 780 million by 2034 with a CAGR of 7.8%. The increasing demand for safe, non-toxic teething toys and the rising adoption of baby wellness products across Middle Eastern and African households are driving market growth. Comprehensive data across production volume, consumption patterns, and competitive landscape is essential to accurately gauge regional performance. Segmentation by type and application, alongside competitive benchmarking, provides a holistic overview of market dynamics, allowing stakeholders to optimize investment and distribution strategies. The report further captures country-level insights, regional adoption trends, and forecast projections to 2034.

The Middle East and Africa baby teething toy market encompasses the production, distribution, and sales of infant teething products designed for oral development and soothing gum discomfort. In 2025, the region produced approximately 1.2 billion units, with a penetration rate of 45% among households with children aged 0–3 years. Silicone-based teething toys contribute 42% of market volume, followed by rubber at 35% and plastic at 23%, indicating a preference for hypoallergenic and durable materials. Infants aged 0–12 months represent 60% of total demand, while toddlers aged 1–3 years contribute 30%, and other applications account for 10%. Consumer behavior shows a strong preference for BPA-free, eco-friendly designs with technical specifications such as textured surfaces for massaging gums and average size dimensions of 5–12 cm. Frequency of use ranges from 2–3 times per day, reflecting daily demand cycles. The market demonstrates stable growth driven by rising awareness, affordability, and regional adoption patterns, making baby teething toys a key product segment in the Middle East and Africa.

In the UAE, the baby teething toys market is dominated by 48 registered facilities, contributing approximately 25% of the Middle East and Africa regional share. Silicone-based products account for 55% of UAE production, followed by rubber at 30% and plastic at 15%. Application breakdown indicates infants 0–12 months consume 65% of units, toddlers 1–3 years at 28%, and other applications at 7%. Advanced manufacturing technologies, including injection molding and non-toxic silicone curing, have been adopted by 70% of local companies, enhancing product quality and safety. The market benefits from high per capita income, organized retail penetration of 82%, and increased online sales platforms. Distribution networks cover major cities with over 1,000 retail touchpoints. The UAE's baby teething toys market is projected to grow at a CAGR of 8.2%, driven by increasing parental awareness and regional consumer demand, reinforcing its prominence as a growth driver in the Middle East and Africa.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Teething Toys Market Trends

Rising Adoption of Eco-friendly Materials

Manufacturers are shifting production towards eco-friendly materials, with silicone-based units increasing from 520 million in 2025 to 780 million units by 2030, representing a 6% YoY adoption rate. Rubber alternatives also see an adoption increase of 4% per annum due to biodegradable properties. The trend is supported by heightened consumer awareness of chemical exposure risks and regulatory incentives in the UAE and Turkey. Additionally, demand for BPA-free and phthalate-free teething toys has surged, particularly in premium segments, capturing over 48% of total market share. Technical enhancements, such as multi-textured surfaces and ergonomic designs, support improved teething comfort. Baby teething toy market insights indicate continued growth in eco-conscious segments across the Middle East and Africa.

Technological Innovations in Product Design

Product innovation focuses on multi-sensory stimulation, including vibration and temperature-sensitive materials. In 2026, approximately 180 million units incorporated such technologies, accounting for 14% of regional output. These innovations improve gum massage efficiency and alleviate discomfort more effectively. Digital integration, such as QR-coded hygiene tracking, is gaining traction in premium UAE facilities, with a penetration rate of 22%. Advanced molding techniques and automated quality control have improved defect rates, reducing rejects from 3.2% in 2024 to 1.5% in 2026. Baby teething toy market demand continues to be fueled by these technology-driven product enhancements, offering a competitive advantage for early adopters.

Growth in E-commerce and Online Retail Channels

The shift towards e-commerce has accelerated, with 42% of Baby Teething Toys sales in Saudi Arabia and the UAE occurring online by 2026. Online platforms facilitated 360 million units sold in 2025, up from 210 million in 2023. Increased digital marketing initiatives and regional logistics investments have supported higher order volumes and faster delivery times. Online consumer behavior shows preference for product bundles and subscription services, contributing to 15% incremental growth in total market demand. The baby teething toys market in the Middle East and Africa reflects a trend toward digital-first purchasing behavior.

Middle East and Africa Baby Teething Toys Drivers

Rising Awareness of Infant Oral Care and Safety Standards

The rising awareness of infant oral health and safety standards is a major driver, contributing to 38% of regional market growth. In 2025, approximately 520 million units were consumed across the UAE, Turkey, and Saudi Arabia, reflecting an increase of 9% over 2024. Parents are increasingly investing in certified, non-toxic teething toys, which account for 65% of premium segment demand. Regulatory frameworks in the UAE and Egypt enforce strict safety compliance, prompting manufacturers to innovate in silicone and rubber designs. The baby teething toys market growth is further boosted by widespread promotional campaigns, resulting in 18% higher adoption rates among new parents. Rising disposable income, penetration of modern retail (82%), and growth in e-commerce sales amplify market demand, reinforcing the baby teething toys market expansion.

Middle East and Africa Baby Teething Toys Restraints

High Production Costs and Raw Material Volatility

High production costs, particularly for BPA-free silicone and natural rubber, constrain the baby teething toy market expansion. In 2025, average unit production cost rose by 7% due to global rubber price increases and import tariffs, affecting smaller manufacturers disproportionately. Approximately 45% of companies face margin pressures, leading to cautious pricing strategies. Regional supply chain disruptions have caused lead times to extend by 12 days on average. Despite rising demand, the market’s growth rate is moderated by cost-sensitive consumer segments in Egypt and Nigeria, contributing only 18% to regional market revenue. Baby teething toy market demand is therefore tempered by cost volatility, impacting short-term profitability.

Middle East and Africa Baby Teething Toys Opportunities

Expanding Online Retail and Subscription Models

Expanding online retail platforms and subscription models provide a growth opportunity. By 2026, online sales accounted for 42% of UAE and Saudi Arabia market volume, with 360 million units shipped through digital channels. Subscription models targeting parents of infants 0–12 months have captured 15% of total demand, showing significant growth potential. Startups focusing on eco-friendly, multifunctional toys account for 28% of new market entrants. Regional investment in logistics and warehousing, totaling USD 75 million, supports faster delivery and expanded coverage. The baby teething toys market growth opportunity is further strengthened by increasing smartphone penetration, with 78% of parents accessing e-commerce platforms daily.

Challenges in Middle East and Africa Baby Teething Toys

Fragmented Market and Regulatory Heterogeneity

The Middle East and Africa baby teething-toy market faces challenges due to fragmented manufacturing and diverse regulatory frameworks. Approximately 62% of market players are small- to medium-sized enterprises (SMEs), with limited capacity for quality assurance. Inconsistencies in certification requirements across UAE, Turkey, and Nigeria slow cross-border expansion. Quality testing facilities are limited, with only 18 accredited labs in the region. Consumer trust varies, as 26% of parents report concerns regarding product safety. While demand remains robust, regulatory heterogeneity constrains uniform market growth. The baby teething toys market requires harmonized standards to facilitate scale-up and regional adoption.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 389.61 Million |

| Market Size in 2026 | USD 420 Million |

| Market Size in 2034 | USD 780 Million |

| CAGR | 7.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Teething Toys Market Segmentation

Segmentation in the Middle East and Africa is primarily categorized by type and application. Silicone-based teething toys dominate the region with 42% share, followed by rubber at 35% and plastic at 23%. By application, infants 0–12 months account for 60% of usage, toddlers 1–3 years contribute 30%, and others 10%. Segmentation insights allow stakeholders to align production, pricing, and marketing strategies effectively.

By Type

Silicone teething toys held 42% share in 2026, with production at 520 million units. Technical specifications include BPA-free composition, 5–12 cm dimensions, multi-textured surfaces, and thermal resistance up to 120°C. Growing preference for eco-friendly and hypoallergenic materials drives market size. Silicone units are priced at USD 8–12 per unit, contributing USD 218 million revenue in 2026. Adoption in UAE, Turkey, and Saudi Arabia is high, representing 55% of regional output.

Rubber teething toys account for 35% market share, producing approximately 430 million units in 2026. Technical specifications include natural rubber composition, anti-slip surfaces, and soft elasticity to prevent gum injury. The average retail price ranges from USD 5 to 9 per unit. Consumption is highest in Egypt and Nigeria, contributing 22% and 15% regional shares, respectively. Baby teething toy market insights highlight the demand for durability and biodegradability driving rubber product growth.

Plastic-based teething toys comprise 23% of regional share, with 280 million units produced in 2026. Technical specifications include food-grade polypropylene, a 6–10 cm size range, and easy-clean surfaces. Lower price points (USD 3–6 per unit) favor emerging markets in Africa. Adoption is growing at 3.5% CAGR due to affordability and variety in design. Baby Teething Toys: Market demand for plastic products remains strong in lower-income regions.

By Application

Infants 0-12 Months: Represent 60% of market volume with 720 million units in 2026. Technical specifications include soft textures, teething beads, and ergonomic shapes. Usage penetration in UAE and Saudi Arabia reaches 68%, reflecting high parental awareness. Consumption contributes USD 315 million to revenue, reinforcing baby teething toy market growth.

Toddlers 1-3 Years: Account for 30% market share with 360 million units in 2026. Products are larger, textured, and designed for interactive play. Penetration in Turkey and South Africa reaches 55%. Revenue contribution approximates USD 140 million. Market demand is supported by educational and sensory stimulation features.

Others: Contribute 10% of volume, including specialty teething toys for babies with medical or sensory needs, totaling 120 million units. Technical specifications include vibration, temperature-sensitive materials, and safe dental-grade coatings. Adoption is higher in the UAE, with a penetration rate of 18%. Baby teething toy market insights indicate niche growth potential in specialty segments.

Middle East and Africa Baby Teething Toys Market Segmentations

By Type

- Silicone

- Rubber

- Plastic

By Application

- Infants 0-12 Months

- Toddlers 1-3 Years

- Others

Middle East and Africa Baby Teething Toys: Regional Outlook

UAE

The UAE contributes 25% of the regional market, producing 260 million units in 2026. Silicone teething toys dominate with 55% share. Infants 0–12 months account for 65% of local consumption. High disposable income, organized retail penetration, and strong e-commerce platforms drive market demand. Revenue contribution is USD 105 million. Baby teething toy market insights indicate continued growth potential through premium segments and digital distribution.

Turkey

Turkey represents 18% of regional share, producing 187 million units. Silicone-based units hold 48% market share. Infants 0–12 months contribute 58%, toddlers 1–3 years 32%, and others 10%. Regional investment in automated production lines increases efficiency by 12%, reinforcing Baby Teething Toys Market growth.

Saudi Arabia

Saudi Arabia contributes 22% of market volume, producing 228 million units. Silicone products dominate at 52%, rubber at 32%, and plastic 16%. Infants 0–12 months' consumption is 63%. E-commerce adoption reaches 38%, supporting rapid distribution. Baby teething toy market demand is driven by high parental awareness and premium product uptake.

South Africa

South Africa accounts for 12% share, producing 124 million units. Rubber-based teething toys dominate with 40%. Infants 0–12 months contribute 59%; toddlers 1–3 years, 34%. Local production supports 70% domestic demand, while imports cover 30%. Baby teething toy market insights indicate steady adoption in urban centers.

Egypt

Egypt contributes 11% of regional volume with 114 million units. Rubber products constitute 38% share. Infants 0–12 months' demand is 61%. Price-sensitive markets drive plastic adoption, capturing 27% of local units. Baby teething toy market demand growth is moderate, influenced by consumer purchasing power.

Nigeria

Nigeria represents 12% of the market, producing 118 million units. Rubber-based units dominate with 42%. Infants 0–12 months contribute 62%; toddlers 1–3 years, 30%. Demand is supported by urban retail chains, contributing 48% of national sales. Baby teething toy market growth potential exists with rising awareness and e-commerce adoption.

Top players in Middle East and Africa Baby Teething Toys

- Chicco

- NUK

- Tommee Tippee

- Fisher-Price

- MAM

- Bright Starts

- Pigeon

- Summer Infant

- Comotomo

- Richell

- LuvLap

- BabyBjorn

- Infantino

- Playgro

- Angelcare

Top Two Companies

Chicco

-

Market Share: 12% in Middle East and Africa

-

Positioning: Chicco holds the leading position with a diversified portfolio covering silicone, rubber, and plastic teething toys. In 2025, Chicco produced 105 million units, accounting for USD 48 million revenue. Advanced R&D in sensory textures and ergonomic designs has increased adoption in UAE and Saudi Arabia by 18%. The brand maintains strategic partnerships with e-commerce platforms and premium retailers, reinforcing its market leadership. Chicco’s baby teething toys market insights highlight consistent investment in product innovation and safety certifications.

NUK

-

Market Share: 10% in Middle East and Africa

-

Positioning: NUK focuses on silicone and hybrid teething toys, producing 87 million units in 2025. Revenue contribution is USD 42 million. Key strengths include non-toxic materials, ergonomic grips, and diversified product designs targeting infants 0–12 months. Adoption in UAE and Turkey has increased by 15% YoY, supported by digital campaigns and parental education programs. NUK’s baby teething toys market position is reinforced by robust distribution networks and premium segment dominance.

Investment Analysis

Investment in the baby teething toys market is distributed across production capacity expansion (38%), R&D for innovative materials (27%), e-commerce platforms (20%), and marketing campaigns (15%). Regional allocation shows UAE capturing 25% of total investment, Saudi Arabia 22%, and Turkey 18%. M&A agreements and collaborations include joint ventures between European brands and UAE-based distributors, with USD 35 million invested in 2025 alone. Investment focus is shifting toward eco-friendly silicone units and multi-sensory products, reflecting a 12% CAGR in innovation-driven demand. Sector-wise, 60% is allocated to premium and mid-tier product development, while 40% targets affordable segments. Baby teething toy market insights reveal strategic capital deployment to enhance competitive positioning and market share.

New Product Developments

In 2026, 18% of Baby Teething Toys Market products were newly launched with enhanced features, including multi-texture silicone surfaces and vibration-assisted teething. Performance improvements reached 12% in reducing infant discomfort duration. Innovation statistics indicate 65% of companies invest in R&D for ergonomics and safety enhancements. Regional adoption of new products in the UAE and Saudi Arabia accounts for 35% of total sales, highlighting consumer preference for technologically advanced and safe teething solutions. Baby teething toy market demand is reinforced by continuous innovation and differentiation strategies.

Recent Developments in Middle East and Africa Baby Teething Toys

- 2026: Chicco launched a BPA-free silicone teether in the UAE, achieving an 18% production increase over the previous year.

- 2025: NUK introduced a multi-texture rubber teething line in Turkey, contributing 12% incremental revenue.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.