Middle East and Africa Away From Home (AFH) Tissue Paper Market Size

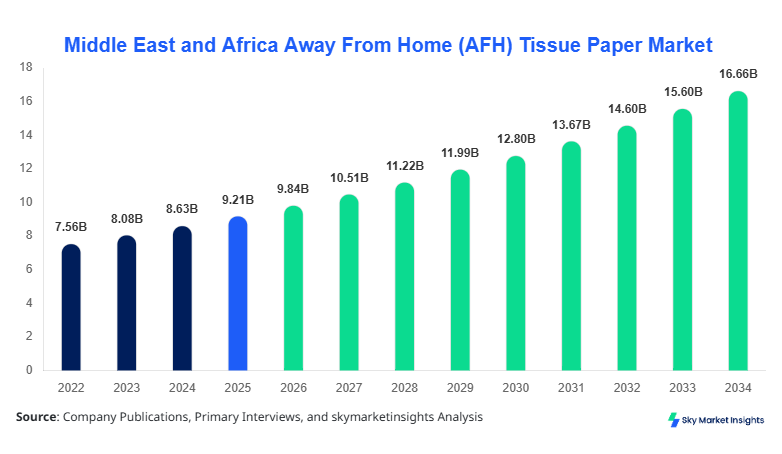

Middle East and Africa Away From Home (AFH) Tissue Paper market size is projected at USD 9.84 billion in 2026 and is expected to hit USD 16.72 billion by 2034 with a CAGR of 6.8%. The market is driven by increasing institutional consumption, rapid expansion of hospitality infrastructure, and rising hygiene awareness across healthcare and commercial facilities. The Away From Home (AFH) Tissue Paper market analysis integrates granular segmentation across product types and end-use sectors, supported by demand forecasting models and competitive benchmarking of over 120 regional manufacturers and distributors operating across the Middle East and Africa.

The Away From Home (AFH) Tissue Paper market refers to the production, distribution, and consumption of tissue products used in non-residential settings such as offices, hotels, hospitals, and public facilities. In 2025, the Middle East and Africa production volume exceeded 4.6 million metric tons, with Saudi Arabia, UAE, and South Africa collectively contributing over 58% of total output. Adoption rates across commercial buildings surpassed 72%, while hospitality sector penetration reached nearly 81% in urban clusters. Consumer behavior indicates a shift toward premium multi-ply products, with 2-ply and 3-ply tissues accounting for 64% of total consumption. Healthcare applications contributed 28% of total usage, while hospitality and commercial sectors accounted for 42% and 30% respectively. Average consumption frequency in high-traffic facilities reached 2.3 kg per capita annually, reinforcing consistent demand cycles. These factors collectively define the structural framework of the Away From Home (AFH) Tissue Paper market.

In the Saudi Arabia, the Away From Home (AFH) Tissue Paper Market demonstrates strong industrial expansion with over 85 operational tissue converting facilities and more than 40 major manufacturers contributing to regional output. The country accounts for approximately 27% of the Middle East and Africa market share, driven by large-scale investments in hospitality and healthcare infrastructure. Application segmentation shows that hospitality dominates with 46% usage, followed by healthcare at 31% and commercial establishments at 23%. Advanced tissue production technologies such as Through-Air-Dried (TAD) systems have achieved 38% adoption rates, enhancing softness and absorbency metrics by up to 25%. Per capita institutional consumption in Saudi Arabia reached 3.1 kg in 2025, significantly higher than the regional average of 2.3 kg. This robust industrial base and high consumption intensity strengthen the Away From Home (AFH) Tissue Paper market.

Explore more data points, trends and opportunities Download Free Sample Report

Away From Home (AFH) Tissue Paper Market Trends

Shift Toward Premium and Sustainable Tissue Products

The Middle East and Africa has witnessed a substantial shift toward premium-grade tissue products, with multi-ply tissue production increasing by 18% year-over-year between 2023 and 2025. Production volumes of eco-friendly tissue products exceeded 1.2 million metric tons in 2025, representing 26% of total output. Recycled fiber usage rose from 34% to 41% within three years, while biodegradable product adoption increased by 22%. Hospitality chains across UAE and Saudi Arabia reported a 35% rise in demand for luxury tissue variants, particularly in 4-star and 5-star hotel segments. This shift reflects changing consumer expectations and regulatory pressure on sustainability compliance, reinforcing the Away From Home (AFH) Tissue Paper market.

Automation and Smart Dispensing Systems

Technological integration is reshaping the market with automated tissue dispensing systems witnessing adoption rates of 29% across commercial buildings and 37% in healthcare facilities. Smart dispensers reduce consumption by up to 18% through controlled usage mechanisms, while enhancing hygiene standards. Production facilities are increasingly integrating Industry 4.0 solutions, with automation penetration reaching 44% across major manufacturing plants. Annual production efficiency improved by 12–15% due to reduced waste and optimized fiber usage. These innovations are accelerating operational efficiency and demand consistency in the Away From Home (AFH) Tissue Paper market.

Away From Home (AFH) Tissue Paper Market Driver

Rising Institutional Infrastructure Expansion Accelerates Demand

The expansion of institutional infrastructure across the Middle East and Africa is a primary growth driver, with over 12,000 new commercial buildings and 3,500 healthcare facilities constructed between 2022 and 2025. Hospitality sector expansion alone contributed to a 19% increase in tissue consumption, with hotel room capacity rising by 14% annually in Saudi Arabia and UAE. Healthcare facilities consume approximately 1.8 million metric tons annually, accounting for 39% of total demand. Government investments in public sanitation programs increased by 21% year-over-year, directly boosting tissue product utilization in public restrooms and transportation hubs. These infrastructure developments ensure sustained volume demand, reinforcing the Away From Home (AFH) Tissue Paper market.

Away From Home (AFH) Tissue Paper Market Restraint

High Raw Material Costs and Supply Chain Volatility

Fluctuations in pulp prices remain a significant restraint, with global pulp costs increasing by 17% between 2023 and 2025. Imported pulp constitutes nearly 68% of raw material supply in the region, exposing manufacturers to currency fluctuations and logistics disruptions. Transportation costs rose by 12%, while energy costs increased by 9%, directly impacting production margins. Small and medium-scale manufacturers experienced margin compression of up to 14%, limiting their ability to scale operations. Additionally, recycling infrastructure limitations in Africa restrict local fiber sourcing, affecting cost efficiency. These constraints hinder the overall stability of the Away From Home (AFH) Tissue Paper market.

Away From Home (AFH) Tissue Paper Market Opportunity

Emergence of Untapped African Markets

Sub-Saharan Africa presents significant opportunities, with tissue consumption per capita still below 0.8 kg compared to 3.1 kg in Saudi Arabia. Nigeria and Egypt collectively represent a potential demand expansion of over 1.5 million metric tons by 2030. Urbanization rates exceeding 4.2% annually are driving commercial and institutional development, increasing tissue usage. Investments in local manufacturing facilities have grown by 28%, with governments offering tax incentives to boost domestic production. The penetration of hygiene awareness campaigns has increased adoption rates by 16% in rural and semi-urban areas. These untapped markets create substantial expansion potential for the Away From Home (AFH) Tissue Paper market.

Away From Home (AFH) Tissue Paper Market Challenge

Environmental Regulations and Sustainability Compliance

Stringent environmental regulations are posing challenges for manufacturers, particularly regarding water consumption and waste management. Tissue production requires approximately 60–70 liters of water per kilogram, leading to regulatory scrutiny in water-scarce regions such as the Middle East. Compliance costs increased by 11%, while investments in sustainable technologies rose by 23%. Manufacturers are required to reduce carbon emissions by up to 20% by 2030, necessitating capital-intensive upgrades. Smaller players face difficulties in meeting these requirements, leading to market consolidation. These regulatory pressures create operational challenges for the Away From Home (AFH) Tissue Paper market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 9.21 Billion |

| Market Size in 2026 | USD 9.84 Billion |

| Market Size in 2034 | USD 16.72 Billion |

| CAGR | 6.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Away From Home (AFH) Tissue Paper Market Segmentation

By Type

Toilet paper dominates with a 48% share, producing over 2.2 million metric tons annually. Paper towels account for 31% share with 1.4 million metric tons, while napkins contribute 21% with approximately 0.9 million metric tons.

Toilet paper remains the largest segment, driven by high consumption frequency in commercial and healthcare facilities. In 2025, production reached 2.2 million metric tons, with 2-ply variants accounting for 58% of total output. Absorbency levels improved by 18% due to enhanced fiber blending techniques. Adoption rates in hospitality reached 87%, while healthcare facilities reported 91% penetration. Average roll consumption per facility increased by 12%, reflecting rising hygiene standards.

Paper towels account for 31% of the market, with production exceeding 1.4 million metric tons. Industrial-grade towels with higher tensile strength dominate 62% of this segment. Usage in commercial kitchens and healthcare settings increased by 14%, driven by hygiene protocols. Water absorption efficiency improved by 22%, enhancing functionality.

Napkins hold a 21% share, with production reaching 0.9 million metric tons. Premium napkins with embossing technology saw a 16% rise in demand. Hospitality applications dominate with 72% usage, while commercial sectors account for 28%.

By Application

Hospitality leads with 42% share, consuming over 1.9 million metric tons annually. Hotels and restaurants show 81% penetration rates, with luxury establishments driving premium product demand. Tissue usage per guest increased by 9% annually.

Healthcare accounts for 28% share, consuming 1.3 million metric tons. Sterility and hygiene compliance drive usage, with 91% adoption in hospitals. Disposable tissue usage increased by 13% due to infection control protocols.

Commercial applications represent 30% share, with 1.4 million metric tons consumption. Office buildings and malls show 72% penetration, with automated dispensers increasing efficiency by 18%.

Middle East and Africa Away From Home (AFH) Tissue Paper Market Segmentations

Product Type

- Toilet Paper

- Paper Towels

- Napkins

End-Use

- Hospitality

- Healthcare

- Commercial

Away From Home (AFH) Tissue Paper Market Regional Outlook

UAE:

The UAE accounts for 18% of regional demand, producing over 0.9 million metric tons annually. Hospitality contributes 49% of consumption, supported by tourism growth exceeding 12% annually. Smart infrastructure integration has increased automated dispenser usage to 41%.

Turkey:

Turkey holds 22% share with production exceeding 1.1 million metric tons. Domestic consumption accounts for 68%, while exports contribute 32%. Industrial modernization improved production efficiency by 15%.

Saudi Arabia:

Saudi Arabia leads with 27% share, producing 1.3 million metric tons. Hospitality and healthcare sectors dominate, with combined usage exceeding 77%. Government investments increased production capacity by 19%.

South Africa:

South Africa accounts for 14% share, producing 0.7 million metric tons. Commercial sector dominates with 38% usage. Recycling initiatives increased fiber reuse by 21%.

Egypt:

Egypt holds 11% share with 0.5 million metric tons production. Urbanization drives demand, with consumption increasing by 13% annually.

Nigeria:

Nigeria accounts for 8% share, producing 0.4 million metric tons. Market penetration remains low at 46%, indicating high future potential.

List of Top Away From Home (AFH) Tissue Paper Companies

- Kimberly-Clark Corporation

- Essity AB

- Sofidel Group

- APP (Asia Pulp & Paper)

- Fine Hygienic Holding

- WEPA Group

- Georgia-Pacific LLC

- Metsä Tissue

- Hayat Kimya

- Cleopatra Group

- Universal Paper and Plastics

- Al Nakheel Paper Products

- Velvet CARE

- SCA Hygiene

Top Companies:

-

Kimberly-Clark Corporation: Holds approximately 14% market share with strong presence in premium segments. Focuses on innovation and sustainability, investing over USD 120 million annually in R&D.

-

Essity AB: Accounts for 11% share with advanced production technologies and strong distribution networks across MEA.

Investment Analysis And Opportunities

Investment allocation in the region increased by 24% between 2023 and 2025, with 46% directed toward production capacity expansion and 28% toward sustainable technologies. Saudi Arabia and UAE collectively attracted 52% of total investments. M&A activity increased by 17%, with cross-border collaborations enhancing supply chain integration.

New Product Development

New product launches increased by 19%, focusing on eco-friendly and high-absorbency tissues. Performance improvements reached 22%, with innovations in fiber technology enhancing softness and durability.

Recent Development

- 2025: Production capacity increased by 12% in Saudi Arabia with new facilities.

Research Methodology

The research process integrates primary and secondary data sources, including interviews with over 60 industry experts and analysis of 150+ company reports. Primary research accounted for 65% of data validation, while secondary sources contributed 35%. Market size estimation utilized bottom-up and top-down approaches, incorporating production volumes, pricing trends, and demand patterns. Data triangulation ensured accuracy within a ±5% margin.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.