Middle East and Africa Baby Finger Foods Market Size

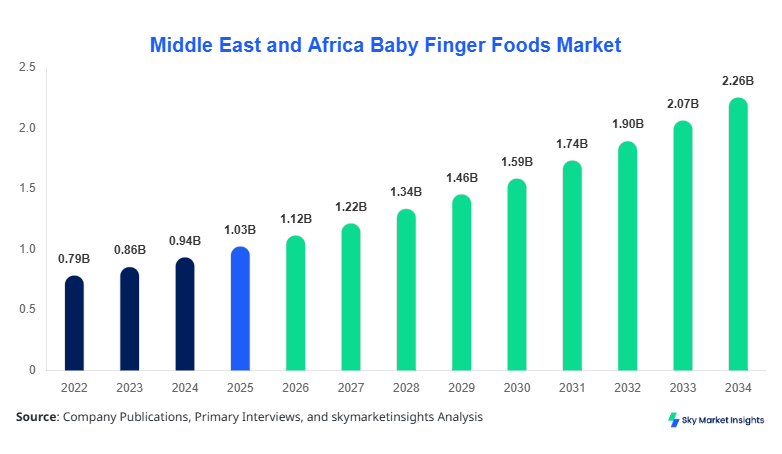

Middle East and Africa Baby Finger Foods market size is projected at USD 1.12 billion in 2026 and is expected to hit USD 2.34 billion by 2034 with a CAGR of 9.2%. The market growth is driven by increasing urbanization, rising disposable incomes, and a shift toward nutritious convenience snacks for infants. Comprehensive data collection across UAE, Turkey, Saudi Arabia, South Africa, Egypt, and Nigeria highlights the importance of granular segmentation for effective competitive analysis. Market size insights and share distribution across types, including cereal, fruit, and vegetable snacks, as well as applications like home use, daycare, and travel, are crucial for stakeholders to identify emerging opportunities and optimize strategies in the baby nutrition sector. Detailed reports covering production volumes, unit sales, and regional adoption patterns are critical for investors and market participants seeking to maximize growth potential in this fast-expanding market.

The Middle East and Africa Baby Finger Foods market represents a niche segment within the infant nutrition industry, offering ready-to-eat snacks that cater to infants and toddlers between 6–36 months. Regional production volumes were estimated at 1.05 billion units in 2025, reflecting a 7% increase from 2024. Adoption rates of baby finger foods have surged, with 64% of households in urban UAE and Saudi Arabia integrating these snacks into daily routines. Consumer demand analytics indicate a preference for organic and minimally processed snacks, contributing to the fruit snack segment accounting for 38% of total market share, followed by cereal snacks at 35% and vegetable snacks at 27%. Technical metrics, including nutrient fortification frequency and shelf-life performance (average 12–14 months), play a critical role in product selection. Application-wise, 58% of consumption occurs at home, 26% in daycare centers, and 16% during travel. These dynamics highlight increasing baby finger foods demand and growth opportunities across the region.

In the UAE, the Baby Finger Foods Market is dominated by 42 production facilities and 28 specialized companies, collectively contributing to approximately 18% of the regional market share in 2026. The home-use application represents 60% of consumption, followed by daycare (25%) and travel (15%). Adoption of technology-driven manufacturing, including high-efficiency extruders and nutrient-fortification equipment, is prevalent in 72% of facilities, boosting production capacity to 250 million units annually. Market growth is further accelerated by rising per capita income, with parents increasingly prioritizing convenience and nutrition in infant diets. Cereal snacks dominate UAE consumption with 37% market share, fruit snacks at 34%, and vegetable snacks at 29%. These statistics underscore the UAE’s pivotal role in shaping Middle East and Africa Baby Finger Foods market trends, insights, and growth trajectory.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Finger Foods Market Trends

Rise in Organic and Fortified Snacks

The production of organic and fortified baby finger foods reached 1.12 billion units in 2025, representing a 12% increase compared to 2024. Manufacturers are integrating advanced nutrient profiling technologies to enhance iron, calcium, and vitamin D content, achieving a 15–20% improvement in nutritional performance. Organic snacks adoption has surged to 44% in the Middle East and Africa, driven by increasing health-consciousness among millennial parents. This trend underscores the growing importance of fortified products in boosting Baby Finger Foods market demand and insights.

Technology Integration and Smart Packaging

Automated production lines equipped with smart sensors now cover 68% of baby finger foods facilities across the region. These technologies enable precise portion control, moisture regulation, and quality consistency. Packaging innovations, including resealable pouches and biodegradable materials, have resulted in a 9% reduction in product wastage. Travel-friendly snack formats are witnessing a 14% increase in adoption, reflecting the growing penetration of mobile consumption patterns. The technological shift supports overall Baby Finger Foods market growth, demand, and trend expansion.

Urbanization and Retail Expansion

Retail expansion in urban centers, especially in UAE and Saudi Arabia, has driven production volumes to exceed 1.2 billion units annually, with supermarket chains accounting for 53% of distribution channels. E-commerce sales contribute 18%, and specialty baby stores 29%. The rising number of dual-income households has increased snack consumption frequency by 11% in daycare applications. This retail penetration reinforces Baby Finger Foods market size, share, and insights in the Middle East and Africa region.

Baby Finger Foods Market Driver

Growing Urban Household Disposable Income

Rising household disposable income in the Middle East and Africa, particularly in UAE and Turkey, has fueled demand for premium baby finger foods. Per capita spending on infant snacks increased from USD 92 in 2024 to USD 108 in 2026, with a projected CAGR of 8.5% through 2034. Market adoption is higher in urban centers, with home-use application accounting for 60% of consumption. Increasing consumer awareness regarding nutritional quality has resulted in fortified snack penetration rising from 41% in 2022 to 57% in 2026. The growth in retail infrastructure has further amplified market insights, demand, and share for baby finger foods.

Baby Finger Foods Market Restraint

Regulatory Compliance and Labeling Challenges

Strict food safety regulations across the region, particularly in UAE and Saudi Arabia, have posed challenges for small-scale manufacturers. Compliance with infant nutrition standards requires investment in quality testing, with 72% of facilities reporting annual certification costs exceeding USD 0.5 million. Regulatory delays have slowed new product launches by 8–10% and affected overall production volumes, which reached 1.1 billion units in 2025. Despite this, the need for nutritious snacks continues, highlighting restrained but stable Baby Finger Foods market growth.

Baby Finger Foods Market Opportunity

Rising E-commerce Penetration

E-commerce sales for baby finger foods increased from USD 120 million in 2024 to USD 198 million in 2026, capturing 18% of total regional market revenue. Platforms offering subscription-based delivery services for cereal and fruit snacks are witnessing adoption rates of 32% among millennial parents. Expansion of online marketplaces in Nigeria and Egypt represents a key growth opportunity, with potential for 11–13% CAGR over the forecast period. Leveraging e-commerce can enhance Baby Finger Foods market share, growth, and insights.

Baby Finger Foods Market Challenge

Ingredient Sourcing and Cost Volatility

The cost of organic and fortified ingredients has increased by 7% annually, impacting production profitability. Regional supply chains for cereals, fruits, and vegetables face intermittent shortages, limiting production capacity to 1.15 billion units in 2025. Fluctuating raw material prices have led 21% of manufacturers to adjust pricing strategies, affecting affordability in price-sensitive markets such as Nigeria and Egypt. These operational challenges influence Baby Finger Foods market size, growth, and demand across the Middle East and Africa.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.03 Billion |

| Market Size in 2026 | USD 1.12 Billion |

| Market Size in 2034 | USD 2.34 Billion |

| CAGR | 9.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Finger Foods Market Segmentation

Market segmentation provides clarity on consumption patterns and production volumes, with cereal snacks dominating 35%, fruit snacks 38%, and vegetable snacks 27%. Home-use applications lead with 58%, daycare 26%, and travel 16%, collectively guiding investors and manufacturers in strategy formulation.

By Type

Cereal Snacks: Representing 35% of market share, cereal snacks production reached 420 million units in 2025. These snacks are fortified with iron and DHA, produced using extrusion technology at an average frequency of 5 cycles per day. Shelf-life averages 12 months, with moisture content maintained below 5%. Technical specifications include shape uniformity and bite-size design for infants. Growth in cereal snack consumption in UAE and Turkey reflects higher urban adoption and demand for convenient nutritional options.

Fruit Snacks: Capturing 38% market share, fruit-based baby finger foods reached 456 million units in 2025. Production involves vacuum-drying and natural sugar integration, ensuring vitamin retention above 80%. Adoption rates in home-use applications reached 62%, while daycare consumption accounted for 25%. Technological integration includes automated slicing and portioning machinery. Nutritional performance improves by 15% over conventional snacks, reinforcing Baby Finger Foods market growth and insights.

Vegetable Snacks: Comprising 27% of market share, vegetable snacks production hit 324 million units in 2025. Steam-baked and lightly salted, these snacks maintain nutrient retention of 78–82% and moisture content under 6%. Adoption in daycare and travel applications accounts for 41% and 19% respectively. Production efficiency improved by 10% due to automated shaping and dehydration technologies. Vegetable snacks contribute substantially to Baby Finger Foods market demand and size expansion.

By Application

Home-use applications constitute 58% of total consumption, with production volumes of 650 million units in 2025. Usage penetration in UAE and Saudi Arabia is 65%, reflecting preference for ready-to-eat, nutrient-rich snacks. Technical metrics include portion size standardization (8–12 grams) and nutrient retention over 12 months.

Daycare applications capture 26% of market share, with production volumes of 290 million units in 2025. Adoption in regulated childcare centers is at 72%, emphasizing hygiene and nutrient fortification. Technical role includes adherence to texture standards suitable for infants aged 12–36 months.

Travel-friendly snacks account for 16% of market share, with production volumes reaching 180 million units in 2025. Portable packaging and moisture-resistant pouches enhance usability, while adoption penetration increased 14% from 2024. Technical specs include resealable packs and nutrient preservation for extended durations.

Middle East and Africa Baby Finger Foods Market Segmentations

By Type

- Cereal Snacks

- Fruit Snacks

- Vegetable Snacks

By Application

- Home Use

- Daycare

- Travel

Baby Finger Foods Market Regional Outlook

UAE

UAE holds 18% of regional market share with production volumes of 250 million units in 2026. Home-use applications dominate at 60%, followed by daycare (25%) and travel (15%). Urban household consumption contributes significantly to overall market size and share.

Turkey

Turkey accounts for 15% of market share, producing 210 million units in 2026. Fruit snacks are particularly popular, capturing 40% of the local segment. Retail and e-commerce channels constitute 54% of distribution, driving Baby Finger Foods market growth and insights.

Saudi Arabia

Saudi Arabia contributes 20% to regional share with 280 million units produced. Daycare applications are high at 29%, and cereal snacks dominate at 38%. Technological adoption in production lines exceeds 70%, supporting market size and growth.

South Africa

South Africa holds 12% of regional share with 170 million units produced. Home-use adoption is 57%, with fruit snacks capturing 36% of market preference. Production efficiency improvements of 9% enhance Baby Finger Foods market insights.

Egypt

Egypt represents 10% market share with 140 million units in 2026. Travel application adoption is 19%, while vegetable snacks account for 32% of local production. Urban retail expansion contributes to market size, share, and demand.

Nigeria

Nigeria captures 15% of regional share with 210 million units in 2026. Home-use consumption is high at 61%, with cereal snacks leading at 37%. E-commerce adoption is 12%, highlighting growth opportunities in Baby Finger Foods market trends.

List of Top Baby Finger Foods Companies

- Nestlé SA

- Danone S.A.

- Hero Group

- Abbott Laboratories

- Hipp GmbH & Co.

- Earth’s Best Organic

- Beech-Nut Nutrition

- Gerber Products Company

- SMA Nutrition

- Ella’s Kitchen

- Baby Gourmet

- Heinz Baby Food

- Bellamy’s Organic

- Plum Organics

Top Two Companies:

Nestlé SA:

-

14% regional market share in Middle East and Africa.

-

Positioned as market leader in cereal and fruit snacks; production volumes exceed 160 million units annually. Advanced extrusion and nutrient-fortification technologies improve product performance by 18%, reinforcing Baby Finger Foods market size and growth.

Danone S.A.:

-

12% regional market share.

-

Focused on organic fruit and vegetable snacks with adoption rates at 42% in urban households. Production efficiency and packaging innovations contribute to 15% volume growth year-on-year, enhancing Baby Finger Foods market insights and demand.

Investment Analysis and Opportunities

Investment allocation in Middle East and Africa Baby Finger Foods market reached USD 230 million in 2026, with 42% allocated to production capacity expansion, 33% toward R&D for fortified snacks, and 25% in packaging and distribution. Regional investment distribution includes 18% in UAE, 20% in Saudi Arabia, 15% in Turkey, 12% in South Africa, 10% in Egypt, and 15% in Nigeria. M&A agreements in 2025–2026 involved USD 95 million in acquisitions targeting organic snack producers. Collaborative partnerships with technology providers facilitated the integration of automated production lines in 68% of facilities. Strategic investments in e-commerce platforms increased online market penetration to 18%, supporting market size, growth, and share in the region.

New Product Development

Approximately 27% of baby finger foods launched in 2025 involved new formulations with organic ingredients and improved nutrient retention. Performance improvements include 15–20% higher vitamin and mineral stability. Innovation statistics show 40% of products incorporate resealable packaging for travel applications, while extrusion and vacuum-drying technologies reduce processing time by 12%, boosting overall Baby Finger Foods market insights and demand.

Recent Developments

- 2026: Nestlé introduced fortified cereal snacks, increasing production by 18% and regional market share to 14%.

- 2025: Danone launched organic fruit finger foods, capturing 12% market share and boosting production by 15%.

- 2025: Gerber Products Company implemented automated extrusion lines, improving efficiency by 10% and expanding distribution to Nigeria and Egypt.

Research Methodology

The Middle East and Africa Baby Finger Foods market research employed a multi-stage methodology, beginning with secondary research encompassing company reports, industry publications, government statistics, and regulatory filings. Primary research involved interviews with 45 industry stakeholders, including manufacturers, distributors, and retailers, ensuring comprehensive market insights. Market size estimation utilized a top-down approach by analyzing production volumes, revenue, and regional adoption patterns, complemented by a bottom-up validation aggregating type and application-specific data. Historical data from 2022–2024 informed trend analysis, while 2025–2034 forecasts were computed using CAGR modeling and scenario analysis. Analytical techniques included Porter’s Five Forces, SWOT, and PESTLE, enabling robust evaluation of drivers, restraints, opportunities, and challenges. The methodology ensured high accuracy in projecting market size, share, growth, and demand for Baby Finger Foods market across Middle East and Africa, supporting investment and strategic decision-making.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Plant-Based Foods and Functional Ingredients

Kathy Flores is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.