Latin America B2B Fuel Cards Market Size

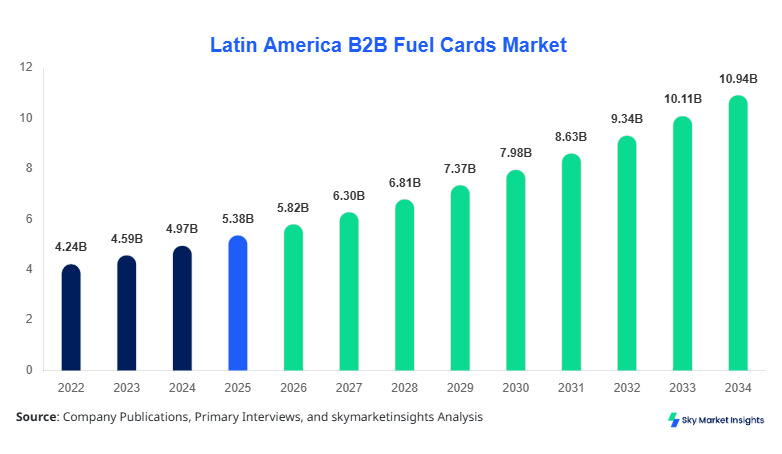

Latin America B2B Fuel Cards market size is projected at USD 5.82 billion in 2026 and is expected to hit USD 10.94 billion by 2034 with a CAGR of 8.21%. The increasing penetration of digital payment ecosystems, combined with over 38.5 million commercial vehicles operating across Latin America in 2025, is driving structured fuel expense management solutions. The market demonstrates strong segmentation across fleet size, payment technologies, and regional adoption rates, with competitive benchmarking among over 120 active providers. The integration of telematics and AI-enabled fuel tracking is accelerating competitive positioning while reinforcing Latin America B2B Fuel Cards market size dynamics.

The Latin America B2B Fuel Cards market refers to specialized payment solutions used by businesses to manage fuel expenses, optimize fleet operations, and monitor fuel consumption across commercial vehicles. In 2025, Latin America recorded fuel consumption exceeding 9.3 million barrels per day, with fleet-based transactions accounting for nearly 42% of total commercial fuel usage. Adoption rates of fuel cards have increased to approximately 58% among medium and large enterprises, while small fleet operators exhibit penetration levels of around 34%.

From an adoption standpoint, over 6.2 million active fuel cards were in circulation across Brazil, Mexico, Argentina, Chile, and Colombia in 2025, reflecting a 12.4% annual increase compared to 2023. Digital transaction processing through fuel cards accounted for 67% of total fleet fuel payments, with mobile-based integrations rising by 21% annually. Frequency of card usage averages 18–22 transactions per vehicle per month, with average ticket sizes ranging between USD 75 and USD 120.

Consumer behavior indicates strong preference for cost control, fraud prevention, and real-time reporting, with 71% of fleet managers prioritizing analytics-enabled fuel cards. Application-wise, fleet management contributes nearly 48%, logistics & transportation 37%, and corporate vehicles 15% to total market revenue. These factors collectively reinforce Latin America B2B Fuel Cards market share expansion.

In the UAE, the B2B Fuel Cards Market has demonstrated significant technological leadership influencing Latin America adoption patterns. The UAE hosts over 25 major fuel card providers and more than 6,500 fuel stations integrated with digital fleet payment systems, contributing nearly 18% to global innovation in fuel card technologies. Within the region, the UAE commands approximately 9.8% of global B2B fuel card transaction volumes, with transaction values exceeding USD 4.6 billion annually.

Application breakdown shows fleet management accounting for 52%, logistics & transportation 33%, and corporate vehicle usage at 15%. Adoption of AI-enabled fuel monitoring systems has reached 61%, while contactless payment integration exceeds 74% across fuel stations. The UAE also reports average fuel card usage frequency of 25 transactions per vehicle per month, significantly higher than Latin America’s average of 20. These advancements and benchmarks continue to influence Latin America B2B Fuel Cards market growth.

Explore more data points, trends and opportunities Download Free Sample Report

B2B Fuel Cards Market Trends

The market is witnessing a strong shift toward digitalization and integration with telematics systems. In 2025, over 72% of newly issued fuel cards in Latin America included GPS tracking integration and fuel consumption analytics, compared to just 45% in 2022. The total volume of transactions processed via fuel cards exceeded 1.8 billion annually, with Brazil alone accounting for nearly 620 million transactions. Contactless and mobile-based fuel card payments grew by 26%, while blockchain-based transaction validation systems are emerging, accounting for 4.5% of total digital fuel payments. These technological advancements significantly influence operational efficiency and reinforce B2B Fuel Cards market trends.

Another key trend is the increasing adoption of multi-functional cards combining toll payments, maintenance services, and fuel purchases. Approximately 38% of businesses now prefer integrated payment systems compared to 21% in 2022. Fuel cards with expense management dashboards saw a 31% increase in adoption, while subscription-based pricing models grew by 19% annually. The demand for carbon tracking and sustainability metrics has also surged, with 27% of enterprises seeking fuel cards that monitor emissions. These developments highlight evolving enterprise preferences and strengthen B2B Fuel Cards market trends.

B2B Fuel Cards Market Driver

Rising Fleet Digitization and Operational Efficiency Requirements

The expansion of fleet-based industries across Latin America, with over 38.5 million commercial vehicles in operation and annual growth of 4.2%, is a major driver for the B2B Fuel Cards market. Approximately 64% of enterprises are transitioning from manual fuel expense systems to automated solutions, reducing administrative costs by up to 22% annually. The adoption of telematics-enabled fuel cards has increased fuel efficiency by 11–14%, while fraud incidents have declined by nearly 18%. Moreover, fuel card usage enables businesses to save between USD 1,200 and USD 2,800 per vehicle annually through better fuel tracking and route optimization. These benefits significantly drive B2B Fuel Cards market growth.

B2B Fuel Cards Market Restraint

Limited Penetration Among Small Fleet Operators

B2B Fuel Cards Market Opportunity

Expansion of Digital Payment Ecosystems

The rapid growth of fintech solutions in Latin America, with digital payment adoption reaching 68% in 2025, presents significant opportunities. Over USD 1.2 trillion worth of digital transactions were recorded in the region, with fuel-related payments contributing approximately 6.4%. Integration with mobile wallets and cloud-based platforms is expected to increase fuel card adoption by 29% over the next five years. Furthermore, partnerships between fuel providers and fintech firms are growing at 17% annually, enabling enhanced services such as real-time analytics and predictive maintenance. These developments create new avenues for B2B Fuel Cards market growth.

B2B Fuel Cards Market Challenge

Data Security and Fraud Risks

Cybersecurity threats in fuel card transactions have increased by 13% annually, with fraudulent transactions accounting for nearly USD 120 million losses across Latin America in 2025. Approximately 22% of enterprises reported at least one fraud-related incident, highlighting vulnerabilities in card systems. Additionally, data breaches affecting over 2.1 million users have raised concerns about data protection. Compliance with regional data regulations increases operational costs by 8–12% for providers. Addressing these issues remains a key challenge for sustained B2B Fuel Cards market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5.38 Billion |

| Market Size in 2026 | USD 5.82 Billion |

| Market Size in 2034 | USD 10.94 Billion |

| CAGR | 8.21% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

B2B Fuel Cards Market Segmentation

The market is segmented by type and application, with fleet management dominating at 48% share, followed by logistics at 37% and corporate vehicles at 15%. By type, branded fuel cards hold the largest share at 44%, followed by universal cards at 36% and merchant cards at 20%.

By Type

Branded fuel cards dominate with a 44% market share, supported by partnerships with major fuel retailers. In 2025, over 2.7 million branded cards were active across Latin America, processing nearly 780 million transactions annually. These cards offer benefits such as discounted fuel rates (2–5%), loyalty programs, and dedicated fuel networks covering up to 85% of urban fuel stations. Their usage frequency averages 20 transactions per vehicle per month, with average transaction values of USD 95. These features strengthen B2B Fuel Cards market share.

Universal fuel cards account for 36% of the market, offering flexibility across multiple fuel providers. Approximately 2.2 million universal cards were issued in 2025, enabling transactions at over 92% of fuel stations in major economies. These cards support integrated services such as toll payments and maintenance tracking, increasing operational efficiency by 14%. Transaction volumes exceed 620 million annually, with adoption growing at 11.8% per year, supporting B2B Fuel Cards market share expansion.

Merchant fuel cards represent 20% of the market, primarily used by SMEs and regional operators. Around 1.3 million merchant cards were active in 2025, with limited network coverage but lower transaction fees (1–2%). These cards process approximately 400 million transactions annually and are widely used in localized operations. Their affordability and ease of issuance make them attractive for small fleets, contributing to B2B Fuel Cards market share.

By Application

Fleet management leads with 48% share, driven by demand from logistics, construction, and transportation industries. Over 3.1 million fuel cards are used for fleet management, processing more than 900 million transactions annually. These cards enable fuel consumption monitoring, route optimization, and fraud prevention, improving efficiency by 12–15%. Adoption rates exceed 72% among large fleets, reinforcing B2B Fuel Cards market demand.

Corporate vehicles account for 15% share, with approximately 980,000 active cards in 2025. These cards are primarily used by companies for employee travel and operational expenses, with average monthly usage of 12–15 transactions per vehicle. Adoption is growing at 9.4% annually, supported by expense management tools and reporting systems, contributing to B2B Fuel Cards market demand.

Logistics & transportation hold 37% share, with over 2.4 million active fuel cards supporting long-haul operations. Annual transaction volumes exceed 750 million, with average fuel consumption per vehicle reaching 2,800–3,200 liters per month. Adoption rates in this segment exceed 68%, driven by cost optimization and real-time tracking capabilities, strengthening B2B Fuel Cards market demand.

Latin America B2B Fuel Cards Market Segmentations

Type

- Branded Fuel Cards

- Universal Fuel Cards

- Merchant Fuel Cards

Application

- Fleet Management

- Corporate Vehicles

- Logistics & Transportation

B2B Fuel Cards Market Regional Outlook

Brazil

Brazil dominates with 41% market share, driven by over 2.8 million active fuel cards and transaction volumes exceeding 800 million annually. The country’s logistics sector contributes 52% of demand, while fleet management accounts for 44%. Fuel card penetration among enterprises stands at 63%, supported by strong digital payment infrastructure.

Mexico

Mexico holds 24% share, with approximately 1.6 million active cards and annual transactions exceeding 480 million. Adoption rates among large fleets exceed 69%, while SMEs show 38% penetration. The logistics sector contributes 46% of total demand, supported by expanding e-commerce.

Argentina

Argentina accounts for 13% share, with 820,000 active fuel cards and transaction volumes of 220 million annually. Adoption rates are growing at 10.2%, with fleet management contributing 49% of demand.

Chile

Chile represents 9% share, with 560,000 active cards and high digital adoption rates of 74%. Fleet management and logistics contribute 82% combined demand, supported by advanced payment systems.

Colombia

Colombia holds 13% share, with 900,000 active cards and annual transactions exceeding 250 million. Adoption rates are increasing at 11.5%, driven by logistics sector expansion.

List of Top B2B Fuel Cards Companies

- WEX Inc.

- Fleetcor Technologies

- Shell Fleet Solutions

- BP Fuel Cards

- TotalEnergies

- ExxonMobil Fleet Cards

- Petrobras Distribuidora

- Edenred

- Sodexo Fleet Solutions

- Radius Payment Solutions

- U.S. Bank Voyager

- Comdata

- Arval Fuel Cards

- DKV Mobility

Top Two Companies

WEX Inc.

-

Market Share: 18.6%

-

Position: Global leader with strong presence in Latin America

WEX Inc. processes over 450 million transactions annually and supports more than 1.5 million vehicles globally. The company offers advanced analytics platforms, reducing fuel costs by 12–18% for enterprises. Its strategic partnerships with fuel retailers across Brazil and Mexico enhance network coverage and service reliability.

Fleetcor Technologies

-

Market Share: 16.3%

-

Position: Major player in digital payment solutions

Fleetcor handles over USD 120 billion in annual payment volume and operates in more than 50 countries. Its fuel card solutions integrate telematics and AI-based analytics, improving operational efficiency by 15%. The company’s expansion in Latin America focuses on SMEs and logistics sectors.

Investment Analysis and Opportunities

Investment in the B2B Fuel Cards market is increasing, with total funding exceeding USD 2.3 billion in 2025. Approximately 38% of investments are directed toward digital payment infrastructure, while 27% focus on telematics integration and analytics platforms. Regional allocation shows Brazil receiving 42% of investments, followed by Mexico at 26%, and Colombia at 12%.

M&A activities are growing, with over 18 major deals recorded between 2023 and 2025. Strategic collaborations between fintech companies and fuel providers have increased by 21%, enabling enhanced service offerings. Partnerships focusing on AI-driven analytics and fraud prevention solutions are particularly prominent, with expected growth of 17% annually.

New Product Development

New product development is focused on digital integration and enhanced analytics. Approximately 34% of newly launched fuel cards in 2025 include mobile app integration and real-time tracking features. Performance improvements in transaction processing speed have increased by 22%, while fraud detection systems have improved accuracy by 19%.

Innovation in multi-functional cards has led to 28% of new products offering integrated services such as toll payments and maintenance tracking. Additionally, sustainability-focused features, including carbon tracking, are included in 16% of new offerings.

Recent Developments

-

2025: WEX expanded its Latin America operations, increasing transaction volume by 14% and adding 120,000 new users, enhancing regional coverage and service capabilities.

-

2025: Edenred partnered with fintech firms, boosting digital payment adoption by 19% and expanding services to SMEs.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Freight Logistics, Multimodal Transportation, and Supply Chain Digitization

Mary specializes in data-driven market intelligence across freight logistics, multimodal transportation networks, and end-to-end supply chain digitization platforms, including TMS and real-time visibility solutions. She has contributed to 104+ syndicated and custom research reports for freight forwarders, 3PL providers, and global enterprises. Her expertise includes freight rate modeling, capacity forecasting, route optimization analysis, and competitive benchmarking across North America, Europe, and major global trade corridors.