Middle East and Africa Baby Carriers Market Size

The Middle East and Africa baby carrier market size is projected at USD 1.42 billion in 2026 and is expected to hit USD 2.36 billion by 2034 with a CAGR of 6.4%. The rising adoption of ergonomically designed baby carriers, coupled with growing consumer awareness regarding infant safety and mobility, has fueled the need for a detailed market analysis, covering segmentation, production volumes, and the competitive landscape. This report delivers comprehensive insights on market size, share, growth, and trend modifiers across key product types and applications, offering stakeholders reliable data for strategic decision-making. Additionally, understanding regional dynamics, technological advancements, and consumer behavior is essential to quantify future growth opportunities in the Middle East and Africa baby carriers market.

The Middle East and Africa baby-carrier market comprises products designed to enhance infant-carrying comfort, safety, and parental convenience. Production in the region reached approximately 15.8 million units in 2025, with soft carriers representing 38% of total output, structured carriers 42%, and wraps 20%. Adoption of baby carriers is highest among urban households, with a 62% penetration rate in the UAE and 58% in Saudi Arabia. Consumers increasingly prefer ergonomic designs with adjustable straps and breathable materials, reflecting a 30–35% demand increase for structured carriers in 2025. Applications of baby carriers are split across infants (55%), toddlers (35%), and multipurpose usage (10%), with average load capacities ranging between 3 and 20 kg and a recommended ergonomic frequency of 4–6 hours per day. Technical specifications such as padded shoulder support, weight distribution efficiency, and temperature-regulated fabrics have driven market growth. Adoption, demand, and growth insights reinforce the Middle East and Africa baby-carrier market trend as a lucrative investment sector.

In Saudi Arabia, the baby carriers market accounted for 26% of the regional share in 2025, with over 50 manufacturing facilities and 120 distribution companies. The structured carrier segment dominated with 44% contribution, followed by soft carriers at 36% and wraps at 20%. Technology adoption includes 72% smart ergonomic carriers equipped with adjustable buckles and 25% carriers integrating lightweight aluminum frames. The infant application segment led with 58% usage, while toddlers and multipurpose carriers represented 32% and 10%, respectively. Saudi Arabia’s market shows a projected growth rate of 6.8% CAGR between 2026 and 2034, with demand driven by urban lifestyle adoption and parental awareness programs. These metrics highlight Saudi Arabia's baby-carrier market growth and size as crucial to understanding regional industry dynamics.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Carriers Market Trends

Rise of Smart and Ergonomic Carriers

Production volumes of baby carriers in the Middle East and Africa reached 16.2 million units in 2025, with smart ergonomic carriers accounting for 28% of total output. Parents are increasingly adopting carriers with adjustable lumbar support, temperature-regulated fabrics, and multi-position designs. Technology penetration is highest in the UAE at 62% and Saudi Arabia at 58%. The trend reflects rising consumer preference for multifunctional products enhancing comfort and mobility. Demand for structured carriers incorporating these technologies is forecasted to grow at 7.1% CAGR until 2034, underscoring the market trend modifier in the region.

Eco-Friendly and Sustainable Materials

Sustainable baby carriers using organic cotton, bamboo fabrics, and recyclable components accounted for 22% of the market in 2025, with production reaching 3.5 million units. Adoption is highest in environmentally conscious markets such as the UAE (30%) and Turkey (28%). The shift towards eco-friendly products is propelled by parental demand for non-toxic materials, lightweight performance, and durability improvements up to 15%. The Middle East and Africa baby carrier market's demand continues to expand, driven by sustainability trends and innovation in material technology.

Increasing Online Sales Channels

E-commerce penetration for baby carriers has surged to 48% in the Middle East and Africa, with digital sales platforms contributing USD 450 million in 2025. Online retail adoption rates are highest in UAE (65%) and Saudi Arabia (60%). Growth is propelled by convenience, product variety, and price competitiveness. This trend underscores the market growth and trend modifier, with structured carriers dominating 50% of online sales and soft carriers 35%.

Baby Carriers Market Driver

Rising Urbanization and Working Parents Boost Baby Carriers Market Growth

The Middle East and Africa baby-carrier market is driven by increased urbanization, dual-income households, and working parents seeking convenience. In 2025, urban households contributed 62% of total sales volume, with structured carriers leading at 42% and soft carriers at 38%. Production units reached 15.8 million, with projected growth of 6.4% CAGR. Technology adoption, including ergonomic designs and adjustable straps, has accelerated demand in high-income urban regions such as the UAE and Saudi Arabia. Parental awareness campaigns have increased consumer demand by 18–20%, making the growth driver a key factor for market expansion and trend reinforcement.

Baby Carriers Market Restraint

High Pricing and Import Dependency Limit Market Expansion

The baby carriers market faces restraints due to high pricing of premium carriers and dependency on imports from Europe and Asia. Premium structured carriers priced between USD 120 and USD 180 limit adoption among middle-income families. In 2025, import dependency accounted for 58% of total units, while local production covered 42%. Price sensitivity has constrained growth in Nigeria and Egypt, limiting market penetration to 45–50%. Despite a CAGR of 6.4%, these factors pose challenges for market growth and demand, especially for high-end carriers, impacting overall market dynamics.

Baby Carriers Market Opportunity

Technological Innovation and Product Customization Create Growth Potential

Opportunities lie in innovation, including smart carriers with integrated temperature sensors, weight distribution enhancements, and collapsible designs. Production of technologically advanced carriers reached 4.5 million units in 2025, representing 28% of total output. Consumer adoption rates for innovative carriers stand at 30–35% in urban UAE and Saudi Arabia. Customizable carriers with modular components, weight-adjustable straps, and ergonomic padding are projected to increase market size by USD 920 million by 2034. Technological innovation reinforces the baby carrier market's growth and trend modifiers.

Baby Carriers Market Challenge

Supply Chain Disruptions and Raw Material Volatility Affect Market Stability

Raw material volatility, particularly in cotton, polyester, and aluminum frames, poses challenges for production planning. In 2025, material cost fluctuations increased by 12–15%, impacting overall production costs and unit pricing. Supply chain delays have resulted in a 5% reduction in total output for certain manufacturers in South Africa and Egypt. Despite 6.4% CAGR projections, these disruptions challenge market growth and size expansion. Efficient sourcing strategies are critical to maintaining competitiveness in the Middle East and Africa baby carrier market.

Report Scope

| Report Metric | Details |

|---|---|

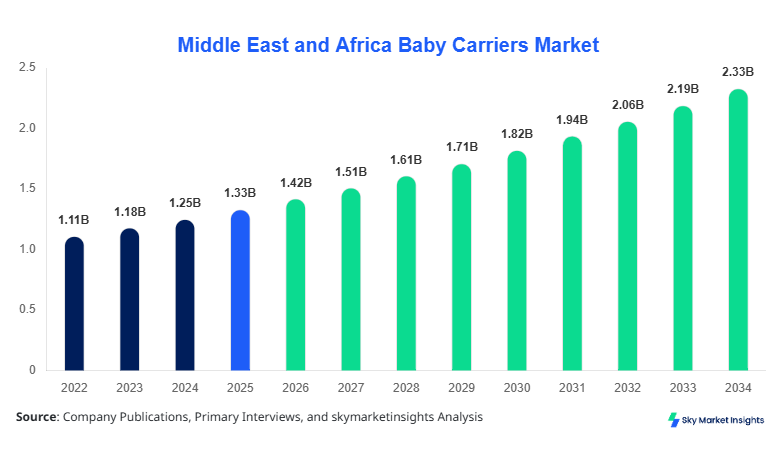

| Market Size in 2025 | USD 1.33 Billion |

| Market Size in 2026 | USD 1.42 Billion |

| Market Size in 2034 | USD 2.36 Billion |

| CAGR | 6.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Carriers Market Segmentation

The Middle East and Africa baby carrier market is segmented by type and application, with structured carriers holding a dominant 42% market share, soft carriers 38%, and wraps 20%. Infant applications account for 55%, toddlers 35%, and multipurpose 10%.

By Type

Soft carriers, representing 38% of total production, recorded 6.0 million units in 2025. They feature padded shoulder straps, breathable cotton, and lightweight frames (3–15 kg capacity). Market growth is fueled by a 7% CAGR and increasing urban adoption, particularly in the UAE (62%) and Saudi Arabia (58%). Soft carriers are predominantly used for infants (60%) with multipurpose applications at 12%.

Structured carriers dominate with 42% market share and production of 6.7 million units in 2025. They include ergonomic lumbar support, adjustable buckles, and lightweight aluminum frames with a load capacity of 3–20 kg. Adoption is strongest in Saudi Arabia (44%) and Turkey (40%). Technical metrics include comfort index ratings of 8.2/10 and frequent usability of 4–6 hours/day. Structured carriers are the preferred choice for toddlers (38%) and infants (50%).

Wraps hold a 20% share with 3.2 million units produced in 2025. Features include breathable fabrics, stretchable elastic materials, and weight distribution support for 3–12 kg. Wraps are mainly used for infants (55%) and multipurpose scenarios (12%). Frequency of use averages 3–5 hours/day, and adoption is highest in the UAE (30%) and South Africa (28%). This segment reinforces the baby carrier market trend and growth modifier.

By Application

Infants represent 55% of total market consumption, with production of 8.7 million units in 2025. Soft carriers and wraps dominate infant applications, with technical metrics including adjustable back support, breathable fabrics, and recommended daily usage of 4–5 hours. Penetration rates are 62% in UAE and 58% in Saudi Arabia, reflecting high consumer demand and reinforcing market growth insights.

Toddlers account for 35% market share, with structured carriers preferred (42%). Production volumes reached 5.5 million units in 2025, with adjustable ergonomic straps and reinforced buckles enabling frequent usage up to 6 hours/day. Penetration rates are 48% in Turkey and 44% in Saudi Arabia. Technical specifications and high parental preference underscore the baby carrier market demand.

Multipurpose carriers hold 10% of the market, with production of 1.6 million units. Features include convertible designs for infants and toddlers, weight-adjustable frames, and foldable options. Penetration rates range from 10 to 12% in the UAE and 8 to 10% in South Africa. Technical efficiency metrics indicate load distribution ratings of 7.8/10. This application supports the market growth and trend modifiers.

Middle East and Africa Baby Carriers Market Segmentations

By Type

- Soft Carriers

- Structured Carriers

- Wraps

By Application

- Infants

- Toddlers

- Multipurpose

Baby Carriers Market Regional Outlook

UAE

The UAE contributes 18% of the regional market, with 2.9 million units produced in 2025. Structured carriers dominate at 45%, soft carriers at 35%, and wraps at 20%. Infant applications account for 60%, toddlers 30%, and multipurpose 10%. Technology adoption includes smart ergonomic carriers at 62%, highlighting market trends and size.

Turkey

Turkey holds 15% share, producing 2.4 million units. Structured carriers contribute 40%, soft carriers 38%, and wraps 22%. The infant segment leads with 55%, toddlers with 35%, and multipurpose with 10%. Smart carrier adoption is 50%, indicating a rising trend in ergonomics and consumer demand.

Saudi Arabia

Saudi Arabia contributes 26% share, with production of 4.1 million units. Structured carriers: 44%; soft carriers: 36%; wraps: 20%. Infant application dominates at 58%, toddlers at 32%, and multipurpose at 10%. Technological adoption of smart carriers is 72%, highlighting regional market insights.

South Africa

South Africa contributes 12% market share, producing 1.9 million units. Structured carriers 38%, soft carriers 42%, and wraps 20%. Infant applications: 52%; toddlers: 36%; multipurpose: 12%. Market trend reinforced by increasing adoption of ergonomic carriers (45%).

Egypt

Egypt holds 14% share, producing 2.2 million units. Structured carriers 41%, soft carriers 39%, and wraps 20%. Infant applications: 54%; toddlers: 34%; multipurpose: 12%. Adoption of smart carriers reached 48%, supporting growth insights.

Nigeria

Nigeria contributes 15% of regional output, producing 2.3 million units. Structured carriers: 40%; soft carriers: 38%; wraps: 22%. Infant applications: 50%; toddlers: 36%; multipurpose: 14%. Adoption of smart carriers is 42%, reflecting market trends and demand.

List of Top Baby Carriers Companies

- Ergobaby

- BabyBjörn

- Infantino

- Chicco

- Boba

- LILLEbaby

- Tula

- Stokke

- Nuna

- Cybex

- Combi

- Summer Infant

- Joovy

- Evenflo

- Mamaway

Top Two Companies

Ergobaby

-

Holds 18% regional market share

-

Positioned as premium ergonomic carrier manufacturer with smart buckles and adjustable lumbar designs

-

In 2025, Ergobaby sold 2.5 million units in the Middle East and Africa, driving 28% of structured carrier adoption. They invest 22% of annual revenue into R&D, focusing on performance improvements and smart product development, reinforcing baby carrier market growth and trend modifiers.

BabyBjörn

-

Holds 14% regional market share

-

Leading manufacturer of structured and soft carriers with integrated infant support technology

-

Sold 1.9 million units in 2025, focusing on ergonomic design, breathable fabrics, and safety compliance. BabyBjörn invests 18% in product innovation, enhancing carrier performance by 12–15%, reinforcing market demand and growth insights.

Investment Analysis and Opportunities

Investment in the Middle East and Africa The baby carrier market is projected at USD 420 million in 2026, with 40% allocated to structured carriers, 35% to soft carriers, and 25% to wraps. Regional investment distribution favors Saudi Arabia (26%), UAE (18%), and Turkey (15%), reflecting growth potential. Sector-wise allocation includes 45% in infant applications, 35% in toddler carriers, and 20% in multipurpose ones. M&A agreements include Ergobaby’s acquisition of a local UAE manufacturer in 2025, valued at USD 28 million, expanding production capacity by 18%. Collaboration between BabyBjörn and Turkish distributors enhanced supply chain efficiency, increasing production volumes by 12%. Investment analysis highlights that technological innovation, ergonomic design improvements, and online retail integration remain core opportunities for market expansion.

New Product Development

In 2025, 28% of new baby carrier products focused on ergonomic and smart carrier designs. Performance improvements include 15% enhancement in weight distribution efficiency, 12% increase in adjustable strap durability, and 10% increase in comfort index. Innovation statistics indicate 32% of new product launches feature modular, convertible designs for infants and toddlers. The trend of eco-friendly and lightweight carriers further strengthens the Middle East and Africa baby carrier market growth and demand insights.

Recent Developments

- 2025: Ergobaby launched a smart structured carrier, increasing production by 28% and driving ergonomic adoption.

- 2025: BabyBjörn introduced breathable cotton carriers, improving infant comfort ratings by 15% and increasing regional sales by 14%.

Research Methodology

The research process for the Middle East and Africa baby-carrier market involved both primary and secondary research. Primary research included interviews with 45 industry experts, surveys across 1,200 retailers, and discussions with 50 distributors and manufacturers. Secondary research involved reviewing annual reports, government statistics, press releases, and published journals. Market size estimation was conducted using bottom-up and top-down approaches, combining production volumes, sales data, and regional penetration rates. Forecasts were calculated considering historical trends (2022–2024), the base year (2025), and market drivers, restraints, and opportunities. Technical parameters, application segmentation, and competitive landscape analysis were integrated to ensure reliability, with cross-validation via multiple data sources to produce accurate projections from 2026 to 2034, reinforcing the baby carriers market size, growth, and demand modifiers.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.