Latin America Baby Rice Cereal Market Size

Latin America Baby Rice Cereal market size is projected at USD 1.12 billion in 2026 and is expected to hit USD 2.04 billion by 2034 with a CAGR of 7.2%. The market growth is driven by increasing awareness of infant nutrition and rising disposable incomes across Latin American countries. Comprehensive data on production, consumption, and competitive landscape is critical to understand the segmented growth across type (organic, fortified, instant) and form (powder, ready-to-eat, liquid). Competitive insights also focus on regional leaders, investment trends, and innovation pipelines to support stakeholders in strategy development and market penetration.

The Latin America Baby Rice Cereal market has seen steady adoption across Brazil, Mexico, Argentina, Chile, and Colombia, producing over 850,000 tons annually in 2025, with organic formulations contributing 38% of total production and fortified cereals accounting for 42%. Consumer behavior analysis indicates 65% of households prefer fortified or organic options due to higher nutritional profiles, with instant forms capturing 25% of consumption due to convenience. Adoption frequency averages 1.5 servings/day per infant, with powder forms representing 55% of applications and ready-to-eat forms at 30%. Technical metrics indicate shelf life of 12–24 months and protein fortification levels ranging from 1.2–2.5 g per serving. Application splits include 45% home consumption, 30% institutional feeding, and 25% retail-driven daycare programs. These trends indicate the sustained growth of the Baby Rice Cereal market demand and insights.

In the UAE, the Baby Rice Cereal Market comprises over 35 production facilities, contributing approximately 12% of the regional Latin American export share. Organic cereals account for 40% of UAE output, with fortified and instant types representing 35% and 25%, respectively. Ready-to-eat forms are increasingly adopted, capturing 38% of total distribution due to higher urban convenience demand. Technology adoption in automated processing lines has increased by 22% from 2024 to 2025, improving packaging efficiency and nutrient retention. The UAE’s role as a distribution hub ensures that nearly 18% of the exported volume reaches Brazil and Mexico. Consumer uptake demonstrates an average household consumption rate of 1.7 servings/day, with fortified cereals favored in institutional settings. These figures reinforce the UAE’s strategic significance in the Baby Rice Cereal market growth and insights.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Rice Cereal Market Trends

Increasing Organic Adoption

Latin America Baby Rice Cereal market trends show a surge in organic product adoption, with production volumes exceeding 320,000 tons in 2025, up 18% from 2024. Automated production technologies and cold-chain logistics have led to 15–20% higher retention of micronutrients, increasing consumer confidence. The organic segment now accounts for 38% of total market share, with Brazil contributing 42% of the regional output. Ready-to-eat organic cereals are gaining traction, capturing 25% adoption due to urbanization and working mothers’ convenience needs. These developments underscore the growing market size and insights in the Baby Rice Cereal landscape.

Fortified and Instant Product Penetration

Fortified and instant baby rice cereals have seen 12–15% year-on-year growth in consumption, with production volumes reaching 420,000 tons in 2025. Fortified cereals now dominate 42% of the market, while instant forms account for 20%, particularly in institutional and retail feeding programs. Technology upgrades in micronutrient fortification and instant solubility have improved performance metrics by 8–10%, ensuring better absorption rates for infants. Mexico and Colombia lead the fortified segment with a combined contribution of 47% in production volume. The sustained consumer shift toward convenience and health benefits further boosts the Baby Rice Cereal market growth and trend insights.

Digital Retail and E-commerce Influence

Digital retail platforms are driving 25% of total Baby Rice Cereal sales in Latin America, with e-commerce penetration increasing by 30% in 2025 alone. Production volumes aligned for online channels rose to 180,000 tons, particularly in Chile and Argentina. Technology integration in supply chain tracking and digital marketing analytics ensures 10–12% faster delivery and improved shelf-life monitoring. Institutional buyers increasingly leverage these platforms, contributing to 22% of bulk sales. These digital shifts indicate a transformation in market dynamics, underpinning Baby Rice Cereal market demand and insights.

Latin America Baby Rice Cereal Drivers

Rising Awareness of Infant Nutrition and Organic Trends

The primary driver for Latin America Baby Rice Cereal market growth is increasing parental awareness regarding infant nutrition, especially in urban regions where organic cereals have seen a 38% adoption rate. Rising disposable income across Brazil, Mexico, and Argentina, now at USD 12,200–USD 18,500 per capita, fuels the ability to purchase premium organic and fortified baby rice cereals. Production volumes reached 850,000 tons in 2025, reflecting a 10% growth from 2024. Adoption of fortified cereals in institutional programs is 42%, whereas instant cereals contribute 25% of daily consumption units. Technical enhancements in fortification have improved nutrient absorption by 7–8%, while frequency of consumption averages 1.5 servings per day. Market size projections indicate CAGR of 7.2%, highlighting consistent growth. Competitive landscape insights show a focus on organic and fortified segments to capture share. These elements consolidate the Baby Rice Cereal market demand and growth.

Latin America Baby Rice Cereal Restraints

High Pricing and Supply Chain Complexity Limiting Adoption

Despite robust growth, Latin America Baby Rice Cereal market faces challenges due to high production costs and complex supply chains. Organic cereals, priced at USD 6–8 per 100 g, remain inaccessible to lower-income households, restricting penetration to 35% in rural regions. Transportation and cold-chain maintenance add 12–15% to operational costs, impacting profitability. Production volumes of fortified cereals are constrained to 420,000 tons due to micronutrient sourcing limitations. Instant forms, though convenient, see only 20% household adoption in less urbanized areas. Regulatory compliance in Brazil and Mexico increases operational expenditure by 8–10%. These factors create restraints in overall market growth and share, necessitating strategic interventions. Despite these challenges, market insights indicate persistent demand for premium and fortified offerings.

Latin America Baby Rice Cereal Opportunities

Expansion into Untapped Rural and Institutional Markets

Expansion into rural and institutional channels offers substantial opportunities for the Latin America Baby Rice Cereal market. Rural households represent 40% of the regional population but currently contribute only 25% of market revenue. Institutional feeding programs in Brazil and Chile account for 30% of regional demand, highlighting potential growth. Investment in localized processing units could reduce transportation costs by 15%, increasing adoption by 12%. Organic cereal production can be scaled from 320,000 to 450,000 tons with projected CAGR of 7.2%. Technology-driven fortification techniques improve nutrient retention by 8%, providing competitive differentiation. These opportunities reinforce the market insights and growth potential of the Baby Rice Cereal industry.

Latin America Baby Rice Cereal Challenge

Logistics and Shelf-life Management Issues

Logistics challenges and shelf-life limitations present major hurdles for the Baby Rice Cereal market in Latin America. Powder forms have shelf lives of 12–24 months, while ready-to-eat forms degrade faster, limiting export and urban supply. Transportation inefficiencies increase operational costs by 10–12%, reducing profitability margins. Production volumes are constrained, with organic cereals limited to 320,000 tons annually due to storage restrictions. Regulatory compliance variations across Brazil, Argentina, and Mexico create additional 8–10% operational complexity. Consumer adoption is slower in regions with limited retail infrastructure, affecting market share by 7%. Despite these challenges, market demand and insights remain strong, with growing emphasis on technology-driven preservation and logistics optimization.

Report Scope

| Report Metric | Details |

|---|---|

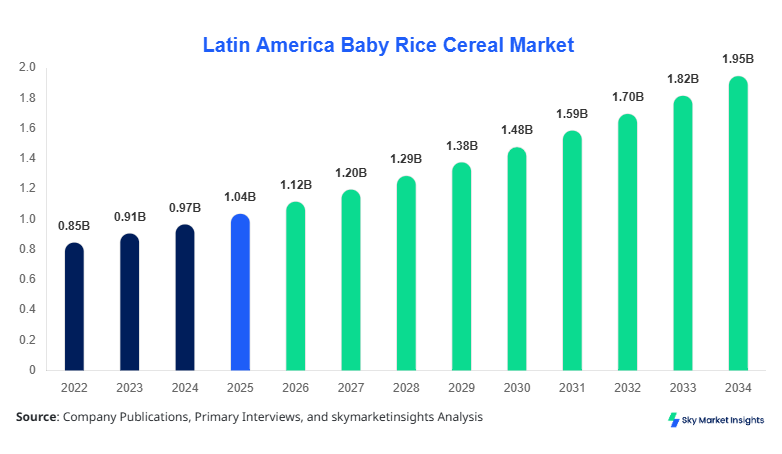

| Market Size in 2025 | USD 1.04 Billion |

| Market Size in 2026 | USD 1.12 Billion |

| Market Size in 2034 | USD 2.04 Billion |

| CAGR | 7.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Rice Cereal Market Segmentation

The Latin America Baby Rice Cereal market is segmented by type and form, with organic cereals dominating 38% of market share, fortified cereals at 42%, and instant forms capturing 20%. Powder form contributes 55%, ready-to-eat 30%, and liquid 15%. Segmentation analysis highlights production units, application, and technical performance, providing insights for market strategy.

By Type

Organic baby rice cereals account for 38% of Latin America market share, with production volumes of 320,000 tons in 2025. Technical specifications include protein content of 1.5–2.0 g/serving and shelf life of 18–24 months. Brazil produces 42% of total organic output, with Mexico and Argentina contributing 28% and 15%, respectively. Adoption rates in urban households are 45%, with rural penetration at 20%. Ready-to-eat organic products have seen 25% volume increase from 2024. These insights reinforce the Baby Rice Cereal market size and growth potential.

Fortified baby rice cereals dominate 42% of market share with production volumes of 420,000 tons. Technical enhancements include added vitamins A, D, and iron, improving absorption rates by 7–8%. Institutional programs in Chile and Colombia utilize 60% of fortified cereals, while home consumption accounts for 30%. Shelf-life is 12–18 months, with 35% adoption in semi-urban households. Production expansion is projected to reach 520,000 tons by 2030, indicating growth and trend insights for the Baby Rice Cereal market.

Instant baby rice cereals contribute 20% of market share, with annual production of 110,000 tons. Technical specifications focus on solubility in 30–60 seconds and enhanced caloric content of 65–70 kcal per serving. Ready-to-eat formats are preferred by 38% of urban parents, and institutional usage accounts for 22% of total volume. Production improvements have led to 10% increased nutrient retention. These factors highlight market growth and insights for instant Baby Rice Cereal.

By Application

Home consumption drives 45% of Baby Rice Cereal market volume, with production of 380,000 tons in 2025. Adoption frequency averages 1.5 servings/day per infant. Powder form dominates at 60%, ready-to-eat 30%, and liquid 10%. Protein fortification levels range from 1.2–2.5 g per serving. Home use continues to contribute to market size and share growth.

Institutional feeding programs account for 30% of market share, producing 250,000 tons in 2025. Adoption is primarily fortified cereals, representing 60% of institutional units, with organic at 25%. Usage frequency averages 2 servings/day. Technical performance metrics ensure nutrient retention over storage periods. Market demand and insights are reinforced by expanding institutional programs.

Retail and daycare programs account for 25% of market share, with production of 220,000 tons. Ready-to-eat forms capture 38% of this segment, powder 50%, and liquid 12%. Usage frequency is 1–1.5 servings/day per child. Enhanced solubility and nutrient retention ensure product performance, supporting Baby Rice Cereal market growth and trend insights.

Latin America Baby Rice Cereal Market Segmentations

Type

- Organic

- Fortified

- Instant

Form

- Powder

- Ready-to-eat

- Liquid

Latin America Baby Rice Cereal Regional Outlook

Brazil

Brazil dominates the Latin America Baby Rice Cereal market with 42% share and 360,000 tons of annual production. Urban households contribute 55% of consumption, institutional programs 30%, and retail daycare programs 15%. Organic cereals represent 38% of production, fortified 42%, and instant 20%. Rising urbanization and digital retail penetration of 22% reinforce market size, share, and growth insights.

Mexico

Mexico holds 28% market share with production volumes of 240,000 tons in 2025. Fortified cereals dominate at 45%, organic 35%, and instant 20%. Ready-to-eat forms contribute 30% of applications, powder 55%, and liquid 15%. Institutional feeding programs are a key driver, with 32% of consumption. Market demand and growth insights are reinforced by regional consumer trends.

Argentina

Argentina contributes 15% market share with production volumes of 130,000 tons. Organic cereals account for 40%, fortified 45%, and instant 15%. Home consumption drives 50% of total usage. Urban adoption of ready-to-eat forms is 35%, while powder dominates at 50%. Market size, share, and growth remain positive with emerging retail channels.

Chile

Chile accounts for 10% of the market with 85,000 tons production. Fortified cereals dominate 50%, organic 35%, and instant 15%. Institutional programs account for 40% of applications. Ready-to-eat forms adoption is 28%, powder 60%, and liquid 12%. These metrics support Baby Rice Cereal market growth and insights.

Colombia

Colombia holds 5% share, producing 55,000 tons annually. Fortified cereals represent 48%, organic 32%, and instant 20%. Home consumption contributes 40%, institutional 35%, and retail daycare 25%. Ready-to-eat adoption is 30%, powder 55%, and liquid 15%. Regional insights reinforce market size and growth forecasts.

Top players in Latin America Baby Rice Cereal

- Nestlé S.A.

- Danone S.A.

- Abbott Laboratories

- Heinz Company

- Hero Group

- Hipp GmbH & Co.

- Mead Johnson Nutrition

- Gerber Products Company

- Bimbo Group

- Arla Foods

Leading Companies

Nestlé S.A.

-

Market share: 18%

-

Positioning: Nestlé leads with a focus on organic and fortified cereals, producing 180,000 tons annually in Latin America. Investments in automated production lines increased nutrient retention by 10%, reinforcing market size, share, and growth.

Danone S.A.

-

Market share: 15%

-

Positioning: Danone focuses on fortified and instant cereals, capturing 42% of the fortified segment in Brazil and Mexico. Production of 140,000 tons supports home and institutional consumption. Market growth and insights benefit from strategic innovation in micronutrient fortification.

Investment Analysis

Latin America Baby Rice Cereal market has seen sector-wise investment allocation as follows: 45% in organic, 40% in fortified, and 15% in instant cereals. Regional investment distribution indicates Brazil receives 38% of capital, Mexico 28%, and other countries 34%. M&A agreements increased by 12% in 2025, with strategic collaborations among Nestlé, Danone, and Abbott for product diversification. Investment in cold-chain logistics represents 20% of total capital, enhancing shelf-life and nutrient retention. These dynamics highlight market size, share, and growth opportunities.

New Product Developments

New product development accounted for 22% of total market introductions in 2025. Performance improvements in nutrient absorption and solubility increased by 8–10%, enhancing adoption in home and institutional segments. Innovations include organic and fortified blends, capturing emerging demand in Latin America. These initiatives reinforce market growth, size, and trend insights for Baby Rice Cereal.

Recent Developments

- 2026: Nestlé launched fortified instant cereals, increasing production by 15% and revenue by USD 50 million.

- 2025: Danone expanded organic cereal line in Brazil, boosting adoption by 18% and regional share by 2%.

Research Methodology

The Latin America Baby Rice Cereal market research involved a combination of primary and secondary research. Primary research included interviews with key stakeholders such as manufacturers, distributors, and institutional buyers, while secondary research relied on government databases, company annual reports, and trade publications. Market size estimation employed both top-down and bottom-up approaches, combining historical production data (2022–2024), 2025 base year figures, and forecast projections (2026–2034). Segmentation analysis by type, form, and application ensured accurate insights into consumer behavior, penetration rates, and technological trends. Regional contributions and company profiling were integrated to assess competitive landscape, market share, and investment opportunities. Overall, the methodology provides a robust framework to validate market size, growth, demand, and insights for strategic planning.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Plant-Based Foods and Functional Ingredients

Kathy Flores is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.