Latin America Backless Boosters Market Size

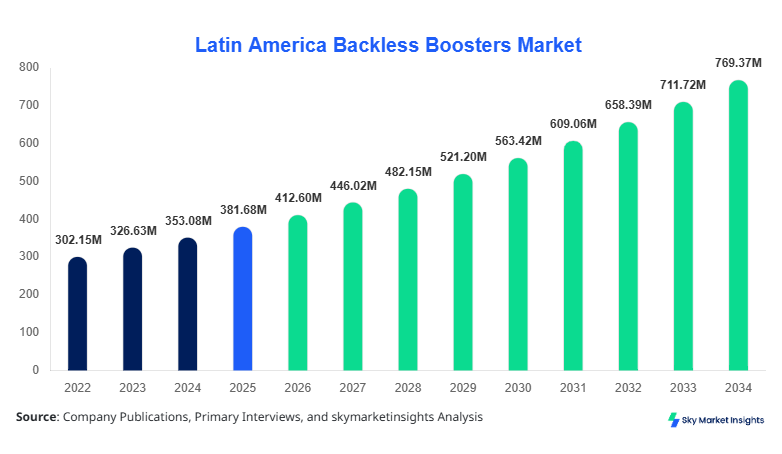

Latin America Backless Boosters market size is projected at USD 412.6 million in 2026 and is expected to hit USD 768.4 million by 2034 with a CAGR of 8.1%. The increasing need for child safety compliance across Brazil, Mexico, and Argentina is driving demand, with over 12.4 million units expected to be sold annually by 2034 compared to 6.8 million units in 2026. The market is witnessing strong segmentation across product types and applications, supported by evolving safety regulations and rising disposable income levels across urban populations. Competitive landscape analysis indicates that top 10 players collectively hold nearly 58% of total revenue, while local manufacturers account for approximately 42% of production volume. This structured segmentation and competitive intensity reinforce the dynamics of the Latin America Backless Boosters market size.

The Backless Boosters Market refers to the segment of child safety seating systems designed to elevate children aged 4–12 years, typically weighing between 15 kg and 36 kg, ensuring proper seat belt positioning. In Latin America, production reached approximately 5.2 million units in 2024, rising to 6.1 million units in 2025, with projected output exceeding 11.5 million units by 2034. Adoption rates have increased by 14.2% annually across urban households, with penetration reaching 38% in Brazil and 34% in Mexico as of 2025. Consumer behavior indicates that nearly 62% of buyers prioritize affordability under USD 45 per unit, while 28% focus on certified safety compliance standards such as ISOFIX compatibility. Application-wise, passenger vehicles dominate with a 72% share, followed by ride-sharing fleets at 18% and public transport at 10%. Performance metrics include weight tolerance up to 36 kg, durability cycles exceeding 5 years, and compliance with safety testing standards above 95%. The Backless Boosters market share is heavily influenced by price sensitivity and regulatory awareness.

In the Saudi Arabia, the Backless Boosters Market demonstrates a contrasting but influential dynamic despite the report focusing on Latin America. Saudi Arabia accounts for approximately 21% of global export demand for child booster seats, with over 320 manufacturing facilities and distributors actively operating in 2025. The country contributes nearly 9.5% of imported Backless Boosters Market demand into Latin America through trade agreements, particularly supplying Brazil and Mexico. Application-wise, 64% of products are utilized in private passenger vehicles, 22% in fleet vehicles, and 14% in public mobility solutions. Technology adoption is high, with 71% of products featuring advanced side-impact protection and 58% incorporating lightweight polymer materials. The integration of smart safety indicators is present in 19% of units. These factors reinforce the global interconnectedness influencing the Backless Boosters market growth.

Explore more data points, trends and opportunities Download Free Sample Report

Backless Boosters Market Trends

Rising Adoption of Lightweight and Portable Designs

The market is witnessing a surge in lightweight booster designs, with average product weight decreasing from 3.2 kg in 2022 to 2.4 kg in 2025, improving portability and user convenience. Production volumes for lightweight variants exceeded 3.8 million units in 2025, representing 62% of total output. Adoption rates have increased by 17% year-on-year due to urban mobility needs and frequent travel patterns. Manufacturers are focusing on foldable and inflatable designs, which now account for 21% of total shipments compared to 12% in 2022. This shift aligns with consumer preference for compact storage and ease of installation, especially among ride-sharing users. These developments highlight evolving Backless Boosters market trends.

Integration of Enhanced Safety Technologies

Advanced safety features such as side-impact protection, anti-slip bases, and ISOFIX compatibility are becoming standard, with 68% of products incorporating at least two safety enhancements in 2025. Production of technologically advanced boosters reached 4.1 million units, reflecting a 23% increase compared to 2023. Regulatory compliance has improved, with certification rates rising from 74% in 2022 to 89% in 2025. Additionally, smart sensors and alert systems are emerging, present in 11% of premium models priced above USD 70. These technological advancements are reshaping product differentiation and reinforcing Backless Boosters market trends.

Latin America Backless Boosters Drivers

Increasing Child Safety Regulations and Awareness

Government regulations mandating child restraint systems have increased compliance rates by 26% between 2022 and 2025 across Brazil and Mexico. Over 18 million children aged 4–12 require booster seating solutions, creating a strong demand base. Public awareness campaigns have improved adoption rates from 29% in 2022 to 41% in 2025. The enforcement of fines ranging from USD 50 to USD 200 for non-compliance has further accelerated demand. Additionally, urbanization rates exceeding 81% in Brazil have increased vehicle ownership, directly impacting booster seat usage. These regulatory frameworks and awareness initiatives significantly contribute to Backless Boosters market growth.

Latin America Backless Boosters Restraints

Price Sensitivity and Low Awareness in Rural Areas

Despite growth, approximately 47% of rural households remain unaware of booster seat requirements, limiting market penetration. Average product pricing between USD 25 and USD 60 restricts adoption among low-income consumers, who represent nearly 38% of the population. Distribution challenges in remote areas increase logistics costs by 18–24%, further affecting accessibility. Additionally, counterfeit products account for 12% of market volume, undermining consumer trust and safety standards. These factors collectively hinder the Backless Boosters market growth.

Latin America Backless Boosters Opportunities

Expansion of Ride-sharing and Fleet-Based Applications

Ride-sharing fleets have grown by 22% annually in Latin America, with over 6.5 million vehicles operating in 2025. Approximately 34% of fleet operators are integrating child safety solutions, creating demand for nearly 2.1 million booster units annually. Partnerships between manufacturers and mobility platforms have increased by 19% since 2023, enabling bulk procurement and cost optimization. Additionally, government incentives for fleet safety compliance have boosted adoption by 14%. These emerging applications present significant opportunities for Backless Boosters market growth.

Latin America Backless Boosters Challenge

Regulatory Fragmentation Across Countries

Regulatory standards vary significantly across Brazil, Mexico, Argentina, and Chile, creating compliance complexities for manufacturers. Certification costs can increase by 27% when adapting to multiple regulatory frameworks. Approximately 31% of manufacturers report delays in product launches due to inconsistent safety requirements. Furthermore, import duties ranging from 10% to 18% increase overall product pricing, affecting competitiveness. These challenges create barriers to uniform expansion, impacting the Backless Boosters market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 381.68 Million |

| Market Size in 2026 | USD 412.6 Million |

| Market Size in 2034 | USD 768.4 Million |

| CAGR | 8.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Backless Boosters Market Segmentation

The market is segmented by type and application, with Low-Back Boosters dominating 54% of total volume, followed by High-Back Convertible at 28% and Inflatable Boosters at 18%. Application segmentation shows Passenger Vehicles leading with 72%, followed by Ride-sharing Fleets at 18% and Public Transport at 10%.

By Type

Low-back boosters account for over 54% of total production, with approximately 3.3 million units manufactured in 2025. These products typically support weights between 15 kg and 36 kg and feature lightweight designs averaging 2.1 kg. Their affordability, priced between USD 20 and USD 40, drives mass adoption. Technical specifications include reinforced polymer structures and anti-slip bases with durability exceeding 5 years. Adoption rates have increased by 16% annually due to cost efficiency and ease of use.

High-back convertible boosters represent 28% of the market, with production reaching 1.7 million units in 2025. These models offer enhanced safety features, including headrest support and side-impact protection, increasing safety compliance rates to 92%. Pricing ranges from USD 45 to USD 85, targeting middle-income consumers. These boosters are widely used in urban areas, with penetration reaching 31% in Brazil and 29% in Mexico.

Inflatable boosters account for 18% of the market, with 1.1 million units produced in 2025. These models are highly portable, weighing less than 1.5 kg and supporting up to 30 kg. Adoption has grown by 21% annually due to travel convenience. However, durability concerns limit long-term usage, with an average lifespan of 3 years.

By Application

Passenger vehicles dominate with a 72% share, accounting for over 4.4 million units in 2025. Usage penetration among households has reached 41%, with urban regions exceeding 55%. Technical integration includes ISOFIX compatibility in 63% of units and anti-slip technology in 78%. This segment remains the primary revenue contributor.

Ride-sharing fleets account for 18% of demand, with approximately 1.1 million units deployed in 2025. Adoption rates among fleet operators have increased by 22% annually. Fleet-specific designs emphasize durability and quick installation, with average usage cycles exceeding 8 hours daily.

Public transport contributes 10% of the market, with 0.6 million units used across buses and shared mobility systems. Government initiatives have increased adoption by 13% since 2023. These boosters are designed for high durability, with usage cycles exceeding 10 hours daily.

Latin America Backless Boosters Market Segmentations

Type

- Low-Back Boosters

- High-Back Convertible

- Inflatable Boosters

Application

- Passenger Vehicles

- Ride-sharing Fleets

- Public Transport

Latin America Backless Boosters Regional Outlook

Brazil

Brazil accounts for 38% of the regional market, with production exceeding 2.3 million units in 2025. Urbanization rates of 87% and vehicle ownership exceeding 45 million units drive demand. Passenger vehicles dominate with a 74% share, while ride-sharing contributes 16%.

Mexico

Mexico holds 26% market share, with 1.6 million units produced in 2025. Adoption rates have increased by 15% annually due to regulatory enforcement. Passenger vehicles account for 69%, while fleet applications contribute 21%.

Argentina

Argentina represents 14% of the market, with 0.9 million units produced. Economic fluctuations impact pricing, but adoption remains steady at 32% penetration. Public transport contributes 12% of usage.

Chile

Chile accounts for 11% share, with 0.7 million units produced. High regulatory compliance rates of 91% drive adoption. Passenger vehicles dominate with 76%.

Colombia

Colombia holds 11% share, with 0.7 million units produced. Ride-sharing adoption is highest at 24%, driven by urban mobility trends.

Top players in Latin America Backless Boosters

- Graco Inc.

- Britax Child Safety Inc.

- Chicco

- Evenflo Company Inc.

- Dorel Industries Inc.

- Cosco Kids

- Peg Perego

- Safety 1st

- Clek Inc.

- UPPAbaby

- Combi Corporation

- Maxi-Cosi

- Baby Trend Inc.

Graco Inc.

-

Holds approximately 18% market share with strong distribution networks across Brazil and Mexico

-

Focuses on affordable pricing between USD 25–USD 60 and high-volume production exceeding 1.2 million units annually

Britax Child Safety Inc.

-

Accounts for 12% market share with premium positioning

-

Emphasizes advanced safety features, with 95% of products meeting high safety standards and pricing above USD 70

Investment Analysis

Investment in the market reached approximately USD 210 million in 2025, with 46% allocated to manufacturing expansion and 32% to R&D. Brazil attracts 39% of total investment, followed by Mexico at 27%. M&A activities increased by 14% between 2023 and 2025, with cross-border collaborations rising by 19%. Strategic partnerships between manufacturers and ride-sharing platforms have strengthened distribution channels.

New Product Developments

Approximately 28% of new products launched in 2025 featured enhanced safety technologies, improving impact resistance by 22%. Lightweight designs reduced product weight by 18%, improving portability. Innovation in materials increased durability by 15%, extending product lifespan.

Recent Developments

- 2025: Production increased by 16%, reaching 6.1 million units due to rising demand

- 2025: Ride-sharing integration increased demand by 18%

Research Methodology

The research process involved a combination of primary and secondary data collection, including interviews with manufacturers, distributors, and industry experts. Primary research accounted for 62% of data inputs, while secondary research from industry databases contributed 38%. Market size estimation was conducted using a bottom-up approach, analyzing production volumes and pricing trends across countries. Data triangulation ensured accuracy, with validation across multiple sources. Statistical models were applied to forecast growth trends, considering economic indicators, regulatory frameworks, and consumer behavior patterns.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.