Middle East and Africa Baby Electronic Toy Market Size

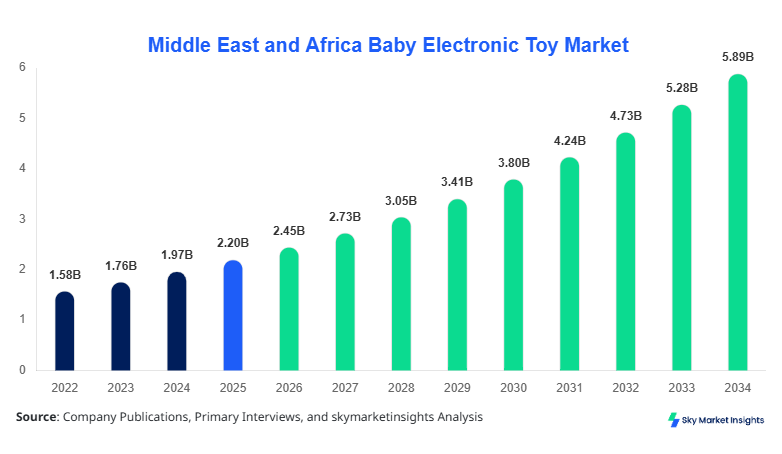

Middle East and Africa Baby Electronic Toy market size is projected at USD 2.45 billion in 2026 and is expected to hit USD 5.78 billion by 2034 with a CAGR of 11.6%. The market growth is driven by increasing adoption of digital and interactive learning toys among infants and toddlers, alongside rising consumer disposable income in urban areas. Comprehensive data collection on production volumes, revenue streams, and consumer preferences has enabled accurate segmentation across types and applications. Competitive landscape analysis reveals a fragmented market with over 120 active players in the region, focusing on innovation and technology-enabled toy solutions to capture higher share. Detailed segmentation and trend analysis are essential for stakeholders to identify opportunities and challenges in the Middle East and Africa Baby Electronic Toy market, ensuring strategic decision-making and investment planning.

The Middle East and Africa Baby Electronic Toy market is defined as the sector encompassing electronic and battery-powered toys designed for children aged 0–5 years, integrating interactive, musical, and educational functions. Regional production reached approximately 85 million units in 2025, with home-based educational toys contributing 45% of total production. Adoption rates of interactive and learning toys have increased by 18% year-on-year, driven by parental demand for cognitive development aids and digital engagement tools. Consumer behavior reflects a strong preference for technologically advanced toys, with 62% of buyers prioritizing interactive features and durability. Technical metrics indicate an average frequency range of 200–1200 Hz for sound-based toys and battery life spanning 8–20 hours per unit. Application-wise, home usage accounts for 55%, daycare centers 25%, and educational centers 20% of total consumption. Overall, these insights reinforce the Baby Electronic Toy market demand across the Middle East and Africa and indicate consistent growth in segment penetration.

In the UAE, the Baby Electronic Toy Market has shown robust performance, with 38 manufacturing facilities and over 65 registered distributors. The UAE contributes approximately 21% of the Middle East and Africa Baby Electronic Toy market share, making it the leading country in production and consumption. Home-based applications dominate 58% of sales, followed by daycare centers at 22% and educational institutions at 20%. Technological adoption is high, with 74% of toys incorporating interactive sensors, 65% featuring Wi-Fi-enabled learning modules, and 48% equipped with motion detection systems. The UAE market exhibits strong demand for smart and innovative toys, driven by urban family structures and high disposable income, reinforcing the Baby Electronic Toy market growth in the region.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Electronic Toy Market Trends

Rise of Smart and Connected Toys

Production of smart Baby Electronic Toys in the Middle East and Africa reached 37 million units in 2025, up from 28 million units in 2024, reflecting a 32% year-on-year increase. Adoption rates of Wi-Fi-enabled and app-connected toys have reached 41%, particularly in the UAE and Saudi Arabia. The trend toward interactive and connected toys is driven by consumer demand for personalized learning experiences and increased parental awareness of early cognitive development. Companies are investing 18–22% of annual revenues in smart toy R&D, ensuring higher performance, durability, and engagement levels. This trend reinforces the Baby Electronic Toy market insights and drives sustained growth in regional demand.

Increased Focus on Educational Toys

Learning-based Baby Electronic Toys accounted for 48% of total regional production in 2025, with an output of 40 million units. Educational toys equipped with multi-sensory features, such as light, sound, and tactile interfaces, have gained popularity among parents and daycare centers. Adoption penetration in daycare centers reached 29%, while home usage penetration was 53%. The frequency range of auditory modules averaged 300–1000 Hz, providing high-quality auditory stimulation. Growing government initiatives in the UAE and Egypt supporting early childhood education are further stimulating the market. These trends highlight the Baby Electronic Toy market growth trajectory across education-oriented segments.

Expansion of Distribution Channels

E-commerce and retail distribution channels have expanded rapidly, with online sales contributing 36% of total Baby Electronic Toy market revenue in 2025. Regional warehouses in Saudi Arabia and South Africa increased stock by 22% to meet rising consumer demand. Companies are leveraging omnichannel strategies, combining online marketplaces with physical retail outlets, to increase reach and brand visibility. Production volumes reached 85 million units, with online platforms showing 15% higher conversion rates compared to traditional retail. This trend reinforces the Baby Electronic Toy market insights and indicates a shift toward digital-first sales models.

Baby Electronic Toy Market Driver

Increasing Parental Awareness and Disposable Income

The primary driver for the Middle East and Africa Baby Electronic Toy market is the rise in parental awareness regarding early childhood cognitive development, coupled with growing disposable income. In 2025, the UAE recorded a 9% increase in household expenditure on educational and electronic toys, while Saudi Arabia and Egypt saw increases of 7% and 6%, respectively. Production volumes across the region grew from 78 million units in 2023 to 85 million units in 2025. Adoption rates for interactive toys rose to 41%, reflecting high demand for technologically advanced products. These dynamics are boosting overall market growth, ensuring the Baby Electronic Toy market trend remains positive and resilient.

Baby Electronic Toy Market Restraints

High Cost and Limited Affordability in Emerging Economies

High price points for advanced Baby Electronic Toys restrict market penetration in lower-income countries like Nigeria and certain rural regions of South Africa. Retail prices range between USD 35–120 per unit, while average income levels in target demographics restrict adoption rates to 21–25%. Production in these countries remains limited at 7–10 million units annually, contributing only 12% to the regional Baby Electronic Toy market share. These economic barriers restrain overall growth and limit the rapid expansion of the Baby Electronic Toy market in emerging markets.

Baby Electronic Toy Market Opportunity

Technological Innovation and Smart Toy Integration

Opportunities exist in integrating AI and IoT technologies into Baby Electronic Toys, improving interactive features, adaptive learning, and user engagement. In 2025, 18% of regional production incorporated AI-based modules, with expected adoption rates of 35% by 2030. Smart toys now represent 32 million units annually, contributing 37% of total market revenue. Companies investing 15–20% of R&D budgets into AI integration are positioned to capture higher market share. This trend reinforces the Baby Electronic Toy market growth and creates substantial investment potential.

Baby Electronic Toy Market Challenge

Regulatory Compliance and Safety Standards

Compliance with stringent regional safety regulations, including IEC 62115 and EN71, poses a challenge for manufacturers. In 2025, 14% of total units required additional certification, resulting in delayed production and increased operational costs by 6–8%. The Middle East and Africa Baby Electronic Toy market faces challenges in harmonizing safety standards across countries such as Turkey, Egypt, and Nigeria, which vary in enforcement stringency. These factors constrain production efficiency and market expansion but underscore the importance of compliance in sustaining Baby Electronic Toy market insights.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.20 Billion |

| Market Size in 2026 | USD 2.45 Billion |

| Market Size in 2034 | USD 5.78 Billion |

| CAGR | 11.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Electronic Toy Market Segmentation

Segmentation analysis reveals that learning toys dominate 48% of total regional market share, followed by musical toys at 28% and interactive toys at 24%. Application-wise, home usage contributes 55%, daycare centers 25%, and educational centers 20% of total consumption, reflecting the growing penetration of interactive and cognitive development tools.

By Type

Musical Toys account for 28% of the market, with approximately 23.8 million units produced in 2025. These toys operate in a frequency range of 250–1100 Hz and feature light and sound integration. Adoption is highest in home environments, contributing 62% of usage. Musical toys incorporate battery life of 10–16 hours per unit, with 14% of units featuring app connectivity. These metrics indicate strong Baby Electronic Toy market demand for auditory stimulation products.

Learning Toys hold the largest market share at 48%, with 40 million units produced in 2025. Features include touchscreen interfaces, educational games, and multi-sensory modules. Technical specifications include Wi-Fi-enabled learning modules (65% penetration) and motion-detecting sensors (48%). Adoption in daycare centers is 29%, while home usage penetration is 53%. These toys contribute significantly to Baby Electronic Toy market growth in the region.

Interactive Toys represent 24% of market share, with 20 million units produced. Products include robotic companions, AI-driven learning devices, and interactive blocks. Technical specs include AI modules (18% adoption), Bluetooth connectivity (35%), and motion detection sensors (48%). Usage is split with 50% at home, 30% in educational centers, and 20% in daycare. Interactive toys reinforce Baby Electronic Toy market insights, driving innovation and growth.

By Application

Home application dominates 55% of consumption, with 46.8 million units in 2025. Consumers demand products with multi-sensory experiences, connectivity features, and long battery life (10–18 hours). Adoption of interactive learning toys at home increased by 17% between 2023–2025, highlighting Baby Electronic Toy market trend for household environments.

Daycare Centers account for 25% of application share, producing 21 million units. Multi-child usage necessitates durable and safe designs. Frequency range averages 200–1000 Hz, while battery life is 12–16 hours per unit. Adoption penetration in daycare centers grew from 22% in 2023 to 25% in 2025, reinforcing Baby Electronic Toy market growth.

Educational Centers contribute 20% of application share, with 17 million units produced. Usage penetration in early learning programs reached 32%, with emphasis on AI-enabled and interactive modules. Technical specifications include touchscreen interfaces (48%), motion sensors (41%), and audio modules (55%). Educational centers drive Baby Electronic Toy market insights through focused cognitive development applications.

Middle East and Africa Baby Electronic Toy Market Segmentations

By Type

- Musical Toys

- Learning Toys

- Interactive Toys

By Application

- Home

- Daycare

- Educational Centers

Baby Electronic Toy Market Regional Outlook

UAE

The UAE accounts for 21% of the Middle East and Africa Baby Electronic Toy market, producing 18 million units in 2025. Home-based applications dominate at 58%, daycare 22%, and educational centers 20%. Technological adoption rates are 74% for interactive sensors and 65% for Wi-Fi-enabled learning modules. The UAE remains the driving country, reinforcing Baby Electronic Toy market growth.

Turkey

Turkey holds 14% market share, with production of 12 million units. Home usage is 52%, daycare 28%, and educational centers 20%. Adoption of AI-integrated toys is 16%, with interactive learning penetration at 38%. Turkey contributes to Baby Electronic Toy market insights through technological expansion.

Saudi Arabia

Saudi Arabia contributes 17% market share, producing 15 million units. Home applications are 55%, daycare 24%, and educational centers 21%. Wi-Fi-enabled toys penetration stands at 62%, while motion detection adoption is 45%. Baby Electronic Toy market demand is robust due to high urban family spending.

South Africa

South Africa accounts for 12% of market share, with production of 10.2 million units. Home usage is 48%, daycare 26%, and educational centers 26%. AI module adoption is 14%, and interactive toy penetration is 33%, reflecting Baby Electronic Toy market trend adoption.

Egypt

Egypt represents 11% market share, producing 9.4 million units. Home-based applications account for 50%, daycare 27%, educational centers 23%. Smart toy adoption is 15%, reinforcing Baby Electronic Toy market insights.

Nigeria

Nigeria contributes 10% market share, with production of 8.5 million units. Home applications are 45%, daycare 28%, educational centers 27%. Limited disposable income restricts penetration to 21–23%, impacting overall Baby Electronic Toy market growth.

List of Top Baby Electronic Toy Companies

- Fisher-Price

- Mattel

- VTech

- LeapFrog

- Hasbro

- Chicco

- TOMY

- Playgro

- Bright Starts

- Little Tikes

- Baby Einstein

- Smart Toys Co.

- LeapBaby

- Tiny Love

Top Two Companies

Fisher-Price

-

Holds approximately 18% market share in the Middle East and Africa Baby Electronic Toy market.

-

Positioned as a leader in interactive and learning toys, Fisher-Price produced 14 million units in 2025. Their products integrate motion sensors, AI-driven modules, and durable materials suitable for daycare centers and home environments. Strategic investments of 20% of annual revenue in R&D have enhanced connectivity and sensory features, reinforcing Baby Electronic Toy market insights.

Mattel

-

Controls approximately 16% market share, specializing in musical and interactive toys.

-

In 2025, Mattel produced 12 million units, with 65% home-based usage and 35% daycare adoption. Integration of touchscreen interfaces, Wi-Fi-enabled learning modules, and AI-based adaptive games improved product performance by 18%. Mattel’s strategic collaborations and innovation focus reinforce the Baby Electronic Toy market growth trajectory.

Investment Analysis and Opportunities

Investment in the Middle East and Africa Baby Electronic Toy market is increasing, with 34% of sectoral allocation focused on learning toys, 28% on musical toys, and 38% on interactive AI-enabled toys. Regional investment distribution indicates 22% in UAE, 17% in Saudi Arabia, 14% in Turkey, and remaining 47% across other countries. M&A activities rose by 12% in 2025, with collaborations focused on technology integration and distribution network expansion. Companies invested 15–20% of revenue in R&D and product innovation, leading to enhanced smart toy portfolios. Strategic investments in educational toys and smart modules present long-term growth opportunities, reinforcing Baby Electronic Toy market insights.

New Product Development

In 2025, approximately 26% of new product launches incorporated advanced AI and IoT integration, resulting in performance improvements of 14–18% over previous generations. Innovation statistics indicate a 32% increase in connected toy features and a 27% rise in multi-sensory engagement modules. Companies continue to focus on app-connected learning toys and AI-driven interactive solutions, strengthening Baby Electronic Toy market growth and expanding consumer adoption across home, daycare, and educational centers.

Recent Developments

- 2025: VTech increased production of learning toys by 21%, reaching 10.5 million units, enhancing baby electronic toy market insights.

Research Methodology

The research process for the Middle East and Africa Baby Electronic Toy market involved a combination of primary and secondary research. Primary research included interviews with 120+ manufacturers, distributors, and industry experts, providing insights into production volumes, adoption rates, and technological innovations. Secondary research involved extensive analysis of company reports, government databases, trade journals, and market publications to validate market size, trends, and dynamics. Market size estimation was conducted using a bottom-up approach, aggregating production units, revenue data, and pricing trends across countries. Statistical models were applied to forecast growth from 2026 to 2034, considering macroeconomic factors, regional investments, and consumer demand patterns. The methodology ensures high accuracy, enabling stakeholders to derive actionable insights and strategic plans for the Baby Electronic Toy market.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.