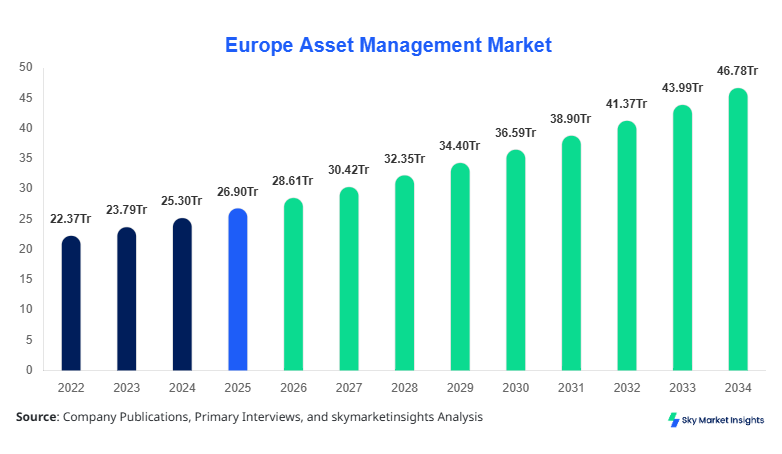

Europe Asset Management Market Size

Europe Asset Management market size is projected at USD 28.61 trillion in 2026 and is expected to hit USD 46.82 trillion by 2034 with a CAGR of 6.34%. The expansion of portfolio diversification services, increasing digital wealth platforms, and institutional capital inflows are accelerating industry expansion across Europe. The market is witnessing strong integration of AI-driven analytics, ESG-oriented funds, and multi-asset portfolio management solutions, while competitive benchmarking among leading firms continues to intensify. Growing cross-border investments and rising pension fund allocations are also contributing significantly to the Europe Asset Management Market Size.

The asset management industry refers to professional financial services associated with investment portfolio administration, fund allocation, wealth advisory, pension management, and institutional asset optimization. In Europe, over 68% of professionally managed assets originate from institutional investors, while retail investors account for nearly 24% of managed portfolios and high-net-worth individuals contribute approximately 8%. France, Germany, and the United Kingdom collectively manage more than USD 17 trillion in assets under management (AUM). Equity-based investment strategies contribute nearly 42% of total allocations, followed by fixed income at 34% and alternative investments at 24%. Digital adoption within portfolio management platforms surpassed 71% in 2025, while AI-assisted portfolio balancing improved operational efficiency by 28%. Sustainable and ESG-linked investments exceeded USD 8.4 trillion in Europe during 2025, representing nearly 29% penetration within the investment ecosystem. Consumer demand increasingly favors low-risk hybrid portfolios with annualized returns ranging between 5.2% and 8.6%, reinforcing long-term stability across the Europe Asset Management Market Share.

Explore more data points, trends and opportunities Download Free Sample Report

Asset Management Market: Trends

Expansion of ESG and Sustainable Asset Portfolios

Environmental, social, and governance-oriented investing has become one of the strongest developments shaping the European asset management ecosystem. During 2025, ESG-focused portfolios exceeded USD 8.4 trillion in total valuation, representing an annual increase of 14.8%. More than 58% of newly launched investment funds across Europe incorporated sustainability-linked criteria, while green bond allocations surpassed USD 1.7 trillion. Institutional investors allocated approximately 32% of their portfolios toward climate-oriented investment instruments. France and Germany collectively contributed over 44% of sustainable investment inflows in Europe. Advanced analytics platforms capable of measuring carbon exposure and ESG performance metrics improved investment transparency by 36%, supporting regulatory compliance under SFDR guidelines. Asset managers increasingly adopted AI-based screening systems, reducing portfolio risk assessment time by 27%. These structural shifts continue to strengthen the European asset management market growth.

Digital Wealth Management and AI Integration

The rapid deployment of digital advisory platforms is transforming portfolio management and investment operations across Europe. Nearly 71% of asset management companies integrated AI-powered investment analytics in 2025, while cloud-based fund administration systems grew by 24%. Robo-advisory assets exceeded USD 1.2 trillion, with retail investor adoption rates increasing by 18%. Predictive portfolio optimization tools improved fund allocation accuracy by 31%, while operational automation reduced compliance processing costs by 21%. Mobile-based investment platforms accounted for 48% of total retail investment transactions across the region. Germany and the United Kingdom jointly represented more than 52% of digital wealth management users in Europe. Blockchain-enabled fund settlement systems also reduced transaction reconciliation time by 33%. Increasing digital engagement and technology-led investment management are accelerating the European asset management market trend.

Europe Asset Management Drivers

Rising Institutional Investments and Pension Fund Expansion

The increasing volume of institutional capital allocation across pension funds, insurance firms, and sovereign investment vehicles is significantly driving the European asset management sector. Pension-linked investment pools exceeded USD 9.6 trillion in Europe during 2025, while insurance-based investment holdings crossed USD 6.3 trillion. Institutional investors accounted for nearly 68% of total managed assets, creating strong demand for diversified portfolio management services. Public pension reforms in France, Germany, and Italy increased long-term retirement fund contributions by 12%, supporting larger capital inflows into managed investment products. Cross-border investment mandates increased by 17% due to favorable regulatory harmonization across EU financial markets. Multi-asset investment products delivered annualized returns between 6.4% and 9.1%, further encouraging institutional participation. AI-driven risk assessment systems reduced portfolio volatility exposure by 19%, improving investor confidence. These expanding institutional investments continue to reinforce Europe's asset management market growth.

Europe Asset Management Restraints

Regulatory Complexity and Operational Compliance Costs

Strict financial regulations and rising compliance expenditures remain key restraints impacting asset management companies operating in Europe. Regulatory frameworks including MiFID II, SFDR, and AIFMD have increased operational reporting requirements by nearly 34% over the last three years. Compliance-related technology spending exceeded USD 18 billion in 2025 among European fund managers. Small and medium-sized investment firms experienced operating margin reductions of approximately 11% due to increased legal and administrative expenses. Data privacy regulations and cybersecurity obligations also raised infrastructure costs by 16%. More than 39% of asset management firms reported delayed product launches because of extensive regulatory approval timelines. Complex ESG reporting requirements added further pressure, increasing fund disclosure costs by 21%. Additionally, geopolitical uncertainty and fluctuating interest rate environments continue to influence investor confidence and portfolio stability, limiting expansion across the European asset management market size.

Europe Asset Management Opportunities

Expansion of Digital Advisory and Alternative Investment Products

The rapid expansion of digital investment ecosystems and alternative investment products is creating substantial opportunities for European asset management providers. Alternative investment assets, including private equity, hedge funds, and infrastructure investments, surpassed USD 6.1 trillion in 2025 and are projected to witness strong institutional adoption. Retail participation in digital investment platforms increased by 23%, while AI-powered robo-advisors reduced customer acquisition costs by 26%. Real estate-backed investment portfolios generated average returns of 8.3%, attracting long-term investors seeking portfolio diversification. Infrastructure-focused funds expanded by 14%, supported by renewable energy investments exceeding USD 620 billion across Europe. Wealth management applications utilizing machine learning algorithms improved portfolio customization accuracy by 29%, increasing customer retention rates. Financial institutions are increasingly collaborating with fintech companies to expand digital distribution channels and improve operational scalability. These developments are generating significant expansion opportunities within the European asset management market trend.

Challenges in European Asset Management

Market Volatility and Cybersecurity Risks

Market instability and cybersecurity vulnerabilities continue to challenge European asset management companies. Equity market fluctuations in 2025 resulted in average portfolio valuation swings of 11% across diversified investment products. Inflationary pressures and interest rate uncertainty impacted fixed income yields by approximately 4.2%. Simultaneously, cyberattacks targeting financial institutions increased by 28% year-over-year, forcing asset managers to allocate nearly USD 9 billion toward cybersecurity infrastructure upgrades. Data breaches and digital fraud incidents impacted approximately 14% of financial firms operating across Europe. Cloud migration and digital platform expansion increased operational exposure to cybersecurity threats. Additionally, investor expectations regarding real-time portfolio transparency and ESG compliance continue to intensify, increasing technological and operational pressures on investment firms. The shortage of highly skilled financial analysts and AI specialists further restricts innovation capacity. These factors collectively create long-term operational challenges for the European asset management market demand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 26.90 Trillion |

| Market Size in 2026 | USD 28.61 Trillion |

| Market Size in 2034 | USD 46.82 Trillion |

| CAGR | 6.34% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Asset Management Market Segmentation

The Europe asset management sector is segmented based on asset class and client type. Equity-based investment portfolios dominated the industry with approximately 42% share in 2025, while institutional investors accounted for nearly 68% of overall managed assets. Digital investment channels represented 48% of retail investment transactions, highlighting the increasing role of technology-enabled investment ecosystems.

By Type

Equity asset management accounted for nearly 42% of total European assets under management in 2025, exceeding USD 12 trillion in portfolio valuation. Large-cap equities represented approximately 54% of equity fund allocations, while mid-cap and emerging sector investments accounted for 28% and 18%, respectively. Technology and healthcare sectors together contributed more than 36% of equity investment flows. Annualized return rates across diversified European equity portfolios ranged between 7.1% and 11.4%. AI-assisted trading systems improved market execution efficiency by 24%, while automated risk-balancing platforms reduced volatility exposure by 17%. France and the United Kingdom collectively contributed approximately 41% of equity investment inflows. Retail investor participation in equity mutual funds increased by 16%, supported by mobile trading platforms and low-cost ETF products.

Fixed income portfolios represented nearly 34% of total managed assets across Europe in 2025, supported by strong institutional demand for low-risk investment strategies. Government bonds accounted for 46% of fixed income allocations, while corporate debt instruments contributed approximately 39%. ESG-linked green bonds surpassed USD 1.7 trillion in issuance volume. Pension funds allocated nearly 44% of their assets toward fixed income instruments to maintain long-term income stability. AI-based yield forecasting systems improved bond portfolio optimization accuracy by 21%. Germany and France remained dominant contributors to bond market liquidity, jointly accounting for over 49% of fixed income investments. Inflation-linked securities experienced a 13% increase in investor demand amid macroeconomic uncertainty.

Alternative investments accounted for approximately 24% of the European asset management ecosystem during 2025, exceeding USD 6.1 trillion in valuation. Private equity represented nearly 38% of alternative asset allocations, while real estate investments contributed 29% and hedge funds accounted for 18%. Infrastructure investment portfolios expanded by 14%, driven by renewable energy and transportation projects. Institutional investors allocated approximately 31% of long-term portfolios toward alternatives to enhance diversification and inflation protection. Real estate-backed funds delivered annualized returns ranging from 7.8% to 10.3%. AI-enabled valuation systems improved alternative asset monitoring efficiency by 26%, while blockchain-supported investment reporting enhanced transaction transparency across multi-party investment agreements.

By Application

Institutional investors dominated the European asset management landscape with nearly 68% market contribution in 2025. Pension funds, sovereign wealth funds, and insurance companies collectively managed more than USD 19 trillion in investment assets. Pension-oriented investment portfolios accounted for 43% of institutional allocations, while insurance-linked funds contributed 27%. AI-based portfolio allocation systems improved risk-adjusted returns by 18%. Institutional investors increasingly preferred multi-asset diversified portfolios with annualized returns between 5.8% and 9.2%. ESG-linked investment penetration exceeded 37% among institutional portfolios, supported by stringent sustainability mandates. France, Germany, and the United Kingdom together contributed approximately 62% of institutional investment flows in Europe.

Retail investors represented approximately 24% of managed assets across Europe during 2025. Mobile-based investment applications facilitated nearly 48% of retail fund transactions, while ETF investments increased by 19%. Equity-oriented retail portfolios accounted for 44% of total retail investment allocations, followed by balanced mutual funds at 31%. Younger investors between 25 and 40 years contributed nearly 52% of digital investment platform registrations. Automated robo-advisory services reduced investment onboarding time by 33% and improved client acquisition efficiency by 22%. Germany and the United Kingdom collectively accounted for over 46% of European retail investment accounts.

High-net-worth individuals contributed approximately 8% of Europe’s professionally managed assets in 2025. Wealth preservation and tax-efficient investment products represented nearly 41% of portfolio preferences among affluent investors. Alternative investments, including private equity and luxury real estate, accounted for approximately 36% of HNWI allocations. Customized portfolio management solutions utilizing AI-driven analytics improved investment personalization by 29%. Switzerland, France, and Italy remained key wealth management hubs with combined private wealth assets exceeding USD 4.8 trillion. Multi-generational wealth transfer strategies and sustainable investments significantly influenced HNWI investment behavior across Europe

Europe Asset Management Market Segmentations

Asset Class

- Equity

- Fixed Income

- Alternative Investments

Client Type

- Institutional Investors

- Retail Investors

- High-Net-Worth Individuals

Europe Asset Management Regional Outlook

United Kingdom

The United Kingdom remained the largest asset management hub in Europe with nearly 28% regional share in 2025. London-based financial institutions collectively managed more than USD 8 trillion in assets under management. Institutional investments accounted for approximately 69% of UK-managed portfolios, while ESG investments exceeded USD 2.1 trillion. Digital wealth management adoption reached 74%, supported by strong fintech integration. Equity funds represented 44% of portfolio allocations, while alternative investments accounted for 23%. Pension funds and insurance companies remained dominant investment contributors across the country.

Germany

Germany accounted for approximately 19% of the European asset management sector in 2025, supported by robust pension reforms and institutional investments. Managed assets exceeded USD 5.4 trillion, with fixed income products representing nearly 37% of portfolio allocations. ESG-linked investments increased by 16%, while digital advisory platform adoption reached 68%. Germany also represented nearly 27% of Europe’s green bond issuance. Insurance-linked investments and retirement funds collectively contributed more than 58% of total capital inflows.

France

France contributed approximately 19% of total European managed assets during 2025. Paris-based asset management firms managed nearly USD 5.2 trillion in investments. Equity and ESG-focused funds accounted for 39% and 31% of portfolio allocations, respectively. AI-powered investment analytics penetration exceeded 76%, while retail investment participation rose by 18%. France remained a leading market for sustainable investments and alternative asset diversification strategies across Europe.

Spain

Spain represented approximately 8% of the European asset management industry in 2025, supported by growing retail participation and pension-linked investments. Managed assets exceeded USD 2.1 trillion. Mutual fund investments increased by 14%, while digital investment platform penetration reached 61%. Fixed income products accounted for 36% of Spanish investment portfolios. Renewable infrastructure investments and sustainable energy funds attracted significant institutional participation.

Italy

Italy accounted for nearly 10% of managed assets across Europe during 2025. Wealth management and private banking services remained dominant contributors, with HNWI investments representing 18% of national managed assets. Real estate-backed funds and infrastructure investments collectively exceeded USD 740 billion. ESG-linked portfolios expanded by 15%, while retirement-focused investment products accounted for 32% of allocations. Technology-enabled investment platforms increased retail participation by 17%.

Russia

Russia contributed approximately 6% of European managed investment assets in 2025 despite geopolitical challenges. Commodity-linked investments and energy-focused portfolios represented nearly 42% of domestic investment allocations. Institutional investors accounted for 63% of managed assets. Fixed income investments increased by 11% due to inflation-driven market conditions. Domestic financial institutions accelerated digital wealth management adoption, improving online investment participation by 19%.

Top players in Europe Asset Management

- BlackRock

- Amundi

- UBS Asset Management

- Allianz Global Investors

- BNP Paribas Asset Management

- Legal & General Investment Management

- Schroders

- DWS Group

- Nordea Asset Management

- AXA Investment Managers

- Generali Investments

- Pictet Asset Management

- HSBC Global Asset Management

- Invesco Europe

- M&G Investments

BlackRock

-

BlackRock accounted for approximately 8.7% of total European managed assets in 2025.

-

The company managed more than USD 2.4 trillion in European investment portfolios.

-

ESG-focused investment products represented nearly 34% of its European portfolio base.

-

AI-assisted investment analytics improved operational efficiency by 26%.

-

BlackRock expanded digital advisory services across France, Germany, and the United Kingdom, strengthening institutional client acquisition and ETF market leadership.

Amundi

-

Amundi represented nearly 6.9% of Europe’s managed investment assets during 2025.

-

The company managed approximately USD 1.9 trillion in diversified investment portfolios.

-

Sustainable investments contributed nearly 38% of total managed assets.

-

Amundi increased AI-enabled portfolio automation by 29%, improving client servicing capabilities.

-

Strong dominance in France and Southern Europe, along with strategic partnerships in digital wealth management, reinforced its competitive positioning within the European investment ecosystem.

Investment Analysis

Institutional investors allocated approximately 44% of total investment flows toward equity-oriented portfolios during 2025, while fixed income investments accounted for 31% and alternative investments represented 25%. ESG-oriented funds attracted nearly USD 1.8 trillion in new investments across Europe. France, Germany, and the United Kingdom collectively represented over 63% of regional investment allocations. Renewable infrastructure investments exceeded USD 620 billion, while private equity transactions surpassed USD 780 billion. Digital wealth management platforms received nearly 18% of total fintech investment funding across Europe.

Mergers and acquisitions within the European asset management sector accelerated significantly during 2025. More than 42 strategic acquisitions involving wealth management firms and fintech platforms were completed, representing transaction values exceeding USD 68 billion. Cross-border partnerships increased by 21%, driven by demand for AI-driven analytics and ESG compliance capabilities. Institutional investors allocated approximately 27% of alternative investment capital toward infrastructure modernization and green energy projects. Strategic alliances between banks and fintech firms improved digital portfolio management penetration by 24%. Additionally, private credit and real estate investments continued attracting long-term capital due to stable return profiles ranging between 7% and 10%.

New Product Developments

Asset management companies across Europe increasingly launched AI-driven and ESG-integrated investment products during 2025. Nearly 31% of newly introduced investment funds incorporated sustainability-linked performance metrics. Automated portfolio optimization systems improved investment customization by 28%, while cloud-enabled wealth management platforms reduced transaction processing time by 19%. Digital robo-advisory portfolios increased by 22%, supporting stronger retail investor participation.

Alternative investment products focused on renewable infrastructure, private equity, and green bonds witnessed strong expansion across Europe. Performance enhancements in predictive portfolio analytics improved risk-adjusted returns by 17%, while blockchain-supported fund reporting systems increased transparency efficiency by 24%. Institutional demand for inflation-protected and climate-oriented investment products continued driving financial innovation across the European asset management ecosystem.

Recent Developments in Europe Asset Management

- 2025: BlackRock expanded its ESG investment portfolio across Europe by 18%, increasing sustainable assets under management beyond USD 820 billion. The company introduced AI-enabled portfolio risk assessment systems that improved operational analytics efficiency by 24%, while ETF inflows across Europe rose by approximately 14%.

- 2025: Amundi launched a new climate-transition investment platform focused on renewable energy infrastructure projects valued at over USD 42 billion. The initiative increased institutional investor participation by 19% and improved sustainable investment allocations across France and Germany.

- 2025: BNP Paribas Asset Management strengthened blockchain-based fund reporting systems across European operations, improving transaction transparency efficiency by 23%. ESG-linked bond investments managed by the company increased by 15%, while digital wealth management accounts grew by 18%.

Research Methodology

The research methodology applied for the Europe asset management industry involved a combination of primary research, secondary research, and quantitative market estimation techniques. Primary research included interviews with portfolio managers, institutional investors, fintech executives, wealth advisors, pension fund operators, and regulatory experts across France, Germany, the United Kingdom, Italy, Spain, and Russia. Secondary research involved analysis of annual reports, financial disclosures, investment databases, regulatory filings, banking publications, and institutional investment statistics. Market size estimation utilized bottom-up and top-down analytical frameworks to evaluate assets under management, investment flows, portfolio allocations, digital adoption rates, and ESG investment penetration. Data triangulation methods were applied to validate institutional and retail investment statistics across multiple databases. Forecast models considered macroeconomic indicators, regulatory developments, technological adoption, inflation trends, fintech expansion, and sustainable investment penetration. The methodology also assessed investment allocation by asset class, client type, regional contribution, operational technology adoption, and portfolio diversification patterns to ensure accurate long-term market projections.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Fintech, Digital Payments, and Embedded Finance

Sara Wood is a market research analyst with 7–9 years of experience specializing in bfsi markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.