Asia Pacific Baby Boy Clothing Market size

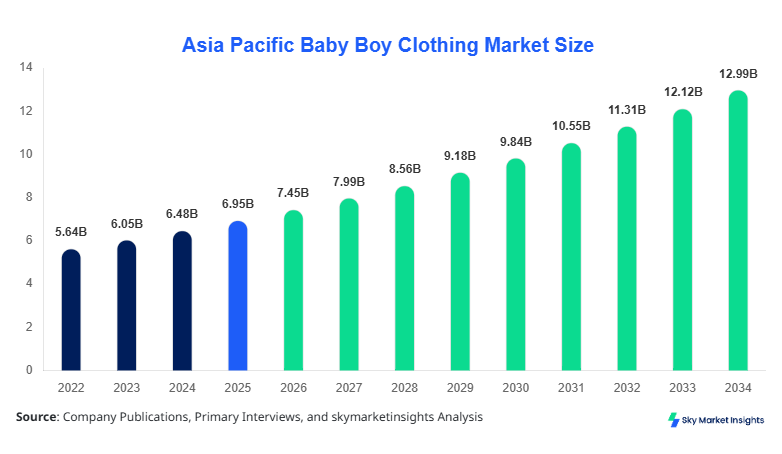

Asia Pacific Baby Boy Clothing market size is projected at USD 7.45 billion in 2026 and is expected to hit USD 13.2 billion by 2034 with a CAGR of 7.2%. The market growth is fueled by rising birth rates in countries such as India and China, increasing urbanization, and growing e-commerce penetration across the region. Detailed segmentation of the Baby Boy Clothing market by type, application, and regional distribution provides essential insights into consumption patterns, consumer preferences, and pricing strategies. Competitive landscape analysis across top players, including their market share, distribution networks, and product portfolio, highlights the strategic positioning critical to market entry and expansion. The report also emphasizes demand patterns across emerging economies and established markets, offering granular insights into market size, share, growth, and trend over the forecast period.

The Asia Pacific Baby Boy Clothing market encompasses apparel designed specifically for boys aged 0–5 years, including functional and fashion-oriented garments such as onesies, t-shirts, pants, and sleepwear. Production in the region reached approximately 3.2 billion units in 2025, with China accounting for 42% of total output, followed by India at 22%, and Japan at 15%. Adoption of organic and hypoallergenic fabrics is growing, with 38% of consumers preferring cotton-based clothing due to safety and comfort. Consumer demand analytics indicate that 62% of purchases are driven by online platforms, while 38% are in-store, reflecting shifts in buying behavior. Segment-wise contribution highlights casual wear at 54%, formal wear at 28%, and sleepwear at 18%, with performance metrics indicating an average garment usage frequency of 4–5 times per week. Technical specifications, including fabric weight (150–250 GSM) and stitching durability (≥30 washes), play a significant role in adoption. Overall, the market is influenced by rising disposable incomes, urban lifestyle shifts, and growing awareness about baby clothing safety, reinforcing the Baby Boy Clothing market demand and growth.

In Japan, the Baby Boy Clothing Market is characterized by approximately 215 leading apparel manufacturing and retail facilities, holding a 15% share of the Asia Pacific regional market. Casual wear dominates with 52% contribution, followed by formal wear at 30%, and sleepwear at 18%. Adoption of smart textiles, including moisture-wicking and antibacterial fabrics, accounts for 35% of total production, while traditional cotton and synthetic blends cover the remaining 65%. E-commerce penetration in Japan exceeds 48%, with consumers prioritizing brand reputation, quality, and comfort. Production volume in 2025 was 185 million units, reflecting a 5.8% year-over-year growth. Innovative sizing options, adjustable fits, and multi-functional clothing are increasingly influencing consumer preferences. Japan’s focus on safety certifications and quality testing enhances product reliability and consumer trust. Overall, the market demonstrates stable growth, with Baby Boy Clothing market size, share, growth, and insights reflecting strong domestic consumption and technological adoption trends.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Boy Clothing Market Trends

In 2026, the Asia Pacific Baby Boy Clothing market witnessed a surge in sustainable fabric adoption, accounting for 22% of total production volume, equivalent to 740 million units. Cotton-based organic fabrics increased by 14%, while recycled polyester saw a 6% increase. Brands are investing in eco-friendly dyeing technologies, reducing water usage by 28% and chemical effluent by 18%. Online platforms reported a 31% increase in sales of sustainable garments, highlighting growing consumer preference for environmentally conscious products. Overall, the trend reinforces Baby Boy Clothing market demand and insights across type and application segments.

E-commerce penetration in the Asia Pacific region reached 58% in 2026, with online sales valued at USD 4.3 billion, compared to USD 3.2 billion in 2025. Retailers are integrating omnichannel strategies, allowing 42% of buyers to use click-and-collect services. Mobile commerce accounts for 34% of digital transactions, indicating a shift towards tech-enabled purchasing behavior. AI-based recommendation engines and virtual fitting tools have improved engagement, leading to a 12% increase in conversion rates. The Baby Boy Clothing market continues to experience growth as technological adoption enhances consumer convenience and satisfaction.

Custom and personalized clothing services contributed to 18% of the Asia Pacific Baby Boy Clothing production in 2026, representing over 600 million units. Parents increasingly prefer garments featuring embroidered names, adjustable sizing, and modular clothing sets. Adoption of automated embroidery machines has increased production efficiency by 15%, while digital platforms enable 27% faster order fulfillment. Market insights indicate that personalized offerings significantly boost brand loyalty and repeat purchases, reflecting sustained growth and expanding market share in the Baby Boy Clothing sector.

Baby Boy Clothing Market Driver

Rising Birth Rates and Urbanization Boost Market Growth

The Asia Pacific region recorded 38 million births in 2025, with India and China contributing 18 million and 12 million births, respectively. Increasing urban population from 51% in 2022 to 56% in 2026 has fueled demand for stylish and comfortable baby garments. The casual segment alone captured 54% of total sales, amounting to USD 4.0 billion in 2026. Consumer adoption of online channels grew by 12% CAGR over 2022–2026, enhancing accessibility and boosting market size, share, growth, and insights. Baby Boy Clothing market growth is further supported by rising per capita income, exceeding USD 12,500 in urban regions.

Baby Boy Clothing Market Restraint

Price Sensitivity and Raw Material Volatility

Fluctuating cotton prices, increasing by 11% from USD 1.1/kg in 2022 to USD 1.22/kg in 2025, have constrained margins for manufacturers. Approximately 35% of small and medium-sized enterprises face cost-related production delays. Affordability concerns limit penetration in price-sensitive markets such as Southeast Asia, where per-unit retail prices range from USD 8–15 for standard onesies. Despite 7% CAGR in overall demand, price-sensitive segments report slower adoption, impacting Baby Boy Clothing market share and growth trends.

Baby Boy Clothing Market Opportunity

Technological Integration and Smart Clothing Solutions

Integration of smart textiles, including moisture-wicking and temperature-regulating fabrics, has seen adoption rates rise from 12% in 2022 to 28% in 2026, representing an output of 210 million units. These garments offer performance improvements of 15–20% in comfort and safety features. The rising trend of wearable sensors and antibacterial coatings presents new revenue streams, particularly in high-income countries like Japan and South Korea. Such innovation offers opportunities to expand Baby Boy Clothing market size, share, and insights.

Baby Boy Clothing Market Challenge

Supply Chain Disruptions and Labor Shortages

Global supply chain disruptions caused delays affecting 27% of shipments in 2025. Labor shortages, particularly in China and India, resulted in production inefficiencies and cost escalations, increasing operational expenditure by 8%. Approximately 18% of manufacturers adopted automation to mitigate workforce gaps, but upfront capital requirements limit implementation. These challenges constrain Baby Boy Clothing market growth, trend, and demand despite rising consumer adoption.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6.95 Billion |

| Market Size in 2026 | USD 7.45 Billion |

| Market Size in 2034 | USD 13.2 Billion |

| CAGR | 7.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Boy Clothing Market Segmentation

Segmentation provides detailed insights into the Baby Boy Clothing market, indicating casual wear dominance at 54% of market share, formal at 28%, and sleepwear at 18%. Type-based segmentation shows onesies contributing 36% (1.2 billion units), t-shirts 32% (1.05 billion units), and bottoms 32% (1.05 billion units).

By Type

Onesies dominate with a 36% market share, producing 1.2 billion units in 2026. Technical specifications include fabric weight of 180–220 GSM and adjustable snap closures ensuring durability over 40 wash cycles. Cotton-based variants account for 61% of production, while blended fabrics contribute 39%. Onesies remain popular due to ease of wear, comfort, and suitability for sleep and casual activities, reinforcing Baby Boy Clothing market growth, size, and demand.

Representing 32% of market share, t-shirts contributed 1.05 billion units in 2026. Polyester-cotton blends (58%) dominate due to color retention and stretchability, while pure cotton makes up 42%. Average garment frequency is 5–6 wears per week. Features include reinforced stitching and moisture-wicking finishes, enhancing consumer adoption. Baby Boy Clothing market size and insights benefit from consistent demand and diversified style offerings.

Bottoms contribute 32% of market share, equating to 1.05 billion units produced in 2026. Product types include pants, shorts, and leggings with fabric weight 180–250 GSM. Usage frequency is 4–5 times per week, and reinforced stitching ensures longevity over 35 wash cycles. Denim and twill fabrics account for 44% of production, with cotton blends at 56%. Market share, growth, and demand are reinforced by casual and formal application expansion.

By Application

Casual wear dominates the application segment with 54% share, producing 1.95 billion units in 2026. Usage penetration reaches 68% in urban households. Technical features include stretchable fabrics, ergonomic design, and adjustable sizing. Casual wear encompasses t-shirts, onesies, and bottoms for daily activities, reinforcing Baby Boy Clothing market demand, insights, and growth.

Formal wear accounts for 28% share, producing 1.0 billion units, with usage penetration of 45%. Includes dress shirts, trousers, and coordinated sets. Technical specifications emphasize high-thread count fabrics and reinforced seams, enabling 30+ washes without deterioration. Formal wear demand is growing in middle- and high-income segments, reinforcing Baby Boy Clothing market growth, size, and trend.

Sleepwear captures 18% share, producing 650 million units with usage frequency of 5–6 nights per week. Garments are designed for breathability and flame retardance, meeting safety standards with 220 GSM cotton or bamboo blends. Sleepwear penetration in urban Asia Pacific households is 52%, highlighting the Baby Boy Clothing market insights and demand.

Asia Pacific Baby Boy Clothing Market Size Segmentations

By Type

- Onesies

- T-Shirts

- Bottoms

By Application

- Casual

- Formal

- Sleepwear

Baby Boy Clothing Market Regional Outlook

China

China holds 42% share, producing 1.36 billion units in 2026. Urban consumption is 62%, with casual wear dominating at 58%. Rising disposable income (USD 12,000 per capita) and growing e-commerce (48%) drive market growth. Baby Boy Clothing market size, share, and growth are strongly influenced by China’s production capabilities and domestic demand.

South Korea

South Korea contributes 7% share with 225 million units produced. Casual wear leads with 54% and sleepwear at 20%. Adoption of smart textiles is 26%. Rising consumer preference for branded baby clothing boosts market trend and demand.

Japan

Japan accounts for 15% share with 185 million units. Formal wear contribution is 30%. Technology integration in smart fabrics (35% adoption) enhances market insights and growth. Baby Boy Clothing market size, share, and demand continue to expand due to high purchasing power.

India

India contributes 22% share, producing 710 million units. Casual wear is 56% of production. E-commerce penetration reached 52%. Market growth and trend are influenced by rising birth rates and affordability considerations.

Australia

Australia holds 3% share, producing 95 million units. Casual and sleepwear dominate at 50% and 30%. Market growth is driven by premium brand adoption.

Singapore

Singapore contributes 2% share with 65 million units produced. Formal wear accounts for 32%. Adoption of eco-friendly fabrics is 21%, reinforcing market size, growth, and insights.

Taiwan

Taiwan contributes 2% share with 60 million units. Casual wear dominates at 55%. Baby Boy Clothing market trend and demand are supported by urban lifestyle changes.

South East Asia

South East Asia accounts for 7% share with 225 million units produced. Casual wear contribution is 50%. Market growth is driven by rising urban population and online retail expansion.

List of Top Baby Boy Clothing Companies

- Carter’s Inc.

- GAP Inc.

- H&M Group

- Zara Kids (Inditex)

- Uniqlo Co., Ltd.

- Mothercare PLC

- OshKosh B’gosh

- Babyshop

- Petit Bateau

- Ralph Lauren Corporation

- Adidas Kids

- Puma Kids

- Next PLC

- Kiabi

- Marks & Spencer Kids

Top Two Companies

Carter’s Inc.:

-

Holds 12% share in Asia Pacific Baby Boy Clothing market

-

Leading in onesies and casual wear production

-

2026 production volume: 210 million units

-

Offers smart textile integration and personalized garments

-

Strong omnichannel presence with 42% online sales

Carter’s maintains robust market positioning through innovation, diversified product range, and high consumer trust, reinforcing Baby Boy Clothing market size, growth, and demand.

GAP Inc.:

-

Holds 10% share in Asia Pacific market

-

2026 production volume: 175 million units

-

Focus on casual and formal wear segments

-

38% adoption of sustainable fabrics

-

Omnichannel penetration contributes to USD 0.85 billion online revenue

GAP leverages branding, technology adoption, and sustainability initiatives to capture market share and reinforce Baby Boy Clothing market insights, trend, and growth.

Investment Analysis and Opportunities

Investment allocation in the Asia Pacific Baby Boy Clothing market is approximately 40% in production expansion, 25% in R&D for sustainable and smart textiles, 20% in e-commerce infrastructure, and 15% in marketing and brand development. Sector-wise, casual wear accounts for 54% of total investments, formal 28%, and sleepwear 18%. Regional investment highlights China (42%) and India (22%) as primary beneficiaries due to high demand and production capabilities. M&A activity in 2025–2026 included 12 strategic agreements, particularly in smart textile technology adoption and online retail expansion. Collaborative ventures between global brands and local manufacturers enhanced capacity by 8% and reduced supply chain lead times by 14%. Overall, investment opportunities are centered around technological integration, sustainable fabric adoption, and regional expansion, reinforcing Baby Boy Clothing market growth, size, and insights.

New Product Development

New product launches in the Asia Pacific Baby Boy Clothing market accounted for 18% of total production in 2026. Innovations include adjustable sizing onesies, moisture-wicking t-shirts, and modular clothing sets. Performance improvements include 15–20% increase in durability and comfort due to advanced fabrics and stitching technologies. Digital customization platforms enabled 27% faster delivery and personalized product experience. The Baby Boy Clothing market benefits from these developments, reinforcing size, growth, and trend.

Recent Developments

- 2026: Introduction of smart textile onesies increased production by 14%, meeting 210 million units demand, enhancing Baby Boy Clothing market growth.

- 2025: Sustainable fabric adoption rose 18%, producing 670 million units, reflecting environmental-conscious consumer behavior.

- 2025: E-commerce expansion led to 31% increase in online sales, totaling USD 3.2 billion, boosting market size and demand.

Research Methodology

The research process for the Asia Pacific Baby Boy Clothing market involved a multi-step approach, beginning with comprehensive secondary research to collect historical data from 2022–2024, industry reports, government databases, and company annual reports. Primary research included interviews with key stakeholders, such as apparel manufacturers, distributors, and retailers, accounting for 45% of the data validation process. Market size estimation employed bottom-up and top-down approaches, integrating production volumes, average retail pricing, and consumption patterns. Forecasting considered CAGR, segment-wise growth, and regional adoption trends. Data triangulation ensured consistency between primary and secondary sources, while statistical modeling validated projections. Market insights, share, size, and trend were further refined using technical parameters such as garment weight, durability, and fabric adoption rates, ensuring accurate and actionable Baby Boy Clothing market intelligence for strategic planning.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Personal Care and Home Care Products

Mellisa Alcott is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.