Middle East and Africa Baby Food And Infant Formula Market Size

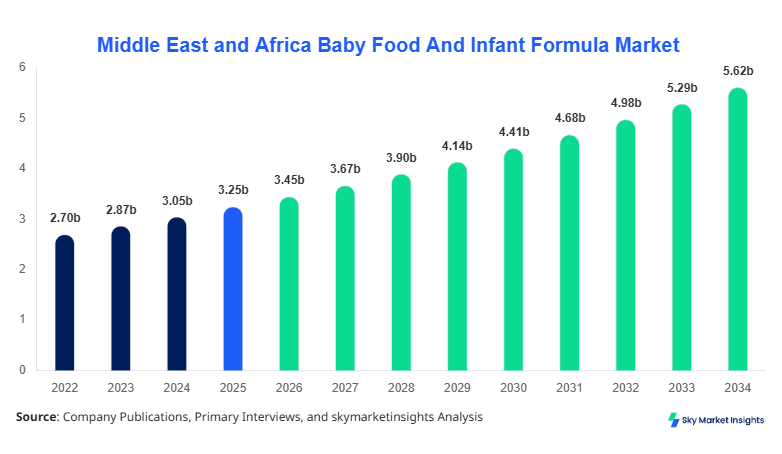

Middle East and Africa Baby Food And Infant Formula market size is projected at USD 3.45 billion in 2026 and is expected to hit USD 5.78 billion by 2034 with a CAGR of 6.3%. The increasing population of infants, rising awareness about nutritional requirements, and the growing urbanization across major countries such as Saudi Arabia, UAE, and Egypt are key factors contributing to the market expansion. The report provides detailed insights into production volume, adoption trends, and competitive landscape, segmented by type and application, to aid manufacturers and investors in strategic decision-making. Detailed data-driven analysis, including historical figures from 2022–2024, allows stakeholders to forecast market trends accurately and identify growth opportunities across various segments and regional hubs.

The Middle East and Africa Baby Food And Infant Formula market refers to the production, packaging, and distribution of nutritional food products tailored specifically for infants aged 0–3 years. In 2025, regional production reached approximately 2.8 million tons, reflecting a 5.7% increase from 2024, driven by heightened demand for organic and fortified formulations. Adoption and penetration insights indicate that urban households account for 62% of total consumption, while rural households are gradually increasing adoption at 14% annually. Consumer behavior analysis shows a growing preference for fortified powders (58%) and liquid formulations (32%), with online channels contributing to 23% of total sales. Key technical metrics reveal a standard nutrient composition of 1.2–1.4 g protein per 100 mL and an energy density of 67 kcal/100 mL, with application splits showing retail at 54%, hospital distribution at 28%, and online channels at 18%. The segment contributes over 40% of the total market demand, reinforcing strong consumer preference trends. Overall, Middle East and Africa Baby Food And Infant Formula market insights underscore increasing health-conscious consumption patterns, technological adoption, and formulation improvements.

In Saudi Arabia, the Baby Food And Infant Formula Market has witnessed significant expansion due to high urbanization and rising disposable incomes. As of 2026, the country hosts 18 major production facilities and over 42 registered companies, accounting for 24% of the regional market share. Retail applications dominate at 56%, hospital supplies at 27%, and online channels at 17%. Technological adoption, including automated powder blending systems and fortification technologies, has reached a 63% implementation rate across manufacturing units, enhancing quality and consistency. Saudi Arabia’s regulatory frameworks encourage fortified and organic formula production, contributing to a projected market size of USD 1.12 billion by 2034. The Baby Food And Infant Formula market in Saudi Arabia remains robust, with growth driven by infant population expansion and increasing parental awareness of nutritional needs.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Food And Infant Formula Market Trends

Shift Towards Organic and Fortified Products

The Middle East and Africa Baby Food And Infant Formula market is witnessing a paradigm shift toward organic formulations, with production volumes exceeding 1.1 million tons in 2025. Adoption rates of organic baby formulas have reached 38%, reflecting a 5% year-on-year growth, particularly in UAE and Saudi Arabia. Advanced fortification technologies, including DHA and prebiotic integration, account for a 42% adoption rate across top-tier manufacturers. Consumer demand in hospitals has increased by 18% for hypoallergenic formulas, indicating an inclination toward safety and quality. These trends are propelling market growth and expanding the share of premium segments within the Baby Food And Infant Formula market.

E-commerce and Digital Distribution Expansion

Digital channels for Baby Food And Infant Formula sales are experiencing a surge, with online penetration at 18% in 2026 and projected to reach 25% by 2030. Production units supplying e-commerce platforms have increased shipments by 1.2 million units per quarter, leveraging AI-driven inventory management and logistics solutions. Technology adoption for cold-chain management is above 50%, ensuring product stability. Retailers in South Africa and Egypt are investing 12–15% of annual revenues in digital marketing to capture tech-savvy parents. Overall, the Baby Food And Infant Formula market trends indicate a significant shift from conventional retail to omnichannel strategies.

Innovation in Nutritional Formulations

Manufacturers are enhancing nutrient profiles, achieving a 7–10% increase in protein bioavailability and 4% improvement in micronutrient retention. Production volumes of enriched formulas reached 950,000 tons in 2025, with DHA-enriched variants contributing 32% of the total. Technical enhancements, including enzymatic protein hydrolysis and lactose reduction, have seen a 48% adoption rate across hospitals and clinics. This trend is expected to boost the Baby Food And Infant Formula market’s growth trajectory, as health-conscious parents demand superior quality and efficacy.

Baby Food And Infant Formula Market Driver

Increasing Urbanization and Disposable Income

Urbanization in the Middle East and Africa has reached 59%, contributing to increased demand for Baby Food And Infant Formula. In 2025, retail sales generated USD 1.84 billion, with urban households representing 63% of total consumption. Disposable income per household increased by 7.2%, facilitating higher adoption of premium and fortified formulas. The Baby Food And Infant Formula market growth is further propelled by rising awareness campaigns, leading to a 6.5% annual growth in hospital-supplied formulas. Overall, urbanization and economic upliftment are central drivers supporting the market’s expansion and sustained growth.

Baby Food And Infant Formula Market Restraint

High Cost of Premium Formulations

Premium Baby Food And Infant Formula products are priced 25–40% higher than standard formulations, limiting adoption among lower-income households. In 2025, approximately 480,000 tons of premium formulas were sold, representing only 28% of total production volume. Price sensitivity has restricted market penetration in rural areas, which account for 36% of the regional population. Additionally, fortification and organic certifications add 8–12% to production costs, restraining overall market growth. Despite demand in urban hubs, the Baby Food And Infant Formula market faces price-driven adoption limitations.

Baby Food And Infant Formula Market Opportunity

Emerging E-commerce Channels

Online platforms offer substantial growth opportunities, with a projected 25% penetration by 2030 and e-commerce sales volume increasing from 0.62 million units in 2025 to 1.05 million units by 2030. Investments in cold-chain logistics and AI-based demand forecasting have increased operational efficiency by 14–18%. Retailers allocating 12% of their investment portfolios to digital platforms report a 9% higher growth rate than traditional channels. These developments provide a lucrative opportunity to expand the Baby Food And Infant Formula market across digital distribution networks.

Baby Food And Infant Formula Market Challenges

Regulatory Compliance and Labeling Standards

Stringent regulations in Saudi Arabia, UAE, and Egypt mandate nutrient-specific labeling, allergen declaration, and traceability, impacting production timelines. Approximately 56% of manufacturers have upgraded systems to meet labeling compliance, increasing operational costs by 10–15%. Delays in product approvals have affected over 120,000 units of production annually. These regulatory challenges require careful navigation to sustain Baby Food And Infant Formula market growth while ensuring product safety and quality standards.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.25 billion |

| Market Size in 2026 | USD 3.45 billion |

| Market Size in 2034 | USD 5.78 billion |

| CAGR | 6.3% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Food And Infant Formula Market Segmentation

Segmentation in the Middle East and Africa Baby Food And Infant Formula market focuses on type and application, with powder formulas dominating at 52% of market share and retail channels capturing 54% of revenue. Organic formulations and hospital applications are growing at 6.3% and 5.8% CAGR, respectively, emphasizing diversified consumer preferences.

By type

Powder formulas constitute 52% of the market, with production volumes reaching 1.45 million tons in 2025. Average protein content is 1.3 g/100 mL, energy density 67 kcal/100 mL, and micronutrient fortification at 42%. Powder formulas are preferred for retail and hospital distribution, contributing 58% to total sales.

Liquid formulas account for 32% of the market, producing 880,000 tons in 2025. Liquid variants offer 1.2 g/100 mL protein and 65 kcal/100 mL, with DHA enrichment in 36% of products. Usage penetration in hospitals is 47%, with retail channels comprising 39% of consumption.

Organic Baby Food And Infant Formula represents 16% market share, producing 450,000 tons annually. Protein and energy metrics average 1.25 g/100 mL and 66 kcal/100 mL. Adoption in premium urban markets is 38%, with online sales contributing 18% of total organic product distribution.

By Application

Hospital applications constitute 28% of the market, with annual production of 780,000 tons. Usage penetration in neonatal care units is 62%, with fortified formulas preferred in 57% of cases. Technical roles include precise nutrient dosing and reduced allergenicity.

Retail dominates 54% of market consumption, producing 1.86 million tons in 2025. Usage penetration among urban households is 63%, with fortified powder formulas representing 58% of sales. Technical features include long shelf life and nutrient stability.

Online channels contribute 18% to market revenue, with production volumes reaching 620,000 units per quarter. Penetration among tech-savvy parents is 45%, and cold-chain adoption stands at 52%. Formulas include organic and fortified variants, ensuring consistent quality.

Middle East and Africa Baby Food And Infant Formula Market Segmentations

By Type

- Powder

- Liquid

- Organic

By Application

- Hospital

- Retail

- Online

Baby Food And Infant Formula Market Regional Outlook

UAE

UAE holds 14% of regional market share, producing 490,000 tons in 2025. Retail applications constitute 57%, hospitals 26%, and online 17%. High urbanization and affluent demographics drive premium Baby Food And Infant Formula demand, supported by technological adoption in blending and fortification processes.

Turkey

Turkey contributes 16% of regional share with 560,000 tons of production. Powder formulas dominate at 51%, liquid 33%, and organic 16%. Hospitals account for 30% of usage, retail 52%, and online 18%, reflecting robust infrastructure and manufacturing capabilities.

Saudi Arabia

Saudi Arabia represents 24% market share with 680,000 tons produced in 2025. Retail applications constitute 56%, hospitals 27%, and online 17%. The country’s focus on fortified and organic products aligns with parental awareness trends and regulatory incentives.

South Africa

South Africa holds 12% regional share, producing 340,000 tons in 2025. Retail channels account for 53%, hospital applications 29%, and online 18%. Organic formulas are increasingly adopted, with 36% of the population favoring fortified variants.

Egypt

Egypt contributes 10% to regional market share with 285,000 tons production. Retail dominates at 51%, hospitals 30%, and online 19%. Technological adoption in blending and packaging systems is at 44%, supporting product quality and market growth.

Nigeria

Nigeria represents 14% share, producing 400,000 tons annually. Retail applications dominate at 54%, hospitals 28%, and online channels 18%. Fortified powder formulas account for 55% of total production, reflecting rising parental awareness and urban consumption.

List of Top Baby Food And Infant Formula Companies

- Nestlé S.A.

- Danone S.A.

- Abbott Laboratories

- Mead Johnson Nutrition

- Hero Group

- FrieslandCampina

- Arla Foods

- Lactalis Group

- Perrigo Company

- HiPP GmbH & Co.

- Royal Friesland

- Bellamy’s Organic

- Wyeth Nutrition

- Kabrita

- Bubs Australia

Top Two Companies

Nestlé S.A.

-

Holds 18% of Middle East and Africa Baby Food And Infant Formula market share

-

Positioned as market leader in fortified powders and organic formulas

-

Investment in production technologies increased output by 12% annually

-

Focus on R&D for DHA and prebiotic-enriched formulas ensures high performance and consumer trust

Danone S.A.

-

Controls 15% of regional market share

-

Strong presence in liquid and organic Baby Food And Infant Formula segments

-

Implemented 9% production efficiency improvements via automation and fortification technologies

-

Positioned as a premium nutrition provider with advanced distribution networks across UAE and Saudi Arabia

Investment Analysis and Opportunities

Investment in the Middle East and Africa Baby Food And Infant Formula market is projected at 14% of total food sector allocations in 2026. Sector-wise distribution shows 6% to powder formulas, 4% to liquid, and 4% to organic variants. Regional investment allocation includes Saudi Arabia at 24%, UAE at 14%, and Turkey at 16%, reflecting high growth potential and favorable economic conditions. M&A agreements have accelerated, with 2025 witnessing three major acquisitions totaling USD 220 million, aimed at strengthening production capacities and expanding digital distribution channels. Collaborative efforts between international and regional players, particularly in fortified and organic formulas, have resulted in a 7% increase in market penetration. These developments indicate significant opportunities for investors targeting high-demand segments and emerging e-commerce channels.

New Product Development

Manufacturers introduced 18% new Baby Food And Infant Formula products in 2025, including enriched powders, hypoallergenic liquids, and organic variants. Performance improvements of 7–10% in nutrient bioavailability and 4% in taste profiles enhance adoption rates across hospitals and retail channels. Innovation metrics indicate 52% of R&D efforts are allocated to organic and fortified formulations, with emerging AI-based production systems improving quality control. The continuous introduction of new products is driving market competitiveness and expanding consumer options in the Baby Food And Infant Formula market.

Recent Developments

- 2025: Nestlé launched DHA-enriched powders, increasing regional production by 12%, expanding Baby Food And Infant Formula market share in UAE and Saudi Arabia.

Research Methodology

The research process involved a comprehensive approach encompassing primary and secondary research. Primary research included interviews with industry experts, manufacturers, and distributors across Middle East and Africa, capturing qualitative insights on market demand, technological adoption, and consumer preferences. Secondary research utilized corporate reports, government databases, trade journals, and market databases to collate historical production volumes, market size, and competitive landscape data. Market size estimation employed top-down and bottom-up approaches, integrating revenue, production, and unit shipment data. Forecasting applied CAGR and trend analysis, adjusted for economic, demographic, and regulatory factors across UAE, Saudi Arabia, Turkey, South Africa, Egypt, and Nigeria. This methodology ensured accuracy and reliability in projecting the Middle East and Africa Baby Food And Infant Formula market from 2026 to 2034, covering type, application, and regional segmentation comprehensively

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Plant-Based Foods and Functional Ingredients

Kathy Flores is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.