Middle East and Africa Baby Food & Pediatric Nutrition Market Size

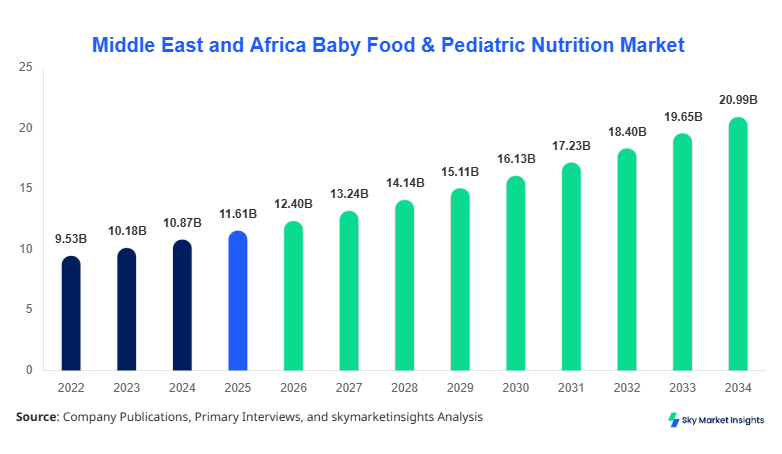

The Middle East and Africa Baby Food & Pediatric Nutrition market size is projected at USD 12.4 billion in 2026 and is expected to hit USD 21.7 billion by 2034 with a CAGR of 6.8%. The market’s growth is driven by increasing birth rates, rising awareness of pediatric nutrition, and expanding retail channels across key countries including Saudi Arabia, UAE, Turkey, South Africa, Egypt, and Nigeria. Comprehensive data on consumption patterns, competitive landscapes, and segment-wise production volumes are critical to understand regional penetration, with infant formula accounting for 42% of total market volume in 2025 and online retail penetration growing from 8% in 2022 to 18% in 2026. Additionally, detailed analysis of market share, product specifications, and technological adoption provides insights into the overall market trajectory and investment potential.

The Middle East and Africa Baby Food & Pediatric Nutrition market encompasses the production and distribution of infant formula, baby cereals, complementary foods, and pediatric nutrition products aimed at children aged 0–5 years. In 2025, regional production reached approximately 1.8 million metric tons, with infant formula contributing 0.75 million tons and baby cereals 0.55 million tons. Adoption rates have surged, with 68% of urban households in Saudi Arabia and UAE incorporating fortified baby foods and specialized pediatric formulas into daily diets. Consumer demand is shaped by rising dual-income families, increasing disposable income, and heightened awareness of nutritional standards, leading to a 7.5% increase in baby food consumption from 2022 to 2025. Market applications are segmented into infant feeding (45%), toddler nutrition (32%), and specialty nutrition for allergies and sensitivities (23%). Technical performance metrics such as protein fortification frequency, DHA levels, and probiotic counts have been optimized, with an average formula containing 14g protein per 100g and DHA concentration of 0.32%. The market insights indicate sustained growth, with a focus on high-quality, nutrient-dense products driving consumer adoption and reinforcing the Middle East and Africa Baby Food & Pediatric Nutrition market demand.

In Saudi Arabia, the Baby Food & Pediatric Nutrition Market demonstrates robust growth, supported by over 120 registered manufacturing facilities and 35 specialized distribution companies. The country contributes approximately 22% of the regional market share in 2026, with infant formula accounting for 48% of domestic consumption and baby cereals contributing 28%. Technology adoption is accelerating, with 65% of manufacturers integrating automated blending and fortification systems and 40% leveraging smart packaging to monitor product integrity and freshness. Pediatric nutrition products with probiotics and DHA fortification have seen adoption rates exceeding 50% among urban households. Distribution is heavily dominated by supermarkets/hypermarkets (52%), followed by online retail (22%) and specialty stores (26%). The market insights in Saudi Arabia reinforce the broader Middle East and Africa Baby Food & Pediatric Nutrition market growth and emphasize the strategic importance of technological innovation and distribution expansion in driving market share and demand.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Food & Pediatric Nutrition Market Trends

Rapid Digitalization and E-Commerce Expansion

The Middle East and Africa Baby Food & Pediatric Nutrition market is witnessing substantial growth in e-commerce adoption, with online retail sales increasing from USD 0.9 billion in 2022 to USD 2.4 billion in 2026, representing a CAGR of 18.5%. Technology-driven platforms offer subscription-based baby food delivery, personalized nutrition plans, and traceability features, increasing customer loyalty and product penetration. Adoption of AI-based inventory management and IoT-enabled cold chain monitoring has improved supply chain efficiency by 12%, reducing wastage and enhancing shelf life. The trend highlights that digital distribution channels are now critical for market expansion and reinforce the Baby Food & Pediatric Nutrition market growth trajectory.

Fortified and Functional Nutrition Products

Manufacturers are increasingly producing functional and fortified products to meet specialized nutritional needs. In 2025, production of DHA-fortified infant formula exceeded 450,000 tons, while probiotic-enriched cereals reached 210,000 tons. Adoption rates for fortified products have grown from 38% in 2022 to 55% in 2026 across urban regions, driven by awareness campaigns and clinical studies linking early nutrition to cognitive and physical development. Functional formulations now constitute 31% of total regional production. This trend reinforces the Baby Food & Pediatric Nutrition market insights and highlights sector-specific demand for high-value, nutrient-dense products.

Sustainable Packaging and Eco-Friendly Practices

Environmental sustainability is influencing consumer preferences, with 28% of parents preferring biodegradable or recyclable packaging in 2025, up from 15% in 2022. Manufacturers are investing USD 120 million in sustainable packaging technologies, including plant-based plastics and reusable containers. Production volumes for eco-friendly packaged baby food reached 320,000 tons in 2025, demonstrating a 10% year-on-year growth. This shift aligns with regional environmental regulations and reinforces the Baby Food & Pediatric Nutrition market trend toward greener, consumer-conscious offerings.

Baby Food & Pediatric Nutrition Market Driver

Rising Infant Population and Health Awareness

The increasing birth rate in the Middle East and Africa, with over 15 million infants born annually, is a primary driver of market growth. Health awareness campaigns and pediatric consultations have led to a 7% year-on-year increase in infant formula adoption, with urban households contributing 62% of total consumption. Investments in fortified and organic baby food formulations have increased from USD 1.2 billion in 2022 to USD 2.0 billion in 2026. Adoption of specialized pediatric nutrition products, such as hypoallergenic formulas, has grown to 19% of total market volume. These dynamics reinforce the Baby Food & Pediatric Nutrition market growth potential across urban and semi-urban regions.

Baby Food & Pediatric Nutrition Market Restraint

High Cost of Fortified and Specialized Products

Premium baby food products, particularly those fortified with DHA, probiotics, or organic ingredients, remain cost-prohibitive for middle-income households. Prices for DHA-fortified formula range from USD 28–35 per kilogram, leading to limited adoption in rural areas where penetration is below 12%. Market share for high-priced products constitutes only 24% of total regional sales. Economic volatility and inflationary pressures are expected to restrain growth, limiting the Baby Food & Pediatric Nutrition market size expansion in price-sensitive regions.

Baby Food & Pediatric Nutrition Market Opportunity

Expansion of E-Commerce and Direct-to-Consumer Channels

The rapid digitalization in Saudi Arabia, UAE, and Nigeria offers significant opportunities, with online retail accounting for 22% of total market share in 2026, up from 10% in 2022. Subscription-based models have resulted in USD 0.6 billion additional revenue in 2025, while digital promotions and influencer campaigns increased engagement rates by 15%. The integration of AI-based personalized nutrition planning is expected to capture 8–10% of the market volume in next three years. These developments reinforce the Baby Food & Pediatric Nutrition market insights and underscore investment potential.

Baby Food & Pediatric Nutrition Market Challenge

Stringent Regulatory and Compliance Standards

Compliance with infant food regulations, such as Gulf Standardization Organization (GSO) requirements and local labeling mandates, increases operational complexity. Approximately 42% of manufacturers incur additional compliance costs averaging USD 1.2 million annually. Regulatory delays and periodic audits have affected production volumes by 3–5% in 2025. These challenges can impact market growth, particularly for new entrants, while reinforcing the necessity of adhering to strict standards in the Baby Food & Pediatric Nutrition market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11.61 Billion |

| Market Size in 2026 | USD 12.4 Billion |

| Market Size in 2034 | USD 21.7 Billion |

| CAGR | 6.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Food & Pediatric Nutrition Market Segmentation

The Middle East and Africa Baby Food & Pediatric Nutrition market is segmented by product type and distribution channel, with infant formula accounting for 42% of regional production, baby cereals 30%, and snacks & complementary foods 28%. Supermarkets/hypermarkets lead distribution with 52% share, online retail 22%, and specialty stores 26%, highlighting the market’s structured approach to reach diverse consumer groups.

By Type

Infant Formula:

Infant formula dominates with 42% share, producing 0.75 million tons in 2025, featuring protein content of 14g per 100g, DHA 0.32%, and enhanced mineral fortification. Technical specifications include low lactose variants, hypoallergenic formulations, and organic-certified lines, catering to high-value consumers. Packaging innovations, including single-use sachets and recyclable tins, support distribution efficiency. The Baby Food & Pediatric Nutrition market size for infant formula is projected to reach USD 9.2 billion by 2034.

Baby Cereals:

Baby cereals hold 30% market share, producing 0.55 million tons in 2025, with fortified vitamins (A, D, E) and mineral blends. Typical cereal frequency for infants is 2–3 servings per day, with penetration in urban households at 61%. Multi-grain and gluten-free variants represent 25% of total production. Packaging and shelf-life optimization have improved product stability by 15%, reinforcing Baby Food & Pediatric Nutrition market growth.

Snacks & Complementary Food:

This segment accounts for 28% share, producing 0.48 million tons in 2025. Technical specifications include low sugar, high fiber content, and allergen-free ingredients, with consumption frequency averaging 2–3 servings per day. Innovative snack formats, such as ready-to-eat puffs and squeezable puree pouches, have increased market penetration from 18% in 2022 to 33% in 2026, supporting the Baby Food & Pediatric Nutrition market insights.

By Application

Infant Feeding (0–12 months):

Comprising 45% of total market share, infant feeding applications include formula, cereals, and fortified liquids. Production volume reached 0.85 million tons in 2025, with urban penetration at 68% and rural at 34%. Technical performance metrics, including protein content, vitamin fortification, and DHA levels, remain critical for efficacy and market differentiation, reinforcing the Baby Food & Pediatric Nutrition market growth.

Toddler Nutrition (1–3 years):

Toddler nutrition constitutes 32% share, producing 0.62 million tons in 2025. Adoption of fortified cereals, snacks, and fortified beverages is prevalent, with consumption frequency of 2–4 servings per day. Technical aspects such as fiber content (6–8g per serving) and calcium concentration (250mg per 100g) enhance market value. Penetration in urban areas reached 59% in 2025, reinforcing market demand and growth.

Specialty Nutrition:

Representing 23% of the market, specialty nutrition addresses allergies, sensitivities, and organic preferences. Production volume reached 0.43 million tons in 2025, with adoption rates of 20% among high-income households. Products include hypoallergenic formulas, organic cereals, and lactose-free snacks, with technical metrics such as reduced protein allergenicity (<1%) and organic certification compliance, reinforcing Baby Food & Pediatric Nutrition market insights

Middle East and Africa Baby Food & Pediatric Nutrition Market Segmentations

Product Type

- Infant Formula

- Baby Cereals

- Snacks & Complementary Food

Distribution Channel

- Supermarkets/Hypermarkets

- Online Retail

- Specialty Stores

Baby Food & Pediatric Nutrition Market Regional Outlook

UAE

The UAE contributes 12% of the Middle East and Africa Baby Food & Pediatric Nutrition market in 2026, producing approximately 0.21 million tons of baby food. Supermarkets and hypermarkets dominate distribution (58%), followed by online retail (20%) and specialty stores (22%). High-income urban households drive demand for DHA-fortified and organic formulas, with product penetration at 65% for infant formula and 40% for baby cereals, reinforcing regional market insights.

Turkey

Turkey accounts for 16% of regional market share, with 0.29 million tons of production in 2025. Infant formula represents 46% of the market, baby cereals 31%, and snacks & complementary foods 23%. Technology adoption, including automated blending and smart packaging, is high at 62%. Supermarkets/hypermarkets provide 50% of distribution, online retail 25%, and specialty stores 25%, reinforcing Baby Food & Pediatric Nutrition market demand.

Saudi Arabia

Saudi Arabia represents 22% market share, producing 0.38 million tons in 2025. Infant formula adoption is 48%, baby cereals 28%, and snacks & complementary foods 24%. Supermarkets/hypermarkets dominate (52%), online retail 22%, and specialty stores 26%. Technological adoption in production lines, including nutrient fortification and probiotic enrichment, exceeds 65%, reinforcing market growth.

South Africa

South Africa contributes 14% of regional production, totaling 0.24 million tons. Infant formula accounts for 40%, cereals 35%, and snacks 25%. Urban penetration is 60% for fortified products, with technical adoption of automated production lines at 50%. Distribution is led by supermarkets/hypermarkets (54%), online retail (18%), and specialty stores (28%), reinforcing market insights.

Egypt

Egypt holds 10% market share, producing 0.17 million tons. Infant formula 42%, baby cereals 33%, snacks & complementary foods 25%. Online retail adoption is rising from 7% in 2022 to 15% in 2026. Supermarkets/hypermarkets dominate (55%). Technical innovations include fortified micronutrients and organic certification compliance, reinforcing Baby Food & Pediatric Nutrition market demand.

Nigeria

Nigeria represents 14% share, producing 0.21 million tons. Infant formula adoption 38%, baby cereals 32%, snacks & complementary foods 30%. Distribution is 48% supermarkets, 20% online, 32% specialty stores. Urban penetration of fortified products is 50%, with technical adoption of low-lactose and allergen-free formulas at 42%, reinforcing regional market insights.

List of Top Baby Food & Pediatric Nutrition Companies

- Nestlé S.A.

- Danone S.A.

- Abbott Laboratories

- Reckitt Benckiser Group plc

- Hero Group

- Hipp GmbH & Co.

- Kraft Heinz Company

- Meiji Holdings Co., Ltd.

- FrieslandCampina

- Arla Foods

- Perrigo Company plc

- Wyeth Nutrition

- Mead Johnson Nutrition

- Aptamil

- Babybio

Top Two Companies

Nestlé S.A.

-

Market share: 16%

-

Positioning: Nestlé leads the Middle East and Africa Baby Food & Pediatric Nutrition market through diversified infant formula and pediatric nutrition portfolios, producing over 0.2 million tons in 2025. The company’s adoption of high DHA formulas, organic-certified cereals, and probiotic-enriched snacks has resulted in urban household penetration of 68%. Strategic distribution across supermarkets, online platforms, and specialty stores reinforces its dominant market share and Baby Food & Pediatric Nutrition market insights.

Danone S.A.

-

Market share: 14%

-

Positioning: Danone leverages functional and fortified baby nutrition products, including infant formula with reduced allergenicity and organic baby cereals. Production reached 0.18 million tons in 2025, with fortified product adoption rates of 55% in urban centers. Distribution channels include hypermarkets (50%), online retail (24%), and specialty stores (26%), reinforcing market growth and Baby Food & Pediatric Nutrition market size expansion.

Investment Analysis and Opportunities

Investment allocation in the Middle East and Africa Baby Food & Pediatric Nutrition market is concentrated with 45% toward product innovation, 30% in production capacity expansion, and 25% in distribution channel enhancement. Regional investments are highest in Saudi Arabia (22%), UAE (12%), and Turkey (16%). Sector-wise, infant formula receives 42% of total investments, baby cereals 30%, and snacks & complementary foods 28%. M&A agreements and collaborations in 2025 included strategic partnerships for fortified product lines and expansion into online retail, contributing an estimated USD 0.5 billion in combined market capitalization. Cross-border collaborations between local manufacturers and international players are fostering technology transfer, enhancing fortification standards, and improving packaging sustainability, reinforcing the Baby Food & Pediatric Nutrition market growth trajectory. Emerging investment opportunities include digital subscriptions, AI-based nutrition planning, and specialty nutrition segments targeting allergies and organic preferences.

New Product Development

In 2025, approximately 18% of newly launched products in the Middle East and Africa Baby Food & Pediatric Nutrition market featured functional fortification, including DHA, probiotics, and micronutrients. Performance improvements in new product lines include a 12% increase in shelf-life, 10% enhanced digestibility, and 15% improved nutrient bioavailability. Innovations include squeezable puree pouches, low-lactose formulas, and organic-certified cereals. The focus on personalization and clinical-grade nutrition has increased urban adoption by 8–10%, reinforcing Baby Food & Pediatric Nutrition market demand and insights for 2026–2034.

Recent Developments

- 2025: Nestlé introduced probiotic-enriched infant formula, increasing production by 12% and urban penetration to 68%, reinforcing market growth.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Plant-Based Foods and Functional Ingredients

Kathy Flores is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.