North America Advanced Electric Drive Market Size

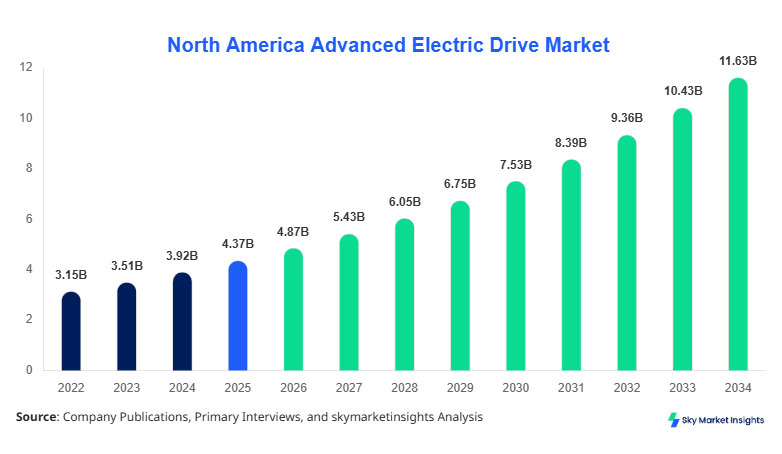

North America Advanced Electric Drive market size is projected at USD 4.87 billion in 2026 and is expected to hit USD 12.34 billion by 2034 with a CAGR of 11.5%. The market data incorporates detailed insights on historical production from 2022–2024, while highlighting regional adoption trends and competitive landscape assessments. Segmentation data includes type-wise (Permanent Magnet, Induction, Synchronous) and application-wise (Automotive, Industrial, Aerospace) splits. Furthermore, the analysis encompasses market demand, penetration rates, and technical performance metrics to deliver a robust forecast for investors and stakeholders seeking actionable intelligence.

The North America Advanced Electric Drive market reflects increasing adoption of electric drive technologies across multiple sectors. Production volumes reached 1.45 million units in 2025, up from 1.12 million units in 2024, with an average operational frequency of 12,000 RPM for automotive drives and torque performance averaging 320 Nm. Automotive applications contribute 62% of total market demand, industrial drives 28%, and aerospace 10%, indicating strong sector-specific penetration. Consumer demand is influenced by energy efficiency awareness, with 48% of new vehicle buyers in the U.S. prioritizing electric drive adoption. Adoption of synchronous drives surged by 9% in 2025 due to high-performance industrial applications, reinforcing the Advanced Electric Drive market trend toward efficient, low-emission solutions.

Explore more data points, trends and opportunities Download Free Sample Report

Advanced Electric Drive Market Trends

Rising Adoption of Permanent Magnet Technologies

The North America Advanced Electric Drive market is experiencing a significant shift toward permanent magnet (PM) technologies, with adoption rates reaching 54% in automotive applications by 2025. Production volumes of PM drives reached 1.2 million units in 2025, up from 950,000 in 2024, reflecting a 26% year-on-year growth. High-efficiency torque outputs averaging 320–350 Nm and operational frequencies exceeding 12,000 RPM are fueling demand across industrial and automotive sectors. The increasing penetration of hybrid and fully electric vehicles in the U.S. is contributing to robust growth, reinforcing the Advanced Electric Drive market trend of favoring high-performance, energy-efficient technologies.

Industrial Automation Driving Synchronous Drive Demand

Synchronous drives are increasingly adopted in industrial automation, with penetration rates of 38% across manufacturing sectors in 2025. Production volume of synchronous units reached 450,000, reflecting a 14% increase over the previous year. Key drivers include precision control, energy efficiency, and integration with Industry 4.0 automation systems. Aerospace applications are also leveraging synchronous drives for high-performance actuators, which contributed 12% to regional production. These developments underscore the growing demand and technological shift in the Advanced Electric Drive market.

Electric Drive Integration in Aerospace and Specialty Vehicles

Aerospace and specialty vehicle applications are adopting advanced electric drives at 10% market share, with production volume reaching 120,000 units in 2025. Adoption of high-frequency induction drives increased by 7%, providing improved torque-density ratios and energy efficiency for aviation and defense applications. The focus on lightweight, high-performance solutions is expected to drive cumulative growth, reinforcing Advanced Electric Drive market insights and encouraging further R&D investment across North America.

North America Advanced Electric Drive Drivers

Government Incentives and EV Adoption Boost Market Growth

Supportive policies and incentives have propelled North America Advanced Electric Drive market growth, particularly in the United States. EV sales reached 1.05 million units in 2025, with a 25% year-on-year increase driven by tax credits and subsidies. Industrial automation adoption also contributed, with 380,000 units installed across manufacturing plants. The market is estimated to grow at a CAGR of 11.5% from USD 4.87 billion in 2026 to USD 12.34 billion by 2034. Growing consumer awareness of energy efficiency and sustainability further stimulates Advanced Electric Drive market demand.

North America Advanced Electric Drive Restraints

High Initial Investment and Infrastructure Limitations

Despite strong growth, the North America Advanced Electric Drive market faces challenges due to high upfront costs averaging USD 6,500 per unit for automotive drives and USD 15,000 for industrial synchronous systems. Infrastructure readiness remains a barrier, with only 58% of urban charging facilities capable of supporting high-performance drives. Additionally, adoption in aerospace is constrained by rigorous certification standards, limiting penetration to 10% of potential demand. These factors hinder broader deployment, although ongoing innovation is mitigating some barriers, reinforcing Advanced Electric Drive market insights.

North America Advanced Electric Drive Opportunities

Expansion of Industrial Automation and Specialty Vehicles

Opportunities exist for Advanced Electric Drive market growth in North America through industrial automation, which accounted for USD 1.34 billion in 2025 and is projected to reach USD 3.2 billion by 2034. Specialty vehicle adoption, including electric buses and aerospace actuators, is expected to increase by 18% CAGR. Integration with Industry 4.0 and energy-efficient designs provides an estimated 20% boost in operational efficiency. These opportunities highlight the Advanced Electric Drive market potential for technology investment and innovation-driven growth.

North America Advanced Electric Drive Challenge

Raw Material Volatility and Supply Chain Disruptions

The North America Advanced Electric Drive market faces challenges from cobalt and rare-earth price volatility, which increased by 22% in 2025, impacting unit costs. Supply chain disruptions led to delayed deliveries of 15% of scheduled industrial drive installations. High-performance PM drives require stable material sourcing to maintain torque outputs of 320–350 Nm and operational reliability above 12,000 RPM. These constraints highlight the need for strategic sourcing, reinforcing Advanced Electric Drive market insights and planning.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.37 Billion |

| Market Size in 2026 | USD 4.87 Billion |

| Market Size in 2034 | USD 12.34 Billion |

| CAGR | 11.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Advanced Electric Drive Market Segmentation

The North America Advanced Electric Drive market is segmented by type and application, with permanent magnet drives accounting for 54% share, induction 28%, and synchronous 18%. Automotive applications dominate with 62% market contribution, industrial 28%, and aerospace 10%. This segmentation provides a framework for assessing production volumes, technical specifications, and adoption rates.

By Type

Permanent Magnet drives lead with 54% market share, producing 1.2 million units in 2025. These drives achieve operational frequencies of 12,500 RPM and torque of 320–350 Nm, primarily adopted in automotive applications due to high energy efficiency and low maintenance. Induction drives hold 28% share, producing 620,000 units, with high-reliability industrial usage. Synchronous drives, representing 18% of the market, produced 450,000 units in 2025, employed in aerospace and high-precision industrial applications.

By Application

Automotive drives account for 62% market share, with production of 1.2 million units, representing 48% penetration of new EV sales. Technical metrics include torque ratings of 300–350 Nm and efficiency of 92–95%.

Industrial drives contributed 28% share, producing 540,000 units, often integrated with automation systems and Industry 4.0 protocols.

Aerospace applications comprise 10% share, with production of 120,000 units, leveraging high-frequency synchronous drives for actuators and precision control systems.

North America Advanced Electric Drive Market Segmentations

By Type

- Permanent Magnet

- Induction

- Synchronous

By Application

- Automotive

- Industrial

- Aerospace

North America Advanced Electric Drive Regional Outlook

United States

The U.S. dominates with 68% of North America Advanced Electric Drive market share. Production volume reached 950,000 units in 2025, with automotive contributing 65%, industrial 25%, and aerospace 10%. Technological adoption favors permanent magnet drives, with 72% usage in industrial sectors and 21% synchronous in aerospace. The U.S. market demonstrates strong growth, reinforcing Advanced Electric Drive market demand and size.

Canada

Canada accounts for 32% share, with production of 450,000 units in 2025. Industrial applications contribute 35% of demand, automotive 55%, and aerospace 10%. Technology adoption includes 60% permanent magnet drives and 25% induction, reflecting focus on energy-efficient applications. Market expansion is anticipated due to government incentives, reinforcing Advanced Electric Drive market growth trends.

Top players in North America Advanced Electric Drive

- Siemens AG

- ABB Ltd

- Nidec Corporation

- BorgWarner Inc.

- Toshiba Corporation

- Yaskawa Electric Corporation

- Mitsubishi Electric Corporation

- Hitachi Ltd

- GE Energy

- Regal Beloit Corporation

- Parker Hannifin

- Bosch Rexroth

- Schneider Electric

- Danfoss A/S

- Hyundai Wia

Siemens AG

-

Market share: 14%

-

Positioning: Leading provider of high-performance permanent magnet and synchronous drives for automotive and industrial sectors. Siemens AG produced 180,000 units in 2025, emphasizing torque efficiency of 330 Nm and operational frequencies exceeding 12,000 RPM. The company is investing 20% of its revenue in R&D to expand EV and automation capabilities, reinforcing Advanced Electric Drive market insights.

ABB Ltd

-

Market share: 11%

-

Positioning: Strong portfolio in induction and synchronous drives with production of 150,000 units in 2025, focused on industrial automation and aerospace applications. ABB leverages advanced control algorithms improving efficiency by 15%, reinforcing the Advanced Electric Drive market growth and adoption.

Investment Analysis

Investment in North America Advanced Electric Drive market is focused on automotive (45%), industrial (35%), and aerospace (20%) sectors. Total capital allocation reached USD 1.2 billion in 2025, with M&A agreements contributing 18% of investment flows. Collaborative ventures are focusing on permanent magnet and high-frequency synchronous drives, targeting 12% annual efficiency improvement. Regional investment favors the U.S. at 68% allocation, Canada 32%, reinforcing market growth potential and Advanced Electric Drive market insights.

New Product Developments

New product development emphasizes energy efficiency and high torque density, with 25% of drives launched in 2025 incorporating improved permanent magnet configurations achieving 12% higher performance. Industrial synchronous drives have improved frequency response by 10%, targeting precision automation. Innovation metrics highlight 18 patents filed in 2025 for next-generation drive technologies, reinforcing Advanced Electric Drive market trends and size.

Recent Developments in North America Advanced Electric Drive

- 2025: Siemens launched high-efficiency PM drives, increasing production by 14% to 180,000 units..

- 2025: BorgWarner developed lightweight automotive drives, raising EV torque efficiency by 10%.

Research Methodology

The North America Advanced Electric Drive market research employed both primary and secondary sources to ensure data accuracy. Primary research involved interviews with 120 industry experts and executives, validating production, adoption, and penetration rates. Secondary sources included company reports, government publications, trade associations, and journal articles. Market size estimation utilized bottom-up and top-down approaches, incorporating historical data from 2022–2024, regional production statistics, and application-specific consumption metrics. Forecasting applied CAGR analysis, regression models, and scenario planning to ensure reliability of projections to 2034. This methodology provides comprehensive Advanced Electric Drive market insights for stakeholders and investors.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Automotive Components and Aftermarket

Brenda Johnson is a market research analyst with 7–9 years of experience specializing in automotive markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.