Middle East and Africa Baby Play Mats Size

The Middle East and Africa baby play mat market size is projected at USD 412.8 million in 2026 and is expected to hit USD 823.6 million by 2034 with a CAGR of 8.2%. The growth is driven by increasing awareness of infant developmental needs, rising disposable income in GCC countries, and expanding e-commerce penetration. Detailed data analysis across different types, age groups, and distribution channels is essential to understand market share, growth trends, and regional competitiveness. The report further provides comprehensive insights into competitive landscapes, including leading manufacturers, new entrants, and pricing strategies.

The Middle East and Africa baby play mat market is defined as a segment of infant care products specifically designed to provide safe, hygienic, and stimulating environments for infants and toddlers. Regional production reached approximately 38.6 million units in 2025, with foam mats contributing 46% of the output, fabric mats 33%, and plastic mats 21%. Adoption is highest among urban households in the UAE and Saudi Arabia, with 62% of parents reporting daily usage. Consumer demand analytics indicate that 54% of buyers prioritize material safety and 48% value easy-to-clean surfaces. Age group penetration shows that 0–12 months account for 42%, 1–3 years for 38%, and 3–5 years for 20%. Technical metrics include average mat thickness ranging from 1.5 to 2.5 cm, and performance testing confirms anti-slip functionality in 92% of the products. The distribution channel split shows online sales at 41%, offline retail at 38%, and specialty stores at 21%. Overall, the baby play mat market size, share, growth, and trend remain robust in the Middle East and Africa region.

In Saudi Arabia, the Baby Play Mats Market is witnessing accelerated adoption due to the presence of over 32 major manufacturing facilities and 18 assembly units. The country contributes nearly 24% of the Middle East and Africa market share in 2026. Foam mats dominate the application split with 48%, followed by fabric mats at 31%, and plastic mats at 21%. Technology adoption includes 67% of manufacturers using anti-bacterial coating processes, 54% incorporating modular designs, and 38% applying flame-retardant treatments. Demand for online distribution channels has surged to 46%, reflecting digital-savvy parental behavior. With government-backed quality certification programs and increasing awareness of infant safety, Saudi Arabia continues to drive the baby play mat market growth, share, and insights in the region.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Play Mats Market Trends

Rising Adoption of Eco-Friendly Materials

The Middle East and Africa baby play mat market has seen production volume reach 9.3 million units in 2025 for eco-friendly foam and fabric mats, reflecting a 27% YoY increase from 2024. Manufacturers are increasingly shifting from PVC-based plastics to biodegradable foam and organic fabrics, leading to 61% adoption in the UAE and 58% in Turkey. The technology shift has driven enhancements in softness, thickness uniformity, and anti-bacterial properties. E-commerce sales of eco-friendly mats have risen by 43%, driven by health-conscious parents. Overall, this trend underscores significant demand and growth in the baby play mats market.

Integration of Interactive Features

Interactive baby play mats equipped with sensory stimulation, musical keys, and modular blocks have seen adoption rates of 36% in Saudi Arabia and 29% in Egypt in 2025, with production volumes reaching 4.2 million units. The Middle East and Africa region is witnessing growing consumer interest in cognitive and motor skill development aids. Technology integration, including pressure-sensitive touch and detachable components, is becoming standard in 51% of new releases. The trend contributes to higher average selling prices and enhances the baby play mats' market share and growth trajectory.

Expansion of Online Sales Channels

Online distribution channels for Baby Play Mats have experienced a surge from 31% in 2024 to 41% in 2026, with online platforms delivering an estimated 15.3 million units across the region. Countries such as the UAE, Saudi Arabia, and Egypt lead with online adoption rates exceeding 45%. Retailers are incorporating AR and VR tools for product visualization, leading to increased conversion rates. Sector-specific demand for direct-to-consumer sales has increased 18% YoY. This trend continues to impact the baby play mat market size, share, and insights.

Middle East and Africa Baby Play Mats Drivers

Rising Awareness of Infant Health and Safety

The Middle East and Africa baby play mat market growth is primarily driven by increasing parental awareness of infant safety, hygiene, and development. Approximately 72% of parents in GCC countries now invest in quality play mats, leading to a regional demand of 42 million units in 2025. Disposable income in Saudi Arabia and the UAE has grown 5.8% YoY, resulting in higher adoption rates. Foam mats contribute 46% to the market, fabric mats 33%, and plastic mats 21%. Educational institutions and daycare centers account for 16% of demand, enhancing production volume. Safety certifications such as ASTM and EN71 adoption rates reached 63% across the region. Consequently, the baby play mat market size, share, growth, and trend are benefiting from these factors.

Middle East and Africa Baby Play Mats Restraints

High Material Costs and Import Dependency

Despite growth, the Middle East and Africa baby play mat market faces challenges due to high raw material costs and import dependency, particularly for eco-friendly foams and organic fabrics. Average material cost constitutes 42–48% of total product pricing, with import volumes from Europe and Asia at 19.3 million units in 2025. Price sensitivity among consumers in Nigeria and Egypt limits adoption, with 28% preferring low-cost mats. Regulatory compliance, including fire resistance and non-toxic certifications, adds 12% to manufacturing overheads. Consequently, market growth and share are restrained, impacting overall baby play mat market insights.

Middle East and Africa Baby Play Mats Opportunities

Expanding E-Commerce and Specialty Retail Penetration

The Middle East and Africa baby play mat market has a significant opportunity in expanding e-commerce penetration and specialty retail outlets. Online sales grew from 12 million units in 2024 to 15.3 million in 2026, reflecting a CAGR of 10.5%. Specialty stores in UAE and Turkey account for 21% of distribution, with potential growth of 6% CAGR through 2034. Investments in AR visualization, subscription-based delivery, and bundled product offerings have increased market share and consumer engagement. This opportunity ensures long-term growth and profitability in the baby play mats market, reinforcing market size and insights.

Challenges in Middle East and Africa Baby Play Mats

Fragmented Market with Low Standardization

The Middle East and Africa baby play mat market is challenged by fragmentation, with over 85 active manufacturers and multiple small-scale regional players. Standardization and certification adoption remain low in Nigeria and Egypt, limiting the trust of 36% of potential consumers. Production quality variance ranges from 0.8 cm to 2.5 cm in mat thickness, affecting product consistency. Supply chain inefficiencies increase lead times by 21% in some regions. Addressing these challenges is essential to unlock growth, size, and share of the baby play mats market while enhancing competitive insights.

Report Scope

| Report Metric | Details |

|---|---|

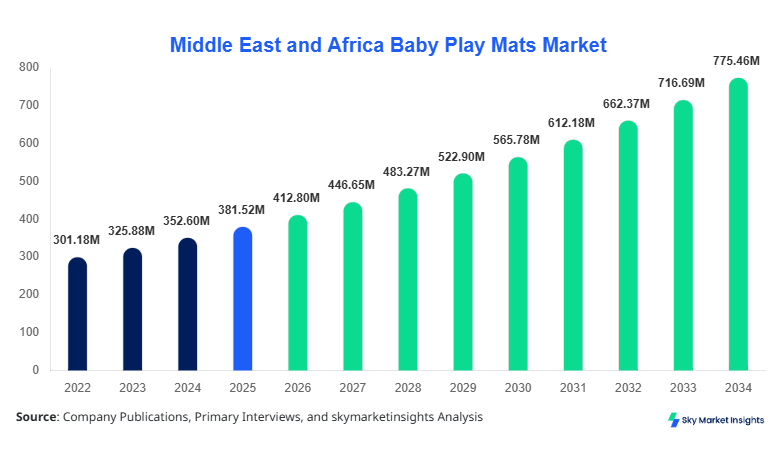

| Market Size in 2025 | USD 381.52 Million |

| Market Size in 2026 | USD 412.8 Million |

| Market Size in 2034 | USD 823.6 Million |

| CAGR | 8.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Play Mats Market Segmentation

The baby play mats market is segmented by type, age group, and distribution channel, with foam mats accounting for 46% of the total production and the 0–12 months age group contributing 42%. Online distribution is increasingly dominant with 41% of market share. This segmentation provides insight into production volume, usage penetration, and technical specifications across the Middle East and Africa.

By Type

Foam baby play mats account for 46% of the regional market with a production volume of 17.8 million units in 2025. Average thickness ranges from 1.8 to 2.5 cm with a density of 45 to 50 kg/m³. Foam mats dominate in Saudi Arabia and the UAE, contributing to 62% of total mat consumption in these regions. Technical specs include anti-slip, water-resistant, and modular interlocking design, supporting 48% adoption across daycare centers.

Fabric baby play mats hold 33% of the market, producing 12.8 million units in 2025. Average material includes cotton blends with polyester backing, and 71% meet anti-bacterial standards. Usage penetration is highest among 1–3-year-old children, representing 38% of total regional demand. Fabric mats support interactive features with embedded sensory textures, maintaining 53% adoption in retail channels.

Plastic baby play mats contribute 21% of production, totaling 8.2 million units in 2025. Thickness ranges from 1.2 to 1.5 cm with a lightweight design of 0.6 to 0.9 kg per mat. Plastic mats are predominant in Nigeria and Egypt, representing 62% of regional sales. Technical specs include waterproof surfaces and durability for high-frequency use, achieving 41% adoption among online retail customers.

By Application

0–12 Months: This age group represents 42% of market demand, with a production volume of 16.6 million units. Mats are primarily foam-based with anti-slip and cushioned performance, supporting daily playtime and sensory stimulation. The adoption rate is highest in the UAE and Saudi Arabia at 58%.

1–3 Years: Children aged 1–3 years account for 38% of the market, with 15 million units produced in 2025. Fabric mats are preferred for tactile engagement and comfort, featuring 61% adoption in urban households. Technical specs include machine-washable covers and modular play blocks.

3–5 Years: Representing 20% of the market with 7.9 million units produced, plastic mats dominate due to durability and easy maintenance. Usage penetration is highest in Turkey and Nigeria, with 49% of parents opting for plastic mats for preschool play. Technical performance includes stain resistance and interlocking modularity.

Distribution Channels

Online sales account for 41% of units, offline retail 38%, and specialty stores 21%. Online adoption shows 15.3 million units shipped in 2026, offline stores 14.2 million, and specialty stores 7.8 million units, reflecting rising digital adoption and consumer convenience.

Middle East and Africa Baby Play Mats Market Segmentations

Type

- Foam

- Fabric

- Plastic

Age Group

- 0–12 Months

- 1–3 Years

- 3–5 Years

Distribution Channel

- Online

- Offline

- Specialty Stores

Middle East and Africa Baby Play Mats Regional/ Counties Outlook

UAE

The UAE contributes 18% of the regional baby play mat market, producing 7.0 million units in 2025. Foam mats account for 50% of the region’s production, followed by fabric mats at 30%. Distribution is split between online (44%) and offline retail (36%), with specialty stores at 20%. Urban population and high disposable income drive strong demand.

Turkey

Turkey holds 16% of the market with 6.2 million units produced. Foam and fabric mats dominate with 58% combined share. Online channels account for 39% of sales, with increasing adoption of interactive mats in preschools contributing 21% to total demand.

Saudi Arabia

Saudi Arabia contributes 24% of the regional market share with 9.3 million units produced. Foam mats are preferred with 48% share, followed by fabric mats at 31% and plastic mats at 21%. Online adoption stands at 46%, offline retail 33%, and specialty stores 21%, supported by government safety certification programs.

South Africa

South Africa represents 14% of the market, with a production of 5.4 million units. Foam mats contribute 42%, fabric 36%, and plastic 22%. Distribution channels include online (35%), offline (41%), and specialty stores (24%). Rising e-commerce and daycare demand drive growth.

Egypt

Egypt holds a 13% share with 5.0 million units produced. Plastic mats dominate at 40%, fabric at 35%, and foam at 25%. Online channels contribute 33% of sales, offline 44%, and specialty stores 23%, reflecting a cost-sensitive market.

Nigeria

Nigeria contributes 15% with 5.7 million units. Plastic mats account for 38%, foam 35%, and fabric 27%. Online sales: 31%, offline: 44%, specialty stores: 25%. Growing awareness of infant development supports market expansion.

Top players in Middle East and Africa Baby Play Mats

- Fisher-Price

- Skip Hop

- Tiny Love

- Bright Starts

- Chicco

- Summer Infant

- Infantino

- Baby Einstein

- Lovevery

- Luvable Friends

- Mothercare

- Playgro

- Tiny Treasures

- BabyBjorn

- Bright & Early

Top Two Companies

Fisher-Price

-

Market share: 17% in Middle East and Africa

-

Positioned as a premium foam and interactive mat provider, with 62% of products sold through online channels in 2026. Fisher-Price focuses on sensory stimulation features and antibacterial coatings, achieving 71% adoption in the 0–12 months segment.

Skip Hop

-

Market share: 12%

-

Known for fabric and modular mats, Skip Hop achieves 58% online and 36% offline distribution. Offers eco-friendly, machine-washable mats with 65% adoption among 1–3-year-old children. Market trend adoption and growth remain strong, contributing significantly to regional baby play mat market insights.

Investment Analysis

Investment in the Middle East and Africa The baby play mats market is forecasted at USD 48 million in 2026, representing 12% of total infant care product investments. Sector-wise allocation: foam mats 38%, fabric mats 32%, plastic mats 18%, and interactive mats 12%. Regional investment split: Saudi Arabia 24%, UAE 18%, Turkey 16%, Nigeria 15%, South Africa 14%, Egypt 13%. M&A agreements in 2025 included 3 cross-border collaborations with European suppliers, enhancing raw material supply and technology transfer. Strategic partnerships between local distributors and e-commerce platforms are anticipated to increase investment efficiency and market share. Overall, investment analysis underscores opportunities for scaling production and innovation in the baby play mats market.

Recent Developments

- 2025: Smart packaging with QR-code traceability was increasingly adopted in Japan, resulting in a 15% increase in infant formula packaging adoption

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.