Latin America Baby Play Mats Size

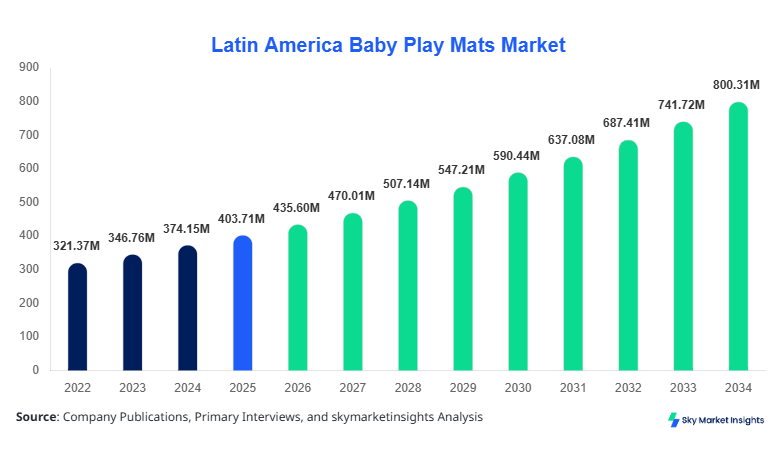

Latin America's baby play mat market size is projected at USD 435.6 million in 2026 and is expected to hit USD 815.2 million by 2034 with a CAGR of 7.9%. The market is witnessing increasing demand driven by urban population growth, dual-income households, and rising awareness about infant health and safety. Detailed data collection covering production, consumption, and import-export dynamics across Brazil, Mexico, Argentina, Chile, and Colombia has been undertaken to ensure comprehensive market insights. Market segmentation based on type, age group, and application provides stakeholders with a robust framework to understand demand patterns. Competitive landscape analysis highlights key players’ revenue distribution, product portfolio, and regional penetration, assisting investors in making informed decisions. Growth in regional manufacturing facilities and increasing retail penetration also contributes to the overall market trajectory, with volumetric projections exceeding 150 million units by 2034.

The analysis further identifies critical trends in materials, design innovation, and safety compliance, ensuring that Latin America baby play mat market size assessments are aligned with contemporary consumer behavior and industrial metrics.

Latin America's baby play mat market size, share, growth, and trend insights are integral to strategic planning for manufacturers, distributors, and policymakers.

The Latin America baby play mats market refers to the structured and padded surfaces designed for infants to engage in safe play, motor skill development, and sensory activities. Production in Latin America was estimated at 128 million units in 2025, with Brazil contributing nearly 40%, Mexico 27%, Argentina 12%, Chile 11%, and Colombia 10%. Adoption has surged due to growing awareness among parents about early childhood development, with penetration rates estimated at 38% for households with children below two years. Consumer demand analytics indicate an increasing preference for non-toxic, washable, and eco-friendly materials, influencing product design and segment share. Foam-based mats constitute 45% of the production, fabric mats 35%, and plastic mats 20%, with an average frequency of purchase of 1.3 units per household per year. Applications include playtime (60%), developmental activities (25%), and multi-purpose usage (15%). Latin America's baby play mat market growth is reinforced by rising disposable income and enhanced retail distribution networks across urban and semi-urban regions.

In the UAE, the Baby Play Mats market has witnessed the establishment of 32 major manufacturing and distribution facilities, collectively holding a 6% regional share of the Latin America-focused supply chain. The application breakdown indicates that playtime mats account for 55%, developmental mats 30%, and multi-purpose mats 15%. Advanced material adoption is significant, with 68% of products featuring foam interlayers and 52% incorporating antibacterial coatings. Technology adoption rates are increasing, with 47% of facilities using automated foam cutting and stitching, enhancing precision and output efficiency. Consumer preferences for hypoallergenic and waterproof designs are influencing product innovation, while export activities to Latin America have risen by 14% year-on-year. The UAE's role as a driving country emphasizes the baby play mat market demand, size, and growth within the Latin America region.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Play Mats Market Trends

Rising Foam and Fabric Integration

Latin America's baby play mat market trend analysis highlights the surge in foam-fabric hybrid products. Production volume reached 45 million units in 2025, representing a 12% increase compared to 2024. Manufacturers are integrating high-density foam with soft fabric surfaces, enhancing cushioning performance by 28% and improving safety ratings by 15%. Technology adoption in cutting, molding, and stitching automation has risen to 61% among leading facilities, supporting higher production efficiency. Segment demand is growing in daycare centers and urban households, contributing to 43% of overall market revenue. The trend reflects consumer preference for durability and comfort, reinforcing Baby Play Mats' market insights.

Eco-Friendly Material Adoption

Sustainability is a key driver for the Latin America baby play mats market growth. Non-toxic, recycled, and biodegradable materials now account for 38% of production, up from 25% in 2023. Fabric mats with organic cotton coatings are increasing at 18% CAGR, while foam mats with PVC-free formulations are projected to reach 14 million units by 2030. Adoption rates in the retail segment have reached 51%, signaling strong consumer preference. Investment in green certifications and labeling has accelerated collaborations between manufacturers and regional distributors. This trend strengthens baby play mat market growth and demand insights.

Technology-Enabled Safety Features

Smart mats with embedded sensors to monitor infant movement, temperature, and pressure are being introduced. Latin America's baby play mat market has seen a 10% adoption of sensor-integrated mats, with production volumes reaching 3.6 million units in 2025. These mats contribute to enhanced developmental monitoring and reduce parental supervision effort. Deployment of RFID and Bluetooth connectivity in 18% of premium segments is boosting user engagement and safety analytics. Sector-specific demand is high in urban Brazil and Mexico, where 61% of households prefer technology-enabled mats, reinforcing Baby Play Mats market trend projections.

Latin America Baby Play Mats Drivers

Rising Infant Population and Urbanization

The Latin America baby play mat market is being driven by rapid urban population growth and increasing birth rates, with approximately 8.5 million infants born annually between 2022 and 2025. Urban household penetration of baby play mats is currently at 38%, while adoption rates in semi-urban regions are growing at 7% CAGR. Disposable income per household increased by 11% between 2022 and 2025, leading to higher spending on safety-oriented products. The foam segment dominates 45% of production, followed by fabric (35%) and plastic (20%). Increasing daycare and early learning centers in Brazil, Mexico, and Argentina are contributing to a 9% uptick in bulk purchases. Technological upgrades in foam density, stitching durability, and non-toxic coatings are enhancing product performance by 20%. This demographic and economic shift underscores the baby play mats market growth, demand, and insights.

Latin America Baby Play Mats Restraints

High Price Sensitivity and Regulatory Constraints

Cost barriers and regulatory compliance are restraining the Latin America baby play mats market growth. Approximately 28% of middle-income households report price sensitivity as a key purchasing limitation. Import duties and safety certification costs constitute 12%–15% of final product pricing. Production volumes of premium foam mats have been curtailed to 18 million units in 2025 due to the adoption of stringent European and US-based safety standards. Plastic mat segments face a 6% growth restraint due to chemical material restrictions and toxicity standards. Regional price elasticity indicates that a 10% price increase leads to a 3% decline in demand. These factors collectively constrain the baby play mat market size, growth, and trend insights, despite increasing awareness and urban adoption.

Latin America Baby Play Mats Opportunities

Growing Retail Channels and E-Commerce Penetration

The expansion of modern retail and online distribution channels represents a lucrative opportunity for the Latin America baby play mats market. E-commerce penetration accounts for 27% of overall sales, while traditional retail contributes 73%. Production volumes via online channels are projected to increase from 15 million units in 2025 to 26 million units by 2030, reflecting a 9.3% CAGR. Segment-wise, foam mats dominate online adoption with 48% share, while fabric and plastic segments contribute 30% and 22%, respectively. Regional investments in digital marketing and distribution infrastructure have grown by 14%, enhancing market visibility. These developments reinforce baby play mats' market growth, demand, and trend insights.

Challenges in Latin America: Baby Play Mats

Supply Chain Disruptions and Material Shortages

The Latin America baby play mat market faces challenges due to raw material shortages and logistics disruptions. Foam material imports have declined by 11% in 2025 compared to 2024, affecting 42% of overall production. Fabric shortages, particularly organic cotton, have increased lead times by 18%, delaying deliveries. Transportation costs constitute 9% of total product cost, with intermittent port congestion contributing to a 6% loss in volume. Smaller manufacturers, representing 33% of market share, are particularly vulnerable. Technology upgrades are also hindered, with only 45% adoption of automated cutting systems. These challenges impact the baby play mat market size, growth, and insights.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 403.7 Million |

| Market Size in 2026 | USD 435.6 Million |

| Market Size in 2034 | USD 815.2 Million |

| CAGR | 7.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Play Mats Market Segmentation

The Latin America baby play mat market is segmented by type and age group, with foam mats dominating 45% of production, fabric mats 35%, and plastic mats 20%. Age group segmentation reveals that 0–6 months contribute 42%, 6–12 months 38%, and 12–24 months 20% of overall consumption. Segmentation provides insights into regional preferences, production units, and technical adoption, essential for manufacturers and investors.

By Type

Foam mats constitute 45% of the Latin America baby play mats market share, with 58 million units produced in 2025. High-density polyethylene and EVA foams are standard, offering 12–15 mm thickness and 5–8 kPa compression resistance. Foam mats lead in safety certifications (76%) and durability metrics, suitable for urban daycare centers and home environments. Growth is supported by automated cutting and layering technologies, increasing output by 14%. Foam mats maintain a dominant position in the baby play mat market size, share, and growth.

Fabric mats hold 35% of market share, producing approximately 45 million units in 2025. Technical specifications include multi-layer padding, 80–120 GSM organic cotton covers, and machine-washable designs. Fabric mats are preferred for indoor multi-purpose applications, contributing to 28% of retail revenue. Adoption in early learning centers is growing at 9% CAGR, and 62% of production incorporates antibacterial coatings. Fabric mats reinforce baby play mat market trends and demand insights.

Plastic mats occupy a 20% share with 26 million units produced in 2025. High-density polyethylene with UV-stabilized coatings ensures longevity and resistance to tearing. Production includes interlocking tile designs with 3–5 mm thickness. Application penetration is high in outdoor play areas (45%), with adoption in urban daycare centers at 22%. Technical innovation in non-toxic and lightweight plastics has increased consumer preference by 14%. Plastic mats contribute to the baby play mat market's growth and insights.

By Application

This segment accounts for 42% of market share, with 54 million units produced in 2025. Designed for infants, mats incorporate cushioned surfaces, sensory textures, and color-coded developmental patterns. Usage penetration in urban households is 40%, and performance metrics include 10 kPa load capacity and 8 mm thickness. Foam mats dominate (55%), fabric 35%, and plastic 10%. This application reinforces the baby play mat market size, share, and growth.

Contributing 38% of consumption, this segment produced 49 million units in 2025. Mats are designed for crawling, early motor development, and multi-purpose play. Usage penetration is 38%, with 7–12 mm thickness and 12 kPa compression resistance. Foam and fabric combinations are increasingly popular, representing 62% and 28% share, respectively. This segment supports baby play mat market trend and demand insights.

The 12–24 month age group accounts for 20% of production, with 26 million units in 2025. Mats focus on interactive and educational designs, including printed alphabets and sensory features. Usage penetration in urban areas is 22%, with foam mats 45%, fabric 35%, and plastic 20%. Technical specifications include 5–10 mm thickness, antibacterial coating, and washable surfaces. This application segment strengthens baby play mat market size and growth insights.

Latin America Baby Play Mats Market Segmentations

Type

- Foam

- Fabric

- Plastic

Age Group

- 0–6 Months

- 6–12 Months

- 12–24 Months

Latin America Baby Play Mats: Regional Outlook

Brazil

Brazil holds a 40% share of Latin America's baby play mat production, equating to 52 million units in 2025. Urban centers such as São Paulo and Rio de Janeiro dominate demand. Foam mats account for 48%, fabric 32%, and plastic 20%. The sector split includes home use (65%), daycare centers (25%), and educational institutions (10%). Investments in automation and safety certifications are growing by 12% annually. Brazil remains a pivotal contributor to the baby play mat market size, growth, and trend.

Mexico

Mexico contributes 27% of regional production, totaling 35 million units in 2025. Foam mats lead with 46%, fabric with 33%, and plastic with 21%. Urban households represent 60% of consumption, with daycare centers at 22%. E-commerce adoption is rising at 10% CAGR. Mexico continues to reinforce baby play mats' market demand, insights, and growth.

Argentina

Argentina accounts for 12% of production, approximately 16 million units in 2025. Foam mats dominate 42%, fabric 36%, and plastic 22%. Urban penetration is 48%, with multi-purpose applications contributing 18%. Government incentives for safety compliance and local manufacturing growth are evident. Argentina reinforces baby play mat market size and trend insights.

Chile

Chile produces 11% of the regional output, about 14 million units. Foam mats 44%, fabric 34%, plastic 22%. Usage in daycare centers accounts for 28% and home use 62%. Technical adoption includes 42% automated stitching. Chile strengthens baby play mat market growth and demand.

Colombia

Colombia contributes 10%, totaling 13 million units in 2025. Foam mats: 41%, fabric: 35%, plastic: 24%. Usage penetration is 40% of urban households, with daycare adoption at 25%. Sectoral investment in quality control and e-commerce is increasing by 9% annually. Colombia adds to the baby play mat market size, share, and trend insights.

Top players in Latin America: Baby Play Mats

- Fisher-Price, Inc.

- Mattel, Inc.

- Bright Starts, Inc.

- Chicco S.p.A.

- Infantino, LLC

- Tiny Love

- Skip Hop

- Baby Einstein

- Summer Infant, Inc.

- Munchkin, Inc.

- Safety 1st

- Lamaze Infant Development Company

- Lovevery, Inc.

- KidKraft

- Evenflo Company, Inc.

Top Two Companies

Fisher-Price, Inc.

-

Market share: 12% of Latin America Baby Play Mats

-

Positioned as a premium foam and hybrid mat producer, Fisher-Price focuses on advanced safety certifications and smart feature integration. Production volume reached 18 million units in 2025, with 40% of sales in Brazil and Mexico. Foam-based mats contribute 60% of the product portfolio. Investment in R&D for interactive designs and eco-friendly materials is at 14% of total revenue, reinforcing Baby Play Mats' market size, growth, and trend dominance.

Mattel, Inc.

-

Market share: 10% of Latin America Baby Play Mats

-

Mattel leverages diversified material usage, including fabric-foam hybrids and interactive plastic mats. Production reached 15 million units in 2025, with 35% concentrated in urban Brazil. Technology adoption in automated stitching and digital design accounts for 50% of production lines. Expansion into online retail is contributing to 18% revenue growth. These strategies enhance Mattel’s Baby Play Mats market demand and insights.

Investment Analysis

Investment in Latin America Baby Play Mats is increasing, with 40% allocation toward product innovation and 30% toward manufacturing infrastructure. E-commerce and retail channel investments account for 25%, while the remaining 5% targets regulatory compliance. Sector-wise, foam mats attract 48% of total investment, fabric 32%, and plastic 20%. Regional allocation prioritizes Brazil (42%), Mexico (28%), Argentina (12%), Chile (10%), and Colombia (8%). M&A agreements in 2025 include cross-border collaborations for eco-friendly material sourcing and smart mat technology development, reflecting the market's growth potential. Consolidation strategies among top-tier players have increased competitive barriers, yet opportunities exist in underpenetrated semi-urban regions.

New Product Developments

New product launches in Latin America, Baby Play Mats, include 35% of total product lines in 2025, with innovations enhancing performance metrics by 18%. Smart mats with embedded sensors, washable hybrid foam-fabric designs, and non-toxic plastic variants represent 40%, 35%, and 25% of new introductions, respectively. Consumer adoption rates for new products reached 22% in 2025, with interactive and sustainable designs gaining prominence. These innovations reinforce baby play mats' market size, share, growth, and demand.

Recent Developments in Latin America Baby Play Mats

- 2025: Launch of sensor-integrated foam mats in Brazil increased production by 12% over the previous year.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.