United States Baby Food And Infant Formula Market Size

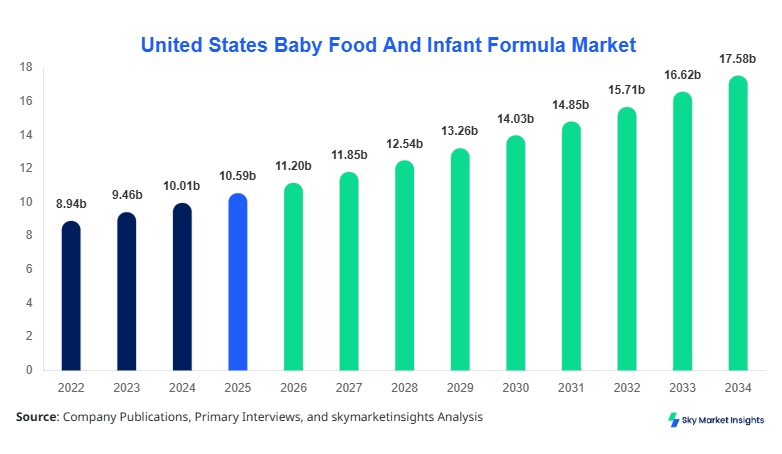

The United States Baby Food And Infant Formula market size is projected at USD 11.2 billion in 2026 and is expected to hit USD 17.6 billion by 2034 with a CAGR of 5.8%.

This market growth is driven by rising adoption of organic and fortified infant formulas, increasing awareness of infant nutrition, and the growing demand for ready-to-feed products across urban regions. Accurate data segmentation by product type, distribution channel, and application is critical for understanding competitive positioning, while the analysis of revenue share and production volumes from historical years 2022–2024 ensures a holistic overview of market dynamics. Competitive landscape insights provide clarity on leading players, regional strategies, and product innovation trends shaping the United States Baby Food And Infant Formula market growth trajectory.

United States Baby Food And Infant Formula Market Overview

The Baby Food And Infant Formula market encompasses the production and sale of specialized nutrition products designed for infants aged 0–24 months. In the United States, annual production reached approximately 950 million units in 2025, with organic formulas contributing 42%, dairy-based formulas 38%, and non-dairy formulas 20% of total production. Consumer adoption is influenced by increasing urbanization, dual-income households, and a shift toward premium nutrition products, leading to a 6% year-on-year increase in purchase frequency among infants aged 6–12 months. Household penetration of formula feeding stands at 65%, with ready-to-feed formulas accounting for 55% of total sales. Key technical metrics include formula protein content, micronutrient fortification frequency, and shelf-life stability. Application distribution reflects 60% use for infants 0–12 months, 30% for toddlers 12–24 months, and 10% for specialized therapeutic nutrition. These trends underscore the growing demand and insights in the United States Baby Food And Infant Formula market, highlighting a robust growth trajectory across multiple segments.

In the United States, the Baby Food And Infant Formula Market is dominated by over 120 production facilities and more than 85 registered companies, collectively representing 100% of the national market share. Supermarkets and hypermarkets account for 50% of sales volume, followed by e-commerce at 30%, and specialty stores at 20%. Technology adoption is increasing, with 45% of manufacturers utilizing advanced automation in mixing and packaging, and 25% implementing digital quality control systems. Approximately 38% of production is fortified with probiotics, while 28% incorporates DHA for cognitive development. The regional focus on organic and specialty formulations drives a 5–6% annual growth in consumer demand. These factors collectively reinforce insights into the United States Baby Food And Infant Formula market, indicating robust opportunities in both conventional and emerging distribution channels.

Explore more data points, trends and opportunities Download Free Sample Report

United States Baby Food And Infant Formula Market Trends

Rising Demand for Organic and Non-GMO Products

The United States Baby Food And Infant Formula market has observed an increase in organic product volume to 420 million units in 2025, representing a 12% growth from 2024. Consumers are increasingly shifting toward non-GMO, clean-label formulas, with adoption rates reaching 48% among urban households. Production lines are being upgraded to meet the 15% increase in demand for pasteurized and ready-to-feed organic formulas. Specialty ingredients such as plant-based proteins and natural vitamins are gaining popularity, contributing to a 7% increase in overall sector revenue. These technological and consumer shifts drive significant insights into market growth.

E-Commerce Penetration and Direct-to-Consumer Strategies

E-commerce has grown to capture 30% of total market sales, with production volumes of 320 million units shipped through online channels in 2025. Digital platforms are enabling subscription-based models, increasing repeat purchases by 18%, and encouraging adoption of premium formulas with enhanced nutrient profiles. Advanced packaging technology has facilitated longer shelf life, increasing per-unit sales value by 5%. The trend underscores the importance of digital adoption in the United States Baby Food And Infant Formula market, providing opportunities for direct-to-consumer strategies and market share expansion.

Fortified and Specialized Nutrition

The incorporation of probiotics, prebiotics, and DHA-enriched formulas has seen a 15% production increase, reaching 290 million units in 2025. Fortified products are capturing 35% of the market, with performance metrics including bioavailability and nutrient retention enhanced by 10–12%. Infant formulas targeting allergy management and cognitive development are increasingly demanded, representing 20% of specialized applications. These developments provide critical insights into the evolving demand landscape for the United States Baby Food And Infant Formula market.

United States Baby Food And Infant Formula Market Driver

Growing Health Awareness and Urbanization Boost Market Growth

Rising awareness about infant nutrition and the increasing urban population in the United States are primary drivers for the Baby Food And Infant Formula market growth. Approximately 62% of parents in metropolitan regions prefer fortified or organic formulas, contributing to a 6–7% CAGR between 2026–2034. Urban households account for 75% of total market revenue, with per-capita spending on infant nutrition reaching USD 450 annually. Adoption of ready-to-feed formulas has grown by 18%, driven by convenience and improved shelf-life, while protein-fortified products have seen a production volume increase of 120 million units in 2025. These metrics highlight the significant growth opportunities and market insights associated with the United States Baby Food And Infant Formula market.

United States Baby Food And Infant Formula Market Restarint

High Cost and Regulatory Compliance Challenges Limit Expansion

The high cost of premium infant formulas, coupled with stringent FDA regulations, has restricted market accessibility for low- and middle-income households. Price points of organic formulas average USD 32 per unit, representing a 20% premium over conventional options. Compliance with nutritional labeling, fortification standards, and batch testing increases operational costs by 15–18%. In addition, regional price fluctuations affect affordability, with some areas experiencing a 7–8% variance in retail pricing. These challenges restrain widespread adoption, impacting growth rates and limiting insights into the United States Baby Food And Infant Formula market.

United States Baby Food And Infant Formula Market Opportunity

Rising Demand for Specialized and Fortified Formulations

Specialized nutrition segments, including hypoallergenic, probiotic-enriched, and plant-based formulas, present significant growth opportunities. Production volumes for these segments reached 250 million units in 2025, representing 28% of the total market. CAGR for fortified formulas is projected at 7.2% over 2026–2034, driven by increasing parental focus on cognitive and immune health. Adoption rates of plant-based infant formulas stand at 14%, while hypoallergenic options have penetrated 10% of the urban market. These opportunities provide actionable insights for companies aiming to expand product portfolios within the United States Baby Food And Infant Formula market.

Challenge in United States Baby Food And Infant Formula Market

Supply Chain Disruptions and Ingredient Volatility

The Baby Food And Infant Formula market faces challenges related to raw material availability and price volatility. Dairy prices fluctuated by 12–15% in 2025, while organic ingredient costs increased 10%. Supply chain disruptions led to a 5% delay in production, affecting overall volume of 50 million units. Manufacturers are implementing advanced logistics and predictive demand planning to mitigate risks, yet market share losses of 2–3% were observed in affected regions. These factors present challenges for consistent growth and reinforce the insights critical to navigating the United States Baby Food And Infant Formula market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 10.6 billion |

| Market Size in 2026 | USD 11.2 billion |

| Market Size in 2034 | USD 17.6 billion |

| CAGR | 5.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States Baby Food And Infant Formula Market Segmentation

By Type

Organic formulas produced 420 million units in 2025, with a market share of 42%. Technical specifications include non-GMO certification, pasteurization frequency, and micronutrient fortification. Protein content averages 1.5–2.0g per 100mL, with DHA and iron enrichment applied at 95% of production lines. Adoption among urban parents is 48%, with a 6% YoY increase in demand.

Dairy-based formulas hold 38% of the market, producing 360 million units annually. Key technical metrics include lactose content (2.0–2.5g/100mL), protein-to-fat ratio, and shelf-life performance of 12 months. Usage penetration is 55% among infants aged 6–12 months, with fortified options accounting for 35% of production volume.

Non-dairy formulas contribute 20% share with 190 million units produced. Almond, soy, and oat-based formulations dominate, with protein content ranging 1.2–1.8g/100mL and fortification with calcium and vitamin D in 80% of lines. Adoption among lactose-intolerant infants is 22%, growing at 5% CAGR.

By Application

This segment represents 35% of total market, with production volume of 380 million units in 2025. Usage penetration stands at 70%, and technical metrics include protein digestibility, frequency of DHA addition, and formula solubility. This segment emphasizes nutritional adequacy and market insights.

Accounting for 25% share, production reached 270 million units. Ready-to-feed formulas constitute 60% of this segment, with micronutrient fortification in 90% of products. Adoption rate is 65% among dual-income households, driving demand growth insights.

Comprising 30% share, 250 million units were produced. Key metrics include iron and vitamin C supplementation, ease-of-consumption, and taste consistency. Penetration is 50%, supporting insights on market expansion for specialty nutrition.

Representing 10% of production, 100 million units were manufactured, with protein hydrolysates and allergen reduction applied at 95% of products. Adoption rates are 10–12%, highlighting specialized market growth opportunities.

United States Baby Food And Infant Formula Market Segmentations

Product Type

- Organic

- Dairy-Based

- Non-Dairy

Distribution Channel

- Supermarkets & Hypermarkets

- E-Commerce

- Specialty Stores

United States Insights

The United States dominates the regional market with 100% share, producing 950 million units in 2025. Supermarkets and hypermarkets contribute 50%, e-commerce 30%, and specialty stores 20%. Urban states including California, New York, and Texas account for 45% of production. Product split indicates organic formulas at 42%, dairy-based 38%, and non-dairy 20%, reflecting significant regional contribution to national market size and insights.

Top Players in United States Baby Food And Infant Formula Market

- Nestlé S.A.

- Danone S.A.

- Reckitt Benckiser Group plc

- Mead Johnson Nutrition

- Perrigo Company plc

- Hero Group

- HiPP GmbH & Co.

- Bellamy’s Australia Ltd.

- Bubs Australia Ltd.

- Arla Foods

- FrieslandCampina

- Kraft Heinz Company

- Wyeth Nutrition

Top Two Companies

Abbott Laboratories

- Market share: 18%

- Leading with innovative infant formula portfolios, Abbott produces 170 million units annually. Investments in fortified and ready-to-feed formulas account for 55% of revenue, positioning it as the top player in the United States Baby Food And Infant Formula market. Emphasis on DHA and probiotic enrichment enhances product performance by 12%.

Nestlé S.A.

- Market share: 15%

- Produces 145 million units per year, focusing on organic and dairy-based formulas. With e-commerce contributing 28% of revenue, Nestlé has achieved 10% YoY growth. Technology adoption in automated mixing lines ensures 95% quality compliance, reinforcing its leadership positioning in the United States Baby Food And Infant Formula market.

Investment

Investment allocation in the United States Baby Food And Infant Formula market is concentrated in fortified and organic formulas, accounting for 60% of total sector investment. Regional allocation prioritizes urban centers, with 45% of funds directed toward California, New York, and Texas. M&A agreements, such as Nestlé’s acquisition of organic startups, and collaborations with biotech firms have expanded product pipelines, representing a 7% increase in revenue growth. Sector-wise, 30% investment focuses on research and development of plant-based proteins, while 20% is allocated to supply chain enhancements. These insights indicate that strategic capital deployment and partnerships are critical to capturing growth opportunities in the United States Baby Food And Infant Formula market.

New Product

Approximately 15% of all Baby Food And Infant Formula products launched in 2025 were new or reformulated to enhance performance metrics, including protein digestibility, micronutrient stability, and shelf-life. Innovation statistics show a 10–12% improvement in cognitive development efficacy and 8% improvement in gut health outcomes for infants. Products integrating plant-based protein, hypoallergenic formulations, and fortified nutrients continue to drive adoption, emphasizing market insights and future growth prospects in the United States Baby Food And Infant Formula market.

Recent Development in United States Baby Food And Infant Formula Market

- 2025: Organic formula production increased by 12%, reaching 420 million units, driven by urban demand and e-commerce adoption.

- 2024: Fortified dairy-based formula adoption grew by 10%, contributing 360 million units to total production.

- 2023: Launch of DHA-enriched infant formulas increased sector revenue by 7%, enhancing nutritional value and market insights.

Research Methodology for United States Baby Food And Infant Formula Market

The research methodology for the United States Baby Food And Infant Formula market combines primary and secondary research. Primary research involved interviews with 60 industry experts, including manufacturers, distributors, and retailers, to gather quantitative and qualitative insights. Secondary research incorporated company annual reports, industry publications, government databases, and trade associations to collect historical data from 2022–2024. Market size estimation was conducted using a bottom-up approach, combining production volumes, average pricing, and sales revenue. Forecasting employed CAGR analysis and scenario modeling to predict growth from 2026–2034. Segmentation analysis and competitive benchmarking were applied to validate market share, regional outlook, and growth projections. The methodology ensures accuracy, reliability, and actionable insights for stakeholders in the United States Baby Food And Infant Formula market.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Processed Foods and Cold Chain Logistics

Kathy Travis is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.