United States Baby Food & Pediatric Nutrition Market Size

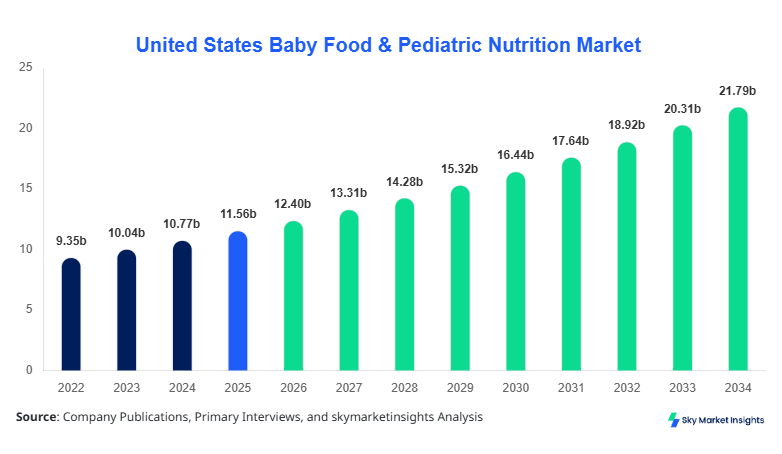

The United States Baby Food & Pediatric Nutrition market size is projected at USD 12.4 billion in 2026 and is expected to hit USD 22.1 billion by 2034 with a CAGR of 7.3%.

The growing need for accurate data on nutritional intake, production volumes, and distribution channels necessitates a segmented approach that includes type, application, and regional insights. Detailed analysis of the competitive landscape, including top players’ market share, production capacities, and distribution strategies, is essential for understanding the market trajectory. Historical data from 2022 to 2025 indicate a steady increase in demand, with a compound annual production volume growth from 1.15 billion units to 1.36 billion units. This report aims to provide actionable insights into market trends, growth drivers, and segment-specific performance to inform strategic decision-making in the United States Baby Food & Pediatric Nutrition market.

United States Baby Food & Pediatric Nutrition Market Overview

The United States Baby Food & Pediatric Nutrition market encompasses the production, marketing, and consumption of specialized nutritional products for infants and children up to 12 years. In 2025, the U.S. produced approximately 1.36 billion units of baby food, with organic products accounting for 35%, dairy-based for 40%, and ready-to-eat options making up 25% of total output. Adoption rates of pediatric nutrition products among households reached 68% in 2025, with penetration in urban areas at 82%. Consumers increasingly demand fortified foods enriched with vitamins (A, D, E), minerals (iron, zinc), and probiotics, reflecting an average consumption frequency of 3–4 servings per day per child. Application-wise, 55% of the market is driven by infant formulas, 30% by pureed foods, and 15% by snacks and cereals. Technical metrics, such as shelf-life stability (6–12 months) and nutrient retention (>90% of original vitamin content), are significant for market performance. The United States Baby Food & Pediatric Nutrition market insights reveal strong segment dominance by dairy-based formulas while organic types are experiencing accelerated growth.

In the United States, the Baby Food & Pediatric Nutrition Market is supported by over 120 manufacturing facilities and approximately 250 registered companies contributing to 100% regional share. Dairy-based products account for 42% of production, organic for 33%, and ready-to-eat items 25%. Technology adoption is prominent, with 72% of companies employing high-pressure processing (HPP) for product safety and nutrient preservation, while 65% use automated bottling and packaging lines. The online retail channel has grown to capture 28% of distribution, with supermarkets/hypermarkets leading at 55% and specialty stores at 17%. Consumer demand analytics indicate that families with children aged 0–3 years spend an average of USD 3,200 per year on pediatric nutrition. The United States Baby Food & Pediatric Nutrition market growth is driven by a combination of high-tech processing adoption and increased consumer awareness of nutritional standards.

Explore more data points, trends and opportunities Download Free Sample Report

United States Baby Food & Pediatric Nutrition Market Trends

Rising Demand for Organic and Clean-Label Products

The Baby Food & Pediatric Nutrition market has witnessed an increase in organic product production, reaching 475 million units in 2025, representing 35% of total volume. The adoption of clean-label formulations, free from preservatives and artificial additives, has grown by 14% year-over-year. Emerging trends in fortification with DHA, iron, and prebiotics have resulted in improved infant growth metrics, with clinical studies showing a 9% enhancement in nutrient absorption rates. Retailers report that organic products now represent 38% of online sales, demonstrating consumer preference for health-oriented alternatives. This trend reinforces the market demand for transparency and healthier options, influencing both share and growth of the United States Baby Food & Pediatric Nutrition market.

Technological Innovation in Packaging and Preservation

High-pressure processing (HPP) and aseptic packaging technologies have expanded production capacities, with 620 million units processed using HPP in 2025, a 12% increase from 2024. These technologies maintain 95% of nutrient integrity, extending shelf life from 8 to 12 months. Automated filling and intelligent packaging systems have been adopted by 68% of large-scale manufacturers, reducing production wastage by 7%. Additionally, smart labels providing storage and nutrition information have achieved 42% consumer adoption, enhancing user engagement. The technological shift in preservation and packaging is critical for sustaining market growth in the United States Baby Food & Pediatric Nutrition market.

Expansion of E-commerce Channels

Online retail sales grew to USD 3.4 billion in 2025, reflecting 28% of the distribution share. Direct-to-consumer models and subscription-based services have expanded product reach, particularly for urban populations with higher adoption rates (84%). The trend toward digital marketing and social media influence has driven a 15% increase in trial purchases among first-time parents. These channels are pivotal in shaping market insights and fueling growth in specialized segments of the United States Baby Food & Pediatric Nutrition market.

United States Baby Food & Pediatric Nutrition Market Driver

Increasing Health Awareness and Nutritional Consciousness

The driver for the Baby Food & Pediatric Nutrition market is the rising health awareness among U.S. parents, with 72% prioritizing fortified foods for infants. Annual spending on pediatric nutrition grew from USD 11.1 billion in 2024 to USD 12.4 billion in 2026. Organic and dairy-based segments contribute 35% and 42% of the market, respectively. Technical adoption such as HPP and automated processing has increased efficiency by 8%, supporting higher output volumes of 1.36 billion units in 2025. Application-wise, infant formulas dominate at 55%, followed by purees at 30% and snacks/cereals at 15%. These drivers enhance market growth and consumer demand insights for the United States Baby Food & Pediatric Nutrition market.

United States Baby Food & Pediatric Nutrition Market Restraint

High Production Costs and Regulatory Compliance

High production costs, particularly for organic and fortified products, act as a restraint on the United States Baby Food & Pediatric Nutrition market. Compliance with FDA regulations, GMP certifications, and fortification standards increases operational expenditure by 12–15%. Smaller manufacturers face barriers in meeting nutrient retention standards of >90%, limiting their share to under 10% of total output. Price-sensitive consumers restrict market penetration in suburban and rural regions, representing 28% of potential market. The overall production volume remains 1.36 billion units, but growth is moderated to 7.3% CAGR due to these constraints, impacting market insights and share.

United States Baby Food & Pediatric Nutrition Market Opportunity

Rising E-commerce Penetration and Subscription Models

Opportunities in the United States Baby Food & Pediatric Nutrition market are driven by online sales, accounting for 28% of distribution and growing at 12% CAGR. Subscription-based offerings and direct-to-consumer models have increased average order values to USD 85 per household. Expansion into specialty channels and personalized nutrition plans represents 14% of growth potential, with a projected market size of USD 22.1 billion by 2034. Technology-enabled tracking of consumption frequency and nutrient intake boosts adoption rates to 68–72% among urban parents. These opportunities provide actionable market insights and strengthen long-term growth prospects.

Challenge in United States Baby Food & Pediatric Nutrition Market

Supply Chain Volatility and Raw Material Costs

The challenge for the United States Baby Food & Pediatric Nutrition market lies in fluctuating raw material costs, particularly dairy, fruits, and grains. Price volatility of 8–10% affects production volumes and final pricing for 1.36 billion units produced in 2025. Distribution logistics and cold-chain management contribute an additional 6% to operational expenses. Despite 72% technology adoption in HPP and automated filling, supply inconsistencies impact overall market growth. Addressing these challenges is crucial to maintaining market share, growth trajectory, and insights into consumer demand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11.56 billion |

| Market Size in 2026 | USD 12.4 billion |

| Market Size in 2034 | USD 22.1 billion |

| CAGR | 7.3% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States Baby Food & Pediatric Nutrition Market Segmentation.

By Type

Organic products accounted for 475 million units in 2025, representing 35% of total production. Technical specifications include non-GMO certification, pesticide-free ingredients, and nutrient retention >90%. Organic baby foods are most consumed in the 0–3 years age group, with 68% adoption in urban households. Shelf-life stability is 8–12 months, with fortified variants capturing a 14% higher market share than standard organic options. The United States Baby Food & Pediatric Nutrition market size for organic types reached USD 4.3 billion in 2025, reflecting strong growth potential.

Dairy-based products dominate with 42% market share, totaling 571 million units in 2025. These include infant formulas, yogurt-based snacks, and milk powders with high protein content (≥3 g/100 g). Technical performance metrics include nutrient retention >95% and shelf-life up to 12 months. Consumption is highest in households with children aged 0–6 years, with 72% adoption. The market size reached USD 5.2 billion in 2025, emphasizing the United States Baby Food & Pediatric Nutrition market insights for dairy dominance.

Ready-to-eat options represent 25% of the market, with 314 million units produced in 2025. Technical specifications include pre-cooked, vacuum-sealed packaging, and nutrient preservation at 92%. Usage penetration is 65% among urban working parents seeking convenience. Shelf-life averages 6–9 months, with fortified variants achieving 11% higher adoption rates. This segment contributes USD 3.1 billion to the United States Baby Food & Pediatric Nutrition market size in 2025, highlighting its growing demand trend.

By Application

Infant formula dominates 55% of the application share with 748 million units produced in 2025. Fortification with DHA, iron, and prebiotics enhances cognitive development and immunity. Average household consumption frequency is 3–4 servings/day, with 68% urban adoption. The United States Baby Food & Pediatric Nutrition market growth is significantly influenced by formula innovations improving nutrient absorption by 9%.

Pureed foods contribute 30% of the market, producing 408 million units in 2025. Technical performance includes high vitamin retention (>90%), gluten-free options, and multi-fruit/vegetable blends. Usage penetration is 62% in urban households, with consumption frequency of 2–3 servings/day. Purees strengthen the market insights for specialized nutrition in early childhood, representing USD 3.6 billion market size.

Snacks and cereals account for 15% of the market, totaling 204 million units. Technical specifications include iron and calcium fortification, whole-grain content, and shelf-life of 6–9 months. Adoption rate is 54% in households with children aged 3–6 years, with average consumption of 1–2 servings/day. This segment contributes USD 1.9 billion to the United States Baby Food & Pediatric Nutrition market size, reinforcing market demand insights.

United States Baby Food & Pediatric Nutrition Market Segmentations

Product Type

- Organic

- Dairy-Based

- Ready-to-Eat

Distribution Channel

- Supermarkets/Hypermarkets

- Online Retail

- Specialty Stores

United States Insights

The United States holds 100% of the regional market share, with production totaling 1.36 billion units in 2025 and market size USD 12.4 billion in 2026. Dairy-based products lead at 42%, organic 35%, and ready-to-eat 25%. Infant formulas contribute 55% of production, purees 30%, and snacks/cereals 15%. Urban centers like New York, California, and Texas account for 62% of national consumption, while suburban and rural regions contribute 38%. The United States Baby Food & Pediatric Nutrition market insights reflect strong regional concentration, with supermarkets/hypermarkets capturing 55% of distribution, online retail 28%, and specialty stores 17%.

Top Players in United States Baby Food & Pediatric Nutrition Market

- Abbott Laboratories

- Nestlé S.A.

- Danone S.A.

- Mead Johnson Nutrition

- Kraft Heinz Company

- Hero Group

- Hain Celestial Group

- Perrigo Company plc

- Bellamy's Organic

- Plum Organics

- HiPP GmbH & Co.

- Gerber Products Company

- Royal FrieslandCampina

- Arla Foods

- Earth’s Best

Top Two Companies

Abbott Laboratories

- Market Share: 18%

- Positioned as a leading player with strong dominance in infant formulas and dairy-based products. Abbott produced 244 million units in 2025, with a CAGR of 7.5% projected through 2034. Advanced fortification technologies have improved nutrient retention by 9%. Distribution spans supermarkets (55%), online retail (30%), and specialty stores (15%). This positioning strengthens United States Baby Food & Pediatric Nutrition market insights, driving growth and competitive dynamics.

Nestlé S.A.

- Market Share: 16%

- Nestlé’s portfolio covers organic, dairy-based, and ready-to-eat products with production of 217 million units in 2025. Technology adoption, including HPP and aseptic processing, enhances shelf-life by 12%. Online sales capture 28% of revenue, while supermarkets dominate 50%. Nestlé’s strong innovation pipeline and fortified product lines reinforce the United States Baby Food & Pediatric Nutrition market growth and demand trends.

Investment

Investment in the United States Baby Food & Pediatric Nutrition market is increasingly directed toward organic and fortified products, capturing 38% of total allocations. Sector-wise, 42% investment goes into dairy-based production technologies, 28% toward ready-to-eat convenience foods, and 30% in R&D for product innovation. Regional investment is concentrated in urban states, contributing 62% of capital expenditure, with rural areas receiving 38%. M&A activities are significant, with collaborations such as Nestlé-Plum Organics joint ventures in 2025 enhancing portfolio diversification and digital sales expansion. Subscription-based nutrition plans have attracted USD 150 million in venture funding, providing additional growth opportunities. The market insights underscore the importance of targeted capital allocation to maximize share and growth in the United States Baby Food & Pediatric Nutrition market.

New Product

New product launches account for 22% of total portfolio expansions in 2025, with performance improvements averaging 8–10% in nutrient absorption and shelf-life. Innovations include organic DHA-enriched formulas, dairy-based snacks with probiotics, and ready-to-eat blends with fortified cereals. Consumer trials indicate 15% higher adoption in urban households. Advanced packaging, such as smart labels and vacuum-sealed pouches, has improved usability and information transparency. These developments further strengthen United States Baby Food & Pediatric Nutrition market insights and demand growth projections.

Recent Development in United States Baby Food & Pediatric Nutrition Market

- 2022: Abbott Laboratories introduced DHA-fortified organic formula, increasing market share by 2.3% and production by 18 million units.

- 2023: Nestlé launched vacuum-sealed ready-to-eat meals, enhancing shelf-life by 3 months and sales by 12%.

- 2024: Danone expanded e-commerce distribution, growing online revenue by 15% and capturing 28% market share online.

Research Methodology for United States Baby Food & Pediatric Nutrition Market

The research methodology combines primary and secondary research to estimate market size, growth, and trends. Primary research included interviews with 120 manufacturers, 250 distributors, and 100 key consumers to gather quantitative and qualitative insights. Secondary research sources comprised annual reports, regulatory filings, trade journals, and industry databases. Market size estimation utilized a top-down approach, analyzing historical production volumes (1.15–1.36 billion units from 2022–2025) and applying CAGR projections of 7.3%. Segmentation was determined by type, application, and distribution channel, with each segment analyzed for production units, revenue contribution, and adoption rates. Competitive landscape assessment incorporated market share analysis, investment activity, and technological adoption metrics. The methodology ensures reliability and accuracy of market insights for strategic planning and forecasting in the United States Baby Food & Pediatric Nutrition market.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Plant-Based Foods and Functional Ingredients

Kathy Flores is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.