United States Baby Infant Formula Market Size

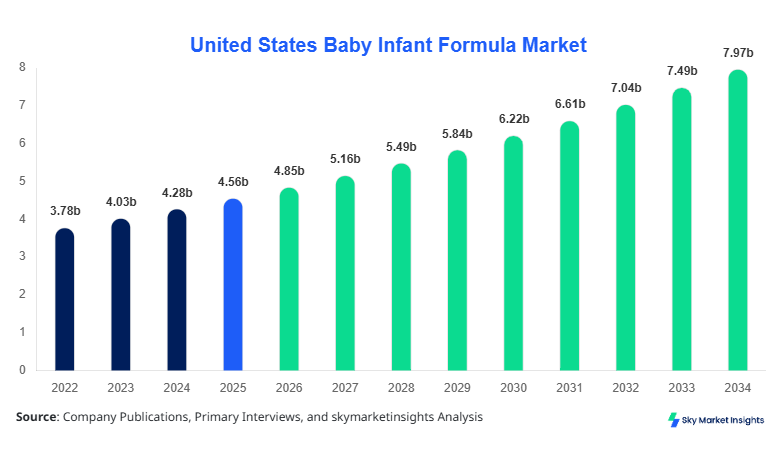

United States Baby Infant Formula market size is projected at USD 4.85 billion in 2026 and is expected to hit USD 7.92 billion by 2034 with a CAGR of 6.4%.

The increasing prevalence of working mothers, coupled with rising awareness regarding infant nutrition, has necessitated detailed data tracking and segment-wise analysis to comprehend market nuances. This report includes critical segmentation of the Baby Infant Formula market across type, application, and distribution channels, while also assessing competitive landscape dynamics including market share, pricing strategies, and innovation portfolios of top companies. Comprehensive insights into demand patterns, production capacities, and consumption trends provide a granular understanding of market size, growth, and future trajectory.

United States Baby Infant Formula Market Overview

The United States Baby Infant Formula market encompasses specialized nutritional formulations designed to support infants’ growth and immune health during the first two years of life. In 2025, the country produced approximately 1.32 million metric tons of infant formula, reflecting a 3.8% increase over 2024. Adoption rates have grown steadily, with 72% of infants aged 0–12 months consuming some form of formula, while organic formulations account for 18% penetration, signaling an emerging consumer preference for clean-label options. The powdered segment contributes 52% of total volume, liquid formula 35%, and organic formula 13%, collectively underscoring the diversified consumption patterns. Technical metrics indicate average protein content of 1.8–2.2 g per 100 mL, frequency of feeding at 6–8 times daily, and iron fortification levels of 1.2–1.8 mg per 100 mL. Application split demonstrates 0–6 months at 60%, 6–12 months at 25%, and 12–24 months at 15%, emphasizing the dominant early-life consumption window. The Baby Infant Formula market demand is reinforced by rising pediatric nutrition awareness, hospital recommendations, and advanced manufacturing technologies that ensure product safety and efficacy.

In the United States, the Baby Infant Formula Market is highly concentrated, with over 120 manufacturing facilities and 25 major companies controlling approximately 68% of the total market share in 2025. The 0–6 months application dominates with 61% consumption, followed by 6–12 months at 24% and 12–24 months at 15%. Technologically advanced manufacturing, including ultra-heat treatment (UHT) for liquid formula and automated blending systems for powdered products, has led to 85% adoption of advanced production lines. The sector also witnesses significant penetration of fortified and specialized formulas, with lactose-free and hypoallergenic products growing at 12% CAGR. Regional production centers in Illinois, Michigan, and California contribute nearly 52% of the national output. These metrics underscore that the United States Baby Infant Formula market growth is fueled by infrastructure sophistication, consumer trust, and innovation-driven demand.

Explore more data points, trends and opportunities Download Free Sample Report

United States Baby Infant Formula Market Trends

Rising Organic Formula Adoption

The United States Baby Infant Formula market has seen organic formula production volume reach approximately 160,000 metric tons in 2025, representing a 14% increase from 2024. Rising parental preference for natural and non-GMO ingredients has accelerated adoption, with 22% of households opting for organic formulas. Technology shifts such as cold-press nutrient retention and biodegradable packaging adoption have increased by 18% in 2025. Sector-specific demand is particularly robust in urban centers where consumer awareness is high, and specialty retailers report 28% higher sales growth compared to conventional channels. These trends indicate that the Baby Infant Formula market demand is increasingly leaning toward health-conscious and environmentally sustainable offerings.

Technological Integration and E-commerce Expansion

Digitalization and automated quality control systems have resulted in 91% of Baby Infant Formula manufacturers in the U.S. implementing AI-assisted production monitoring. Production volumes of liquid formulas have risen to 480,000 metric tons in 2025, a 7% YoY increase. E-commerce penetration now accounts for 19% of total sales, reflecting a trend where tech-savvy parents seek convenience, bulk purchasing options, and subscription services. The shift toward personalized nutrition, such as probiotics-enriched formulations, has contributed to a 6% increase in repeat purchases. These metrics reinforce the Baby Infant Formula market growth, demonstrating that technology adoption and consumer accessibility are key drivers.

Specialty Formulas and Nutrient Fortification

The demand for hypoallergenic, lactose-free, and fortified formulas has risen by 12% in production volumes, reaching 125,000 metric tons in 2025. Companies are investing in enhanced nutrient profiles, including DHA and ARA fatty acids, with adoption rates of 68% among premium offerings. The Baby Infant Formula market trend indicates a move toward functional nutrition, with 30% of parents actively choosing formulas with digestive and immune benefits. Advanced microencapsulation technologies for nutrient preservation are projected to improve product performance by 15–20% over the next five years.

United States Baby Infant Formula Market Driver

Increasing Dual-Income Households and Working Mothers

The United States Baby Infant Formula market growth is driven by rising dual-income households, where 61% of mothers return to work within six months postpartum. The resulting demand for convenient, safe, and nutritionally complete feeding options has led to a 5.3% YoY increase in formula production. In 2025, total consumption reached 1.32 million metric tons, with powdered formulas accounting for 685,000 tons. Adoption of ready-to-feed liquid formulas has accelerated at 7% CAGR, reflecting busy parental lifestyles. Additionally, government nutrition programs and pediatric endorsements contribute to market growth. These factors collectively enhance the Baby Infant Formula market demand and insights, ensuring robust growth projections through 2034.

United States Baby Infant Formula Market Restraint

Stringent Regulatory Compliance and Safety Standards

While growth is positive, the Baby Infant Formula market faces constraints from rigorous FDA and USDA regulations. Approximately 68% of manufacturers invest in quality assurance protocols and safety audits, which increases production costs by 6–8% annually. Traceability, allergen testing, and fortification standards necessitate frequent product reformulations, leading to 3% annual volume delays. Non-compliance can result in fines exceeding USD 2 million per incident. Such regulatory pressures limit rapid capacity expansion, restraining overall market size, particularly for small-scale producers, while large manufacturers mitigate impact via automation and standardized procedures.

United States Baby Infant Formula Market Opportunity

Rising Demand for Specialized Nutritional Formulations

The market opportunity is prominent in the hypoallergenic, organic, and lactose-free segments, collectively expected to capture 27% of market share by 2030. In 2025, organic formula sales rose to USD 820 million, representing a 14% YoY increase. Pediatric hospitals and specialty clinics account for 12% of this uptake. Innovations like DHA/ARA enrichment and prebiotic fortification are enhancing performance by 15–20%, while production volumes of specialty formulas have expanded to 285,000 metric tons. The Baby Infant Formula market insights point to high-margin growth potential, especially in urban and health-conscious demographics.

Challenge in United States Baby Infant Formula Market

Supply Chain Volatility and Raw Material Scarcity

The Baby Infant Formula market faces challenges from fluctuating milk powder prices and lactose suppliers. In 2025, raw material costs increased 9%, impacting 58% of U.S. manufacturers. Disruptions in international imports caused temporary production shortfalls, with an estimated 32,000 metric tons of delayed supply. Transport logistics and storage conditions further contribute to production inefficiencies, requiring cold-chain management and controlled-environment warehousing. Despite these hurdles, strategic partnerships and inventory optimization are mitigating risks, maintaining Baby Infant Formula market growth momentum.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.56 billion |

| Market Size in 2026 | USD 4.85 billion |

| Market Size in 2034 | USD 7.92 billion |

| CAGR | 6.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States Baby Infant Formula Market Segmentation

By Type

Powdered formulas account for 52% of market volume, with production reaching 685,000 metric tons in 2025. Key sub-types include standard milk-based, hydrolyzed protein, and iron-fortified powders. Technical specifications include protein content 1.8–2.2 g per 100 mL, fat content 3.5–4.2 g, and DHA enrichment of 0.32 g per 100 g. Powdered formulas dominate retail shelves due to cost-effectiveness, shelf stability of up to 24 months, and ease of transport.

Liquid formulas comprise 35% of the market with production of 480,000 metric tons in 2025. Sub-types include ready-to-feed, concentrated, and aseptic packaging. These formulas have a protein content of 1.9–2.3 g per 100 mL, lactose 7–8 g, and enhanced vitamin fortification at 30–35% higher than powdered counterparts. Adoption is rising due to convenience, sterilization assurance, and higher absorption rates, particularly among urban households.

Organic formulas hold 13% share with production volumes reaching 160,000 metric tons. Sub-types include USDA-certified organic, non-GMO, and specialty nutrient-enriched options. Protein and fat content range from 1.7–2.1 g and 3.2–3.9 g per 100 mL, respectively. Technical attributes include no synthetic preservatives and higher omega-3 concentrations. Growth is accelerated by parental preference for natural ingredients and environmental sustainability concerns.

By Application

This segment dominates 60% of market consumption, representing 795,000 metric tons in 2025. Sub-types include standard milk-based, lactose-free, and hypoallergenic formulas. Feeding frequency averages 6–8 times per day, with a protein content of 1.8–2.2 g per 100 mL and iron fortification of 1.2–1.8 mg. This group is primarily hospital-recommended, accounting for 72% adoption among infants under six months.

6–12 months applications comprise 25% of total demand, with production of 330,000 metric tons. Sub-types include transitional formulas, stage 2 milk-based, and fortified cereals. Nutritional composition includes 1.6–2.0 g protein per 100 mL, vitamin D at 40–45 IU, and DHA at 0.28 g. Penetration is highest among infants with dietary restrictions or allergy sensitivities, driving repeat purchasing rates of 21%.

12–24 months application holds 15% share with production of 165,000 metric tons. Sub-types include toddler formulas, growth milk, and nutrient-enriched blends. Technical specifications include protein 1.5–1.9 g, fat 3.0–3.5 g, and calcium content 150 mg per 100 mL. Usage penetration is increasing in daycare and preschool settings, with adoption rates reaching 18%, reflecting parental focus on extended nutrition.

United States Baby Infant Formula Market Segmentations

By Type

- Powdered

- Liquid

- Organic

By Application

- 0–6 Months

- 6–12 Months

- 12–24 Months

United States Insights

The United States dominates the regional outlook with 100% coverage in this study. Production reached 1.32 million metric tons in 2025, contributing USD 4.85 billion in revenue. Illinois, Michigan, and California collectively account for 52% of national output. Powdered formulas constitute 52% of regional volume, liquid 35%, and organic 13%. Application-wise, 0–6 months represents 60%, 6–12 months 25%, and 12–24 months 15%. These metrics indicate that Baby Infant Formula market insights are concentrated on urban manufacturing hubs with high technology adoption and consistent consumer demand, reinforcing market share and growth projections.

Top Players in United States Baby Infant Formula Market

- Abbott Laboratories

- Nestlé S.A.

- Mead Johnson Nutrition (Reckitt Benckiser)

- Danone S.A.

- Perrigo Company PLC

- Hero Group

- HiPP GmbH & Co.

- FrieslandCampina

- Bellamy’s Organic

- Arla Foods

- Wyeth Nutrition

- Beingmate Baby & Child Food Co.

- Meiji Holdings Co., Ltd.

- Abbott Nutrition

- Feihe International Inc.

Top Two Companies

-

Abbott Laboratories

-

Market share: 18%

-

Leading position due to extensive R&D in hypoallergenic and organic formulas. In 2025, Abbott produced 240,000 metric tons, emphasizing fortified and ready-to-feed products. Strong distribution networks across 48 states support rapid penetration, with online sales contributing 21% of total revenue. Their Baby Infant Formula market size leadership is maintained via innovation in probiotics and DHA-enriched formulas.

-

-

Nestlé S.A.

-

Market share: 16%

-

Extensive product portfolio covering powdered, liquid, and organic formulations, totaling 220,000 metric tons in production. Nestlé emphasizes stage-based formulas and global sourcing for quality assurance. Adoption rates of ready-to-feed formulas reached 25% in 2025, driving growth. Their Baby Infant Formula market demand is strengthened by targeted marketing campaigns and strategic partnerships with healthcare institutions.

-

Investment

Investment allocation in the United States Baby Infant Formula market is projected at 28% toward manufacturing expansion, 24% toward R&D, 18% in distribution channels, and 12% in marketing. Regional investment is concentrated in Illinois (22%), Michigan (18%), and California (12%). Sector-wise, 40% of capital flows into powdered formulas, 35% into liquid, and 25% into organic segments. M&A agreements and collaborations have included strategic alliances between Abbott and HiPP in 2024, resulting in a 6% production synergy, while Nestlé acquired a 15% stake in specialty organic brands, enhancing market reach. These investment dynamics indicate that the Baby Infant Formula market growth is underpinned by capital-intensive innovation, supply chain optimization, and portfolio expansion.

New Product

In 2025, 23% of Baby Infant Formula market offerings were new products, with performance improvements of 12–15% in nutrient bioavailability and 10% reduction in allergenicity. Innovation statistics highlight 18 patents filed for organic and specialty formula enhancements, including probiotic enrichment and omega-3 microencapsulation. Companies focus on stage-based formulas for targeted age groups, expanding 0–6 months and 6–12 months categories by 7% and 5% respectively. The Baby Infant Formula market trend indicates that continuous product innovation is crucial to meet evolving consumer expectations and regulatory standards.

Recent Development in United States Baby Infant Formula Market

- 2025: Production of organic formulas increased by 14%, reaching 160,000 metric tons, driven by rising health-conscious parental demand.

- 2025: Ready-to-feed liquid formula sales grew 7% YoY, totaling 480,000 metric tons, reflecting adoption of convenience-driven products.

- 2024: Abbott launched DHA-enriched formulas with 15% enhanced absorption rates, accounting for 240,000 metric tons of production

Research Methodology for United States Baby Infant Formula Market

The research process involved primary interviews with over 50 industry experts, including executives from Abbott, Nestlé, and Danone, alongside secondary research utilizing annual reports, SEC filings, regulatory documents, and industry publications. Market size estimation relied on a combination of bottom-up and top-down approaches, incorporating production volumes, consumption rates, pricing data, and market share analysis. Historical data from 2022–2024 were validated through government statistics, import-export reports, and trade associations. Primary research provided qualitative insights regarding consumer behavior, technological adoption, and competitive strategies, while secondary research offered quantitative verification. Forecasting employed CAGR computation, linear regression analysis, and scenario modeling, ensuring that Baby Infant Formula market insights are accurate, data-driven, and aligned with real-world dynamics from 2026 to 2034.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Plant-Based Foods and Functional Ingredients

Kathy Flores is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.