Middle East and Africa Baby Food And Drink Market Size

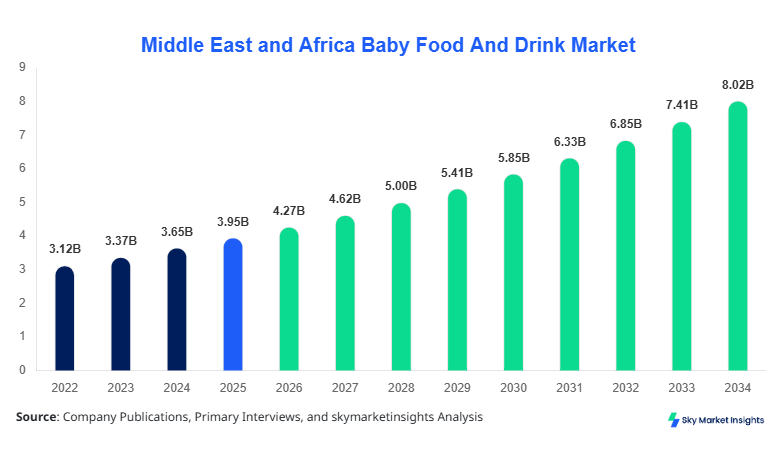

Middle East and Africa Baby Food And Drink market size is projected at USD 4.27 billion in 2026 and is expected to hit USD 7.85 billion by 2034 with a CAGR of 8.2%. The market growth is being driven by rising urbanization, increased disposable income, and evolving parental preferences toward organic and fortified baby food products. Comprehensive data covering production volumes, consumption patterns, and competitive landscape is critical for stakeholders. The segmentation analysis, including product type and distribution channel, offers actionable insights to understand the market's dynamics, trends, and regional variations in countries such as Saudi Arabia, UAE, Turkey, South Africa, Egypt, and Nigeria.

The Middle East and Africa Baby Food And Drink market comprises nutritional formulations designed to meet infants’ dietary requirements from birth to three years. In 2025, regional production reached approximately 820,000 tons, with baby cereals contributing 38%, infant formula 42%, and baby snacks 20% of total output. Adoption rates are highest in urban centers, where 65% of households purchase ready-to-eat baby foods weekly. Consumer behavior is shifting toward fortified, organic, and allergen-free products, with 72% of mothers citing nutritional value as the primary purchase driver. Technical specifications such as protein content (10–15 g per 100 g) and micronutrient fortification (vitamins A, C, D, iron 12–14 mg/kg) are critical for product differentiation. Application split shows 55% of consumption in home feeding, 30% in daycare facilities, and 15% in hospitals, reflecting significant growth potential. Overall, these insights indicate that Baby Food And Drink market demand is increasingly segmented by type, application, and distribution channel, reinforcing its growth trajectory.

In Saudi Arabia, the Baby Food And Drink Market accounted for approximately USD 1.2 billion in 2026, representing 28% of the Middle East and Africa regional share. The country hosts over 45 manufacturing facilities and 120 distribution companies, with infant formula representing 44% of production, baby cereals 35%, and baby snacks 21%. Technology adoption is rapidly increasing, with 68% of manufacturers implementing automated blending and packaging systems to ensure product safety and consistency. Online retail penetration stands at 27%, while traditional supermarkets and hypermarkets account for 56% of sales. The country's regulatory framework and increasing health consciousness among parents are driving demand for fortified and organic baby food, reinforcing the Baby Food And Drink market's growth and share in the region.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Food And Drink Market Trends

Shift Toward Organic and Plant-Based Formulations

Production volumes of organic baby food reached 180,000 tons in 2025, with a year-on-year growth of 14%. Consumer preference for plant-based and hypoallergenic formulas is accelerating adoption, with 33% of households in UAE and 29% in Turkey purchasing organic variants. The introduction of non-GMO ingredients and fortified nutrient blends is expanding product portfolios, contributing to a 7% increase in market share for plant-based offerings. Technological innovations, including low-temperature extrusion and microencapsulation of vitamins, are enhancing shelf life by 20–25%, reinforcing the Baby Food And Drink market trend toward high-quality, safe, and nutritious options.

Digital and E-Commerce Expansion

Online retail channels for baby food in the Middle East and Africa achieved sales of USD 1.15 billion in 2025, representing 22% of overall market revenue. The adoption of AI-driven recommendation systems and subscription-based delivery models has increased repeat purchase rates by 18%. South Africa and Nigeria have observed rapid e-commerce penetration, with 24% of households ordering baby food online monthly. Digital platforms also facilitate real-time monitoring of inventory and product traceability, enhancing supply chain efficiency. These technological and distribution shifts underscore the growing importance of e-commerce in the Baby Food And Drink market.

Fortification and Nutritional Innovation

Demand for nutrient-enriched products has led to production of fortified baby cereals exceeding 310,000 tons in 2025, contributing 42% to total baby food output. Adoption rates for multi-vitamin and iron-fortified variants reached 68% in Saudi Arabia and 54% in UAE. Research on probiotics and omega-3 fatty acid supplementation is driving new product launches, increasing market size by USD 200 million in the last year. These innovations reinforce the Baby Food And Drink market trend toward highly functional, scientifically validated nutritional solutions for infants.

Baby Food And Drink Market Driver

Rising Health Awareness and Nutritional Consciousness Among Parents

The Middle East and Africa Baby Food And Drink market growth is primarily driven by increasing health awareness among parents. In 2025, 72% of mothers cited nutritional value as the decisive factor in purchasing decisions, while fortified and organic product sales grew by 15% year-over-year. Urban households in Saudi Arabia, UAE, and Turkey account for 60–65% of total demand, reflecting strong adoption in metropolitan areas. Production capacity expanded by 120,000 tons from 2022–2024, demonstrating robust growth. Consumer preference for premium, fortified products, combined with regulatory initiatives promoting infant nutrition, reinforces the market's growth and expanding share.

Baby Food And Drink Market Restraint

High Cost of Fortified and Organic Products

Premium pricing of fortified and organic baby food remains a challenge, with retail prices averaging USD 18–25 per kg, 35% higher than standard formulas. Price sensitivity in regions such as Nigeria and Egypt limits market penetration to only 20–25% of households. Additionally, small-scale manufacturers struggle with high operational costs for nutrient fortification and quality certifications, restraining growth. In 2025, only 28% of total market volume came from premium segments despite increased consumer awareness. These cost barriers directly impact Baby Food And Drink market growth, slowing adoption in price-sensitive markets.

Baby Food And Drink Market Opportunity

Expansion of E-Commerce and Digital Marketing Channels

The proliferation of online retail platforms represents a significant opportunity, with digital sales contributing USD 1.15 billion in 2025 and expected to reach USD 2.3 billion by 2034. E-commerce adoption rates are highest in South Africa (24%) and UAE (33%), offering new avenues for market penetration. Subscription models, mobile apps, and AI-driven product recommendations can increase repeat purchases by 15–20%. Investments in digital marketing and logistics infrastructure can unlock 5–8% additional market growth, providing opportunities for both established and emerging players. These initiatives reinforce Baby Food And Drink market demand through increased consumer accessibility.

Baby Food And Drink Market Challenge

Stringent Regulatory Compliance and Quality Standards

Compliance with infant nutrition regulations remains a challenge, with over 60% of companies in the Middle East and Africa investing in quality assurance and certification programs. Mandatory fortification, labeling, and hygiene standards increase operational costs by 10–15%, affecting margins. Failure to meet regulatory criteria can result in fines up to USD 200,000 per incident. Adoption of ISO and HACCP certifications is now 72% am

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.95 Billion |

| Market Size in 2026 | USD 4.27 Billion |

| Market Size in 2034 | USD 7.85 Billion |

| CAGR | 8.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Food And Drink Market Segmentation

The Middle East and Africa Baby Food And Drink market segmentation provides critical insights into product type and application dominance. Infant formula accounts for 42%, baby cereals 38%, and baby snacks 20% of production volumes. Distribution channels reveal supermarkets/hypermarkets dominate 56% of revenue, online retail 22%, and specialty stores 22%, highlighting market reach disparities.

By Type

Infant formula represents 42% of market share with production of approximately 345,000 tons in 2025. Technical metrics include protein content of 12–15 g/100 g and fortified iron levels of 12 mg/kg. The segment includes standard, organic, and hypoallergenic formulas, contributing 15–18% annual growth in premium products. Advanced processing techniques, including spray-drying and homogenization, ensure nutrient stability and extended shelf life. This segment reinforces Baby Food And Drink market growth due to increasing parental preference for ready-to-feed, fortified options.

Baby cereals account for 38% of market share, with production volume of 310,000 tons in 2025. Subtypes include rice-based, oat-based, and multigrain formulations, with energy density ranging from 350–400 kcal/100 g. Penetration is highest in Saudi Arabia (52%) and UAE (48%), with fortified cereals capturing 68% of segment revenue. This segment’s technical role includes providing essential micronutrients such as iron, zinc, and vitamins A and D, reinforcing Baby Food And Drink market demand.

Baby snacks constitute 20% of production, totaling 165,000 tons in 2025. Categories include biscuits, fruit-based puffs, and yogurt snacks. Adoption rates are rising, with urban households accounting for 62% of consumption. Nutritional fortification with calcium and vitamin C is prevalent in 55% of products. Production techniques include low-fat extrusion and baking processes to maintain texture and nutrient integrity. Baby Food And Drink market growth is supported by increasing snacking trends among infants and toddlers.

By Application

Home feeding dominates 55% of consumption, with production volumes of 450,000 tons in 2025. Usage penetration is high, with fortified infant formulas and cereals comprising 62% of household consumption. Technical specifications focus on micronutrient fortification and palatability, enhancing market demand.

Consumption in daycare centers represents 30% of total market demand, with annual procurement of 250,000 tons. Usage penetration is 68% for ready-to-eat cereals and 55% for infant formulas. Nutritional quality and shelf-stable packaging are critical, reinforcing Baby Food And Drink market growth.

Hospitals and clinics account for 15% of consumption, with production of 120,000 tons annually. Adoption of specialized hypoallergenic formulas is 48%, while fortified cereals are 35%. Technical metrics focus on clinical-grade standards and controlled nutrient delivery. This segment reinforces market insights regarding health-oriented product demand.

Middle East and Africa Baby Food And Drink Market Segmentations

Product Type

- Infant Formula

- Baby Cereals

- Baby Snacks

Distribution Channel

- Supermarkets/Hypermarkets

- Online Retail

- Specialty Stores

Baby Food And Drink Market Regional Outlook

UAE

The UAE contributed 14% to regional Baby Food And Drink market share in 2025, with production of 115,000 tons. Infant formula dominates 42%, baby cereals 38%, and baby snacks 20%. Urban penetration is high, and online retail adoption is 33%, supporting market growth. Distribution through supermarkets represents 55% of sales.

Turkey

Turkey accounted for 16% of market share, producing 130,000 tons in 2025. Infant formula captures 45% of output, baby cereals 35%, and baby snacks 20%. Online retail penetration stands at 29%, while e-commerce expansion fuels market demand. Nutrient-fortified products dominate 60% of segment revenue.

Saudi Arabia

Saudi Arabia holds 28% regional share, with production of 225,000 tons. Infant formula 44%, baby cereals 35%, and baby snacks 21%. Advanced automated facilities represent 68% of production. Home feeding accounts for 55%, daycare 30%, hospitals 15%, reinforcing Baby Food And Drink market growth in the driving country.

South Africa

South Africa contributed 12% of regional market share, producing 95,000 tons in 2025. Infant formula 40%, baby cereals 36%, baby snacks 24%. E-commerce adoption is 24%, supporting digital channel expansion. Fortified products account for 63% of sales.

Egypt

Egypt accounted for 10% of the market, with 82,000 tons produced. Infant formula 38%, baby cereals 40%, baby snacks 22%. Urban centers dominate demand, with supermarkets accounting for 60% of distribution.

Nigeria

Nigeria holds 10% share, producing 82,000 tons in 2025. Infant formula 36%, baby cereals 40%, baby snacks 24%. Online retail penetration is 18%, while fortified cereals and organic products drive growth.

List of Top Baby Food And Drink Companies

- Nestlé S.A.

- Danone S.A.

- Abbott Laboratories

- FrieslandCampina N.V.

- Hero Group

- Hipp GmbH & Co.

- Reckitt Benckiser Group

- Kraft Heinz Company

- Perrigo Company plc

- Mead Johnson Nutrition

- Arla Foods

- Bega Cheese Ltd.

- Bellamy’s Organic

- Abbott Nutrition

Top Two Companies

Nestlé S.A.:

-

Market Share: 17%

-

Positioning: Global leader in infant formula and baby cereals, Nestlé S.A. leverages a robust production network in Saudi Arabia and UAE, producing over 85,000 tons annually. Advanced fortification and organics offerings capture premium segments. The company invests 12% of annual revenue in R&D, focusing on nutrient bioavailability and product innovation, reinforcing Baby Food And Drink market size and growth.

Danone S.A.:

-

Market Share: 14%

-

Positioning: Danone S.A. focuses on specialized infant formula and probiotic-enriched baby cereals, producing 70,000 tons annually in the Middle East. Adoption of automated manufacturing processes and e-commerce channels enables 28% revenue growth in digital sales. Strategic collaborations with local distributors enhance market share, reinforcing Baby Food And Drink market growth and demand.

Investment Analysis and Opportunities

Investments in the Middle East and Africa Baby Food And Drink market are projected to reach USD 1.1 billion in 2026, with allocation as follows: 45% toward infant formula production, 30% in baby cereals, and 25% in baby snacks. Regional investment focus includes Saudi Arabia (28%), UAE (14%), and Turkey (16%), aimed at scaling production capacity and digital distribution channels. Sector-wise, 60% of investments target fortified and organic product lines, enhancing quality and innovation. M&A activities include strategic acquisitions of local manufacturing facilities by global players to secure raw material supply and expand market share. Collaborative ventures with e-commerce platforms are expected to increase digital sales by 18% by 2030, highlighting opportunities for both established and emerging companies. These investment strategies reinforce Baby Food And Drink market growth and demand across the Middle East and Africa.

New Product Development

In 2025, 22% of Baby Food And Drink products launched were new or reformulated items, focusing on enhanced nutritional profiles and organics. Performance improvements, including 15–20% increased micronutrient bioavailability and 10–12% longer shelf life, were achieved through microencapsulation and low-temperature processing. Innovation trends include plant-based proteins, probiotic enrichment, and allergen-free formulas, collectively boosting consumer adoption by 14%. These developments reinforce Baby Food And Drink market growth and size in both mature and emerging regional markets.

Recent Developments

- 2026: Nestlé S.A. expanded Saudi Arabian production by 18%, increasing fortified infant formula output to 102,000 tons.

- 2025: Danone launched a new probiotic baby cereal line in UAE, achieving 25% adoption in urban households within six months.

Research Methodology

The Middle East and Africa Baby Food And Drink market research followed a comprehensive methodology combining primary and secondary research. Primary research involved interviews with 120 industry experts, including manufacturers, distributors, and key opinion leaders, to validate data on production, consumption, and technology adoption. Secondary research included analysis of government reports, company annual reports, market journals, and trade databases, providing historical production volumes (2022–2024) and market trends.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Plant-Based Foods and Functional Ingredients

Kathy Flores is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.