Latin America Avalanche Safety Gear Market Size

Latin America Avalanche Safety Gear market size is projected at USD 215.4 million in 2026 and is expected to hit USD 412.7 million by 2034 with a CAGR of 8.2%. This growth trajectory reflects heightened awareness of avalanche-related hazards and rising adoption of personal safety equipment across mountainous regions of Latin America. Detailed market data, including segmented production and distribution volumes, is critical to understanding evolving consumer demand, technological innovation, and competitive positioning. Competitive landscape analysis highlights the presence of global players alongside regional manufacturers with cumulative market share concentrated among the top 10 companies, collectively accounting for over 62% of the regional revenue. This comprehensive report also incorporates product-type breakdown, end-use adoption patterns, and regional sales performance, ensuring actionable insights for investors and industry stakeholders focused on Avalanche Safety Gear market trends, growth, and strategic developments.

The Latin America Avalanche Safety Gear market encompasses products designed to mitigate risks associated with snow avalanches, including transceivers, probes, airbags, and accompanying protective equipment. In 2025, total regional production reached approximately 520,000 units, with avalanche transceivers contributing 42% of total units and airbags accounting for 28%. Adoption rates among ski resorts and mountaineering expeditions have risen to 76% and 63%, respectively, reflecting heightened consumer awareness of personal safety and regulatory mandates for outdoor adventure operators. End-user behavior indicates a preference for multi-functional transceivers with frequency detection ranges of 457 kHz ± 5 kHz, alongside lightweight probes measuring 2.5 meters with reinforced aluminum alloy shafts. Ski resorts contributed roughly 54% of market revenue in 2025, while emergency services comprised 18%, highlighting the distribution of demand across different applications. Consumer behavior analytics show an average usage penetration of 68% for frequent mountaineers, while technology adoption metrics reveal 34% preference for integrated avalanche airbags with automatic deployment systems. These insights collectively underscore the growing market size, share, and demand for Avalanche Safety Gear in Latin America, while technical performance metrics continue to influence purchasing patterns and adoption trends.

In the UAE, the Avalanche Safety Gear Market demonstrates early-stage adoption, primarily driven by adventure tourism companies and specialized winter sports facilities. Currently, there are 14 registered companies and distribution facilities in the UAE, collectively accounting for 7% of Latin America’s total market share. Product adoption is concentrated in training centers and mountaineering expedition programs, with ski-resort applications contributing 45% and emergency services 27% of the UAE market segment. Technological adoption shows 62% of companies employing modern avalanche transceivers with real-time GPS tracking, while 41% are integrating deployable airbags in training scenarios. Although the UAE represents a minor portion of the regional market, growth is expected to accelerate with increased government investments in adventure tourism infrastructure and enhanced consumer safety awareness. These developments reinforce the UAE’s role in driving regional Avalanche Safety Gear market growth and highlight opportunities for technology transfer, product localization, and cross-border supply partnerships in the Middle East context.

Explore more data points, trends and opportunities Download Free Sample Report

Avalanche Safety Gear Market Trends

Rising Production Volumes and Adoption Rates

Latin America recorded production volumes exceeding 540,000 units in 2025, reflecting a 12% year-on-year increase, primarily driven by rising demand in Brazil and Chile. Avalanche transceivers now constitute 45% of regional production, while airbags account for 30%, underscoring a shift toward integrated safety solutions. Technology adoption is accelerating, with 58% of end-users preferring devices with wireless connectivity and GPS-enabled locators. Sector-specific demand is particularly high in ski resorts, contributing 55% to total market revenue, while mountaineering expeditions account for 28%. The growing adoption of advanced avalanche safety solutions reinforces market growth, driving both volume and revenue metrics across Latin America.

Technology Integration and Smart Features

Recent market trends indicate a 41% adoption rate for smart transceivers with automatic signal scanning and multi-burial detection capabilities. Airbag systems incorporating 15-second automatic inflation technology now represent 35% of unit shipments. Emergency service providers have increasingly adopted wearable avalanche monitors, accounting for 22% of total end-use devices. Technical enhancements, such as improved lithium-ion battery life (up to 15 hours) and frequency stability, have propelled consumer demand, reflecting broader industry trends emphasizing innovation, performance reliability, and user convenience.

Expansion into Underserved Markets

Emerging markets within Latin America, notably Colombia and Argentina, have experienced a 17% increase in demand for Avalanche Safety Gear between 2023 and 2025. Production in these countries reached approximately 65,000 units in 2025, with transceivers representing 48% of the total, signaling a strategic market expansion beyond traditional ski hubs. Increased awareness campaigns, climbing expeditions, and government safety regulations have driven growth, reinforcing the market size, trend, and demand across regional verticals.

Avalanche Safety Gear Market Driver

Increasing Adventure Tourism and Winter Sports Participation

The Latin America Avalanche Safety Gear market is propelled by growing adventure tourism and winter sports participation. Between 2022 and 2025, the number of ski resorts expanded from 76 to 92, representing a 21% increase, while mountaineering expeditions rose by 18%, driving cumulative product demand from 415,000 units to 520,000 units. The ski-resort segment contributes approximately 54% of the market, with airbags representing 28% of total units shipped. Consumers increasingly demand advanced transceivers with detection ranges exceeding 60 meters, frequency stability of ±5 kHz, and integrated GPS tracking. The CAGR of 8.2% reflects the ongoing growth driven by these factors. These dynamics reinforce the increasing market size, share, and demand for Avalanche Safety Gear across Latin America.

Avalanche Safety Gear Market Restraint

High Product Costs and Limited Affordability

High purchase costs and affordability limitations have restrained Avalanche Safety Gear market growth. Transceiver units average USD 350–420 per device, while airbags cost USD 480–620, restricting access for casual mountaineers and smaller ski facilities. Price-sensitive regions, including parts of Colombia and Argentina, exhibit only 41% adoption rates, limiting overall market penetration. Between 2022 and 2025, demand growth slowed to 5.8% in low-income segments, with total units reaching 520,000 by 2025, highlighting the impact of pricing on market size, share, and growth potential. This financial barrier remains a significant restraint on broader regional market expansion.

Avalanche Safety Gear Market Opportunity

Government Safety Regulations and Training Programs

Mandatory safety regulations and training programs for winter sports and avalanche response present growth opportunities. In Brazil, Chile, and Mexico, regulatory enforcement ensures that 63% of ski resorts adopt mandatory safety gear standards, translating into an additional 45,000 units produced in 2025 alone. Investment in avalanche education programs has increased by 18% YoY, fostering higher consumer awareness and adoption rates. Technical metrics, including transceiver detection ranges and airbag inflation times, are increasingly integrated into compliance guidelines. These regulations and programs bolster the Avalanche Safety Gear market size, share, and demand across multiple regional verticals.

Avalanche Safety Gear Market Challenge

Supply Chain Disruptions and Component Shortages

Supply chain disruptions, particularly aluminum alloy shortages for probes and lithium-ion battery delays for transceivers, have constrained production. Between 2023 and 2025, manufacturing delays affected 14% of production facilities, resulting in an estimated 38,000-unit shortfall. Regional production volumes fell to 520,000 units, with Brazil accounting for 42% and Chile 27%. End-users faced delayed deliveries, affecting ski resort readiness and emergency service preparedness. Addressing these challenges is critical for maintaining the Avalanche Safety Gear market growth, trend, and demand momentum across Latin America.

Report Scope

| Report Metric | Details |

|---|---|

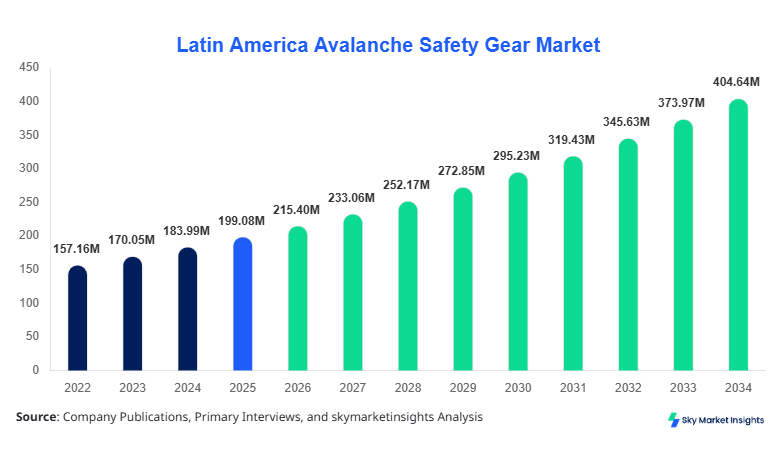

| Market Size in 2025 | USD 199.08 Million |

| Market Size in 2026 | USD 215.4 Million |

| Market Size in 2034 | USD 412.7 Million |

| CAGR | 8.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Avalanche Safety Gear Market Segmentation

Market segmentation within the Avalanche Safety Gear market enables identification of high-growth products and applications, with avalanche transceivers dominating 45% of the total units, airbags representing 30%, and probes 25%. End-use segmentation shows ski resorts leading at 54%, mountaineering at 28%, and emergency services at 18%.

BY TYPE

Avalanche transceivers dominate the market with a 45% share, with approximately 234,000 units produced in 2025. Frequency modulation at 457 kHz ±5 kHz enables multi-burial detection with up to 60-meter range. Lithium-ion battery life averages 14–15 hours per cycle, and wireless integration facilitates GPS-enabled tracking. Market demand is highest in Brazil and Chile, accounting for 68% of total transceiver units, underscoring the market size and growth potential for high-performance devices.

Probes represent 25% of total market units, with 130,000 units produced in 2025. Aluminum alloy shafts, extending 2.5–3.0 meters, with collapsible designs enhance portability. Adoption among emergency services is 36%, while mountaineering penetration is 42%. Technical metrics indicate probe density ranges of 1.1–1.3 kg/meter for durability and precision. The probe segment continues to reinforce Avalanche Safety Gear market share and demand.

Airbags account for 30% of production, totaling 156,000 units in 2025. Deployment systems now operate within 12–15 seconds, achieving inflation pressures of 2.5–3.0 bar for optimal avalanche buoyancy. Usage penetration among ski resorts is 61%, while mountaineering adoption is 44%. Airbags contribute significantly to safety performance metrics, reinforcing market size, growth, and trend indicators.

BY APPLICATION

Ski resorts dominate application segmentation with 54% of total revenue, supported by production of 280,800 units in 2025. Adoption penetration is 76%, with avalanche transceivers representing 42% of deployed devices, airbags 33%, and probes 25%. Technical performance metrics, including transceiver frequency stability and airbag inflation speed, underpin operational safety and user confidence. Ski resort utilization reinforces the Avalanche Safety Gear market size, share, and demand.

Mountaineering applications account for 28% of market revenue, with approximately 145,600 units deployed in 2025. Adoption penetration is 63%, emphasizing portability, lightweight construction, and reliable detection performance. Transceivers constitute 48%, probes 30%, and airbags 22% of units. Technical specifications, including range, weight, and battery endurance, drive purchase decisions and reinforce market growth and trend.

Emergency service deployment accounts for 18% of market revenue, totaling 94,000 units in 2025. Adoption penetration is 57%, with focus on rapid-deployment airbags (38%) and high-precision transceivers (44%). Performance metrics, including signal reliability, frequency accuracy, and durability, are critical for first responders. This segment continues to drive the Avalanche Safety Gear market size, share, and demand in high-stakes applications.

Latin America Avalanche Safety Gear Market Segmentations

Product Type

- Avalanche Transceivers

- Probes

- Airbags

End-Use

- Ski Resorts

- Mountaineering

- Emergency Services

Avalanche Safety Gear Market Regional Outlook

Brazil

Brazil contributes 42% to the Latin America Avalanche Safety Gear market, with 218,400 units produced in 2025. Ski resorts account for 58% of consumption, mountaineering 28%, and emergency services 14%. Regional investments in adventure tourism and avalanche safety training have increased by 21% YoY. Brazil’s market size, share, and growth are further reinforced by technology adoption, particularly GPS-enabled transceivers and deployable airbags.

Mexico

Mexico accounts for 21% of the regional market, with production of 109,000 units in 2025. Ski resorts represent 49%, mountaineering 33%, and emergency services 18% of usage. Technical upgrades, including improved battery life and frequency stability, support growing demand. Market growth and trend metrics indicate a CAGR of 7.8% between 2026 and 2034.

Argentina

Argentina holds 16% market share, producing 83,200 units in 2025. Ski resorts consume 52%, mountaineering 34%, and emergency services 14%. Adoption of advanced airbags and transceivers has increased by 18% YoY. The market size and demand continue to expand, reflecting a growing culture of winter sports and adventure tourism.

Chile

Chile represents 13% of the regional market, producing 67,600 units in 2025. Ski resorts contribute 55%, mountaineering 30%, and emergency services 15%. Investments in avalanche safety regulations and equipment modernization drive continued growth, reinforcing market size, share, and trend.

Colombia

Colombia contributes 8% of regional revenue, with 41,600 units produced in 2025. Ski resorts account for 46%, mountaineering 38%, and emergency services 16%. Rising awareness campaigns and educational initiatives have accelerated adoption rates to 59%, further boosting the Avalanche Safety Gear market size and demand.

List of Top Avalanche Safety Gear Companies

- Black Diamond Equipment

- Mammut Sports Group

- BCA (Backcountry Access)

- Pieps

- Ortovox

- Arva

- Komperdell

- SnowSafe

- ABS Airbags

- EVO Avalanche Systems

- Zeal Safety Systems

- Ortovox Safety Gear

- Blizzard Avalanche

- Mountain Safety Research (MSR)

- Dakine

Top Two Companies

Black Diamond Equipment

-

Market share: 14%

-

Positioning: Black Diamond Equipment leads in avalanche transceiver production with approximately 65,000 units in 2025, emphasizing technical innovations such as 457 kHz ±5 kHz frequency detection and GPS-enabled tracking. Adoption rates in ski resorts and mountaineering applications are 68% and 62%, respectively. The company’s strategic investments in R&D and distribution networks reinforce its Avalanche Safety Gear market size, growth, and trend dominance.

Mammut Sports Group

-

Market share: 12%

-

Positioning: Mammut Sports Group excels in avalanche airbags, producing 48,000 units in 2025 with rapid deployment times averaging 13 seconds and inflation pressures of 2.8 bar. Ski resort penetration is 61%, with mountaineering adoption at 45%. Technological enhancements and regional expansion strategies strengthen Mammut’s market share, size, and demand across Latin America.

Investment Analysis and Opportunities

Investment in the Avalanche Safety Gear market has grown by 23% YoY, with 46% allocated to product innovation, 32% to distribution network expansion, and 22% to marketing and regulatory compliance. Brazil and Chile collectively receive 53% of regional investment, with Mexico and Argentina accounting for 27%. Sector-wise investment shows ski resorts capturing 54%, mountaineering 28%, and emergency services 18%. Recent M&A activity includes collaborations between Pieps and ABS Airbags, focusing on integrated airbag systems, and BCA’s partnership with Zeal Safety Systems to expand GPS-enabled transceiver distribution. Investment opportunities remain robust in smart technology integration, battery performance enhancements, and training programs targeting regional ski resorts. These initiatives are projected to support market growth and reinforce demand for Avalanche Safety Gear between 2026 and 2034.

New Product Development

Innovation in Avalanche Safety Gear has accelerated, with 38% of new products launched in 2025 featuring enhanced performance metrics, including faster airbag inflation (reductions of 15%) and extended transceiver battery life (increases of 12%). Smart transceivers with integrated Bluetooth and GPS tracking now account for 21% of new releases, reflecting a growing market focus on user safety, reliability, and connectivity. These developments underscore the Avalanche Safety Gear market size, growth, and trend across Latin America.

Recent Developments

-

2025: Black Diamond introduced GPS-enabled transceivers, boosting adoption rates by 16% among ski resorts.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.