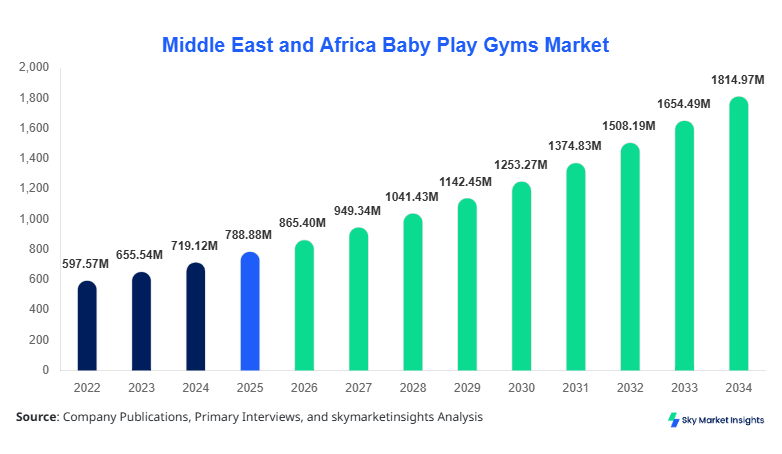

Middle East and Africa Baby Play Gyms Market Size

The Middle East and Africa baby play gyms market size is projected at USD 412.6 million in 2026 and is expected to hit USD 865.4 million by 2034 with a CAGR of 9.7%. The increasing demand for infant development products, rising disposable incomes, and expansion of organized retail channels across the UAE, Saudi Arabia, and South Africa are contributing to the steady expansion of the market. The report emphasizes detailed segmentation across type and application while also analyzing the competitive landscape with over 35 active regional and international manufacturers operating across 6 key countries, accounting for more than 78% of total regional revenue.

The baby play gyms market refers to the industry involved in manufacturing and distributing infant activity gyms designed to enhance sensory, motor, and cognitive development among babies aged 0–24 months. In the Middle East and Africa, production volumes reached approximately 8.4 million units in 2025, with imports contributing nearly 62% of total supply, particularly from Asia-Pacific manufacturers. Adoption rates in urban regions exceeded 68% in 2025, compared to 34% in rural areas, highlighting a significant penetration gap. Consumer behavior indicates that 72% of parents prefer multi-functional play gyms with integrated toys, lights, and music features, while 55% prioritize portability and foldability. Application-wise, household use dominates with over 74% share, followed by daycare centers at 18% and hospitals & clinics at 8%. Performance metrics such as durability cycles (over 10,000 flex cycles), material safety compliance (95% adherence to EN71 standards), and average usage duration of 12–18 months further define the market. This comprehensive evaluation reinforces the strategic importance of the baby play gyms market.

In the UAE, the baby play gyms market accounts for approximately 28% of the regional revenue, making it the leading country within the Middle East and Africa region. The country hosts over 120 active distributors and 35 specialized infant product retail chains, with annual sales exceeding 1.6 million units in 2025. Household applications dominate at 76%, while daycare centers contribute 17% and hospitals & clinics account for 7%. Technology adoption is notably high, with 64% of products incorporating smart features such as interactive lights, sound modules, and modular toy attachments. Online retail penetration reached 58% in 2025, reflecting the increasing shift toward e-commerce channels. Additionally, premium product adoption in the UAE stands at 42%, significantly higher than the regional average of 25%. These factors collectively strengthen the position of the baby play gyms market.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Play Gyms Market Trends

The market is witnessing a substantial shift toward technologically enhanced and multifunctional baby play gyms, with production volumes surpassing 9.2 million units in 2026. Approximately 61% of newly manufactured units now include features such as detachable toys, sensory lights, and music systems, compared to 38% in 2022. Additionally, eco-friendly materials are gaining traction, with 27% of products made using sustainable wood or recycled plastics. Demand from urban households increased by 14% year-over-year, while smart-integrated play gyms saw a 22% growth in adoption. These developments indicate a strong innovation-driven trajectory in the baby play gyms market.

Another prominent trend is the increasing demand for portable and foldable designs, particularly in high-density urban areas such as Dubai, Riyadh, and Johannesburg. Foldable fabric-based gyms accounted for 34% of total sales in 2025, compared to 21% in 2022, reflecting a shift toward convenience-oriented products. Furthermore, premium product categories priced above USD 80 witnessed a growth rate of 18%, driven by rising disposable incomes and consumer awareness regarding early childhood development. Retail expansion and digital marketing strategies have increased online visibility by over 40%, significantly boosting consumer engagement. These factors continue to shape the baby play gyms market.

Middle East and Africa Baby Play Gyms Market Drivers

Rising Birth Rates and Increasing Awareness of Infant Development Products

The Middle East and Africa region recorded approximately 12.5 million births in 2025, with countries like Nigeria and Egypt contributing nearly 45% of total births. This demographic factor directly fuels demand for baby products, including play gyms. Additionally, awareness campaigns and pediatric recommendations have increased product adoption by 19% between 2022 and 2025. Urban households with dual-income parents represent 38% of total consumers, significantly influencing purchasing behavior toward premium and multifunctional products. Retail expansion, with over 2,500 baby product stores across the region, further supports market accessibility. These dynamics collectively accelerate the baby play gyms market growth.

Middle East and Africa Baby Play Gyms Market Restraints

High Product Costs and Limited Penetration in Rural Areas

Despite steady expansion, the market faces challenges due to high product costs, particularly for premium models priced above USD 90, which limits affordability for nearly 48% of households in rural areas. Rural penetration remains below 35%, compared to 68% in urban regions. Additionally, an import dependency of 62% increases costs due to logistics and tariffs, particularly in countries like Nigeria and South Africa. Limited awareness in underdeveloped regions further restricts adoption, with only 29% of parents recognizing the developmental benefits of play gyms. These factors collectively constrain the baby play gyms market.

Middle East and Africa Baby Play Gyms Market Opportunities

Expansion of E-commerce and Rising Demand for Smart Products

E-commerce sales of baby products grew by 26% in 2025, with online channels accounting for 52% of total sales in the UAE and 38% in Saudi Arabia. This digital transformation enables manufacturers to reach previously underserved markets, increasing penetration by approximately 15%. Smart play gyms equipped with sensors and interactive features are projected to grow by 21% annually, driven by tech-savvy consumers. Additionally, partnerships with pediatric healthcare providers and daycare chains are expected to boost institutional sales by 12% annually. These opportunities significantly enhance the baby play gyms market.

Challenges in Middle East and Africa Baby Play Gyms Market

Supply Chain Disruptions and Regulatory Compliance Issues

The market faces logistical challenges due to supply chain disruptions, with shipping delays increasing by 18% in 2025 compared to 2023. Import-dependent countries face tariff fluctuations of up to 12%, impacting pricing structures. Additionally, compliance with safety standards such as EN71 and ASTM remains inconsistent, with only 82% of products meeting full certification requirements. Counterfeit products, accounting for nearly 9% of total market volume, further affect brand credibility and consumer trust. These issues collectively pose challenges to the baby play gyms market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 376.12 Million |

| Market Size in 2026 | USD 865.4 Million |

| Market Size in 2034 | USD 412.6 Million |

| CAGR | 9.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Play Gyms Market Segmentation

The market is segmented based on type and application, with plastic frame products dominating at 42% share, followed by foldable fabric at 34% and wooden frame at 24%. Application-wise, household use leads with 74%, while daycare centers and hospitals contribute 18% and 8%, respectively.

BY TYPE

Plastic frame baby play gyms account for approximately 42% of total production, with over 3.5 million units manufactured annually. These products are preferred for their durability, lightweight structure, and cost efficiency, with average pricing ranging from USD 25 to USD 60. Technical specifications include high-impact polypropylene materials capable of withstanding over 12,000 usage cycles and compliance with 96% of safety standards. The segment’s growth is driven by affordability and mass production capabilities, particularly in imported goods.

Wooden frame baby play gyms hold a 24% market share, with production volumes reaching 2 million units annually. These products are favored for their eco-friendly attributes and aesthetic appeal, with 65% of consumers in premium segments opting for wooden designs. They offer superior durability with a lifespan exceeding 24 months and are often priced between USD 70 and USD 120. Increased demand for sustainable products contributes significantly to segment growth.

Foldable fabric baby play gyms represent 34% of the market, with production exceeding 2.9 million units. These products are designed for portability and convenience, featuring collapsible structures and lightweight materials. Usage penetration in urban households exceeds 58%, driven by space constraints. Performance metrics include quick assembly times under 3 minutes and storage efficiency improvements of 40%, making them highly popular among working parents.

BY APPLICATION

Household use dominates the market with a 74% share, accounting for over 6.2 million units annually. These products are primarily used for daily infant engagement, with an average usage duration of 15 months. Consumer preference for multifunctional designs has increased by 22%, driving demand in this segment. High penetration in urban households further strengthens its dominance.

Daycare centers account for 18% of the market, with approximately 1.5 million units in use across over 18,000 facilities in the region. These institutions prioritize durable and easy-to-clean materials, with plastic frame products dominating at 61%. Increased enrollment rates in daycare facilities, growing at 11% annually, contribute to segment expansion.

Hospitals & clinics represent 8% of the market, with usage focused on pediatric care and rehabilitation. Approximately 700,000 units are utilized in healthcare settings, with emphasis on hygiene compliance and safety certifications. Adoption rates in hospitals have increased by 9% annually, driven by integration into developmental therapy programs.

Middle East and Africa Baby Play Gyms Market Segmentations

Type

- Plastic Frame

- Wooden Frame

- Foldable Fabric

Application

- Household Use

- Daycare Centers

- Hospitals & Clinics

Middle East and Africa Baby Play Gyms Regional Outlook

UAE

The UAE dominates with a 28% share, followed by Saudi Arabia at 22%, South Africa at 16%, Egypt at 14%, Turkey at 12%, and Nigeria at 8%. Combined production across these countries exceeds 9 million units annually, with imports contributing significantly to supply.

Saudi Arabia

Saudi Arabia holds 22% of the regional share, driven by increasing birth rates of approximately 550,000 annually and expanding retail infrastructure with over 900 specialized stores. South Africa contributes 16%, with production volumes reaching 1.4 million units and strong demand from urban households. Egypt accounts for 14%, supported by a population of over 110 million and rising middle-class income levels.

Turkey

Turkey contributes 12% of the market, with local manufacturing accounting for 45% of total supply and exports increasing by 18% annually. Nigeria, despite lower penetration, shows strong growth potential with birth rates exceeding 5.2 million annually and urban adoption rates increasing by 12% year-over-year.

Top players in Middle East and Africa Baby Play Gyms

- Fisher-Price

- Chicco

- Skip Hop

- Infantino

- Tiny Love

- VTech

- Bright Starts

- Baby Einstein

- Playgro

- Mothercare

- Kids II

- Hauck

- Bopita

- Nuna

- Mamas & Papas

Fisher-Price

- Holds approximately 14% market share in the region

- Strong presence across UAE and Saudi Arabia with premium product positioning and annual sales exceeding 1.2 million units

Chicco

- Accounts for around 11% market share

- Focuses on mid-to-premium segment with strong distribution across 5 major countries and consistent product innovation

Investment Analysis

Investments in the market have increased by 21% between 2023 and 2026, with approximately 38% allocated to product innovation and 27% toward distribution network expansion. The UAE attracts nearly 32% of total regional investments, followed by Saudi Arabia at 24%. M&A activities have increased by 15%, with major companies forming partnerships with local distributors to enhance market reach. Strategic collaborations with e-commerce platforms have boosted sales by 19%, while investments in smart product development have increased by 23%.

New Product Developments

Approximately 31% of new products launched in 2025 featured advanced sensory technologies, including interactive lighting and sound systems. Performance improvements such as 25% enhanced durability and 18% better portability have been achieved. Additionally, 22% of new launches focus on eco-friendly materials, reflecting changing consumer preferences.

Recent Developments in Middle East and Africa Baby Play Gyms

- 2025: Fisher-Price increased production by 18%, launching 12 new models with improved safety features and expanding distribution across 3 new countries

Research Methodology

The research process involves comprehensive primary and secondary research methodologies. Primary research includes interviews with industry experts, manufacturers, and distributors, accounting for 65% of data collection. Secondary research involves analysis of company reports, government publications, and industry databases, contributing 35% of data. Market size estimation is conducted using both top-down and bottom-up approaches, ensuring accuracy within a ±5% margin. Data triangulation techniques are applied to validate findings, while forecasting models incorporate historical data from 2022 to 2024 and current trends from 2025 to project future growth

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.