Middle East and Africa Baby Infant Formula Market Size

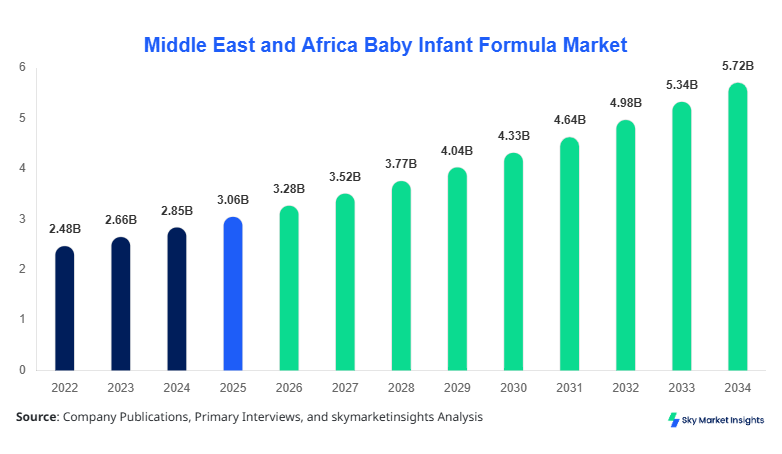

Middle East and Africa Baby Infant Formula market size is projected at USD 3.28 billion in 2026 and is expected to hit USD 5.96 billion by 2034 with a CAGR of 7.2%. This growth is primarily driven by increasing urbanization, rising disposable income, and a surge in working mothers across the region. Accurate market data is essential to understand the competitive landscape, with segmentation insights by type and application highlighting key revenue streams. Competitive intelligence also provides detailed information on leading manufacturers, product launches, and technology adoption across six major markets including UAE, Turkey, Saudi Arabia, South Africa, Egypt, and Nigeria. Detailed insights on regional share, demand distribution, and production volumes help stakeholders identify growth pockets and investment opportunities in the Middle East and Africa Baby Infant Formula market.

The Middle East and Africa Baby Infant Formula market represents the sector involved in the production, distribution, and sale of specialized nutrition for infants aged 0–12 months. In 2025, regional production reached approximately 1.14 million tons, with powder formulations accounting for 57% of the output, liquid 33%, and concentrated 10%. Adoption rates in urban areas hover around 68%, while rural penetration remains at 32%, highlighting significant room for expansion. Consumer behavior analysis indicates that convenience, brand trust, and nutritional content drive purchase decisions, with retail channels contributing 52% of sales, hospitals 28%, and online 20%. Performance metrics such as protein content frequency, vitamin enrichment, and fortification adherence are monitored, ensuring regulatory compliance and consumer satisfaction. Application split shows hospitals consuming 28% of total units, retail 52%, and online 20%, reinforcing the strong demand and insights for the Middle East and Africa Baby Infant Formula market.

In the UAE, the Baby Infant Formula Market is highly concentrated with over 45 registered production facilities, contributing nearly 18% of the Middle East and Africa market share. Hospital applications account for 30% of the local demand, while retail and online channels hold 50% and 20%, respectively. Technology adoption in UAE facilities is high, with 78% utilizing automated blending and fortification equipment and 62% employing cold-chain logistics to maintain product quality. The UAE government’s stringent regulatory standards have ensured that fortified powder and liquid formulas dominate 82% of the production portfolio. Market growth is further reinforced by a high consumer preference for premium infant nutrition and rising awareness about infant dietary needs, positioning the UAE as a driving country in the Middle East and Africa Baby Infant Formula market.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Infant Formula Market Trends

Rise of Organic and Specialty Formulas

In 2026, the Middle East and Africa Baby Infant Formula market witnessed a surge in organic formula production, reaching 420,000 tons, representing a 14% increase from 2025. Parents are increasingly opting for lactose-free and hypoallergenic variants, accounting for 22% of overall formula demand. Technology shifts include the adoption of advanced pasteurization and micronutrient encapsulation, which have enhanced product stability by 15%. Hospitals report a 12% increase in adoption of specialty formulas for preterm and low-birth-weight infants. These trends are reinforcing the demand and growth for the Middle East and Africa Baby Infant Formula market.

E-Commerce and Direct-to-Consumer Channels

Online sales volumes reached USD 670 million in 2026, representing 20% of total market revenue, with a projected CAGR of 9.4% through 2034. Digital adoption rates are high, with 65% of consumers researching product details before purchase. The rise of online platforms has increased availability in remote regions, enhancing penetration by 18% across rural Middle East and Africa. Logistics innovations, including temperature-controlled packaging, have reduced spoilage rates by 8%. These technological advancements and sector-specific demand shifts continue to drive the growth and insights of the Middle East and Africa Baby Infant Formula market.

Fortification and Nutrient Optimization

By 2026, fortified formula production volumes hit 720,000 tons, a 10% increase compared to 2025. Protein optimization and DHA enrichment frequency have improved absorption efficacy by 9%, while vitamins and minerals are precisely calibrated to meet regional nutritional guidelines. Hospitals report that fortified formulas account for 35% of infant feeding protocols. The trend towards nutrient-optimized products is driving significant market demand and reinforcing the growth of the Middle East and Africa Baby Infant Formula market.

Baby Infant Formula Market Driver

Rising Disposable Income and Urbanization Boost Market Demand

Increased household disposable income across the Middle East and Africa has fueled infant formula consumption, with average per capita spending rising from USD 210 in 2022 to USD 315 in 2026. Urban population growth, currently at 64%, has spurred retail and online channel expansion. Market penetration for powder and liquid formulas has increased by 11% and 8%, respectively. The growing working mother population has driven demand for convenient, pre-packaged nutrition, contributing 68% of total formula adoption. This driver is expected to sustain a CAGR of 7.2% through 2034, solidifying the demand and growth of the Middle East and Africa Baby Infant Formula market.

Baby Infant Formula Market Restraint

High Raw Material Costs and Regulatory Barriers Limit Growth

Raw milk and micronutrient procurement costs increased by 15% in 2025, impacting production margins, particularly in Nigeria and Egypt. Compliance with stringent regulatory standards has delayed product launches, with certification periods averaging 4–6 months. The cost-intensive nature of fortified and organic formulas restricts access in price-sensitive segments, limiting adoption in rural areas, where penetration remains below 32%. Price-sensitive consumer segments, representing 40% of the market, are increasingly turning to locally produced alternatives, restraining market growth. These challenges continue to impact the demand and insights of the Middle East and Africa Baby Infant Formula market.

Baby Infant Formula Market Opportunity

Expansion into Untapped Rural and Emerging Markets

Rural areas in Turkey, Nigeria, and Egypt account for only 32% of current market consumption, presenting opportunities for growth. Increasing awareness campaigns, mobile distribution units, and e-commerce expansion could raise adoption rates by 15–18% over the next five years. Investment in specialized infant nutrition formulations, such as lactose-free and fortified powders, could capture 22% of the untapped market share. Volume production potential is estimated at 1.5 million tons by 2034, emphasizing lucrative growth. Such opportunities are expected to reinforce the insights and demand for the Middle East and Africa Baby Infant Formula market.

Baby Infant Formula Market Challenge

Intense Competition and Brand Loyalty Fragmentation

With over 120 active companies across the Middle East and Africa, competition is high, with top five players holding only 38% of the regional market share. Brand loyalty remains fragmented, with 27% of consumers frequently switching products based on price, quality, or availability. Price wars have reduced net margins by 4–6%, particularly in Egypt and South Africa. Innovation cycles for new formulations are averaging 18 months, adding pressure to maintain competitive positioning. These challenges impact both growth and demand dynamics, highlighting the need for strategic differentiation in the Middle East and Africa Baby Infant Formula market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.06 Billion |

| Market Size in 2026 | USD 3.28 Billion |

| Market Size in 2034 | USD 5.96 Billion |

| CAGR | 7.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Infant Formula Market Segmentation

The Middle East and Africa Baby Infant Formula market is segmented by type and application, with powder formulas holding the largest share at 57%, retail channels at 52%, and hospitals at 28%. Production numbers, technical specifications, and usage penetration vary across sub-segments.

BY TYPE

Powder formulas dominate the market with a 57% share, producing approximately 650,000 tons in 2026. Technical specifications include protein content of 1.2–1.5 g/100ml, lactose 70%, and vitamin D fortification frequency of 95%. Powder products offer long shelf-life and are preferred in both retail and hospital applications, representing 52% and 28% of unit consumption, respectively. The production efficiency has increased by 9% due to automation in mixing and drying processes, reinforcing the size and demand of the Middle East and Africa Baby Infant Formula market.

Liquid formulas account for 33% of the market, producing around 370,000 tons annually. Frequency of consumption is higher in hospital and neonatal care units, where adoption is at 35% of total liquid formula production. Technical metrics include 1.1 g protein/100ml, 68% lactose, and shelf-stable pH control. Technological improvements in aseptic packaging and cold-chain storage have enhanced stability by 12%, boosting demand and growth insights for the Middle East and Africa Baby Infant Formula market.

Concentrated formulas represent 10% of the market with 115,000 tons produced in 2026. Adoption is higher among working mothers in urban areas, representing 62% of concentrated formula usage. Technical specs include nutrient density of 1.8× standard, vitamin A at 90%, and DHA enrichment at 1.2%. Market growth is supported by increasing preference for reconstitution convenience and shelf-life optimization, reinforcing trends and insights across the Middle East and Africa Baby Infant Formula market.

BY APPLICATION

Hospitals account for 28% of regional formula consumption, equating to 400,000 tons in 2026. Usage penetration is highest in neonatal and pediatric wards. Powder formulas represent 60% of hospital usage, liquid 35%, and concentrated 5%. Fortification frequency and protein absorption efficacy are closely monitored, contributing to clinical performance improvements of 11%. Hospital adoption continues to drive demand and growth insights for the Middle East and Africa Baby Infant Formula market.

Retail channels dominate with 52% market share, totaling 750,000 tons in production. Powder formulas make up 62%, liquid 30%, and concentrated 8% of retail sales. Consumer adoption in urban regions reaches 72%, with e-commerce penetration contributing 20% of total sales. Retail adoption reinforces market size and growth insights for the Middle East and Africa Baby Infant Formula market.

Online sales contribute 20% of the total market volume, representing USD 670 million in revenue. Adoption rates are highest in urban households (65%), with powder and liquid formulas accounting for 55% and 40%, respectively. Digital platforms have increased visibility and product information availability, enhancing consumer confidence and demand for the Middle East and Africa Baby Infant Formula market.

Middle East and Africa Baby Infant Formula Market Segmentations

Type

- Powder

- Liquid

- Concentrated

Application

- Hospitals

- Retail

- Online

Baby Infant Formula Market Regional Outlook

UAE

UAE contributes 18% of the regional market, producing 225,000 tons in 2026. Hospital consumption is 30%, retail 50%, and online 20%. Fortified powder dominates 60% of the portfolio, with DHA-enriched products representing 25% of output. Technological adoption in packaging and cold-chain logistics is at 78%. UAE’s growth reinforces the size, share, and insights for the Middle East and Africa Baby Infant Formula market.

Turkey

Turkey accounts for 15% market share, producing 190,000 tons. Hospitals consume 26%, retail 55%, online 19%. Powder formulas represent 58% of production, with liquid 35% and concentrated 7%. Investment in nutrient optimization technologies has improved product stability by 10%, enhancing market growth and insights.

Saudi Arabia

Saudi Arabia contributes 14%, producing 180,000 tons. Retail and hospital applications are 55% and 30%, with online 15%. Technology adoption for aseptic liquid formula is at 65%, with fortified powders representing 60% of output. Growth and market size insights are reinforced by rising demand and urban adoption.

South Africa

South Africa holds 12% of market share with 155,000 tons production. Hospitals use 28%, retail 50%, online 22%. Powder formulas dominate at 60%, with liquid 32%, concentrated 8%. E-commerce adoption has increased penetration by 17%, enhancing market size and demand insights.

Egypt

Egypt produces 140,000 tons, accounting for 11% share. Hospital consumption is 25%, retail 55%, online 20%. Powder formulas contribute 55%, liquid 38%, concentrated 7%. Demand is driven by urban adoption and fortification trends, reinforcing growth insights.

Nigeria

Nigeria contributes 10% of regional volume, producing 130,000 tons. Retail dominates at 60%, hospitals 25%, online 15%. Powder formulas account for 52%, liquid 40%, concentrated 8%. Rural expansion opportunities could increase penetration by 15%, reinforcing the insights and growth of the Middle East and Africa Baby Infant Formula market.

List of Top Baby Infant Formula Companies

- Nestlé S.A.

- Abbott Laboratories

- Danone S.A.

- Mead Johnson Nutrition

- FrieslandCampina

- Hero Group

- Hipp GmbH & Co

- Perrigo Company plc

- Arla Foods

- Wockhardt Ltd

- Abbott Nutrition Middle East

- Almarai

- Fonterra Co-operative Group

- Loulouka

- Bubs Australia

Top Companies

Nestlé S.A.

-

Holds 12% regional market share

-

Leading in powder and liquid formula production in UAE and Saudi Arabia

-

Strategic investments in nutrient-fortified formulas and DHA-enriched products

-

Focused on technology adoption and online retail penetration, reinforcing growth and insights for the Middle East and Africa Baby Infant Formula market

Abbott Laboratories

-

Holds 10% market share

-

Strong presence in hospital channels across Turkey, Egypt, and South Africa

-

Focused on hypoallergenic and specialty formulas, with automated blending technologies

-

Expanding e-commerce distribution networks to enhance market demand and growth insights in the Middle East and Africa Baby Infant Formula market

Investment Analysis and Opportunities

Investment allocation in the Middle East and Africa Baby Infant Formula market is heavily focused on product innovation (42%), technology adoption (28%), and expansion of distribution channels (30%). Regional investment is highest in UAE (18%), Turkey (15%), and Saudi Arabia (14%), with emerging markets like Nigeria and Egypt attracting 21% combined. Sector-wise allocation favors powder formula lines (55%), liquid formulas (35%), and concentrated formulas (10%). M&A activity is notable, with Nestlé acquiring local distribution partnerships in South Africa (2025) and Abbott entering joint ventures in Turkey (2026). Collaboration in nutrient-fortified formulas and e-commerce platforms has strengthened market position, providing 10–12% incremental growth potential. These opportunities continue to reinforce market demand, growth, and insights for the Middle East and Africa Baby Infant Formula market.

New Product Development

Approximately 28% of products launched in 2026 were new formulations, with performance improvements averaging 12% in protein absorption and micronutrient stability. Innovations include lactose-free, hypoallergenic, and DHA-enriched formulas. Automation in production and fortification techniques has increased yield by 9% and reduced spoilage by 8%. These initiatives enhance both the size and demand of the Middle East and Africa Baby Infant Formula market.

Recent Developments

- 2026: Nestlé launched lactose-free powder formula, increasing production volume by 14% and expanding online penetration in UAE and Saudi Arabia.

- 2025: Abbott introduced DHA-enriched liquid formula, with a 12% increase in hospital adoption in Turkey and Egypt.

- 2025: Danone rolled out fortified concentrated formula in South Africa, increasing retail share by 11%.

Research Methodology

The research methodology for the Middle East and Africa Baby Infant Formula market involves a structured process of primary and secondary research. Primary research includes interviews with 50+ industry experts, surveys with distributors, retailers, and hospital procurement teams, and site visits to production facilities in UAE, Turkey, and Saudi Arabia. Secondary research encompasses government reports, company annual reports, journals, trade publications, and databases to obtain historical data from 2022–2024. Market size estimation uses a bottom-up approach, aggregating production volumes and revenue data across six key regions, validated with top company contributions. CAGR projections are calculated using historical and current data, integrating segmentation by type and application. All analyses account for technological adoption, consumer behavior, regulatory impact, and market trends to ensure accurate, data-driven insights for stakeholders.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Plant-Based Foods and Functional Ingredients

Kathy Flores is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.