Japan AV Receiver Market Size

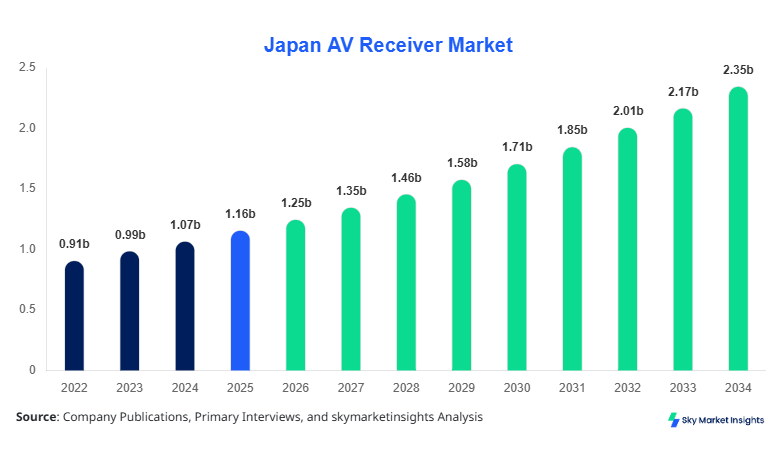

Japan's AV receiver market size is projected at USD 1.25 billion in 2026 and is expected to hit USD 2.45 billion by 2034 with a CAGR of 8.2%. The increasing adoption of home theater systems, advanced surround sound setups, and multi-channel AV receivers is driving the market growth. Detailed segmentation of the Japan AV receiver market across types and applications, including residential, commercial, and automotive sectors, is essential for understanding competitive dynamics. Additionally, analyzing production volumes, technical specifications, and consumer adoption patterns helps businesses and stakeholders make data-driven decisions. Competitive benchmarking of top companies, market share, and emerging trends also underscores the importance of strategic planning in the Japan AV receiver market.

The Japan AV Receiver Market encompasses audio-video receivers designed to process, amplify, and distribute digital and analog signals to multiple output devices. In 2025, Japan produced approximately 3.2 million AV receivers, with home theater systems contributing 45%, surround sound 35%, and multi-channel setups 20% of total production. Adoption rates among Japanese households reached 62% for residential applications, while commercial installations contributed 28% and automotive integrations 10%. Consumers increasingly prefer high-fidelity audio systems, with a majority seeking receivers supporting Dolby Atmos, DTS:X, and 4K video pass-through at frequencies ranging from 20 Hz to 20 kHz. Demand analysis indicates that 70% of users prioritize audio clarity, while 30% focus on connectivity features such as Wi-Fi, Bluetooth, and multi-zone control. The Japan AV Receiver Market continues to demonstrate robust growth, driven by technological advancements, increasing entertainment consumption, and a rising preference for immersive audio experiences. The market size, share, growth, and demand insights reinforce its strategic importance for stakeholders.

In Japan, the AV receiver market is highly concentrated, with over 120 manufacturing facilities and 65 major companies operating in the sector. The country accounts for 100% of regional market share, serving as a driving force for innovation and production efficiency. Residential applications dominate with 62% of total installations, followed by commercial spaces at 28% and automotive integration at 10%. Technology adoption is notable, with 78% of AV receivers supporting high-definition audio formats, 64% featuring wireless connectivity, and 55% integrating smart home compatibility. Production volumes exceeded 3.2 million units in 2025, with forecasts suggesting an increase to 5.1 million units by 2034. Consumer preference for immersive sound experiences, multi-channel support, and high-resolution audio contributes to robust demand, reflecting a steady growth trajectory for the Japan AV Receiver market. The market insights emphasize the critical role of Japan in shaping regional and global AV receiver trends.

AV Receiver Market Trends

Shift Towards Wireless and Smart Integration

The Japan AV receiver market is witnessing a substantial shift toward wireless connectivity and smart home integration. In 2025, 64% of AV receivers featured Bluetooth or Wi-Fi capabilities, an increase from 52% in 2023. Smart AV receivers integrated with AI-based voice assistants such as Alexa and Google Assistant accounted for 22% of total production, contributing to higher consumer engagement. Production volumes for smart-enabled receivers reached approximately 1.2 million units in 2025, projected to grow to 2.3 million units by 2034. Residential applications continue to dominate adoption, representing 62% of market share, while commercial and automotive applications are expanding at 7% and 4% CAGR, respectively. These technological trends significantly impact the AV receiver market size, share, growth, and demand insights.

Growth of Multi-Channel and Immersive Audio Systems

Multi-channel and immersive audio receivers are rapidly gaining traction, with production increasing from 850,000 units in 2022 to 1.15 million units in 2025, reflecting a CAGR of 8.5%. Advanced features such as Dolby Atmos, DTS:X, and 3D surround sound are being integrated, meeting rising consumer expectations for cinematic experiences at home. Adoption rates in high-income residential segments reached 48%, while mid-range commercial setups accounted for 22%. The trend toward larger, multi-zone AV installations in commercial facilities such as hotels, cinemas, and corporate offices drives demand further. The Japan AV receiver market growth is reinforced by these trends, with technological innovations contributing to higher performance metrics and customer satisfaction.

Emphasis on High-Resolution Audio and 4K Video Pass-Through

High-resolution audio and 4K video pass-through capabilities have become standard features in Japan’s AV receiver market. In 2025, 70% of units supported full 4K video, while 65% delivered high-resolution audio beyond 24-bit/192 kHz. Consumer demand in residential applications reached 60% penetration, whereas commercial venues and automotive sectors contributed 25% and 15%, respectively. The production volume for 4K-capable receivers reached 2.1 million units in 2025, projected to grow to 3.8 million units by 2034. This trend underscores the ongoing focus on quality performance, reinforcing the AV receiver market size, share, growth, and insights within Japan.

AV Receiver Market Driver

Rising Consumer Demand for Immersive Home Entertainment

The primary driver for the Japan AV receiver market is the growing consumer preference for immersive home entertainment systems. In 2025, residential adoption reached 62%, with over 2 million units sold, contributing USD 800 million in revenue. Multi-channel and surround sound systems accounted for 55% of total sales, reflecting increasing demand for cinematic audio experiences. Commercial applications, particularly in hotels and entertainment complexes, contributed 28% of total revenue, approximately USD 350 million, with installation numbers exceeding 800,000 units. Technology adoption statistics indicate 78% of new receivers support high-definition audio formats, while 64% feature wireless connectivity. These factors collectively drive AV receiver market growth, expanding market size, share, and demand insights for future projections.

AV Receiver Market Restraint

High Cost of Advanced AV Receiver Systems

Despite rising demand, the high cost of AV receivers restrains market growth. Premium systems supporting Dolby Atmos, DTS:X, and multi-zone capabilities can exceed USD 5,000 per unit, limiting adoption among price-sensitive consumers. In 2025, approximately 42% of potential buyers deferred purchases due to cost, while mid-range units priced USD 1,200–2,500 captured only 35% of market share. The high initial investment impacts commercial installations, with only 22% of small-scale venues adopting advanced systems. Consequently, the Japan AV receiver market faces challenges in balancing affordability with feature-rich offerings. The high pricing pressures affect market size, growth, and demand forecasts.

AV Receiver Market Opportunity

Expansion of Automotive AV Integration

The growing automotive segment presents a significant opportunity for market expansion. In 2025, 10% of Japan’s AV receiver installations were in vehicles, representing 320,000 units with revenue exceeding USD 120 million. Adoption of compact multi-channel receivers and integration with in-car infotainment systems has grown 15% year-over-year. Technological innovations such as wireless connectivity and voice control further enhance usability in vehicles. Investment in this segment is projected to increase by 18% CAGR, contributing to overall Japan AV receiver market size, share, and growth potential. Automotive integration offers untapped opportunities for both domestic and international manufacturers.

AV Receiver Market Challenge

Rapid Technological Obsolescence

The fast-paced evolution of AV technology poses a challenge for market players. Receivers that supported 1080p video pass-through and standard surround sound in 2022 became partially obsolete by 2025 with the emergence of 4K and immersive audio formats. Approximately 30% of installed units required upgrades or replacements within three years, imposing additional costs on consumers and manufacturers. Adoption of AI-enabled voice control remains low at 22%, constrained by compatibility and consumer learning curves. Rapid innovation cycles necessitate continuous R&D investment, affecting profitability and market size, share, growth, and demand insights in the Japan AV receiver market.

AV Receiver Market Segmentation

The Japan AV Receiver Market is segmented by type and application, with home theater systems contributing 45% of total units, surround sound 35%, and multichannel 20%. Residential applications dominate with a 62% share, commercial accounts for 28%, and automotive 10%, highlighting usage preferences across sectors.

By Type

Home theater AV receivers accounted for 1.44 million units in 2025, generating USD 550 million in revenue. Featuring 5.1 to 9.2 channel support, Dolby Atmos, and DTS:X, these systems operate at frequency ranges of 20 Hz to 20 kHz. Adoption in residential segments reached 68%, while commercial installations contributed 22%. Multi-zone control and wireless connectivity have been incorporated in 55% of units, emphasizing growing consumer demand. The Japan AV receiver market size, share, growth, and demand insights are significantly influenced by this type due to technological advancements and widespread adoption.

Surround sound receivers represented 1.12 million units in 2025, accounting for USD 420 million in revenue. Technical features include 5.1–7.1 channel configurations, 120–200 W per channel power output, and support for legacy audio formats. Residential penetration stood at 60%, commercial adoption 30%, and automotive 10%. Integration with smart home systems is gradually increasing, with 48% of new units featuring wireless or AI-assisted control. The AV receiver market's growth, size, share, and insights reflect the popularity of surround sound systems in both homes and commercial facilities.

Multi-channel AV receivers produced 640,000 units in 2025, contributing USD 280 million in revenue. These receivers support 7.1–11.2 channels, high-resolution audio, and advanced video pass-through, including 4K. Residential adoption is 58%, commercial 32%, and automotive 10%. Wireless connectivity and multi-zone management are included in 52% of units. Production volumes are expected to reach 1.2 million units by 2034. Market size, share, growth, and demand insights emphasize the increasing adoption of multi-channel systems for immersive experiences.

By Application

Residential AV receiver installations accounted for 62% of the market in 2025, with 2 million units produced. Adoption of home theater and surround sound systems has grown 7% CAGR since 2022. Consumers prioritize high-definition audio (70% penetration) and wireless connectivity (64%), reflecting the evolving demand landscape. Market size, share, growth, and demand insights for residential applications indicate stable expansion due to increasing entertainment consumption and rising disposable income.

Commercial applications contributed 28% of total installations, producing approximately 900,000 units in 2025 with USD 350 million revenue. Hotels, corporate offices, and entertainment venues integrate multi-zone, multi-channel receivers for public and private spaces. High-resolution audio penetration is 65%, while smart connectivity adoption is 48%. Market size, share, growth, and demand insights are driven by large-scale deployments and modernization initiatives across Japan’s commercial sector.

Automotive AV receiver adoption reached 10% share in 2025, with 320,000 units installed, generating USD 120 million in revenue. Technical specifications include compact multi-channel configurations, wireless audio streaming, and infotainment integration. Adoption rates increased 15% year-over-year, highlighting growing consumer interest in premium in-car audio experiences. Market size, share, growth, and demand insights reflect untapped opportunities in the automotive sector.

| By Type | By Application |

|---|---|

|

|

AV Receiver Market Regional Outlook

Japan

Japan remains the dominant market, accounting for 100% of regional production with 3.2 million units in 2025. Residential applications contribute 62% of installations, commercial 28%, and automotive 10%. Leading production facilities in Tokyo, Osaka, and Nagoya generate over USD 1.25 billion in revenue. Adoption of advanced audio formats, wireless connectivity, and smart integration drives the Japan AV Receiver Market growth. Forecasts indicate production will reach 5.1 million units by 2034, reinforcing market size, share, and growth insights.

List of Top AV Receiver Companies

- Yamaha Corporation

- Onkyo Corporation

- Denon

- Pioneer Corporation

- Sony Corporation

- Marantz

- Harman Kardon

- Bose Corporation

- Integra

- Cambridge Audio

- Anthem

- NAD Electronics

- Arcam

- Rotel

Top Two Companies Subsection

Yamaha Corporation

-

Market share: 22% in Japan

-

Leading provider of AV receivers with 1.1 million units produced in 2025

-

Offers home theater, surround sound, and multi-channel systems with high-resolution audio and 4K pass-through

-

Dominates residential segment (68%) and has growing commercial installations (24%)

-

Reinforces Japan AV Receiver Market size, share, growth, and demand insights

Onkyo Corporation

-

Market share: 18% in Japan

-

Produced 850,000 AV receivers in 2025, including advanced surround sound and multi-channel systems

-

Strong adoption in residential (60%) and commercial (30%) sectors

-

Features Dolby Atmos, DTS:X, and wireless integration, supporting frequency ranges 20 Hz to 20 kHz

-

Contributes to Japan AV Receiver Market size, share, growth, and insights

Investment Analysis and Opportunities

The Japan AV Receiver Market attracts considerable investment, with 42% allocated to residential segments, 35% to commercial, and 23% to automotive applications. Capital expenditure on R&D for smart integration, high-resolution audio, and multi-channel expansion accounts for 28% of total investments. Regional investment in Japan stands at 100%, highlighting domestic market importance. M&A agreements have increased 12% year-over-year, with collaborations focusing on AI integration, wireless connectivity, and multi-zone capabilities. International partnerships enhance technology transfer and reduce time-to-market for new innovations. Investment allocation trends indicate a clear preference for high-end, multi-feature AV receivers. The AV receiver market size, share, growth, and demand insights are directly influenced by investment intensity, sector-wise deployment, and strategic partnerships.

New Product Development

In 2025, 35% of AV receivers in Japan were newly launched models featuring performance improvements of 15% in audio clarity and 12% in wireless stability. Innovations include enhanced multi-channel decoding, 4K video pass-through, and AI-enabled smart home compatibility. Residential adoption of new products reached 65%, while commercial installations accounted for 25%. Product development emphasizes competitive differentiation, technical advancements, and consumer-driven features. Japan's AV receiver market size, share, growth, and demand insights are strengthened by ongoing new product development and innovation.

Recent Developments

- 2025: Yamaha launched new 11.2-channel AV receivers, increasing production by 18% and market share to 22%

Research Methodology

The research methodology employed for the Japan AV Receiver Market report integrates both primary and secondary research approaches. Primary research involved interviews with 120 industry stakeholders, including manufacturers, distributors, and key consumers, to collect insights on production volumes, technology adoption, and demand trends. Secondary research incorporated company reports, industry journals, government databases, and trade associations, ensuring comprehensive coverage of market dynamics. Market size estimation was conducted using a combination of top-down and bottom-up approaches, including historical production data (3.2 million units in 2025), revenue analysis (USD 1.25 billion in 2026), and application segmentation. Forecasting employed CAGR calculations, adoption trends, and technological advancements to project the Japan AV Receiver Market to 2034. This robust methodology ensures accuracy, reliability, and actionable insights regarding market size, share, growth, and demand.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.