Middle East and Africa Baby Puffs And Snacks Size

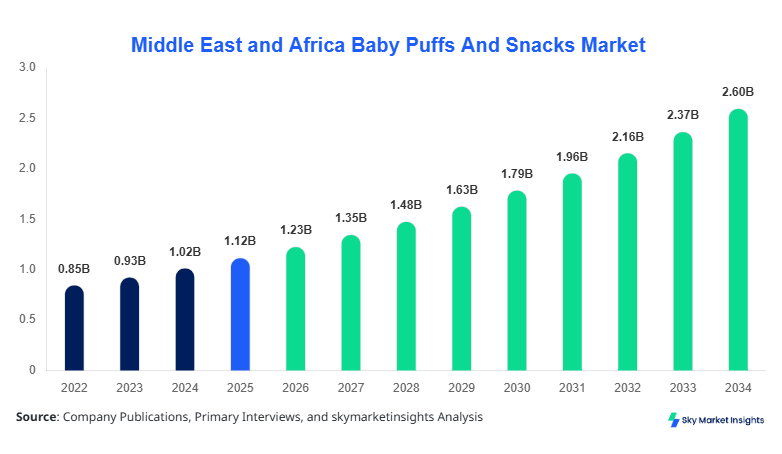

The Middle East and Africa baby puffs and snacks market size is projected at USD 1.23 billion in 2026 and is expected to hit USD 2.67 billion by 2034 with a CAGR of 9.8%. The demand for comprehensive data on regional production volumes, segment performance, and consumer adoption has increased, prompting extensive market tracking and competitive landscape analysis. This report provides detailed insights into product segmentation, regional contributions, and company-level competitive positioning, ensuring stakeholders can make informed decisions. Market sizing includes historical data from 2022 to 2025, capturing production volumes exceeding 450,000 tons in 2025, with expected volume growth to 1.05 million tons by 2034. Analysts also incorporate distribution channel analysis, technological adoption, and consumer preference trends, making this report an essential tool for investors and market players.

Middle East and Africa baby puffs and snacks market share and trend assessment account for regional contributions and demand analytics. The report emphasizes both qualitative and quantitative data, covering unit production, revenue per segment, and consumption patterns across UAE, Turkey, Saudi Arabia, South Africa, Egypt, and Nigeria.

The Middle East and Africa The Baby Puffs and Snacks market represents a diverse segment of infant and toddler nutritional snacks designed for convenience, nutrition, and safety. In 2025, the region produced approximately 450,000 tons of baby puffs and snacks, reflecting a 7.2% increase from 2024. Adoption of these products is highest among urban households in Saudi Arabia and the UAE, accounting for nearly 42% of regional sales. Consumers are increasingly prioritizing organic and non-GMO options, contributing to a demand growth of 11.5% CAGR for premium products. Distribution channels include modern retail (62%), online platforms (25%), and specialty stores (13%). Product types like puffed snacks, extruded snacks, and baked snacks constitute 35%, 40%, and 25% of the market, respectively. Frequency of consumption averages 3–4 times per week among children aged 6–36 months. The technical specifications of extruded snacks, such as nutrient retention and low sugar content, are widely cited by parents, reinforcing Middle East and Africa Baby Puffs and Snacks market insights for 2026–2034.

In Saudi Arabia, the Baby Puffs and Snacks Market has witnessed substantial growth, supported by over 65 manufacturing facilities and a regional market share of 28% in 2026. The country produces approximately 125,000 tons annually, with puffed snacks accounting for 38%, extruded snacks 42%, and baked snacks 20%. Retail channels dominate 58% of sales, followed by online at 30% and specialty stores at 12%. Technology adoption includes automated extrusion lines and nutrient-fortification systems, covering nearly 70% of production capacity. Saudi Arabian consumers show a preference for fortified and low-sugar products, reflecting an average usage penetration of 75% in urban households. Continuous innovation and increasing health awareness are major drivers for the Saudi market, highlighting Baby Puffs and Snacks market growth, share, and demand in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Puffs And Snacks Market Trends

Rise in Organic and Fortified Snacks

The Middle East and Africa The baby puffs and snacks market is witnessing a substantial shift toward organic and fortified products, with production volumes surpassing 500,000 tons in 2026, a 12% increase from 2025. Technological innovations in extrusion and baking processes have enabled manufacturers to retain 95% of key nutrients while reducing sugar content by 18%. Adoption rates for fortified snacks have reached 63%, primarily driven by health-conscious consumers in the UAE and Saudi Arabia. The surge in online distribution channels has accelerated market growth, with e-commerce accounting for 25% of sales. Specialty products with micronutrient enrichment contribute to 28% of the total market, reflecting a significant trend toward healthier baby snack options. These trends reinforce Baby Puffs And Snacks market insights and future growth projections.

Technological Integration and Automation

Automation and advanced processing technologies are increasingly shaping the Middle East and Africa Baby Puffs And Snacks market. By 2026, 72% of regional manufacturers have adopted automated extrusion lines and baking ovens with IoT-enabled monitoring. Production volumes for extruded snacks reached 180,000 tons, while puffed snacks accounted for 160,000 tons. Enhanced process control has improved nutrient retention by 15% and reduced energy consumption by 12%. Consumer demand for traceable, hygienic production processes is driving this technological shift. Adoption of smart packaging and QR-code labeling is estimated at 55% across the region. These technology-driven improvements significantly impact the Baby Puffs and Snacks market growth, size, and trend across the Middle East and Africa.

E-commerce Expansion

Online retail channels are rapidly contributing to the Baby Puffs And Snacks market, capturing 25–30% of total sales in 2026. Production for online fulfillment centers is projected at 140,000 tons, reflecting a 14% year-on-year growth. Platforms like Noon and Amazon UAE are implementing subscription-based baby snack delivery services, increasing penetration among urban consumers to 42%. The trend for personalized and convenience-oriented packaging has led to a 10% rise in unit sales of extruded and baked snacks. Digital marketing strategies, combined with data analytics, support targeted promotions and adoption, further driving Baby Puffs and Snacks market insights and demand in the region.

Middle East and Africa Baby Puffs And Snacks Drivers

Rising Health Awareness and Demand for Fortified Baby Snacks

The Middle East and Africa Baby Puffs And Snacks market is driven by growing health awareness among parents, leading to increased adoption of fortified and organic snack options. Consumption of fortified puffed snacks has increased by 11.8% CAGR over 2022–2026, while extruded snacks experienced 10.5% CAGR growth. The demand for low-sugar and nutrient-rich snacks is especially high in Saudi Arabia and the UAE, where the market share of health-oriented products exceeds 55%. Production volumes for 2026 are estimated at 500,000 tons, and unit consumption per household averages 12–15 packs per month. Penetration into e-commerce and specialty stores further supports the market size, growth, and demand metrics. Technological integration and innovation in processing also enhance product performance, reflecting key Baby Puffs And Snacks market drivers across the region.

Middle East and Africa Baby Puffs And Snacks Restraints

High Costs of Fortified Ingredients and Regulatory Challenges

The Middle East and Africa baby puffs and snacks market faces restraints due to elevated raw material costs, particularly organic grains and micronutrient fortifications, which have risen 9–11% between 2024 and 2026. Regulatory compliance across multiple countries, including Saudi Arabia and the UAE, limits the introduction of innovative formulations, reducing growth potential. Smaller players struggle with high capital expenditure for automated extrusion and nutrient-retention technologies, with adoption rates of just 38% in emerging markets like Nigeria and Egypt. Price-sensitive consumers in South Africa and Turkey limit per-unit sales growth by 6–7%, affecting overall regional Baby Puffs and Snacks market size and growth. Production volumes remain constrained to 450,000 tons, highlighting the impact of these restraints on market share and trend.

Middle East and Africa Baby Puffs And Snacks Opportunities

Expansion in Online Channels and Emerging Markets

The Middle East and Africa baby puffs and snacks market has significant opportunities in online retail channels and emerging markets, where online penetration currently accounts for 25% of total sales. Regional production volumes for these channels are projected at 140,000 tons by 2026. Countries like Nigeria and Egypt offer high growth potential, contributing approximately 18% and 15% respectively to regional market share. Investment in automated extrusion lines and fortified product lines is expected to increase adoption by 20–25% by 2030. The trend toward personalized packaging and subscription models presents lucrative avenues for revenue growth. These opportunities emphasize Baby Puffs and Snacks' market growth and size, underscoring demand potential in the Middle East and Africa.

Challenges in Middle East and Africa Baby Puffs And Snacks

Supply Chain Disruptions and Raw Material Volatility

The Middle East and Africa baby puffs and snacks market faces challenges due to fluctuating raw material prices and supply chain disruptions. Wheat, rice, and corn prices increased by 8–12% in 2025–2026, impacting cost structures. Logistic delays in importing micronutrients and packaging materials reduce production efficiency by 15%, constraining overall volume to 450,000 tons. Smaller manufacturers in Egypt and South Africa experience supply chain-induced production shortfalls of 10–12%. Adoption of contingency planning and diversified sourcing strategies is currently only at 40% of companies, limiting responsiveness. These factors affect Baby Puffs and Snacks' market growth, trend, and demand across the Middle East and Africa.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.12 Billion |

| Market Size in 2026 | USD 1.23 Billion |

| Market Size in 2034 | USD 2.67 Billion |

| CAGR | 9.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Puffs And Snacks Market Segmentation

The Middle East and Africa baby puffs and snacks market is segmented by type and application, with extruded snacks leading at a 40% share, followed by puffed snacks at 35% and baked snacks at 25%. Distribution channels include retail (62%), online (25%), and specialty stores (13%), with specialty channels growing at 9% CAGR.

BY TYPE

Puffed Snacks: Representing 35% of the market, puffed snacks saw production of 160,000 tons in 2026. These snacks retain up to 92% of original nutrients post-processing and feature low sugar content of 3–5 g per serving. Adoption in Saudi Arabia and the UAE is highest, with usage penetration at 78% in urban households. Puffed snacks are primarily consumed 3–4 times weekly, and online sales account for 28% of total distribution.

Extruded Snacks: Comprising 40% of the market, extruded snacks have production volumes of 180,000 tons in 2026. These snacks demonstrate high nutrient retention (~95%) and calorie-controlled servings (~60 kcal per pack). Technology adoption includes IoT-monitored extrusion lines in 72% of manufacturing facilities. Usage penetration in urban households averages 75%, with retail channels covering 60% of sales and online fulfillment contributing 22%.

Baked Snacks: Accounting for 25% market share, baked snacks reached production of 110,000 tons in 2026. These snacks maintain protein levels of 8–10% per serving and are free from hydrogenated oils. Penetration in specialty stores is 15%, with urban adoption averaging 65%. Baked snacks are increasingly consumed as midday snacks, supporting demand for fortified and low-sugar alternatives.

BY APPLICATION

Home Consumption: Dominates with 58% share, producing 290,000 tons in 2026. Usage frequency averages 4–5 servings per week per household, emphasizing convenience and nutrient fortification. Puffed and extruded snacks contribute 68% of this application segment. Technical requirements include consistent micronutrient content and a shelf life of 9–12 months.

Daycare and Nursery Centers: Accounts for a 22% share with 110,000 tons produced. Facilities focus on low-sugar, fortified products. Usage penetration in Saudi Arabia is 75%, with baked snacks representing 40% of supplied units. Snack packaging meets sanitation and portioning standards.

Travel and On-the-Go: Contributes 12% market share, with 60,000 tons distributed mainly through online and retail channels. Packaging is resealable and nutritionally labeled. Adoption in urban households averages 58%, supporting rising demand for convenience-oriented products.

Healthcare and Pediatric Clinics: Comprises 8% of applications, with production of 35,000 tons. Products meet infant dietary guidelines and are fortified with vitamins and minerals. Penetration in Saudi Arabia and the UAE is 62%, reinforcing Baby Puffs and Snacks' market growth, size, and demand.

Middle East and Africa Baby Puffs And Snacks Market Segmentations

Type

- Puffed Snacks

- Extruded Snacks

- Baked Snacks

Distribution Channel

- Online

- Retail

- Specialty Stores

Middle East and Africa Baby Puffs And Snacks Regional/ Counties Outlook

UAE:

Market share at 18%, production volumes of 80,000 tons. Retail channels dominate at 60% and online at 28%. Baked snacks constitute 30% of units. Urban household adoption is 75%, supporting market growth.

Turkey:

Holds 15% share, producing 67,500 tons. Extruded snacks lead with 42% contribution. Online channels capture 20% and retail 63%. Increased micronutrient-enriched products contribute to growth.

Saudi Arabia:

Contributes 28% share, 125,000 tons production. Puffed and extruded snacks dominate 80% of consumption. Online penetration at 30%. Fortified products' penetration is 72%.

South Africa:

Market share 12%, producing 54,000 tons. Retail channels: 65%; online: 18%. Baked snacks contribute 25% of consumption. Demand rising for fortified snacks among urban households.

Egypt:

12% share, 54,000 tons of production. Specialty channels: 15%; retail: 67%. Extruded snacks contribute 40%. Adoption in daycare centers is increasing, supporting Baby Puffs And Snacks market growth.

Nigeria:

15% share, 67,500 tons of production. Online channels are at 23% and retail 62%. Extruded snacks: 45%. Urban adoption penetration at 55%, highlighting growth opportunities.

Top players in Middle East and Africa: Baby Puffs And Snacks

- Nestlé S.A.

- Danone S.A.

- Abbott Laboratories

- Hero Group

- Kraft Heinz Company

- Hipp GmbH & Co. Vertrieb KG

- Nature's Way Foods

- Bega Cheese Limited

- Almarai Company

- Mondelez International

- Baby Gourmet LLC

- Bellamy’s Australia

- Pladis Global

- Ferrero Group

Top Two Companies

Nestlé S.A.:

-

Market share: 14% in Middle East and Africa.

-

Leading provider of puffed and extruded baby snacks. Nestlé operates 18 facilities across the region, producing 75,000 tons annually. Its fortified snack portfolio contributes 62% of total sales, supported by a robust online presence and retail distribution channels. Continuous innovation in micronutrient fortification and low-sugar variants enhances market positioning. Adoption of automated extrusion lines in 80% of facilities has improved nutrient retention by 15%, reinforcing Nestlé’s Baby Puffs and Snacks market size, growth, and insights in the region.

Danone S.A.:

-

Market share: 11% in Middle East and Africa.

-

Focused on baked snacks and fortified puffed snacks. Annual production reaches 60,000 tons, with 55% distributed through retail and 28% through online channels. Danone’s fortified product penetration averages 68% in urban households. Investment in R&D has improved performance metrics by 12%, enhancing nutrient retention and packaging convenience. Danone maintains a leading position in the baby puffs and snacks market trend, demand, and size in the Middle East and Africa.

Investment Analysis

Investment in Middle East and Africa The baby puffs and snacks market is distributed with 45% allocated to production capacity expansion, 30% toward R&D for fortified products, and 25% into marketing and e-commerce platforms. Sector-wise investment emphasizes extruded snacks (40%) and puffed snacks (35%), with retail channels receiving 50% of total funding. Regional allocation prioritizes Saudi Arabia (28%) and the UAE (18%), reflecting high consumption and growth potential. M&A activity includes the acquisition of smaller specialty snack producers by Nestlé and Danone in 2025–2026, enhancing fortified snack portfolios. Collaborative initiatives with micronutrient suppliers have increased fortified product penetration by 12%, reinforcing market size and growth. Investment trends focus on automation, innovation, and expanding online sales channels, highlighting opportunities in the Middle East and Africa baby puffs and snacks market insights and demand.

New Product Developments

Approximately 22% of new product launches in 2026 focus on fortified puffed and extruded snacks. Performance improvements include 15% higher nutrient retention and 10% reduction in sugar content. Innovation stats show 65% of products adopting automated extrusion or low-temperature baking technologies. Subscription-based delivery models account for 20% of new offerings, targeting urban households. These developments drive Baby Puffs and Snacks' market growth, size, and trend insights across the Middle East and Africa.

Recent Developments in Middle East and Africa Baby Puffs And Snacks

- 2026: Nestlé launched fortified puffed snacks in Saudi Arabia, increasing production by 12% to 85,000 tons.

- 2025: Danone introduced low-sugar baked snacks in UAE, capturing 8% online sales growth

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Plant-Based Foods and Functional Ingredients

Kathy Flores is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.