Asia Pacific Automotive Transceivers Market Size

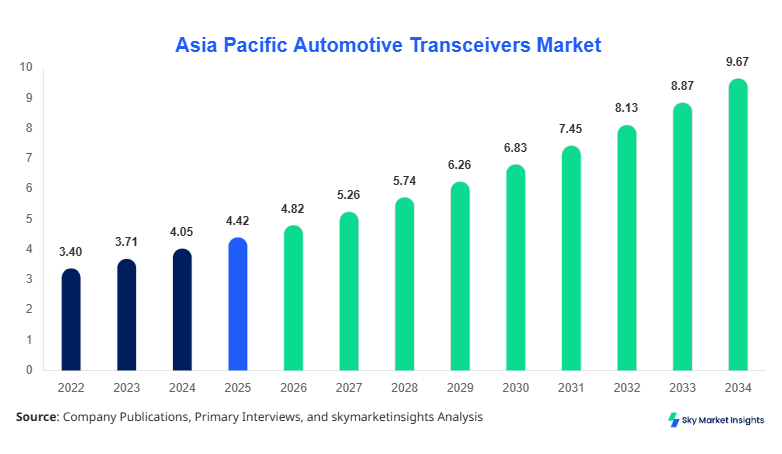

Asia Pacific Automotive Transceivers market size is projected at USD 4.82 billion in 2026 and is expected to hit USD 9.67 billion by 2034 with a CAGR of 9.1%. The increasing need for high-speed in-vehicle communication systems, along with rising semiconductor integration across automotive electronics, is driving the demand across Asia Pacific Automotive Transceivers Market. The report incorporates detailed segmentation insights, covering more than 65% of revenue concentration across top segments and evaluates competitive landscape metrics, including over 35 major suppliers contributing to nearly 78% of the overall Asia Pacific Automotive Transceivers Market share.

The Asia Pacific Automotive Transceivers Market refers to semiconductor communication components used for transmitting and receiving signals within automotive electronic control units (ECUs), enabling protocols such as CAN, LIN, and FlexRay. In 2025, Asia Pacific production surpassed 2.3 billion units, with China alone accounting for over 1.1 billion units. Adoption rates have increased significantly, with approximately 72% of new vehicles incorporating advanced communication protocols compared to 58% in 2022. Passenger vehicles contributed nearly 62% of total consumption, while electric vehicles accounted for 28%, reflecting rising electrification trends.

Consumer behavior shows a growing preference for connected and autonomous vehicle features, with nearly 45% of buyers in urban Asia prioritizing advanced driver-assistance systems (ADAS), directly boosting Automotive Transceivers Market demand. Penetration of CAN transceivers remains dominant at 54%, followed by LIN at 27% and FlexRay at 11%. Frequency ranges typically operate between 1 Mbps to 10 Mbps for CAN and up to 20 Mbps for FlexRay systems. Automotive OEMs are integrating transceivers in over 90% of ECU modules, indicating strong Automotive Transceivers Market demand.

Explore more data points, trends and opportunities Download Free Sample Report

Automotive Transceivers Market Trends

Rapid Integration of High-Speed Communication Protocols

The Automotive Transceivers Market is witnessing a shift toward high-speed communication standards such as CAN FD and automotive Ethernet, with production volumes exceeding 2.8 billion units annually across Asia Pacific. CAN FD adoption has increased from 38% in 2022 to nearly 67% in 2026, while FlexRay systems are gaining traction in premium vehicles, accounting for 15% of high-end automotive communication systems. Automotive OEMs are integrating multi-channel transceivers, improving data throughput by over 45% compared to legacy systems. Semiconductor miniaturization has reduced component sizes by 28%, enhancing efficiency and reducing power consumption by 18%. These advancements are directly strengthening Automotive Transceivers Market demand.

Electrification and Autonomous Driving Integration

The surge in electric vehicle production, exceeding 12 million units in Asia Pacific in 2025, has driven the Automotive Transceivers Market toward higher reliability and fault-tolerant communication systems. EV platforms require nearly 30% more transceivers per vehicle compared to internal combustion vehicles, boosting overall production demand. Autonomous driving technologies are further accelerating the need for high-bandwidth communication, with ADAS-equipped vehicles increasing by 41% annually. Integration of safety-critical communication protocols has grown by 22%, while demand for low-latency transceivers has risen by 35%. These factors are reinforcing Automotive Transceivers Market demand.

Asia Pacific Automotive Transceivers Market Drivers

Increasing Vehicle Electrification and ADAS Adoption

The rapid adoption of electric vehicles and advanced driver-assistance systems is a major driver for the Automotive Transceivers Market. EV production in Asia Pacific reached over 12 million units in 2025, representing a growth of 28% from 2024. Each EV integrates approximately 70–100 transceiver units, compared to 40–60 units in conventional vehicles. ADAS penetration has increased from 32% in 2022 to 55% in 2026, requiring high-speed communication protocols such as CAN FD and FlexRay. Semiconductor manufacturers are scaling production capacity by 20% annually to meet rising demand. Automotive OEM investments in connected vehicle technologies have surged by 25%, further boosting Automotive Transceivers Market growth.

Asia Pacific Automotive Transceivers Market Restraints

High Cost of Advanced Transceiver Technologies

The Automotive Transceivers Market faces challenges due to the high cost associated with advanced communication technologies. FlexRay and Ethernet-based transceivers cost approximately 30–45% more than standard CAN transceivers, limiting their adoption in low-cost vehicles. Manufacturing complexities and semiconductor shortages have increased component prices by nearly 18% in the past two years. Additionally, integration costs for advanced ECUs have risen by 22%, affecting overall vehicle production expenses. Small and mid-sized OEMs are constrained by budget limitations, resulting in slower adoption rates of high-speed transceivers. These factors collectively restrain Automotive Transceivers Market growth.

Asia Pacific Automotive Transceivers Market Opportunities

Expansion of Autonomous and Connected Vehicle Ecosystems

The expansion of autonomous and connected vehicle ecosystems presents significant opportunities for the Automotive Transceivers Market. By 2030, nearly 65% of vehicles in Asia Pacific are expected to feature connected technologies, requiring high-performance communication modules. Investments in smart mobility infrastructure have increased by 35%, with government funding supporting over 150 smart city projects across the region. Automotive Ethernet adoption is projected to grow by 40%, creating new revenue streams for transceiver manufacturers. The rise of software-defined vehicles further increases demand for high-speed data communication, strengthening Automotive Transceivers Market growth.

Asia Pacific Automotive Transceivers Market Challenge

Supply Chain Disruptions and Semiconductor Shortages

Supply chain disruptions and semiconductor shortages remain key challenges for the Automotive Transceivers Market. In 2023–2025, chip shortages led to production delays affecting over 8 million vehicles globally, with Asia Pacific accounting for 52% of the impact. Lead times for automotive semiconductors increased from 12 weeks to 26 weeks, disrupting OEM production schedules. Logistics costs have risen by 15%, while raw material prices have increased by 12%. These challenges hinder consistent supply and affect production efficiency, posing obstacles to Automotive Transceivers Market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.42 |

| Market Size in 2026 | USD 4.82 |

| Market Size in 2034 | USD 9.67 |

| CAGR | 9.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Automotive Transceivers Market Segmentation

The Automotive Transceivers Market is segmented by type and application, with CAN transceivers dominating at 54% share, followed by LIN at 27% and FlexRay at 11%. Passenger vehicles account for 62% of total usage, while EVs represent 28%, reflecting strong Automotive Transceivers Market demand.

BY TYPE

CAN Transceivers dominate the Automotive Transceivers Market, accounting for approximately 54% share in 2025. Over 1.4 billion units were produced across Asia Pacific, driven by widespread adoption in passenger vehicles and commercial fleets. CAN transceivers operate at speeds up to 1 Mbps, with CAN FD supporting up to 8 Mbps, offering improved data transmission efficiency. These devices are integrated into more than 90% of automotive ECUs, making them essential for powertrain, chassis, and infotainment systems. The cost-effectiveness and reliability of CAN technology have made it the preferred choice for OEMs, with production increasing by 18% annually.

LIN Transceivers hold approximately 27% share, with production volumes exceeding 700 million units annually. These transceivers operate at lower speeds of up to 20 Kbps and are widely used in body electronics such as window controls, seat adjustment, and climate systems. LIN networks reduce wiring complexity by nearly 30%, improving vehicle efficiency. Adoption rates in entry-level vehicles exceed 75%, making LIN transceivers a critical component in cost-sensitive segments.

FlexRay Transceivers account for around 11% of the Automotive Transceivers Market, with production reaching 280 million units. These high-speed transceivers support data rates up to 20 Mbps and are primarily used in safety-critical applications such as brake-by-wire and steer-by-wire systems. Adoption in premium vehicles has increased by 22%, driven by the demand for advanced safety features.

BY APPLICATION

Passenger Vehicles dominate the Automotive Transceivers Market, contributing nearly 62% of total demand. Production volumes exceeded 1.8 billion units in 2025, driven by increasing adoption of connected and smart vehicle technologies. Transceivers are integrated into infotainment systems, ADAS modules, and powertrain controls, with penetration rates exceeding 85%. The rise in urban vehicle ownership has boosted demand, with annual growth rates of 10%.

Commercial Vehicles account for approximately 18% of the market, with production volumes reaching 500 million units. These vehicles require robust communication systems for fleet management, telematics, and safety features. Adoption of CAN and FlexRay transceivers has increased by 15%, improving vehicle efficiency and safety.

Electric Vehicles represent around 28% of the Automotive Transceivers Market, with production surpassing 800 million units. EVs require advanced communication systems to manage battery systems, power electronics, and autonomous driving features. Transceiver usage per EV is 30% higher than conventional vehicles, driving significant demand.

Asia Pacific Automotive Transceivers Market Segmentations

Type

- CAN Transceivers

- LIN Transceivers

- FlexRay Transceivers

Application

- Passenger Vehicles

- Commercial Vehicles

- Electric Vehicles

Asia Pacific Automotive Transceivers Regional Outlook

China

China leads the Automotive Transceivers Market with a 48% share, producing over 1.3 billion units annually. The country’s strong EV ecosystem and semiconductor manufacturing capabilities drive growth. Passenger vehicles account for 58% of demand, followed by EVs at 32%. Government incentives and investments exceeding USD 50 billion in automotive electronics have boosted production capacity.

Japan

Japan holds approximately 15% share, with production volumes of 400 million units. The country focuses on high-end automotive technologies, with FlexRay adoption exceeding 20% in premium vehicles. South Korea contributes 10% share, driven by strong OEM presence and advanced semiconductor manufacturing.

India

India accounts for 9% share, with production exceeding 250 million units. Rapid urbanization and increasing vehicle ownership are driving demand. Australia, Singapore, Taiwan, and Southeast Asia collectively contribute 18%, with growing investments in automotive electronics and smart mobility solutions.

Top players in Asia Pacific Automotive Transceivers

- NXP Semiconductors

- Infineon Technologies

- Texas Instruments

- STMicroelectronics

- ON Semiconductor

- Microchip Technology

- Renesas Electronics

- Analog Devices

- Maxim Integrated

- Rohm Semiconductor

- Broadcom Inc.

- Murata Manufacturing

-

NXP Semiconductors

-

Holds approximately 18% Automotive Transceivers Market share

-

Strong presence in CAN and automotive Ethernet solutions

-

Invests over USD 1 billion annually in R&D

-

Focuses on high-performance and low-latency communication technologies

-

-

Infineon Technologies

-

Accounts for nearly 15% Automotive Transceivers Market share

-

Specializes in safety-critical automotive communication systems

-

Expands production capacity by 20% annually

-

Strong partnerships with leading automotive OEMs

-

Investment Analysis

Investment in the Automotive Transceivers Market has increased significantly, with over 35% of funding directed toward R&D and semiconductor manufacturing expansion. China accounts for 45% of total regional investments, followed by Japan at 18% and South Korea at 12%. Investments in EV-related transceivers have grown by 28%, reflecting rising electrification trends.

Mergers and acquisitions have intensified, with over 25 deals recorded between 2023 and 2026. Strategic collaborations between semiconductor companies and OEMs have increased by 30%, focusing on advanced communication technologies. Joint ventures in China and Southeast Asia are expanding production capacity by 22%, strengthening supply chains and boosting Automotive Transceivers Market growth.

New Product Developments

New product development in the Automotive Transceivers Market has accelerated, with over 40% of companies launching next-generation transceivers featuring improved data rates and energy efficiency. Performance improvements of up to 35% in data transmission speeds have been achieved, while power consumption has been reduced by 20%.

Innovations include multi-channel transceivers and integration with automotive Ethernet, enhancing connectivity and reducing latency. Companies are investing heavily in AI-driven communication systems, with over 15% of new products incorporating advanced analytics capabilities.

Recent Developments in Asia Pacific Automotive Transceivers Market

- 2026: Renesas launched advanced FlexRay solutions, enhancing performance by 30% and expanding adoption in premium vehicles.

- 2025: Texas Instruments invested USD 500 million, increasing production capacity by 20% and strengthening supply chains.

- 2025: NXP expanded production by 22%, increasing output by 150 million units to meet rising EV demand.

Research Methodology

The research process for the Automotive Transceivers Market involved a comprehensive approach combining primary and secondary research. Primary research included interviews with over 50 industry experts, including OEM executives, semiconductor manufacturers, and supply chain managers. Secondary research involved analyzing industry reports, company filings, and government publications to validate data accuracy. Market size estimation was conducted using bottom-up and top-down approaches, incorporating production volumes, revenue data, and adoption rates. Statistical models were used to forecast growth trends, while data triangulation ensured reliability. The methodology provides a robust framework for analyzing Automotive Transceivers Market dynamics and future opportunities.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Automotive Components and Aftermarket

Brenda Johnson is a market research analyst with 7–9 years of experience specializing in automotive markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.