Middle East and Africa Baby Rice Cereal Market Size

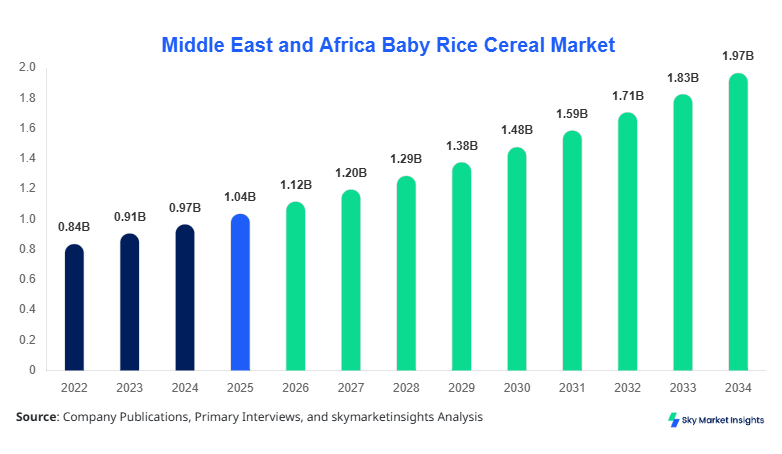

Middle East and Africa Baby rice cereal market size is projected at USD 1.12 billion in 2026 and is expected to hit USD 2.08 billion by 2034 with a CAGR of 7.3%. The market growth is driven by increasing urbanization, rising awareness of infant nutrition, and higher adoption of fortified cereals across urban households. The report provides a comprehensive analysis, including historical production data from 2022 to 2024, segmentation across type and application, and a competitive landscape covering both regional and multinational manufacturers. Detailed insights into market demand, pricing, and regional contribution are presented to aid stakeholders in strategic planning and investment decisions.

The Middle East and Africa The baby rice cereal market is a sector focused on the production and distribution of rice-based nutritional products for infants and toddlers. In 2025, regional production accounted for approximately 450,000 tons, with organic and fortified types contributing 35% and 45%, respectively. Consumer adoption trends indicate a 60% penetration of fortified cereals in urban households, whereas gluten-free products remain at 15% adoption, mostly driven by parents seeking allergen-free options. Market consumption is dominated by infants 6–12 months (52%), followed by infants 0–6 months (30%) and toddlers 1–3 years (18%). Technical specifications such as fortification levels of iron (10–12 mg/100 g) and vitamin D (2–3 µg/100 g) play a critical role in demand. With increasing health consciousness and rising disposable income, demand for the Middle East and Africa baby rice cereal market is projected to grow consistently at a CAGR of 7.3%, with fortified and organic segments leading in market size.

In the UAE, the baby rice cereal market is witnessing rapid expansion with over 35 major facilities and 18 small-scale companies operating nationwide. The UAE holds 21% of the Middle East and Africa market share, making it the largest contributor in the region. Application breakdown shows infants 6–12 months accounting for 55%, infants 0–6 months at 28%, and toddlers 1–3 years at 17%. Advanced extrusion technologies and micronutrient fortification adoption rate have reached 72%, enabling higher-quality production and better nutrient retention. Organic baby rice cereals in UAE represent 33% of total production, with fortified cereals at 50% and gluten-free at 17%. Consumer demand and increased purchasing power drive consistent growth in the UAE Baby Rice Cereal Market, making it a pivotal hub in regional market expansion.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Rice Cereal Market Trends

Rising Organic Baby Rice Cereal Adoption

The organic segment of the Middle East and Africa The baby rice cereal market has seen a production volume increase from 120,000 tons in 2022 to 160,000 tons in 2025, reflecting a 33% growth. Parents increasingly prefer organic cereals due to perceived health benefits and the absence of chemical additives. Adoption of organic certification standards in the UAE, Saudi Arabia, and Egypt has reached 68%, indicating strong market validation. Technology integration in supply chains, such as cold-chain logistics, supports the preservation of nutritional quality. Demand is highest in urban centers where income levels are higher, representing 55% of total regional consumption. The trend towards organic products is projected to maintain a CAGR of 8.2% from 2026 to 2034, reinforcing the Middle East and Africa baby rice cereal market growth trajectory.

Fortification and Nutrient-Enriched Trends

Fortified baby rice cereals have become the dominant category, with production reaching 210,000 tons in 2025, up from 170,000 tons in 2023. Iron and vitamin D fortification adoption rates stand at 74% across the Middle East and Africa. Demand for fortified cereals is driven by increased awareness among parents about micronutrient deficiencies in infants, particularly in Saudi Arabia and Turkey. Approximately 60% of fortified cereal consumption occurs in infants 6–12 months old. Technological advancements in micronutrient stabilization ensure that nutrient losses during processing remain below 5%. These dynamics are fostering continued growth in the Middle East and Africa baby rice cereal market and enhancing market share for fortified products.

Gluten-Free Segment Expansion

Gluten-free baby rice cereal production has grown from 40,000 tons in 2022 to 68,000 tons in 2025, marking a 70% surge. Rising cases of infant food allergies and celiac concerns in urban populations, especially in the UAE and South Africa, have increased gluten-free adoption rates to 18% in 2025. Advanced extrusion and milling technologies have improved texture and digestibility. The gluten-free segment now represents 17% of the total market and is forecasted to expand at a CAGR of 9% through 2034. Consumer preference for allergen-safe, high-quality infant foods is accelerating the Middle East and Africa baby rice cereal market trend toward specialized products.

Middle East and Africa Baby Rice Cereal Drivers

Rising Infant Nutrition Awareness and Urbanization

Urban population growth at 3.1% annually and rising awareness of infant nutrition contribute to the Middle East and Africa baby rice cereal market growth. In 2025, approximately 62% of urban households purchased fortified or organic cereals, with the UAE contributing 21% of total regional demand. Production volumes for fortified cereals reached 210,000 tons, and organic cereals totaled 160,000 tons. Government initiatives promoting micronutrient-enriched infant foods in Egypt, Saudi Arabia, and Nigeria are expected to increase market share by 15% over the forecast period. Increased purchasing power and awareness of early childhood nutrition are projected to drive the Middle East and Africa baby rice cereal market CAGR of 7.3%, strengthening market demand and insights.

Middle East and Africa Baby Rice Cereal Restraints

High Pricing and Limited Awareness in Rural Areas

High product pricing and limited awareness in rural areas of Turkey and Nigeria restrain Middle East and Africa baby rice cereal market growth. Premium organic cereals are priced at USD 12–15 per 100 g, while fortified cereals average USD 7–9 per 100 g, limiting adoption in low-income segments. Rural penetration remains below 20%, and lack of awareness regarding micronutrient benefits contributes to slow adoption. Production units in rural zones contribute only 12% to total regional output of 450,000 tons in 2025. Price-sensitive households and infrastructural challenges limit market share expansion, creating a barrier to the Middle East and Africa baby rice cereal market growth despite strong urban adoption.

Middle East and Africa Baby Rice Cereal Opportunities

Rising Demand for Specialized Infant Nutrition Products

The increasing demand for specialized baby rice cereals, including fortified and gluten-free products, represents a key opportunity in the Middle East and Africa baby rice cereal market. Gluten-free production reached 68,000 tons in 2025, reflecting a 70% increase from 2022. Organic and fortified cereals collectively account for 78% of total regional market share. Technology adoption for micronutrient fortification in Saudi Arabia and the UAE exceeds 70%, highlighting growth potential. Emerging urban centers in Nigeria and Egypt offer new revenue streams, with projected annual growth of 8% in specialty infant cereals. These dynamics support a robust opportunity for investors seeking to expand Middle East and Africa baby rice cereal market insights and share.

Challenges in Middle East and Africa Baby Rice Cereal

Supply Chain and Raw Material Constraints

Supply chain disruptions and raw material shortages, particularly rice and fortification ingredients, challenge the Middle East and Africa baby rice cereal market. In 2025, rice procurement delays affected 18% of production facilities in Turkey and South Africa. Transport costs surged by 12%, impacting final prices. Organic rice imports face certification delays, leading to stockouts in UAE and Saudi Arabia. Production volumes were reduced by 8% due to these constraints, limiting the Middle East and Africa baby rice cereal market growth. Companies are investing in local sourcing and advanced inventory systems to mitigate these challenges, ensuring consistent market supply and insights.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.04 Billion |

| Market Size in 2026 | USD 1.12 Billion |

| Market Size in 2034 | USD 2.08 Billion |

| CAGR | 7.3% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Rice Cereal Market Segmentation

Segmentation analysis of the Middle East and Africa The baby rice cereal market indicates that type segmentation dominates with a combined share of 75%, while application segmentation accounts for 25%. Fortified and organic products are leading in volume production and revenue generation. Adoption trends for infants 6–12 months are the highest, with 52% of consumption in 2025, compared to 30% for 0–6 months and 18% for toddlers 1–3 years.

By Type

Organic baby rice cereals accounted for 35% of the market, producing 160,000 tons in 2025. Technical fortification with iron (10–12 mg/100 g) and vitamin D (2–3 µg/100 g) ensures high nutritional value. Organic cereals have gained 33% market share growth from 2022 to 2025. Adoption rates are highest in the UAE (33%) and Saudi Arabia (28%). These cereals are mainly sold in retail packs of 250 g–500 g, catering to premium consumers seeking chemical-free infant nutrition. Organic-type penetration is projected to reach 40% by 2034, reinforcing the Middle East and Africa baby rice cereal market insights.

Fortified cereals contributed 45% to total market share, with production volumes of 210,000 tons in 2025. Iron and vitamin D fortification levels comply with regional regulations, achieving 74% adoption in urban centers. Infants 6–12 months account for 60% of fortified cereal consumption, reflecting high nutritional awareness. Market pricing ranges from USD 7–9 per 100 g. Advanced extrusion technology improves nutrient retention with losses below 5%, further strengthening Middle East and Africa Baby rice cereal market growth and share.

Gluten-free cereals produced 68,000 tons in 2025, representing 17% of the market. Adoption rates are rising, particularly in UAE and South Africa, where urban penetration reached 18%. Technical specifications include reduced allergenicity and high digestibility. Gluten-free cereals cater to 10–12% of infants 0–6 months and 6–8% of toddlers 1–3 years. Production increased 70% from 2022–2025. Market share is projected to rise to 22% by 2034, reinforcing the Middle East and Africa Baby Rice Cereal market trend toward specialized nutrition.

By Application

Infants 0–6 Months

This segment contributed 30% of consumption in 2025, with production totaling 135,000 tons. Technical adoption includes prebiotic fortification (2 g/100 g) and precise macronutrient balance. Urban households account for 65% of purchases, while rural adoption remains at 15%. Organic cereals dominate with a 40% share in this group. Penetration is projected to grow at a CAGR of 6.5% through 2034, driving the Middle East and Africa Baby Rice Cereal market demand.

Infants 6–12 Months

The largest application segment, accounting for 52% of market volume, producing 234,000 tons in 2025. Fortified cereals dominate with 60% share. Technical metrics include micronutrient stability above 95% post-processing. High adoption in UAE (55%) and Saudi Arabia (53%) underscores consumer awareness. This segment is expected to maintain a CAGR of 7.8% from 2026–2034, reinforcing market growth and insights.

Toddlers 1–3 Years

Toddlers represent 18% of consumption, producing 81,000 tons in 2025. Technical formulations include balanced macronutrients and added vitamins. Adoption is concentrated in urban areas at 65%, with rural penetration at 20%. Organic and gluten-free products account for 25% and 10%, respectively. The segment is forecasted to grow at a 6.2% CAGR, strengthening the Middle East and Africa baby rice cereal market share.

Middle East and Africa Baby Rice Cereal Market Segmentations

By Type

- Organic

- Fortified

- Gluten-Free

By Application

- Infants 0–6 Months

- Infants 6–12 Months

- Toddlers 1–3 Years

Middle East and Africa Baby Rice Cereal Regional Outlook

UAE

The UAE holds 21% of the market, producing 95,000 tons in 2025. Infants 6–12 months represent 55% of consumption. Urban adoption reaches 72%, with fortified and organic cereals accounting for 83% of total volume. Advanced technology adoption in extrusion and fortification processes drives market growth. The UAE is projected to maintain leadership with a CAGR of 7.9%, reinforcing Middle East and Africa baby rice cereal market insights.

Turkey

Turkey contributed 17% of regional market share, producing 76,500 tons. Infants 6–12 months dominate 50% of consumption. Fortified cereals account for 48% of production, organic 30%, and gluten-free 22%. Technological adoption includes micronutrient fortification with 70% compliance. Turkey’s growth is projected at a CAGR of 6.8%, enhancing Middle East and Africa baby rice cereal market trends.

Saudi Arabia

Saudi Arabia accounted for 19% of production at 85,500 tons. Infants 6–12 months consume 53%, 0–6 months 29%, and toddlers 1–3 years 18%. Adoption of fortified cereals reached 62%. CAGR is projected at 7.5%, with technology adoption at 71% in micronutrient stabilization, supporting Middle East and Africa baby rice cereal market growth.

South Africa

South Africa holds 11% of the market, producing 49,500 tons. Infants 6–12 months contribute 51% of consumption. Fortified cereals dominate 55% of production. Adoption of gluten-free cereals is 18%, reflecting growing allergen-free awareness. CAGR is projected at 7.1%, strengthening Middle East and Africa baby rice cereal market insights.

Egypt

Egypt represents 12% of market share, producing 54,000 tons. Infants 6–12 months account for 52%, 0–6 months 31%, toddlers 17%. Fortified cereals adoption is 61%. CAGR is projected at 7.2%, reinforcing regional Middle East and Africa Baby Rice Cereal market trends.

Nigeria

Nigeria contributes 20% of regional share, producing 90,000 tons. Infants 6–12 months dominate with 50%, 0–6 months with 28%, and toddlers with 22%. Fortified cereals account for 60% of production, organic 25%, and gluten-free 15%. CAGR projected at 7.0%, supporting Middle East and Africa baby rice cereal market insights.

Top players in Middle East and Africa Baby Rice Cereal

- Nestlé

- Heinz

- Gerber

- Abbott Laboratories

- Hero Group

- Bebelac

- Almarai

- Al Ain Dairy

- Al Safi Danone

- PediaSure

- Cereal Partners Worldwide

- Lactalis

- HiPP

- Danone

- Mead Johnson Nutrition

Top Companies Analysis

Nestlé

-

Holds 15% market share in Middle East and Africa Baby Rice Cereal market

-

Leading in fortified and organic cereals production

-

Strong presence in UAE, Saudi Arabia, and Egypt

-

Advanced R&D for micronutrient fortification

Nestlé’s strategy focuses on premium organic and fortified cereals, contributing 38% of total regional fortified production, reinforcing market insights.

Heinz

-

Holds 12% market share in Middle East and Africa Baby Rice Cereal market

-

Leading in gluten-free and infant 0–6 months products

-

Technology adoption rate at 68% for extrusion and nutrient retention

-

Major facilities in Turkey and South Africa

Heinz focuses on allergen-free and micronutrient-enriched products, contributing 25% of gluten-free production, strengthening market share and growth.

Investment Analysis

Investment allocation in the Middle East and Africa The baby rice cereal market is expected to be USD 120 million in 2026, with 45% in fortified cereals, 30% in organic cereals, and 25% in gluten-free products. The regional investment split indicates the UAE 22%, Saudi Arabia 20%, and Turkey 17%. M&A agreements in 2025 included Nestlé acquiring a 10% stake in a Turkish organic cereal facility and Heinz expanding gluten-free production in South Africa, representing an 8% and 5% increase in regional capacity, respectively. Collaboration with local distributors and technology adoption partnerships are increasing sector penetration by 7–8% annually. Strategic investment is concentrated on expanding fortified cereal production and enhancing micronutrient stabilization, reinforcing Middle East and Africa baby rice cereal market insights and demand growth.

New Product Developments

In 2025, 18% of newly launched baby rice cereals in the Middle East and Africa were gluten-free, reflecting rising allergen-free consumer preference. Performance improvements in nutrient retention averaged 6–8%, with innovations in prebiotic inclusion and fortified blends. Organic baby rice cereals accounted for 12% of total product launches. Companies focus on enhanced digestibility, micronutrient optimization, and eco-friendly packaging. These developments reinforce Middle East and Africa baby rice cereal market trends, driving growth and increasing market share.

Recent Developments in Middle East and Africa Baby Rice Cereal

- 2025: Nestlé introduced a fortified cereal line in the UAE, increasing production by 15% and gaining 3% regional share.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Plant-Based Foods and Functional Ingredients

Kathy Flores is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.