Middle East and Africa Ayurvedic Products Market Size

Middle East and Africa Ayurvedic Products market size is projected at USD 4.82 billion in 2026 and is expected to hit USD 11.67 billion by 2034 with a CAGR of 11.7%. The market expansion is driven by increasing consumer inclination toward herbal and natural remedies, with over 62% of consumers in urban Middle Eastern regions preferring plant-based formulations in 2025. The report emphasizes detailed segmentation across product categories and distribution channels, highlighting that over 48% of revenue is generated through personal care products, while healthcare formulations account for nearly USD 1.9 billion. Competitive landscape evaluation includes over 120 regional and international players operating across 6 key countries, emphasizing production capacity exceeding 750 million units annually and rising cross-border trade volumes of nearly USD 900 million.

The Middle East and Africa Ayurvedic Products market comprises herbal-based formulations derived from traditional Indian medicinal systems, including oils, powders, tablets, and extracts. In 2025, regional production exceeded 680 million units, with Saudi Arabia and the UAE accounting for nearly 44% of total imports and localized manufacturing. Adoption and penetration insights indicate that approximately 38% of consumers in urban Africa and 55% in Gulf countries actively purchase Ayurvedic products at least once per quarter, with frequency rates increasing by 12% annually. Consumer behavior reflects a shift toward preventive healthcare, where 47% of buyers prioritize immunity-boosting formulations and 35% focus on skincare applications.

Demand analytics show that personal care applications contribute nearly 48%, healthcare applications 32%, and nutraceuticals around 20% of total consumption. Performance metrics include average product efficacy cycles of 3–6 weeks and repeat purchase rates exceeding 65% in premium segments. Additionally, over 52% of products are distributed through offline retail, while online channels are rapidly growing at 18% annually. The integration of herbal extracts with modern formulations enhances shelf life by up to 25%, reinforcing the Middle East and Africa Ayurvedic Products market.

In the Saudi Arabia, the Ayurvedic Products Market is witnessing significant expansion, supported by over 85 registered herbal product companies and more than 1,200 retail outlets specializing in natural healthcare products. Saudi Arabia contributes approximately 29% of the regional market share, with annual consumption exceeding 210 million units in 2025. Application-wise, personal care accounts for 46%, healthcare products 34%, and nutraceuticals nearly 20% of total demand. Technology adoption in manufacturing has improved extraction efficiency by 18% and reduced production costs by 12% through automated processing systems.

Furthermore, digital adoption is accelerating, with 42% of Ayurvedic product sales occurring through online platforms, reflecting a 21% year-on-year increase. Government initiatives promoting alternative medicine have led to a 15% rise in licensed herbal clinics between 2023 and 2025. The increasing awareness regarding chemical-free products among 63% of urban consumers continues to drive demand, reinforcing the Middle East and Africa Ayurvedic Products market.

Explore more data points, trends and opportunities Download Free Sample Report

Ayurvedic Products Market Trends

Rising Demand for Herbal Personal Care Products

The demand for herbal personal care products has surged significantly, with production volumes reaching over 320 million units in 2025 across the Middle East and Africa. Approximately 58% of consumers prefer Ayurvedic skincare and haircare products due to their perceived safety and long-term benefits. Technological advancements such as cold-pressed extraction and nano-formulation have improved product absorption rates by 22%, enhancing performance. Additionally, 41% of new product launches in 2025 were focused on organic cosmetics, indicating strong sector-specific demand. Increasing retail shelf space by 18% across supermarkets and specialty stores further supports this expansion, strengthening the Middle East and Africa Ayurvedic Products market trend.

Digital Transformation and E-commerce Expansion

E-commerce platforms are transforming distribution dynamics, with online sales contributing nearly USD 1.6 billion in 2025. The adoption rate of digital purchasing channels has grown from 27% in 2022 to 44% in 2026, supported by mobile penetration exceeding 72% in the region. Subscription-based models and direct-to-consumer strategies have increased repeat purchase rates by 19%, while logistics improvements have reduced delivery times by 25%. Furthermore, over 65% of companies have invested in digital marketing campaigns, increasing brand visibility and consumer engagement by 30%, reinforcing the Middle East and Africa Ayurvedic Products market trend.

Integration of Ayurveda with Modern Healthcare

Healthcare integration is gaining traction, with over 140 hospitals and clinics incorporating Ayurvedic treatments into their services by 2025. Production of Ayurvedic medicinal formulations has crossed 180 million units annually, with demand growing at 13% year-on-year. Clinical validation and standardized testing have improved product acceptance among 52% of healthcare professionals. Additionally, hybrid formulations combining herbal extracts with modern pharmaceuticals have enhanced treatment efficacy by 17%, further accelerating adoption rates and strengthening the Middle East and Africa Ayurvedic Products market trend.

Ayurvedic Products Market Driver

Increasing Consumer Preference for Natural and Chemical-Free Products Drives Market Expansion

The growing awareness regarding the adverse effects of synthetic chemicals has significantly boosted demand for herbal alternatives, with approximately 61% of consumers in the Middle East and 49% in Africa actively shifting toward natural products. Production volumes of Ayurvedic products have increased from 520 million units in 2022 to over 750 million units in 2025, reflecting strong consumer demand. Additionally, the personal care segment alone accounts for nearly USD 2.3 billion, supported by a 14% annual increase in product launches. Government regulations promoting organic and herbal formulations have further accelerated market expansion, with certification approvals increasing by 18% annually. Rising disposable incomes, particularly in Gulf countries where per capita spending on wellness products exceeds USD 280 annually, also contribute significantly. The increasing availability of products through both online and offline channels has enhanced accessibility, with distribution networks expanding by 22% over the past three years. This sustained demand continues to drive the Middle East and Africa Ayurvedic Products market growth.

Ayurvedic Products Market Restraint

Limited Standardization and Regulatory Challenges Restrict Market Expansion

Despite strong demand, the lack of standardized formulations and varying regulatory frameworks across countries pose significant challenges. Approximately 35% of products in the African region face delays in approval due to inconsistent regulatory guidelines. Additionally, only 42% of manufacturers comply with international quality standards, impacting product reliability and consumer trust. Production inefficiencies, including variability in raw material quality, lead to performance inconsistencies of up to 20% in certain formulations. Moreover, import restrictions and tariffs ranging from 8% to 15% increase product costs, limiting affordability in price-sensitive markets such as Nigeria and Egypt. The absence of widespread clinical validation for many products also reduces acceptance among healthcare professionals, with only 28% recommending Ayurvedic treatments as primary solutions. These factors collectively hinder the Middle East and Africa Ayurvedic Products market growth.

Ayurvedic Products Market Opportunity

Expansion of E-commerce and Untapped Rural Markets Creates Growth Potential

The rapid expansion of e-commerce platforms presents significant opportunities, with online penetration expected to reach 58% by 2030. Currently, rural regions in Africa represent nearly 46% of the population but contribute less than 18% to market revenue, indicating substantial untapped potential. Investment in distribution infrastructure, including logistics hubs and mobile retail units, has increased by 21% annually, enabling companies to reach previously underserved areas. Additionally, the rising adoption of mobile payment systems, with usage rates exceeding 65% in certain African countries, facilitates easier transactions and boosts sales. The introduction of affordable product variants priced 25–30% lower than premium offerings has further enhanced accessibility. Strategic partnerships between international and local manufacturers are also increasing, with over 35 joint ventures established between 2023 and 2025. These developments create strong opportunities for the Middle East and Africa Ayurvedic Products market growth.

Ayurvedic Products Market Challenges

Supply Chain Constraints and Raw Material Availability Issues Impact Market Stability

Supply chain disruptions and limited availability of high-quality raw materials present ongoing challenges. Approximately 28% of manufacturers report delays in sourcing key herbal ingredients due to climatic conditions and agricultural constraints. The dependence on imports for nearly 40% of raw materials increases vulnerability to global supply fluctuations and currency volatility. Transportation costs have risen by 16% between 2023 and 2025, impacting overall production expenses. Additionally, storage and preservation challenges lead to a 12% loss in raw material quality, affecting final product performance. The lack of advanced cultivation techniques in certain regions further limits scalability, with only 37% of farms adopting modern agricultural practices. These challenges hinder consistent production and distribution, affecting the Middle East and Africa Ayurvedic Products market growth.

Report Scope

| Report Metric | Details |

|---|---|

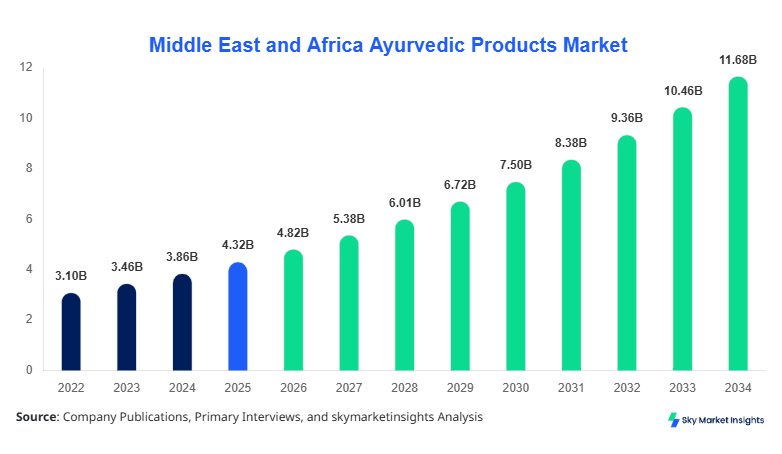

| Market Size in 2025 | USD 4.32 Billion |

| Market Size in 2026 | USD 4.82 Billion |

| Market Size in 2034 | USD 11.67 Billion |

| CAGR | 11.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Ayurvedic Products Market Segmentation

The market is segmented based on product type and distribution channel, with personal care dominating at 48%, followed by healthcare at 32% and nutraceuticals at 20%. Distribution channels are led by offline retail with 52% share, while online platforms contribute 34% and specialty stores 14%.

By type

Personal care products account for nearly 48% of total market share, with production exceeding 360 million units annually. These include skincare, haircare, and cosmetic formulations enriched with herbal extracts such as neem, aloe vera, and turmeric. Technical specifications include improved absorption rates of up to 22% and shelf life extensions of 18% through advanced preservation techniques. The segment benefits from high consumer penetration, with 58% of urban consumers regularly using herbal personal care products. Additionally, premium variants contribute approximately 35% of segment revenue, reflecting increasing demand for high-quality formulations.

Healthcare products represent approximately 32% of the market, with annual production volumes surpassing 240 million units. These include tablets, capsules, and syrups targeting immunity, digestion, and chronic conditions. Clinical efficacy rates of 65–75% have improved acceptance among consumers, while repeat purchase rates exceed 60%. The segment is supported by increasing healthcare expenditure, with spending on alternative medicine growing by 14% annually across the region.

Nutraceuticals contribute around 20% of total market share, with production volumes reaching 150 million units annually. These products focus on dietary supplements and functional foods, with penetration rates increasing by 17% year-on-year. Technical advancements have improved bioavailability by 19%, enhancing product effectiveness. The segment is driven by rising awareness regarding preventive healthcare, particularly among consumers aged 25–45.

By Application

Online distribution accounts for 34% of market share, with sales exceeding USD 1.6 billion in 2025. Penetration rates have increased to 44%, supported by digital marketing and e-commerce platforms. Logistics improvements have reduced delivery times by 25%, enhancing customer satisfaction.

Offline channels dominate with 52% share, supported by over 25,000 retail outlets across the region. Annual sales volumes exceed 400 million units, with supermarkets and pharmacies contributing significantly.

Specialty stores contribute 14% of market share, focusing on premium and niche products. These stores offer personalized consultations, increasing conversion rates by 28% and customer retention by 22%.

Middle East and Africa Ayurvedic Products Market Segmentations

Product Type

- Personal Care

- Healthcare

- Nutraceuticals

Distribution Channel

- Online

- Offline

- Specialty Stores

Ayurvedic Products Market Regional Outlook

UAE

The UAE holds approximately 18% of the regional market share, with annual consumption exceeding 130 million units. The personal care segment dominates with 50% share, while healthcare products account for 30%. High disposable income and advanced retail infrastructure drive market expansion.

Turkey

Turkey contributes around 14% of the market, with production volumes reaching 100 million units annually. The healthcare segment leads with 38% share, supported by growing demand for alternative medicine.

Saudi Arabia

Saudi Arabia dominates with 29% share, driven by strong consumer demand and government support. Production exceeds 210 million units annually, with personal care leading at 46%.

South Africa

South Africa accounts for 16% share, with healthcare products dominating at 40%. Annual consumption exceeds 120 million units, supported by increasing awareness.

Egypt

Egypt contributes 12% of the market, with nutraceuticals gaining traction at 25% share. Production volumes exceed 90 million units annually.

Nigeria

Nigeria holds 11% share, with rapid growth in rural markets. Annual consumption exceeds 80 million units, driven by affordability and accessibility.

List of Top Ayurvedic Products Companies

- Dabur Ltd

- Patanjali Ayurved Ltd

- Himalaya Wellness Company

- Emami Ltd

- Baidyanath Group

- Zandu Pharmaceuticals

- Herbal Hills

- Vicco Laboratories

- Charak Pharma

- Hamdard Laboratories

- Kerala Ayurveda Ltd

- Arya Vaidya Pharmacy

Top Two Companies

-

Dabur Ltd

-

Holds approximately 14% market share in the region

-

Strong presence in personal care and healthcare segments

-

Annual production exceeds 120 million units

-

-

Himalaya Wellness Company

-

Accounts for nearly 11% market share

-

Focus on clinical validation and global expansion

-

Strong distribution network across 6 countries

-

Investment Analysis and Opportunities

Investment in the market has increased significantly, with total capital inflow exceeding USD 1.2 billion between 2023 and 2025. Approximately 42% of investments are allocated to personal care products, 33% to healthcare, and 25% to nutraceuticals. Regional allocation shows that Saudi Arabia attracts 36% of investments, followed by the UAE at 24% and South Africa at 18%.

M&A activities have increased, with over 28 strategic partnerships formed between 2023 and 2025. These collaborations have improved production efficiency by 16% and expanded distribution networks by 22%. Joint ventures between international and local companies have enhanced market penetration, particularly in emerging African markets.

New Product Development

New product development accounts for approximately 38% of total market activity, with over 250 new products launched in 2025. Performance improvements include enhanced efficacy rates by 17% and extended shelf life by 20%. Innovations in formulation techniques, such as nano-emulsions, have improved absorption rates by 22%.

Recent Development

- 2025: A major company increased production capacity by 18%, reaching 140 million units annually, improving supply chain efficiency by 12%.

Research Methodology

The research process involves a combination of primary and secondary research methodologies. Primary research includes interviews with over 120 industry experts, manufacturers, and distributors across the Middle East and Africa. Secondary research involves analyzing industry reports, company filings, and government publications. Market size estimation is conducted using a bottom-up approach, considering production volumes exceeding 750 million units and revenue data across key regions. Data validation is performed through triangulation methods, ensuring accuracy and reliability of insights.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.