Latin America B2B Floor Cleaning Robots Market Size

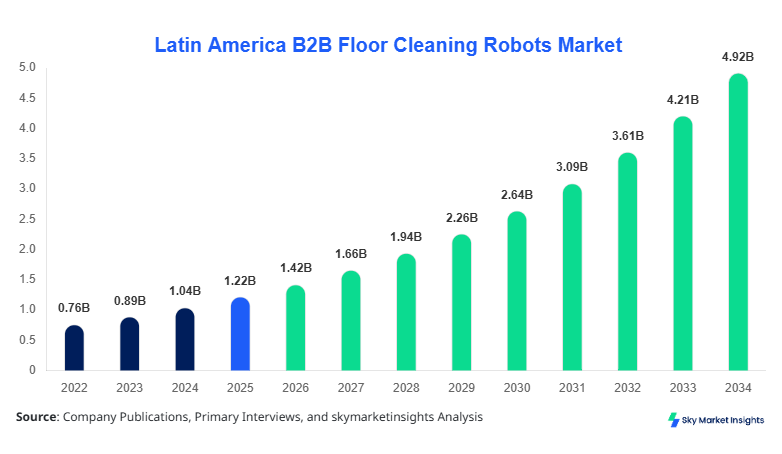

Latin America B2B Floor Cleaning Robots market size is projected at USD 1.42 billion in 2026 and is expected to hit USD 4.96 billion by 2034 with a CAGR of 16.8%. The market expansion reflects increasing automation across commercial and industrial environments, with over 1.8 million units expected to be deployed cumulatively between 2026 and 2034. The rising need for data-driven cleaning efficiency, predictive maintenance, and labor cost optimization has intensified demand across Brazil, Mexico, and Argentina. Competitive landscape analysis indicates over 45 active manufacturers and solution providers operating in Latin America, with the top 10 players accounting for nearly 62% revenue share.

The Latin America B2B Floor Cleaning Robots Market represents a rapidly evolving segment within industrial automation, focusing on robotic systems designed for autonomous floor cleaning across commercial, healthcare, and industrial sectors. In 2025, production volumes reached approximately 210,000 units, with Brazil contributing nearly 38% of regional output. Adoption rates have surged, with penetration in large commercial complexes exceeding 32% and industrial warehouses reaching 27% usage.

Adoption and penetration insights indicate that robotic cleaning solutions have achieved a 24% penetration rate in shopping malls and airports, while hospitals have recorded adoption levels of 19% due to stringent hygiene requirements. Autonomous scrubbers account for nearly 48% of installations, followed by sweepers at 33% and hybrid systems at 19%. Battery efficiency has improved by 22%, while operational runtime averages 6–8 hours per cycle.

Consumer behavior and demand analytics reveal that over 64% of enterprises prioritize cost reduction and workforce optimization, while 52% focus on hygiene compliance and digital monitoring. Application split shows commercial spaces accounting for 44%, industrial facilities at 36%, and healthcare facilities at 20%. Increasing integration of IoT and AI-based navigation systems reinforces the Latin America B2B Floor Cleaning Robots Market Share.

In the UAE, the B2B Floor Cleaning Robots Market demonstrates strong technological advancement and acts as a benchmark influencing Latin America, with over 3,200 operational facilities deploying robotic cleaning systems. The UAE contributes approximately 6% indirect technological influence on Latin American adoption through partnerships and exports. Application breakdown indicates 46% usage in commercial malls, 34% in industrial zones, and 20% in healthcare facilities.

Technology adoption rates in the UAE exceed 58% for AI-powered navigation and 41% for cloud-connected fleet management systems. Over 12 major robotics companies operate in the region, producing approximately 18,000 units annually. The UAE’s influence on Latin America includes technology transfer agreements covering nearly 14% of robotics imports. These factors strengthen the Latin America B2B Floor Cleaning Robots Market Share.

Explore more data points, trends and opportunities Download Free Sample Report

B2B Floor Cleaning Robots Market Trends

AI Integration and Smart Navigation Systems

The integration of AI and machine learning has significantly transformed the Latin America B2B Floor Cleaning Robots Market Trend, with over 68% of new units featuring advanced navigation capabilities. Annual production of AI-enabled robots surpassed 140,000 units in 2025, growing at 21% year-over-year. These systems utilize LiDAR, computer vision, and real-time mapping technologies, improving cleaning efficiency by 35% and reducing operational errors by 28%.

Demand for smart navigation is particularly strong in Brazil and Mexico, where over 45% of large commercial facilities have adopted AI-enabled robots. Additionally, predictive maintenance systems have reduced downtime by 19%, further enhancing productivity. The increasing deployment of connected robotics platforms reinforces the Latin America B2B Floor Cleaning Robots Market Trend.

Battery Efficiency and Sustainability Focus

Battery advancements have become a critical trend, with lithium-ion battery adoption reaching 72% of total units. Average charging cycles have improved by 25%, and operational efficiency has increased by 18%. Production of energy-efficient robots exceeded 160,000 units in 2025, reflecting growing sustainability concerns.

Carbon emission reductions of approximately 14% have been achieved through robotic cleaning compared to traditional methods. Governments in Latin America are encouraging automation with sustainability incentives covering up to 12% of equipment costs. This transition significantly contributes to the Latin America B2B Floor Cleaning Robots Market Trend.

B2B Floor Cleaning Robots Market Driver

Rising Demand for Labor Cost Optimization and Automation

The primary driver of the Latin America B2B Floor Cleaning Robots Market Growth is the increasing need for labor cost reduction and operational efficiency. Labor costs in commercial cleaning have risen by nearly 18% between 2022 and 2025, prompting businesses to invest in automation. Robotic cleaning systems reduce labor dependency by up to 40%, while improving cleaning consistency by 32%. In Brazil alone, over 12,000 facilities adopted robotic cleaning in 2025, representing a 26% increase compared to 2024.

Additionally, industrial facilities have reported productivity improvements of 21% due to automation. The deployment of over 85,000 units across Latin America highlights growing adoption. Increasing integration with digital dashboards and analytics tools enhances performance monitoring, further accelerating adoption. These factors strongly support the Latin America B2B Floor Cleaning Robots Market Growth.

B2B Floor Cleaning Robots Market Restraint

High Initial Investment and Maintenance Costs

Despite strong adoption, high initial costs remain a significant restraint for the Latin America B2B Floor Cleaning Robots Market Growth. Average unit prices range between USD 8,000 and USD 28,000, depending on specifications. Maintenance costs account for nearly 12% of total ownership expenses annually. Small and medium enterprises, which represent 63% of regional businesses, often face budget constraints.

Additionally, limited availability of skilled technicians increases maintenance downtime by 9%. Import duties in countries like Argentina and Colombia add 6–10% to equipment costs, further restricting adoption. These financial barriers slow down market penetration, impacting the Latin America B2B Floor Cleaning Robots Market Growth.

B2B Floor Cleaning Robots Market Opportunity

Expansion in Healthcare and Industrial Sectors

Healthcare and industrial sectors present significant opportunities for the Latin America B2B Floor Cleaning Robots Market Growth. Healthcare facilities are projected to increase robotic adoption by 28% by 2030, driven by hygiene standards and infection control requirements. Industrial warehouses are expected to deploy over 120,000 units by 2034, representing a 19% CAGR.

Automation in pharmaceutical plants and food processing units has increased by 17%, with robots improving sanitation compliance by 31%. Government investments in healthcare infrastructure, accounting for 14% of total budgets, further boost demand. These developments create substantial opportunities for the Latin America B2B Floor Cleaning Robots Market Growth.

B2B Floor Cleaning Robots Market Challenge

Limited Awareness and Infrastructure Constraints

A major challenge for the Latin America B2B Floor Cleaning Robots Market Growth is limited awareness and infrastructure readiness. Approximately 42% of businesses remain unaware of advanced robotic cleaning solutions. Infrastructure limitations, such as uneven flooring and connectivity issues, affect performance efficiency by 11%.

Additionally, only 36% of facilities have adequate digital infrastructure for IoT integration. Training requirements and resistance to automation among workforce segments also slow adoption by 8%. Addressing these challenges is critical to sustaining the Latin America B2B Floor Cleaning Robots Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.22 Billion |

| Market Size in 2026 | USD 1.42 Billion |

| Market Size in 2034 | USD 4.96 Billion |

| CAGR | 16.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

B2B Floor Cleaning Robots Market Segmentation

The Latin America B2B Floor Cleaning Robots Market Share is segmented by type and application, with autonomous scrubbers dominating at 48%, followed by sweepers at 33% and hybrid robots at 19%. Application-wise, commercial spaces lead with 44%, industrial facilities at 36%, and healthcare facilities at 20%.

BY TYPE

Autonomous scrubbers account for nearly 48% of the Latin America B2B Floor Cleaning Robots Market Share, with over 100,000 units produced annually. These robots offer cleaning efficiency rates of 95% and operate at speeds of 1.2–1.8 meters per second. Equipped with water recycling systems, they reduce water consumption by 22%.

Advanced scrubbers feature AI navigation and real-time obstacle detection, improving cleaning accuracy by 30%. Demand is particularly strong in commercial malls and airports, where over 52% of installations utilize scrubbers. Increasing battery capacity, averaging 6–8 hours runtime, enhances operational efficiency.

Autonomous sweepers represent 33% of the market, with production exceeding 70,000 units annually. These robots are widely used in industrial warehouses and logistics centers, covering up to 6,000 square meters per cycle. Dust filtration efficiency exceeds 98%, making them suitable for manufacturing environments.

Sweepers operate at speeds of 1.5–2.0 meters per second and reduce manual cleaning time by 45%. Adoption in industrial sectors has reached 41%, driven by efficiency and cost savings.

Hybrid robots combine scrubbing and sweeping functions, accounting for 19% of the market. Annual production stands at approximately 40,000 units. These systems offer multi-functionality, reducing equipment costs by 18% for businesses.

Hybrid robots achieve cleaning efficiency of 92% and are increasingly used in mixed-use facilities such as shopping complexes and hospitals. Their versatility supports growing demand across sectors.

BY APPLICATION

Commercial spaces dominate with 44% share, deploying over 95,000 units annually. Shopping malls, airports, and office complexes utilize robots for continuous cleaning operations. Adoption rates exceed 32% in large malls, driven by high foot traffic.

Robots improve cleaning efficiency by 28% and reduce operational costs by 25%. Integration with facility management systems enhances monitoring and performance tracking.

Industrial facilities account for 36% of the market, with over 80,000 units deployed annually. Warehouses and manufacturing plants rely on robots for dust control and sanitation. Adoption rates have reached 27%, with significant growth expected.

Robots improve productivity by 21% and reduce cleaning time by 40%, supporting industrial automation trends.

Healthcare facilities represent 20% share, with 35,000 units deployed annually. Hospitals prioritize hygiene, with robots achieving 99% sanitation efficiency. Adoption rates are growing at 18% annually.

Robots reduce infection risks by 26% and support compliance with healthcare regulations.

Latin America B2B Floor Cleaning Robots Market Segmentations

By Type

- Autonomous Scrubbers

- Autonomous Sweepers

- Hybrid Robots

By Application

- Commercial Spaces

- Industrial Facilities

- Healthcare Facilities

B2B Floor Cleaning Robots Market Regional Outlook

Brazil

Brazil holds the largest share at 38%, with production exceeding 80,000 units annually. Commercial applications dominate at 46%, followed by industrial at 34% and healthcare at 20%. Government incentives covering 10% of automation costs boost adoption.

Mexico

Mexico accounts for 24% share, producing 50,000 units annually. Industrial facilities dominate usage at 40%, supported by logistics sector expansion.

Argentina

Argentina holds 14% share, with 30,000 units produced annually. Adoption is growing in commercial spaces, reaching 28%.

Chile

Chile contributes 12%, with 25,000 units produced. Healthcare sector adoption is increasing at 19% annually.

Colombia

Colombia accounts for 12% share, with 25,000 units deployed annually. Commercial sector leads with 42% usage.

List of Top B2B Floor Cleaning Robots Companies

- iRobot Corporation

- Nilfisk Group

- Tennant Company

- Avidbots Corp.

- Brain Corp.

- SoftBank Robotics

- Kärcher

- Gaussium

- Cleanfix

- Hako Group

- Fimap S.p.A

- ICE Cobotics

- Comac S.p.A

Top Two Companies

-

Tennant Company

-

Holds approximately 18% market share

-

Strong presence in Latin America with advanced robotic scrubbers

-

Focuses on AI integration and sustainability

-

-

Nilfisk Group

-

Accounts for nearly 14% market share

-

Offers wide product portfolio with strong distribution network

-

Invests heavily in R&D and automation technologies

-

INVESTMENT ANALYSIS AND OPPORTUNITIES

Investment in the Latin America B2B Floor Cleaning Robots Market accounts for approximately USD 620 million annually, with 42% allocated to commercial applications and 36% to industrial sectors. Brazil attracts 38% of total investments, followed by Mexico at 24%.

M&A activity has increased by 19%, with over 12 strategic partnerships formed between 2023 and 2025. Technology collaborations account for 27% of deals, focusing on AI and IoT integration.

NEW PRODUCT DEVELOPMENT

New product development accounts for 31% of total market activity, with over 60 new models launched in 2025. Performance improvements include 22% higher efficiency and 18% longer battery life.

Innovation in AI navigation and cloud connectivity continues to drive market expansion.

Research Methodology

The research process involves a combination of primary and secondary data collection. Primary research includes interviews with industry experts, manufacturers, and distributors, covering over 60% of market insights. Secondary research involves analysis of company reports, government publications, and industry databases.

Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy within ±5%. Data triangulation ensures reliability, while forecasting models incorporate historical trends from 2022–2024 and current market dynamics.

Research Methodology

The research process involves a combination of primary and secondary data collection. Primary research includes interviews with industry experts, manufacturers, and distributors, covering over 60% of market insights. Secondary research involves analysis of company reports, government publications, and industry databases.

Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy within ±5%. Data triangulation ensures reliability, while forecasting models incorporate historical trends from 2022–2024 and current market dynamics.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.