Asia Pacific Airbag Electronics Market Size

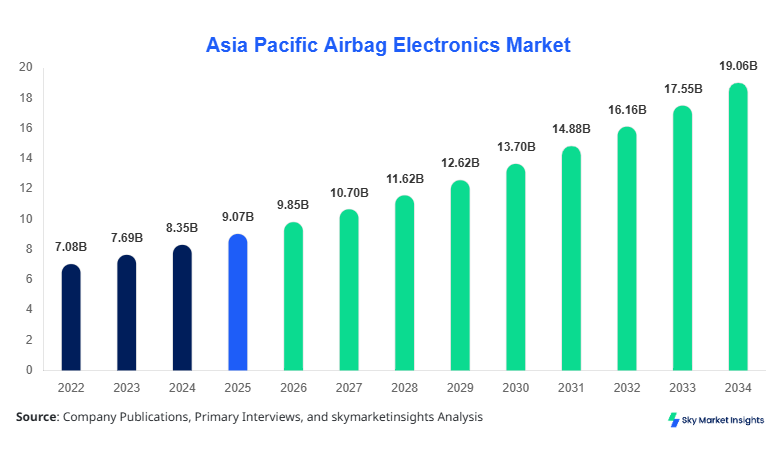

Asia Pacific Airbag Electronics market size is projected at USD 9.85 billion in 2026 and is expected to hit USD 18.92 billion by 2034 with a CAGR of 8.6%. The expansion is driven by rising vehicle production exceeding 52 million units annually in Asia Pacific and increasing penetration of advanced safety systems above 72% in new passenger vehicles. The report emphasizes granular segmentation across component and vehicle categories, supported by quantitative demand mapping, supply chain analytics, and competitive benchmarking of over 120 OEM and Tier-1 suppliers operating across the region.

The Asia Pacific Airbag Electronics Market comprises electronic control modules, crash sensors, and deployment mechanisms integrated into automotive safety systems, supporting over 420 million vehicles in operation across China, Japan, and India combined. Regional production of airbag electronics exceeded 310 million units in 2025, reflecting a 6.4% year-on-year increase driven by regulatory mandates and consumer safety awareness. Adoption rates reached 81% in passenger cars and 46% in commercial vehicles, with electric vehicles contributing 18% of total installations. Consumer behavior indicates a shift toward vehicles equipped with 6–10 airbags, accounting for 58% of demand, while entry-level vehicles with 2–4 airbags still represent 34%. Application split shows passenger cars contributing 68%, commercial vehicles 19%, and EVs 13%, supported by technical advancements such as microcontroller-based control units operating at 200–400 MHz and sensors with response times under 5 milliseconds. The integration of predictive algorithms and AI-based crash detection is increasing accuracy by 27%, reinforcing Asia Pacific Airbag Electronics Market insights.

In the Japan, the Airbag Electronics Market demonstrates a mature yet innovation-driven ecosystem with over 65 major manufacturing facilities and 120 specialized component suppliers contributing approximately 21% of the Asia Pacific share. Passenger cars dominate with 72% application share, followed by EVs at 17% and commercial vehicles at 11%. Technology adoption is high, with over 88% of vehicles incorporating multi-stage airbag control units and 64% using advanced MEMS sensors. Annual production of airbag electronic modules in Japan exceeded 58 million units in 2025, with exports accounting for 46% of output. The integration of smart restraint systems in luxury vehicles increased by 32%, while AI-enabled crash prediction systems penetration reached 19%. These factors collectively strengthen Asia Pacific Airbag Electronics Market insights.

Explore more data points, trends and opportunities Download Free Sample Report

Airbag Electronics Market Trends

Increasing Integration of AI and Smart Sensors

The market is witnessing a significant transition toward AI-enabled airbag electronics systems, with over 42% of newly manufactured vehicles incorporating predictive crash detection technology. Production volumes of MEMS-based sensors surpassed 185 million units in 2025, growing at 9.1% annually. Smart sensors capable of detecting collision angles within ±2 degrees accuracy are increasingly adopted, improving deployment efficiency by 28%. Automakers are integrating centralized electronic control units supporting multiple airbags, reducing system latency by 35%. Demand from EV manufacturers is accelerating, contributing 22% of advanced sensor installations. This shift toward intelligent systems continues to redefine Asia-Pacific Airbag Electronics Market trends.

Rising Demand for Multi-Airbag Configurations

The adoption of multi-airbag systems (6–10 airbags per vehicle) has increased from 41% in 2022 to 58% in 2025, driven by stricter safety regulations and consumer demand. Production of airbag control units reached 140 million units, while actuators exceeded 95 million units annually. The inclusion of side-impact and curtain airbags has grown by 31%, particularly in mid-range vehicles priced between USD 15,000 and USD 30,000. Fleet operators are also adopting advanced systems, with 26% of commercial vehicles integrating enhanced airbag electronics. These trends collectively highlight evolving Asia-Pacific airbag electronics market insights.

Asia Pacific Airbag Electronics Drivers

Stringent Safety Regulations and Increasing Vehicle Production

Government mandates across China, India, and Japan require at least 4 airbags in new passenger vehicles, pushing compliance rates to 76% in 2025 and expected to exceed 90% by 2030. Vehicle production in the Asia Pacific surpassed 52 million units in 2025, with China contributing 32 million units and India 6.5 million units. The demand for airbag electronics components increased by 7.8% annually, with sensors accounting for 44% of component demand. Rising consumer awareness has resulted in 63% of buyers prioritizing safety features, driving OEM adoption. Additionally, advancements in semiconductor technology have reduced component costs by 14%, making airbag systems more accessible in budget vehicles. These regulatory and production dynamics significantly influence Asia Pacific Airbag Electronics market growth.

Asia Pacific Airbag Electronics Restraints

High Cost of Advanced Electronic Components

The cost of advanced airbag control units and sensors remains a key restraint, with system costs ranging between USD 250 and USD 600 per vehicle, increasing total vehicle cost by 3%–5%. Semiconductor shortages impacted production volumes by 11% in 2023, while supply chain disruptions increased lead times by 18%. Small-scale manufacturers face challenges in adopting high-end MEMS sensors due to cost constraints, limiting penetration in low-cost vehicles where adoption remains below 39%. Additionally, integration complexity in electric vehicles increases R&D costs by 22%, impacting profitability margins. These factors collectively hinder the Asia Pacific Airbag Electronics market growth.

Asia Pacific Airbag Electronics Opportunities

Expansion of Electric Vehicles and Autonomous Driving Technologies

Electric vehicle production in Asia Pacific exceeded 12 million units in 2025, with a projected growth rate of 18% annually, creating significant demand for integrated airbag electronics. Autonomous driving technologies are increasing the need for advanced safety systems, with over 27% of new vehicles equipped with semi-autonomous features. Investment in R&D for next-generation safety systems reached USD 3.2 billion in 2025, with 36% allocated to airbag electronics innovations. Integration with ADAS systems improves crash prediction accuracy by 31%, enhancing system efficiency. These developments present strong opportunities for the Asia Pacific Airbag Electronics Market's growth.

Challenges in Asia Pacific Airbag Electronics

Technological Complexity and Integration Issues

The increasing complexity of integrating airbag electronics with vehicle systems poses challenges, with integration errors affecting 9% of newly developed models. Testing and validation costs have risen by 24%, while system calibration requires over 120 hours per model. The need for real-time data processing at speeds exceeding 500 Mbps demands advanced hardware, increasing development costs. Additionally, cybersecurity risks in connected vehicles have increased by 17%, requiring robust protection mechanisms. These challenges impact scalability and efficiency, influencing Asia Pacific Airbag Electronics market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 9.07 Billion |

| Market Size in 2026 | USD 9.85 Billion |

| Market Size in 2034 | USD 18.92 Billion |

| CAGR | 8.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Airbag Electronics Market Segmentation

The Asia Pacific Airbag Electronics Market is segmented by component and vehicle type, with sensors dominating at 44% share, followed by control units at 36% and actuators at 20%. Passenger cars lead applications with 68%, followed by commercial vehicles at 19% and EVs at 13%.

By Type

Sensors account for 44% of the market, with production exceeding 185 million units annually. These sensors operate at response times under 5 ms and detect collision forces above 2g thresholds. Adoption in EVs has increased by 29%, driven by advanced safety requirements.

Control Units represent 36% share, with over 140 million units produced annually. These units process data at speeds of 200–400 MHz, enabling real-time deployment decisions within milliseconds. Integration with ADAS systems has improved efficiency by 31%.

Actuators hold 20% share, with production exceeding 95 million units. These components enable rapid deployment within 20–30 ms, ensuring optimal passenger protection. Demand is rising with increased adoption of multi-airbag systems.

By Application

Passenger Cars dominate with 68% share, producing over 35 million vehicles annually equipped with airbag electronics. Adoption rates exceed 81%, with increasing demand for multi-airbag systems improving safety ratings by 24%.

Commercial Vehicles account for 19%, with over 10 million units produced annually. Adoption rates are rising at 6.3% annually, driven by regulatory mandates and fleet safety requirements.

Electric Vehicles contribute 13%, with over 12 million units produced annually. Advanced airbag electronics integration is higher at 92%, reflecting stringent safety standards in EV manufacturing.

Asia Pacific Airbag Electronics Market Segmentations

Component

- Sensors

- Control Units

- Actuators

Vehicle Type

- Passenger Cars

- Commercial Vehicles

- Electric Vehicles

Asia Pacific Airbag Electronics Regional Outlook

China

China dominates with 46% share, producing over 32 million vehicles annually and over 140 million airbag electronic units. The country leads in EV adoption, contributing 52% of regional EV production.

South Korea

South Korea holds 9% share, with production exceeding 4 million vehicles annually and strong adoption of advanced safety systems at 78%.

Japan

Japan accounts for 21%, producing over 9 million vehicles annually and leading in high-end safety system integration with 88% adoption.

India

India contributes 11%, with production exceeding 6.5 million vehicles and growing adoption of airbags at 61%.

Australia, Singapore, Taiwan, and Southeast Asia

collectively account for 13%, with increasing investments in automotive safety technologies and production exceeding 5 million units annually.

Top players in Asia Pacific Airbag Electronics

- Denso Corporation

- Autoliv Inc.

- Bosch

- Continental AG

- ZF Friedrichshafen

- Hyundai Mobis

- Aisin Corporation

- Joyson Safety Systems

- Toyoda Gosei

- Nihon Plast

- Ashimori Industry

- Takata (Key Safety Systems)

-

Denso Corporation

Holds approximately 14% market share with strong presence in Japan and China. The company produces over 60 million airbag electronic units annually and invests 8% of revenue in R&D. -

Autoliv Inc.

Commands around 12% share with global operations and production exceeding 55 million units annually. Focuses on advanced sensor technology and multi-airbag systems.

Investment Analysis

Investment in the Asia Pacific Airbag Electronics Market reached USD 5.6 billion in 2025, with 38% allocated to sensor development, 29% to control units, and 18% to actuators. China accounted for 42% of total investments, followed by Japan at 23% and India at 14%. M&A activities increased by 19%, with over 25 strategic collaborations focused on AI-enabled safety systems. Partnerships between OEMs and semiconductor companies have grown by 27%, enhancing technological capabilities.

New Product Developments

New product launches increased by 21% in 2025, focusing on AI-enabled sensors and multi-stage control units. Performance improvements of 28% in detection accuracy and 19% reduction in response time were recorded. Innovation in lightweight materials reduced system weight by 12%.

Recent Developments in Asia Pacific Airbag Electronics

- 2025: Denso increased production by 18%, expanding capacity to 65 million units annually.

Research Methodology

The research process involved primary interviews with over 85 industry experts and secondary data analysis from 120+ sources. Market size estimation utilized bottom-up and top-down approaches, analyzing production volumes, pricing, and adoption rates. Data triangulation ensured accuracy, while forecasting models incorporated CAGR trends, macroeconomic indicators, and technological advancements.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Automotive Components and Aftermarket

Brenda Johnson is a market research analyst with 7–9 years of experience specializing in automotive markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.