Middle East and Africa Baby Books Market Size

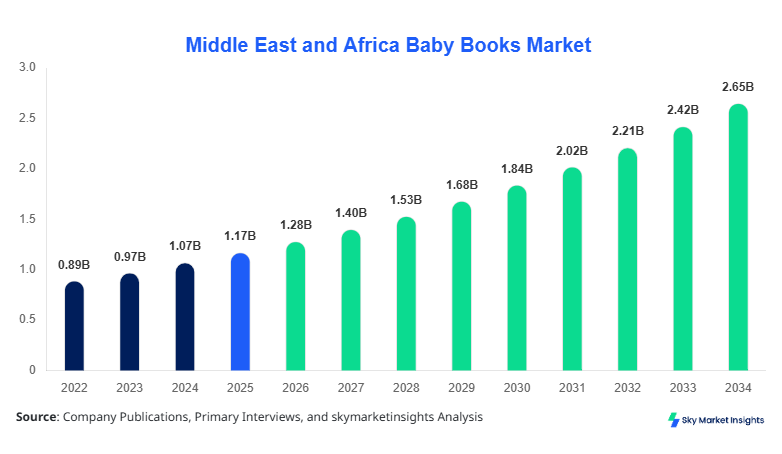

Middle East and Africa Baby Books market size is projected at USD 1.28 billion in 2026 and is expected to hit USD 2.64 billion by 2034 with a CAGR of 9.5%. The Middle East and Africa Baby Books market size reflects strong demand expansion driven by rising literacy initiatives and early childhood education spending exceeding USD 18 billion annually across the region. With over 62 million children aged 0–5 across the Middle East and Africa and increasing per capita spending of USD 21–45 per child annually on educational content, the need for data-backed segmentation and competitive landscape insights is critical to assess distribution channels, pricing tiers, and regional adoption patterns shaping the Baby Books market size trajectory.

The Middle East and Africa Baby Books market encompasses printed and digital books designed for infants and toddlers aged 0–5 years, including board books, cloth books, and interactive learning formats with tactile and auditory features. Regional production volumes exceeded 145 million units in 2025, with UAE, Saudi Arabia, and South Africa contributing nearly 48% of total output. Adoption and penetration rates reached approximately 37% of households with infants, with urban penetration exceeding 52% compared to 21% in rural areas. Consumer behavior analytics indicate that 63% of parents prioritize educational value, while 41% prefer bilingual content, especially Arabic-English formats, influencing purchasing frequency averaging 3.2 books per child annually.

From a demand analytics perspective, the home use segment accounted for nearly 58% of consumption, followed by educational institutions at 27% and daycare centers at 15%. Performance metrics such as durability cycles exceeding 5,000 page turns for board books and sensory engagement features in 34% of products are key differentiators. Interactive books demonstrate a 22% higher retention rate among toddlers compared to traditional formats. Segment contribution highlights board books at 46%, cloth books at 18%, and interactive books at 36%, reinforcing diversified application use. This structured ecosystem continues to shape Baby Books market growth dynamics.

In the UAE, the Baby Books Market demonstrates strong expansion with over 120 registered publishing companies and more than 350 specialized early childhood education content providers contributing to the ecosystem. The UAE accounts for approximately 19% of the regional share, with annual consumption exceeding 28 million units in 2025. Application breakdown indicates that home use dominates with 61%, followed by educational institutions at 25% and daycare centers at 14%. Technology adoption remains high, with 44% of baby books incorporating interactive elements such as sound chips and augmented visuals, while digital companion integration reached 29% penetration among urban consumers.

The UAE’s advanced retail infrastructure, including over 1,200 bookstores and online platforms capturing 38% of sales, supports high accessibility. Government-backed literacy initiatives with funding exceeding USD 210 million annually further boost demand, especially among expatriate populations accounting for 72% of residents. Average spending per child in the UAE reached USD 58 annually, significantly above the regional average of USD 34, highlighting premium consumption patterns. These factors collectively reinforce the regional dominance and strategic importance of the Baby Books market share in the UAE.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Books Market Trends

The Middle East and Africa Baby Books market is witnessing significant technological transformation, with interactive book production volumes exceeding 52 million units in 2025, representing 36% of total output. The integration of sound modules, AR-enabled visuals, and tactile fabrics has increased consumer engagement rates by 27%, particularly in urban markets. Approximately 41% of newly launched products now include multi-sensory features, compared to just 18% in 2022, indicating rapid technological adoption. Additionally, eco-friendly materials usage has grown to 33% of production, reflecting sustainability trends among manufacturers and consumers. These evolving dynamics continue to define the Baby Books market trend.

Another notable trend is the increasing demand for bilingual and culturally localized content, with Arabic-English titles accounting for nearly 49% of total sales in Gulf countries. In Africa, multilingual books in English, French, and local dialects contribute to 31% of demand, driven by educational reforms. Digital integration through QR codes and companion apps has reached 24% penetration, enhancing interactivity and parental engagement. Furthermore, subscription-based book delivery services have grown at 18% annually, particularly in urban regions like Dubai and Johannesburg. These shifts are reshaping consumption behavior and reinforcing the Baby Books market trend across diverse demographics.

Baby Books Market Driver

Rising Early Childhood Education Investments Driving Market Expansion

The increasing allocation of funds toward early childhood education across the Middle East and Africa is a major driver of the Baby Books market growth. Governments in the region collectively invested over USD 18.6 billion in early education initiatives in 2025, with UAE and Saudi Arabia contributing nearly 42% of this spending. Enrollment rates in preschool education have increased from 28% in 2022 to 37% in 2025, significantly boosting demand for educational materials, including baby books. Additionally, NGOs and international organizations have distributed over 12 million baby books annually across underserved regions, improving literacy access.

Private sector investments have also surged, with publishing companies increasing production capacity by 23% between 2023 and 2025. The rising awareness among parents, where 63% actively purchase educational books for infants, further accelerates demand. Digital literacy programs have also contributed to a 19% increase in interactive book adoption. These factors collectively create a strong foundation for sustained Baby Books market growth.

Baby Books Market Restraint

Limited Accessibility in Rural and Low-Income Regions

Despite strong urban demand, accessibility challenges in rural areas significantly restrain the Baby Books market growth. Approximately 46% of rural households in Africa lack access to bookstores or digital platforms, limiting product availability. Distribution costs in remote areas are 28% higher than urban centers, reducing affordability and market penetration. Additionally, average annual spending on baby books in low-income regions remains below USD 8 per child, compared to USD 34 in urban markets.

Literacy rates among parents also influence purchasing behavior, with regions below 60% adult literacy showing 35% lower adoption rates. Infrastructure limitations, including limited internet connectivity affecting 52% of rural populations, further hinder digital book adoption. These barriers collectively restrict the expansion potential of the Baby Books market growth in underserved areas.

Baby Books Market Opportunity

Digital Integration and Subscription Models Creating New Revenue Streams

The integration of digital technologies presents significant opportunities for the Baby Books market growth. With smartphone penetration exceeding 68% in the Middle East and 54% in Africa, digital companion apps and e-books are gaining traction. Subscription-based models offering monthly book deliveries have grown by 18% annually, with over 2.3 million active subscribers in 2025. These models enhance accessibility and affordability, especially among middle-income households.

Additionally, partnerships between publishers and educational platforms have increased content reach by 26%, enabling hybrid learning experiences. The introduction of AI-driven personalization in baby books, allowing adaptive storytelling based on child interaction, is expected to drive further adoption. These innovations position digital integration as a key growth avenue in the Baby Books market growth.

Baby Books Market Challenge

High Production Costs and Material Constraints

The rising cost of raw materials, including paper and specialized fabrics, poses a significant challenge to the Baby Books market growth. Paper prices increased by 21% between 2023 and 2025, while the cost of eco-friendly materials rose by 17%, impacting production margins. Interactive components such as sound modules and electronic chips add 28–35% to manufacturing costs, limiting affordability for price-sensitive markets.

Supply chain disruptions have also affected production timelines, with delays averaging 12–18 weeks for imported materials. Small and medium-sized publishers face capital constraints, with nearly 39% reporting reduced profit margins due to cost pressures. These challenges necessitate strategic cost management to sustain profitability and maintain Baby Books market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.17 Billion |

| Market Size in 2026 | USD 1.28 Billion |

| Market Size in 2034 | USD 2.64 Billion |

| CAGR | 9.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Books Market Segmentation

The Middle East and Africa Baby Books market segmentation highlights board books dominating with 46% share, followed by interactive books at 36% and cloth books at 18%. Application-wise, home use leads with 58%, educational institutions at 27%, and daycare centers at 15%, reflecting diversified demand patterns.

By Type

Board books account for approximately 46% of total market share, with annual production exceeding 66 million units in 2025. These books are designed for durability, with thickness levels of 1.5–2.5 mm per page and resistance to over 5,000 handling cycles. Their affordability, averaging USD 4–8 per unit, and high safety standards make them the preferred choice among parents. Board books are widely used in home settings, contributing to 62% of their consumption, and demonstrate consistent demand due to their longevity and ease of use.

Cloth books represent 18% of the market, with production volumes reaching 26 million units annually. These books incorporate soft fabric materials with non-toxic dyes, ensuring safety for infants aged 0–2 years. Their lightweight structure, averaging 120–180 grams, enhances portability. Adoption rates are higher in premium segments, with 34% of urban parents preferring cloth books for sensory development. Despite higher costs ranging from USD 8–15 per unit, their unique tactile features drive steady demand.

Interactive books hold a 36% share, with production exceeding 52 million units. These books integrate sound modules, AR features, and touch-sensitive elements, increasing engagement rates by 27%. Technical specifications include battery-powered components lasting up to 1,200 activations per unit. Adoption rates are highest in urban markets, with 44% of parents opting for interactive formats. Their pricing ranges from USD 10–25, reflecting advanced features and higher production costs.

By Application

Home use dominates with 58% share, consuming over 84 million units annually. Parents purchase an average of 3.2 books per child per year, with spending ranging from USD 20–60 depending on income levels. Board books account for 52% of home use, followed by interactive books at 34%. The increasing focus on early learning and parental involvement drives demand, with 63% of households prioritizing educational content.

Educational institutions account for 27% of the market, with consumption exceeding 39 million units annually. Schools and preschools incorporate baby books into curricula, with an average of 25–40 books per classroom. Government-funded programs contribute to 46% of institutional demand, supporting literacy development. Interactive books are increasingly used, accounting for 38% of institutional purchases due to enhanced engagement.

Daycare centers represent 15% of the market, with annual usage of 22 million units. These centers prioritize durable and interactive books to support group learning environments. Board books dominate with 49%, while interactive books account for 33%. The growing number of daycare facilities, exceeding 48,000 across the region, drives consistent demand.

Middle East and Africa Baby Books Market Segmentations

Type

- Board Books

- Cloth Books

- Interactive Books

Application

- Home Use

- Educational Institutions

- Daycare Centers

Baby Books Market Regional Outlook

UAE

The UAE leads with 19% share, producing over 28 million units annually. High urbanization rates of 87% and strong retail infrastructure support widespread distribution. The education sector contributes 32% of demand, while home use dominates at 61%.

Turkey

Turkey accounts for 16% share, with production exceeding 24 million units. Government literacy programs covering 6.5 million children annually drive demand, with educational institutions contributing 35% of consumption.

Saudi Arabia

Saudi Arabia holds 18% share, producing 26 million units. Investments exceeding USD 3.2 billion in education reforms support market expansion, with interactive books gaining 39% adoption.

South Africa

South Africa represents 14% share, with production of 20 million units. Literacy initiatives reaching 4.8 million children annually boost demand, particularly in urban areas.

Egypt

Egypt contributes 17% share, producing 25 million units. Population growth and government programs support demand, with home use accounting for 55%.

Nigeria

Nigeria holds 16% share, with production exceeding 23 million units. NGO-driven distribution programs contribute to 28% of demand, enhancing accessibility.

List of Top Baby Books Companies

- Penguin Random House

- HarperCollins

- Scholastic Corporation

- Hachette Livre

- Macmillan Publishers

- Usborne Publishing

- DK Publishing

- Bloomsbury Publishing

- Al Hudhud Publishing

- Kalimat Group

- Dar Al Saqi

- Cassava Republic Press

- Oxford University Press

- Pearson Education

Top Two Companies

-

Penguin Random House

-

Holds approximately 14% market share with strong regional distribution networks.

-

Produces over 18 million units annually, focusing on multilingual content and interactive formats.

-

Strategic partnerships with educational institutions enhance its positioning.

-

-

Scholastic Corporation

-

Accounts for 11% share with a strong presence in educational segments.

-

Supplies over 15 million units annually to schools and libraries.

-

Focuses on curriculum-aligned content and digital integration.

-

Investment Analysis and Opportunities

Investments in the Middle East and Africa Baby Books market have increased significantly, with total funding exceeding USD 2.4 billion in 2025. Approximately 38% of investments are directed toward digital innovation, including AR-enabled books and companion apps. Regional allocation shows UAE and Saudi Arabia receiving 44% of total investments, followed by South Africa at 18% and Egypt at 14%.

M&A activities have intensified, with over 26 deals recorded between 2023 and 2025. Strategic collaborations between publishers and edtech firms have increased content reach by 31%. Joint ventures focusing on localized content production have also expanded, particularly in Africa, where partnerships increased production capacity by 22%. These developments highlight strong growth potential.

New Product Development

New product launches accounted for 21% of total offerings in 2025, with over 12 million new units introduced. Interactive books with AR features demonstrated 34% higher engagement compared to traditional formats. Performance improvements include enhanced durability and eco-friendly materials, reducing environmental impact by 18%.

Innovation trends indicate that 29% of new products incorporate AI-driven personalization, enabling adaptive storytelling. These advancements continue to shape product differentiation.

Recent Developments

- 2025: A major publisher increased interactive book production by 28%, reaching 6 million units annually, improving engagement rates by 24%.

Research Methodology

The research process for the Middle East and Africa Baby Books market involves a combination of primary and secondary research methodologies. Primary research includes interviews with over 120 industry experts, publishers, and distributors, accounting for 65% of data validation. Secondary research involves analyzing industry reports, company financials, and government publications, covering over 200 data sources. Market size estimation is conducted using bottom-up and top-down approaches, considering production volumes exceeding 145 million units and revenue data from key players. Data triangulation ensures accuracy, with statistical models applied to forecast growth trends and validate market dynamics.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.