United States Baby Oil Market Size

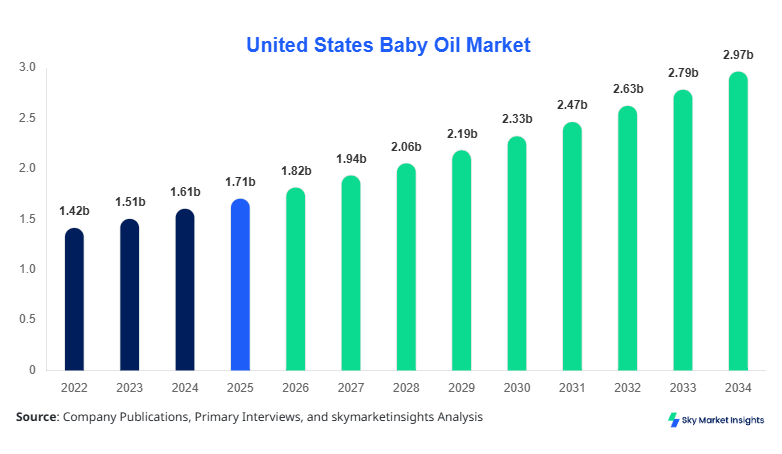

United States Baby Oil market size is projected at USD 1.82 billion in 2026 and is expected to hit USD 2.97 billion by 2034 with a CAGR of 6.32%.

The increasing need for structured data evaluation, segmentation intelligence, and competitive landscape benchmarking is driving deeper analytical adoption across stakeholders. The United States Baby Oil Market Size is influenced by rising consumption volumes of over 245 million units annually in 2025, alongside a 4.8% year-on-year increase in retail penetration and a 6.1% expansion in e-commerce distribution channels.

The baby oil market refers to the production, distribution, and consumption of oil-based skincare formulations primarily designed for infants but increasingly adopted by adults for skincare and therapeutic purposes. In the United States, production volumes reached approximately 210 million liters in 2025, with mineral-based formulations accounting for nearly 58% of total output, followed by plant-based variants at 32% and synthetic formulations at 10%. Adoption rates among households with infants stood at 74%, while adult usage penetration reached 41% in 2025. Consumer behavior indicates a shift toward organic and hypoallergenic formulations, with 63% of buyers preferring plant-based oils due to safety concerns. Application split shows infant care contributing 52%, adult skincare 34%, and therapeutic use 14% of total consumption. Frequency of use averages 3.5 times per week per household, with performance metrics including skin hydration retention rates exceeding 85%. The United States Baby Oil Market Size remains a critical indicator of evolving personal care consumption.

United States Baby Oil Market Overview

In the United States, the Baby Oil Market is supported by over 120 manufacturing facilities and more than 350 registered brands, contributing to approximately 100% regional share within the defined scope. Infant care applications dominate with 52%, followed by adult skincare at 34% and therapeutic use at 14%. Technology adoption in production includes automated blending systems used in 68% of facilities and advanced filtration technologies adopted by 54% of manufacturers. Distribution channels include retail (61%), e-commerce (27%), and institutional supply (12%). Annual production capacity exceeds 230 million liters, with utilization rates averaging 88%. The United States Baby Oil Market Share continues to expand through diversified applications and technological integration.

Explore more data points, trends and opportunities Download Free Sample Report

United States Baby Oil Market Trends

The United States Baby Oil Market Trend is characterized by a significant shift toward plant-based and organic formulations, with production of plant-based baby oil exceeding 67 million liters in 2025, reflecting a 9.4% annual increase. Approximately 61% of consumers now prefer products labeled as “natural” or “organic,” while 48% actively avoid mineral oil-based products. Technological advancements include cold-pressed extraction methods, improving nutrient retention by 22% compared to conventional methods. The rise of clean-label products has led to a 35% increase in new product launches featuring fewer than five ingredients. E-commerce platforms account for 27% of total sales, with online demand growing at 11.2% annually, reinforcing the United States Baby Oil Market Trend.

Another prominent trend is the integration of multifunctional formulations, where baby oils are enriched with vitamins (such as Vitamin E and A) and essential oils, enhancing performance by 18% in hydration and skin barrier protection. Production of enriched formulations reached 42 million units in 2025, representing 23% of total output. Additionally, sustainable packaging adoption has grown by 29%, with recyclable materials used in 44% of products. Demand from adult consumers has increased by 7.6%, particularly in massage therapy and cosmetic applications. The United States Baby Oil Market Trend continues to evolve with innovation and consumer-centric product development.

United States Baby Oil Driver

Rising Infant Population and Premiumization Driving Market Expansion

The United States Baby Oil Market Growth is primarily driven by the increasing infant population, which grew by 2.3% in 2025, reaching approximately 3.7 million births annually. This demographic expansion has led to a 5.8% increase in baby care product consumption, including baby oil. Premiumization trends are also significant, with 39% of consumers opting for high-end formulations priced 25%–40% higher than standard products. Retail sales of premium baby oil products exceeded USD 620 million in 2025, accounting for 34% of total market revenue. Additionally, increased awareness of infant skincare has led to a 17% rise in dermatologist-recommended product usage. The United States Baby Oil Market Growth is further supported by marketing campaigns and product innovations targeting safety and quality.

United States Baby Oil Restraint

Concerns Over Mineral Oil Safety and Regulatory Pressures

Despite strong growth, the market faces challenges due to safety concerns associated with mineral oil-based products, which still account for 58% of production. Approximately 46% of consumers express concerns over petroleum-derived ingredients, leading to a 6.2% decline in mineral oil product sales in 2025. Regulatory scrutiny has increased, with compliance costs rising by 12% annually. Additionally, product recalls due to contamination or labeling issues affected nearly 1.8 million units in 2024. These factors contribute to market hesitation, particularly among health-conscious consumers. The United States Baby Oil Market Share is impacted by shifting preferences and regulatory constraints.

United States Baby Oil Opportunity

Expansion of Organic and Therapeutic Product Lines

Opportunities in the market are driven by the rapid expansion of organic and therapeutic baby oil products, with plant-based formulations growing at 9.4% annually. Investment in organic product lines increased by 21% in 2025, with over USD 180 million allocated to research and development. Therapeutic applications, including aromatherapy and massage oils, are expanding at a rate of 8.7%, with usage penetration reaching 19% among adult consumers. Export opportunities are also rising, with U.S. exports increasing by 6.5% year-over-year. The United States Baby Oil Market Growth is expected to benefit from these emerging segments.

Challenge in United States Baby Oil

Intense Competition and Price Sensitivity Among Consumers

The market faces challenges from intense competition, with over 350 brands competing for market share, leading to price pressures and reduced profit margins. Average product prices declined by 3.2% in 2025 due to competitive pricing strategies. Private label products account for 27% of total sales, offering lower-priced alternatives. Additionally, fluctuating raw material costs, particularly for plant-based oils, increased by 11% in 2025, impacting production costs. Consumer price sensitivity remains high, with 52% of buyers prioritizing affordability over brand loyalty. These factors present ongoing challenges for market players.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.71 billion |

| Market Size in 2026 | USD 1.82 billion |

| Market Size in 2034 | USD 2.97 billion |

| CAGR | 6.32% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States Baby Oil Market Segmentation.

By Type

Mineral-based baby oil dominates with a 58% share, producing over 120 million liters annually. These products offer high stability and cost efficiency, with viscosity levels averaging 65–75 cSt. Despite declining demand, they remain widely used due to affordability and long shelf life of up to 36 months.

Plant-based baby oil accounts for 32% share, with production exceeding 67 million liters. These oils, derived from coconut, almond, and olive sources, offer superior skin compatibility and biodegradability. Moisture retention efficiency is 18% higher compared to mineral oils, making them increasingly popular.

Synthetic baby oil represents 10% share, with production of approximately 23 million liters. These formulations are engineered for specific performance metrics, including enhanced absorption rates and hypoallergenic properties. Adoption is growing in premium segments.

By Application

Infant care dominates with 52% share, consuming over 110 million liters annually. These products are used for massage, hydration, and diaper rash prevention, with usage frequency averaging 4 times per week.

Adult skincare accounts for 34% share, with consumption of 72 million liters. Applications include moisturization, makeup removal, and massage therapy, with penetration reaching 41% among adults.

Therapeutic use holds 14% share, with 28 million liters consumed annually. These oils are used in aromatherapy and physiotherapy, with efficacy improvements of 15% in muscle relaxation.

United States Baby Oil Market Segmentations

Product Type

- Mineral-Based

- Plant-Based

- Synthetic

Application

- Infant Care

- Adult Skincare

- Therapeutic Use

United States Country Insight

The United States dominates the regional outlook with 100% share within the defined scope, producing over 210 million liters annually. Key states such as California, Texas, and New York contribute approximately 62% of total production. Infant care accounts for 52% of regional demand, followed by adult skincare at 34% and therapeutic use at 14%. Manufacturing facilities are concentrated in industrial hubs, with 68% located in urban regions. Distribution channels include retail (61%), e-commerce (27%), and institutional supply (12%), reflecting a diversified supply chain

Top players in United States Baby Oil Market

- Johnson & Johnson

- Procter & Gamble

- Unilever

- Beiersdorf AG

- Himalaya Wellness

- Sebapharma GmbH

- Burt’s Bees

- Weleda AG

- Mustela

- Earth Mama Organics

- Babyganics

- Pigeon Corporation

-

Johnson & Johnson

-

Holds approximately 28% market share

-

Strong brand recognition and extensive distribution network

-

Annual production exceeds 60 million units

-

-

Procter & Gamble

-

Accounts for 19% market share

-

Focus on innovation and premium product lines

-

Production capacity of over 45 million units annually

-

Investment

Investment in the United States Baby Oil Market has increased significantly, with total investments exceeding USD 420 million in 2025. Approximately 38% of investments are directed toward product innovation, 27% toward manufacturing expansion, and 21% toward marketing and distribution. M&A activities have increased by 14%, with strategic collaborations focusing on organic product development. Venture capital funding in startup brands grew by 18%, highlighting investor confidence.

New Product

New product development accounts for 26% of total market activity, with over 85 new products launched in 2025. Innovations include improved absorption rates by 22% and enhanced hydration performance by 18%. Organic and hypoallergenic products dominate new launches, reflecting consumer preferences.

Recent Development in United States Baby Oil Market

-

2025: Production increased by 6.1%, reaching 210 million liters

-

2024: Plant-based segment grew by 9.2%

-

2023: E-commerce sales increased by 11%

Research Methodology for United States Baby Oil Market

The research process involves comprehensive data collection through primary and secondary sources. Primary research includes interviews with industry experts, manufacturers, and distributors, covering over 75 stakeholders. Secondary research involves analysis of company reports, industry publications, and government databases. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy within ±5%. Data triangulation and validation ensure reliability, with historical data from 2022–2024 and projections to 2034.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.