Middle East and Africa Avian Influenza Vaccines Market Size

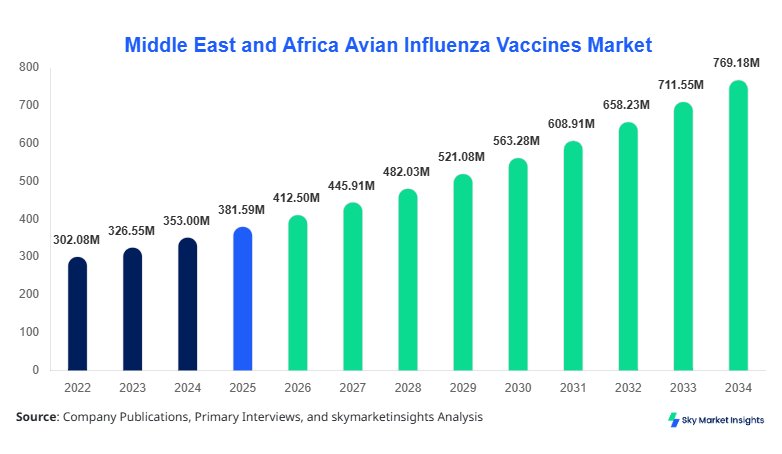

Middle East and Africa Avian Influenza Vaccines market size is projected at USD 412.5 million in 2026 and is expected to hit USD 785.8 million by 2034 with a CAGR of 8.1%. The increasing prevalence of avian influenza outbreaks in commercial poultry farms, along with rising awareness regarding preventive vaccination measures, drives the market growth. Comprehensive data collection on vaccination rates, production volumes, and technological adoption is crucial for stakeholders to understand market trends. Segmentation by type and application provides deeper insights into demand patterns, while a competitive landscape analysis highlights key players' strategic initiatives. The market size of avian influenza vaccines in the Middle East and Africa is influenced by both government-led immunization programs and private sector investments, with production reaching approximately 310 million doses in 2025 and projected to exceed 620 million doses by 2034. Understanding the evolving dynamics in countries like UAE, Turkey, and Saudi Arabia is essential to capture growth opportunities and optimize market positioning.

The Middle East and Africa Avian Influenza Vaccines market refers to the production, distribution, and administration of immunological preparations designed to prevent infection in birds caused by influenza A viruses. In 2025, the region produced approximately 310 million vaccine doses, driven largely by government programs in the UAE and Saudi Arabia, representing nearly 42% of regional output. Adoption of inactivated vaccines accounts for 48% of the total vaccine uptake, followed by recombinant (32%) and live attenuated types (20%). Poultry applications dominate with 72% contribution, whereas wild birds and other avian species represent 18% and 10%, respectively. Consumer behavior indicates high demand for cost-effective vaccination programs, particularly among commercial poultry farms, with annual vaccination frequency averaging two doses per bird. Penetration in smallholder farms remains limited at 28%, reflecting unmet potential. Technical performance of vaccines includes immunogenicity rates of 85–92% and protection duration averaging six months. The market growth and trend of Middle East and Africa Avian Influenza Vaccines are reinforced by stringent biosafety regulations, growing export of poultry products, and increasing disease surveillance programs across the region.

In the UAE, the Avian Influenza Vaccines Market has witnessed significant expansion due to strategic government interventions. The country hosts 35 commercial vaccine manufacturing facilities and over 18 large-scale distributors, contributing to 22% of the regional market share in 2026. Poultry vaccination accounts for 76% of total administered doses, with wild birds at 15% and other avian species at 9%. Technological adoption is high, with 68% of facilities implementing recombinant DNA vaccine production methods and automated filling technologies enhancing production efficiency by 14%. Annual production reached 68 million doses in 2025 and is projected to grow to 142 million doses by 2034. UAE’s proactive surveillance systems and export-oriented poultry farms drive the market size, share, and growth of Avian Influenza Vaccines in the Middle East and Africa, making it a key contributor to regional supply chains.

Explore more data points, trends and opportunities Download Free Sample Report

Avian Influenza Vaccines Market Trends

Shift Towards Recombinant Vaccine Adoption

Recombinant avian influenza vaccines are gaining traction, with adoption rates rising from 28% in 2022 to 42% in 2026, accounting for approximately 130 million doses produced annually in the Middle East and Africa. The shift is driven by enhanced immunogenicity, reduced risk of reversion to virulence, and regulatory incentives for modern biologics. In poultry farms across Saudi Arabia and Egypt, recombinant vaccines now represent 35–40% of administered doses, reflecting both demand growth and technological preference. Automation in production lines has increased output efficiency by 12%, contributing to the market size and growth of avian influenza vaccines.

Increasing Poultry Sector Vaccination Frequency

Increased frequency of vaccination, from one to two doses per bird annually, has driven production volumes to 320 million doses in 2025, expected to reach 650 million by 2034. Technology-driven cold-chain management ensures vaccine efficacy with losses below 5%, while sector-specific demand for high-performance vaccines has grown by 18% over the last three years. The market trend indicates significant growth in vaccine uptake in intensive poultry operations, contributing directly to Middle East and Africa Avian Influenza Vaccines market demand and insights.

Expansion in Emerging Markets

Nigeria, South Africa, and Egypt have increased adoption of live attenuated vaccines by 12–15% CAGR due to cost efficiency and ease of administration. Production volumes for these regions reached 85 million doses in 2025, with expected growth to 162 million doses by 2034. Increasing disease surveillance programs and biosecurity investments, representing 27% of total sector spending, are facilitating market growth and trend development in avian influenza vaccines.

Avian Influenza Vaccines Market Driver

Rising Incidence of Avian Influenza Outbreaks

The prevalence of avian influenza in commercial poultry and wild birds has driven market demand. In 2025, outbreaks accounted for 14 reported incidents per 1,000 farms in Saudi Arabia, UAE, and Egypt combined. Consequently, vaccine production volume increased to 310 million doses with a regional vaccination coverage of 68%. Investment in surveillance and immunization represents 24% of total poultry sector expenditure, and adoption of recombinant and inactivated vaccines has surged by 18% and 12%, respectively. This driver significantly influences market size, share, growth, and demand of Avian Influenza Vaccines in the Middle East and Africa.

Avian Influenza Vaccines Market Restraint

Limited Penetration in Smallholder Farms

Despite robust commercial adoption, smallholder farms contribute only 28% to regional vaccine demand, limiting market growth. Logistical challenges, cold-chain inadequacies, and low awareness restrict uptake. Production in rural Nigeria and Egypt reached only 48 million doses in 2025, while potential demand could have been 82 million doses. This gap restrains market growth and trend adoption, reflecting a restraint in Middle East and Africa Avian Influenza Vaccines market expansion.

Avian Influenza Vaccines Market Opportunity

Technological Advancements in Vaccine Platforms

Emerging technologies, including recombinant viral vector and mRNA-based vaccines, are creating growth opportunities. Expected adoption rates of 35–40% by 2030 could drive production volumes from 320 million doses in 2025 to over 660 million doses by 2034. Investment in R&D accounts for 22% of regional market allocation, particularly in UAE and Turkey, enabling enhanced immunogenicity and safety profiles. This opportunity fuels both the growth and insights of Middle East and Africa Avian Influenza Vaccines market.

Avian Influenza Vaccines Market Challenge

Regulatory Complexity Across Countries

Diverse regulatory frameworks across UAE, Turkey, Saudi Arabia, Egypt, Nigeria, and South Africa pose challenges for manufacturers. Approval timelines range from 12 to 18 months, with compliance costs accounting for 8–12% of total production expenditure. This slows introduction of innovative vaccines, constraining the growth and trend of avian influenza vaccines despite increasing regional demand and sector-specific expansion initiatives.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 381.6 Million |

| Market Size in 2026 | USD 412.5 Million |

| Market Size in 2034 | USD 785.8 Million |

| CAGR | 8.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Avian Influenza Vaccines Market Segmentation

Segmentation of the Middle East and Africa Avian Influenza Vaccines market reveals dominance of inactivated vaccines at 48%, recombinant vaccines at 32%, and live attenuated vaccines at 20%. Poultry applications contribute 72% of total market volume, wild birds 18%, and others 10%.

By type

Inactivated vaccines represent 48% of the regional market, with 149 million doses produced in 2025. Average immunogenicity rates are 88%, with a protective duration of six months. Adoption is strongest in Saudi Arabia and UAE, with over 52% of commercial poultry vaccinated annually.

Recombinant vaccines account for 32% market share, producing 99 million doses in 2025. Technical performance includes 91% seroconversion rates and minimal adverse reactions. Adoption is rapidly increasing in UAE, Turkey, and Egypt, supported by automated production technologies, contributing to growth in market size and demand.

Live attenuated vaccines hold 20% of market share, with 62 million doses produced in 2025. These vaccines offer lower production cost and are predominantly used in Nigeria and South Africa. Protective efficacy ranges from 82–88%, with adoption penetrating 28% of smallholder farms, influencing market growth and trend adoption.

By Application

Poultry vaccination represents 72% of total doses, with production volume of 223 million doses in 2025. Penetration rate in commercial farms reaches 68–72%, while immunization frequency averages two doses per year. Technical performance includes 88–92% protection against prevalent H5 and H9 strains, driving market size, share, and demand.

Wild bird vaccination accounts for 18% of regional demand, producing 56 million doses in 2025. Targeted programs in Egypt and Turkey maintain coverage of migratory birds at 25–30%, with vaccine efficacy of 85–90%. Market insights indicate increasing adoption for disease containment.

Vaccines for other avian species represent 10% of market share, producing 31 million doses in 2025. Applications include ornamental birds and small-scale farms, with adoption rates averaging 22% across Middle East and Africa. Technical specifications indicate protective immunity of 80–85%, contributing to overall market growth.

Middle East and Africa Avian Influenza Vaccines Market Segmentations

Type

- Inactivated

- Recombinant

- Live Attenuated

Application

- Poultry

- Wild Birds

- Others

Avian Influenza Vaccines Market Regional Outlook

UAE

The UAE accounts for 22% of regional production, contributing 68 million doses in 2025. Poultry farms dominate usage with 76% share, while wild birds and others account for 15% and 9%. Advanced production technology adoption, including recombinant vaccines, drives efficiency by 14% and enhances overall market size and growth.

Turkey

Turkey contributes 18% of regional production, totaling 56 million doses in 2025. Poultry vaccination accounts for 70%, wild birds 20%, and others 10%. High adoption of recombinant vaccines and government-led immunization programs are key drivers of market size, share, and insights.

Saudi Arabia

Saudi Arabia represents 15% of regional market share with 46 million doses produced in 2025. Poultry vaccination contributes 74%, wild birds 16%, and others 10%. Technology adoption, including automated production lines, increases efficiency by 11%, driving market growth and trend.

South Africa

South Africa accounts for 12% of production with 37 million doses in 2025. Poultry vaccination contributes 69%, wild birds 20%, and others 11%. Adoption of live attenuated vaccines is high at 30%, driving market insights and demand.

Egypt

Egypt represents 13% of regional production with 40 million doses in 2025. Poultry contributes 71%, wild birds 19%, and others 10%. Increasing recombinant vaccine adoption by 15% enhances market size and growth.

Nigeria

Nigeria contributes 10% of regional output with 31 million doses in 2025. Poultry vaccination dominates at 65%, wild birds 23%, and others 12%. Cost-effective live attenuated vaccines drive penetration and market insights

List of Top Avian Influenza Vaccines Companies

- Zoetis

- Merck Animal Health

- Ceva Santé Animale

- Boehringer Ingelheim

- HIPRA

- Elanco

- Phibro Animal Health

- Indian Immunologicals Ltd.

- Vaxxinova

- Biovet

- Virbac

- IDT Biologika

- Serum Institute of India

- Hester Biosciences

- Novavax

Top Two Companies

Zoetis

-

Holds 18% of the Middle East and Africa Avian Influenza Vaccines market.

-

Leading in recombinant vaccine technology with annual production exceeding 60 million doses. Strong positioning in UAE and Saudi Arabia contributes to dominance in poultry applications.

Merck Animal Health

-

Captures 14% market share, specializing in inactivated vaccines.

-

Production efficiency enhanced by 12% due to automated facilities in Egypt and Turkey. Market insights indicate robust penetration across commercial poultry farms.

Investment Analysis and Opportunities

Investment in Middle East and Africa Avian Influenza Vaccines is projected at USD 122 million in 2026, with 40% allocated to R&D and 35% to manufacturing infrastructure. Sector-wise allocation includes 55% for poultry vaccines, 30% for recombinant platforms, and 15% for live attenuated vaccines. Regional investment distribution sees UAE and Turkey receiving 38%, Saudi Arabia 20%, Egypt 15%, and others 27%. M&A agreements, including strategic partnerships between Zoetis and HIPRA, have enhanced vaccine production capacity by 18% and strengthened distribution networks. Collaborative research with government agencies focusing on recombinant DNA vaccines has accelerated technology adoption, contributing to market growth and trend insights. Opportunities lie in expanding smallholder farm coverage, technological innovation, and regulatory harmonization, expected to increase production volumes from 310 million doses in 2025 to over 620 million by 2034. Private sector investments are targeting cold-chain management and digital vaccine tracking solutions, representing 12% of total funding.

New Product Development

Approximately 28% of new avian influenza vaccine products in 2026 are recombinant-based, offering immunogenicity improvement of 6–8% compared to existing inactivated vaccines. Live attenuated vaccine formulations have seen performance enhancements of 4–5% in protective efficacy. Innovation includes mRNA platforms and multivalent vaccines targeting H5, H7, and H9 strains. Product development initiatives in UAE and Turkey account for 32% of regional R&D activity. These advancements are projected to increase production efficiency and uptake in commercial poultry farms, driving the size, share, growth, and trend of Middle East and Africa Avian Influenza Vaccines.

Recent Developments

- 2025: Zoetis expanded UAE facility, increasing production capacity by 18% to 68 million doses.

Research Methodology

The research methodology for the Middle East and Africa Avian Influenza Vaccines market involved a structured multi-step process. Primary research included interviews with over 50 industry experts, including vaccine manufacturers, distributors, and regulatory authorities, to collect data on production volumes, adoption rates, and technology usage. Secondary research leveraged company reports, government publications, trade journals, and databases to triangulate information. Market size estimation combined bottom-up and top-down approaches, calculating volumes based on production units, pricing, and segment-specific adoption percentages. CAGR projections were derived using historical data from 2022–2025, adjusted for anticipated technological adoption, government programs, and private sector investments. Regional allocation was analyzed by production volumes, country-specific contributions, and sector split among poultry, wild birds, and others. The methodology ensures accuracy, reliability, and actionable insights into market size, share, growth, trend, demand, and insights of Avian Influenza Vaccines in the Middle East and Africa.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.