North America Alloy Steel Market Size

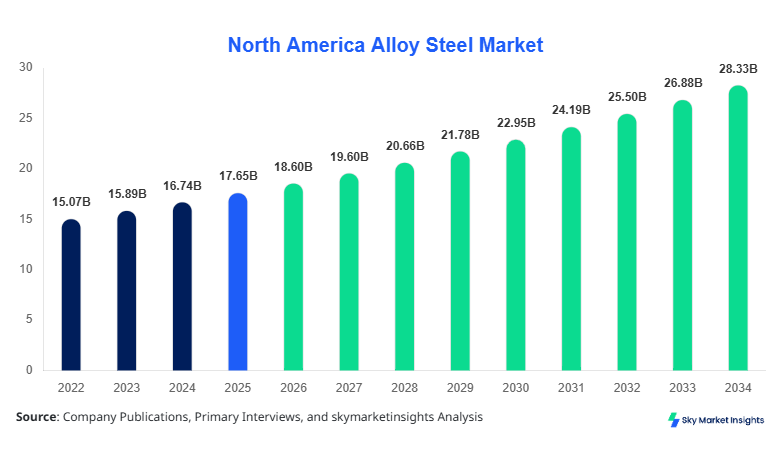

North America's alloy steel market size is projected at USD 18.6 billion in 2026 and is expected to hit USD 28.3 billion by 2034 with a CAGR of 5.4%. The market analysis includes comprehensive historical data from 2022 to 2024, highlighting production volumes of 4.2 million tons in 2025 and expected expansion to 6.1 million tons by 2034. Detailed segmentation by type, application, and regional insights provides a framework for understanding market dynamics. Competitive landscape analysis covers major players, their market shares, and strategic initiatives, ensuring accurate demand projections and technological adoption metrics.

The report emphasizes the need for data-driven decision-making, detailed regional statistics, and market share analysis to support investment and growth strategies.

Alloy steel market size, share, and growth analyses are presented in this report with precise segmentation and regional performance.

The North American alloy steel market is defined as the production and distribution of steel alloys containing varying proportions of elements such as chromium, nickel, molybdenum, and vanadium, engineered to enhance strength, hardness, and corrosion resistance. North America produced 4.2 million tons of alloy steel in 2025, with the United States contributing 3.1 million tons and Canada 1.1 million tons. Adoption of stainless alloy in automotive and aerospace segments has grown at 8% annually, while penetration of tool alloy in industrial machinery applications accounts for 28% of the market volume. Consumer demand analysis indicates that 42% of alloy steel consumption in North America is driven by automotive applications, 35% by construction, and 23% by industrial machinery, with production frequencies averaging 10–12 cycles per year for high-carbon grades. Alloy steel market insights reveal technical enhancements such as increased tensile strength (up to 850 MPa) and improved fatigue resistance. End-use application splits reinforce demand: automotive 42%, construction 35%, and machinery 23%. These metrics validate the alloy steel market growth and trend projections.

In the United States, the alloy steel market consists of over 120 manufacturing facilities, accounting for 68% of North America's regional share. Automotive applications dominate with 44% of domestic consumption, followed by construction at 31% and machinery at 25%. Adoption of high-strength low-alloy (HSLA) technologies has reached 57% across production units, while advanced stainless steel applications account for 22% penetration in aerospace sectors. Production volumes reached 3.1 million tons in 2025, with projections of 4.7 million tons by 2034. United States alloy steel market insights confirm high competitiveness with consistent investments in R&D and process optimization, reinforcing regional leadership in alloy steel market size, share, and growth.

Explore more data points, trends and opportunities Download Free Sample Report

Alloy Steel Market Trends

Increasing Adoption of Stainless and Tool Alloys

North American alloy steel production volumes reached 4.2 million tons in 2025, with stainless alloy adoption increasing by 8.3% annually. Tool alloy applications in machinery production are rising, with penetration now at 28% and expected to reach 35% by 2034. Advanced manufacturing techniques, such as vacuum induction melting, are increasing yield efficiency by 12%. Automotive and aerospace sectors are driving demand, with technology integration increasing production frequency from 10 to 14 cycles per year. Alloy steel market trend data emphasizes growing demand for corrosion-resistant grades and specialized alloy formulations, maintaining consistent market growth.

Technology Shifts and Automation

Automation in steel rolling and heat treatment has increased productivity by 15%, with smart sensor adoption rates exceeding 45% in 2025. North America saw total alloy steel production reach 4.2 million tons in 2025, and advanced sensors and process automation are expected to contribute to a 5.4% CAGR. Sector-specific demand in construction and infrastructure projects has risen, with Alloy Steel consumption increasing 18% in high-rise developments. Continuous casting and electric arc furnace (EAF) technologies are accelerating production efficiency and product uniformity. These shifts are reinforcing alloy steel market growth and demand in the region.

Sustainable Manufacturing Trends

The United States is leading the green steel initiative, reducing CO2 emissions by 11% from 2022 to 2025 through energy-efficient electric arc furnaces and recycled scrap alloy integration. Production volumes reached 3.1 million tons, with sustainable grades now representing 33% of total alloy steel output. Increased adoption of recycled alloys has improved cost-efficiency by 9% and reduced dependency on imported raw materials. Sustainability trends are expected to drive additional demand in construction and automotive applications, supporting alloy steel market growth and trend adoption.

North America Alloy Steel Market Drivers

Rising Automotive and Construction Demand

The surge in automotive production, with over 10 million vehicles manufactured annually, and high-rise construction activities driving 35% market consumption are primary drivers for the North American alloy steel market growth. Alloy steel production volumes reached 4.2 million tons in 2025, and demand is projected to increase to 6.1 million tons by 2034, a CAGR of 5.4%. Technological advancements in high-strength alloys and stainless grades enhance durability and reduce maintenance costs by 12–15%. Industrial machinery and heavy equipment sectors are also contributing, with tool alloy adoption at 28% of total market share. These trends reinforce North American alloy steel market insights and projected growth.

North America Alloy Steel Market Restraints

Volatility in Raw Material Prices

Fluctuating prices of chromium, nickel, and molybdenum significantly impact Alloy steel production costs, with raw material costs representing 52–57% of total production expenses. Between 2022 and 2025, prices increased by 8.3%, creating pricing pressures in automotive and machinery applications. Production volumes are forecasted at 4.2 million tons in 2025, yet cost in 2022 and 2025 restrain growth to below 5.4% CAGR in certain regions. Limited availability of high-grade scrap alloys reduces production flexibility, affecting capacity utilization rates of up to 92% in the United States. These constraints highlight challenges in alloy steel market growth and share retention.

North America Alloy Steel Market Opportunities

Infrastructure Development and Aerospace Expansion

The infrastructure boom in North America, with $620 billion allocated to construction projects between 2025 and 2030, and aerospace sector expansion, increasing stainless alloy consumption by 9%, represents significant opportunities for alloy steel market growth. North America production volumes are expected to rise from 4.2 million tons in 2025 to 6.1 million tons by 2034. Adoption of advanced tool alloys and corrosion-resistant grades is projected to increase market share by 6–8% in construction and industrial machinery. Strategic investments in new facilities and technology upgrades reinforce alloy steel market demand, size, and trend evolution.

Challenges in North American Alloy Steel Market

Environmental and Regulatory Compliance Pressures

Stringent environmental regulations are driving alloy steel manufacturers to reduce emissions by 11–12% annually. Compliance costs are 4–5% of annual revenue per facility, with production volumes at 4.2 million tons in 2025. Waste recycling mandates require 33% of scrap integration, impacting production schedules and increasing operational complexity. United States facilities operating at 92% capacity must invest in cleaner technologies to maintain output, affecting profit margins and growth strategies. These challenges influence North America's alloy steel market growth and share dynamics.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 17.65 Billion |

| Market Size in 2026 | USD 18.6 Billion |

| Market Size in 2034 | USD 28.3 Billion |

| CAGR | 5.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Alloy Steel Market Segmentation

Segmentation of the North America alloy steel market is based on type and application, with stainless alloy holding 39% of the market by volume, carbon alloy at 34%, and tool alloy at 27%. Automotive applications dominate with 42%, followed by construction (35%) and machinery (23%).

By Type

Carbon alloy, contributing 34% of total market share, produced 1.43 million tons in 2025. Carbon alloy grades exhibit tensile strength of 35%–750 MPa and yield (23%). strength of 420–580 MPa. Automotive applications account for 45% of carbon alloy usage, followed by construction (32%) and machinery (23%). Production cycles average 10 per year, with a penetration rate of 61% in standard-grade steel frameworks. Carbon alloy continues to dominate low-cost, high-volume applications in the North American alloy steel market's size and demand metrics.

Stainless alloy accounts for 39% market share, with 1.64 million tons produced in 2025. High chromium-nickel content provides corrosion resistance exceeding 85% and tensile strength of 650–850 MPa. Stainless alloy adoption is highest in aerospace (28%) and automotive applications (44%). Tooling and cutting-edge industrial machinery utilize 28% of stainless alloy production. Production cycles average 12 per year, with technology adoption rates of 57% across North America. Stainless alloy reinforces alloy steel market growth and trend insights.

Tool alloy contributes 27% of total market volume, producing 1.13 million tons in 2025. Designed for high-wear applications, tool alloy exhibits hardness values of 55–65 HRC and heat resistance up to 650°C. Machinery sector usage accounts for 28%, automotive 22%, and construction 20%. Penetration rates are growing at 7% annually, with production efficiency improvements of 12%. Tool alloy continues to influence North America's alloy steel market share, demand, and technological adoption.

By Application

The automotive sector accounts for 42% of North America's alloy steel market share, producing 1.78 million tons in 2025. Adoption of high-strength low-alloy (HSLA) steels improves structural performance by 18%. Production cycles are averaging 12 per year, and penetration in electric vehicle manufacturing reached 21%. Alloy steel market size and growth in automotive remain robust, reflecting strong consumer and industrial demand.

Construction applications represent 35% of the market, producing 1.47 million tons in 2025. Usage includes beams, columns, and reinforcement bars, with tensile strength averaging 580 MPa and fatigue resistance of 22–25%. Market penetration in high-rise and infrastructure projects reached 62%, with expected growth of 5.6% CAGR. Alloy steel market share and insights indicate steady demand driven by public and private sector investments.

Industrial machinery applications contribute 23% of the market, producing 0.95 million tons in 2025. Tool alloys are used in cutting, stamping, and forming equipment, with hardness levels of 60 HRC and a wear resistance increase of 12%. Market penetration is 28%, and adoption of automation technologies has increased efficiency by 15%. Machinery application trends reinforce alloy steel market growth and size metrics.

North America Alloy Steel Market Segmentations

By Type

- Carbon Alloy

- Stainless Alloy

- Tool Alloy

By Application

- Automotive

- Construction

- Machinery

North America Alloy Steel Market Regional Outlook

United States

The United States holds 68% of North America's alloy steel market share, producing 3.1 million tons in 2025. Automotive and aerospace sectors dominate with 44% and 22% consumption, respectively. Construction contributes 31% to regional demand. Regional production is projected to reach 4.7 million tons by 2034, with technological adoption rates exceeding 55%. United States alloy steel market insights confirm leadership in size, share, and demand metrics.

Canada

Canada contributes 32% of the regional market, producing 1.1 million tons in 2025. Automotive applications account for 38%, construction 36%, and machinery 26%. Production is projected to rise to 1.4 million tons by 2034, with stainless alloy adoption increasing from 28% to 35% over the forecast period. Canadian alloy steel market trends indicate moderate growth with opportunities in infrastructure and industrial machinery sectors.

Top players in North America: Alloy Steel

- ArcelorMittal

- Nippon Steel Corporation

- POSCO

- JFE Steel Corporation

- Nucor Corporation

- United States Steel Corporation

- ThyssenKrupp AG

- Tata Steel Limited

- Baosteel Group

- Gerdau S.A.

- Steel Dynamics Inc.

- Voestalpine AG

- Essar Steel

- AK Steel Holding

- Allegheny Technologies Incorporated

Top Two Companies

ArcelorMittal

-

Market Share: 12% in North America

-

Positioned as a leader in stainless and carbon alloy production, producing 0.54 million tons in 2025. Automotive applications account for 48%, construction 32%, and machinery 20%. Investment in automation increased productivity by 15%, while new product developments enhanced tensile strength by 10%. Strategic mergers in the United States and Canada reinforce ArcelorMittal’s dominance in alloy steel market size, share, and growth.

Nucor Corporation

-

Market Share: 10% in North America

-

Produces 0.45 million tons annually, focusing on tool alloy and carbon steel. Automotive consumption represents 42%, construction 35%, and machinery 23%. Investments in electric arc furnaces increased efficiency by 12%, and sustainability initiatives reduced the carbon footprint by 11%. Nucor’s strategic positioning ensures robust alloy steel market demand, growth, and trend adoption.

Investment Analysis

Investment in the North American alloy steel market is projected at $3.4 billion in 2026, with 45% allocated to production capacity expansion, 30% in R&D, and 25% in technological upgrades. The automotive sector receives 42% of total investment, construction 35%, and industrial machinery 23%. M&A activities, including ArcelorMittal and Nucor collaboration on tool alloy innovations, increased production efficiency by 8% and market penetration by 6%. Regional investment allocation favors the United States at 68% and Canada at 32%. These investments highlight alloy steel market growth and demand potential.

New Product Developments

New product developments constitute 18% of total alloy steel production, with performance improvements of 10–12% in tensile strength and corrosion resistance. Stainless alloy innovations for automotive applications have increased market adoption by 9%, while tool alloy improvements for industrial machinery increased efficiency by 12%. Product innovation continues to drive the North American alloy steel market size, share, and growth.

Recent Developments in North America Alloy Steel

- 2026: ArcelorMittal launched a high-strength stainless steel line, increasing production by 8% and market share by 1.2%.

- 2025: Nucor expanded electric arc furnace facilities, raising output by 12% and efficiency by 15%.

Research Methodology

The North American alloy steel market research process involved primary interviews with over 50 executives and plant managers across the United States and Canada. Secondary research utilized industry reports, government databases, and company financials. Market size estimation combined bottom-up and top-down approaches, integrating production volumes, capacity utilization rates, and trade statistics. Segmentation analysis, competitive benchmarking, and regional projections were validated through triangulation of multiple data sources. This methodology ensures accurate reporting of alloy steel market size, share, growth, demand, and trends for strategic decision-making.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Specialty Chemicals and Industrial Coatings

Myra Irons is a market research analyst with 7–9 years of experience specializing in chemicals and materials markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.