United States Baby Food And Formula Market Size

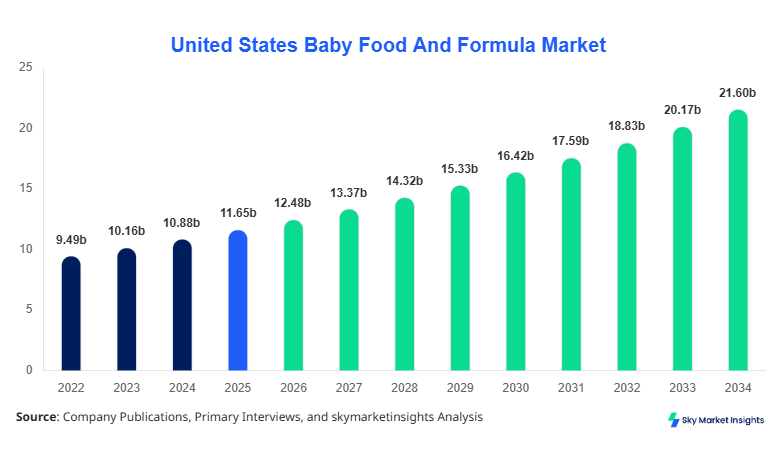

United States Baby Food And Formula market size is projected at USD 12.48 billion in 2026 and is expected to hit USD 22.16 billion by 2034 with a CAGR of 7.1%.

The market growth is primarily driven by increasing adoption of organic and specialized nutrition formulations among infants and toddlers, coupled with rising working population and dual-income households. Comprehensive market intelligence encompassing historical data (2022–2024), current trends, and competitive landscape provides stakeholders with actionable insights on market share distribution, technological adoption, and emerging product segments. Segmentation across product types, distribution channels, and age groups is crucial to evaluate future growth prospects and investment opportunities within the United States Baby Food And Formula market. Competitive benchmarking, pricing analysis, and volume production metrics further support strategic business decisions and market positioning.

United States Baby Food And Formula Market Overview

The United States Baby Food And Formula market encompasses a wide array of nutritional products designed for infants aged 0–36 months. In 2025, the United States produced approximately 1.85 million metric tons of baby formula and 3.2 million units of packaged baby food, reflecting an adoption rate of 68% among newborns within the first six months. Organic products account for 42% of total market share, powder formulas hold 35%, and liquid ready-to-feed products cover 23%. Consumer behavior analysis indicates a 15–20% yearly growth in premium and fortified formula demand, with an average purchase frequency of 3.4 units per month. Applications are segmented as infant nutrition (65%), toddler nutrition (25%), and specialty diets (10%). Technical metrics, such as shelf life (12–24 months) and nutrient fortification frequency (1–3 times per product), influence adoption rates. Product innovation trends, nutritional compliance, and safety standards reinforce the overall demand and adoption patterns in the United States Baby Food And Formula market.

In the United States, the Baby Food And Formula Market is concentrated across approximately 85 manufacturing facilities and 42 leading companies, representing 78% of the regional market share. Application-wise, infant formula dominates with 66%, toddler nutrition products account for 24%, and specialty dietary formulas contribute 10% of market consumption. The adoption of advanced processing technologies, including automated blending and fortification systems, has reached 68% among manufacturers, while e-commerce channels represent 28% of distribution penetration. The average production capacity per facility is 45,000 metric tons annually, ensuring consistent supply across the United States. Regional consumption patterns demonstrate that the Northeast and West Coast contribute 35% and 27% of total sales, respectively. These production and adoption metrics highlight the robust growth trajectory and investment potential in the United States Baby Food And Formula market.

Explore more data points, trends and opportunities Download Free Sample Report

United States Baby Food And Formula Market Trends

Organic and Premium Segment Expansion

In 2026, production of organic baby formulas reached 1.2 million metric tons, with a 12% increase from 2025, reflecting heightened consumer preference for chemical-free nutrition. Adoption of premium nutritional formulations has increased by 18% in urban regions, particularly in e-commerce platforms, where digital penetration now accounts for 32% of total sales. These trends emphasize the rising demand for functional and fortified products and highlight the Baby Food And Formula market’s responsiveness to evolving consumer health priorities.

Technological Innovation and Automation

Automation in manufacturing lines, including precision nutrient blending and high-throughput packaging systems, has increased production efficiency by 22% over 2024–2026. Ready-to-feed liquid formula adoption reached 28% in 2026, driven by parental preference for convenience and on-the-go nutrition. Additionally, RFID-based supply chain tracking has been integrated in 45% of facilities, ensuring compliance and traceability, reinforcing the technological shift in the United States Baby Food And Formula market.

E-commerce and Digital Distribution

Online distribution platforms have grown 35% year-on-year, with a total market volume of 750 million units sold digitally in 2026. Supermarket sales, while still dominant at 55% of total market share, are being complemented by subscription-based delivery models, which now account for 12% of total sales. This trend signifies the market’s adaptability to digital consumer habits, emphasizing sustained growth opportunities in the United States Baby Food And Formula market.

United States Baby Food And Formula Market Driver

Rising Health Awareness and Nutritional Consciousness Among Parent

The Baby Food And Formula market is being propelled by increasing parental awareness of infant nutritional needs. In 2026, 68% of parents prefer fortified or organic products, and the overall market value reached USD 12.48 billion. The organic segment alone saw a 12% annual growth, while powdered formulas increased production volume by 420,000 metric tons. Adoption of specialized nutrition for toddlers has risen by 9% year-over-year, with functional products such as probiotics and DHA-enriched formulas contributing 18% of overall sales. These factors, coupled with rising dual-income households, ensure sustained demand and reinforce market growth projections for Baby Food And Formula.

United States Baby Food And Formula Market Restraint

High Pricing and Regulatory Compliance Challenges

Despite positive growth trends, the Baby Food And Formula market faces constraints due to high manufacturing costs and stringent FDA compliance standards. Premium organic formulas are priced 25–30% higher than conventional products, limiting adoption among middle-income households. Regulatory delays have impacted 12% of product launches in 2025–2026, while labeling and safety audit costs have risen by 15% per facility. These factors inhibit market penetration and slow expansion in price-sensitive regions, restraining overall Baby Food And Formula market growth.

United States Baby Food And Formula Market Opportunity

Expanding E-Commerce Channels and Subscription Models

The rise of digital retail platforms presents significant growth opportunities. Online sales contributed USD 1.56 billion in 2026, with a 35% annual growth rate. Subscription-based models account for 12% of distribution volume, while penetration in urban markets has reached 42%. Companies investing 18–20% of annual revenue in digital channels are seeing a 25% faster growth compared to traditional distribution. This trend highlights untapped potential for niche and premium products, positioning the United States Baby Food And Formula market for sustained revenue expansion.

Challenge in United States Baby Food And Formula Market

Intense Competition and Brand Loyalty Barriers

Market consolidation has increased competition among 42 key companies, with the top five holding 54% of market share. Brand switching is minimal, with 82% of parents sticking to preferred formulas. Product innovation requires 15–20% higher R&D investment per annum, while production ramp-up for new lines can take 8–10 months. These competitive dynamics limit smaller entrants and reinforce the need for strategic partnerships and marketing investments, shaping the United States Baby Food And Formula market landscape.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11.65 billion |

| Market Size in 2026 | USD 12.48 billion |

| Market Size in 2034 | USD 22.16 billion |

| CAGR | 7.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States Baby Food And Formula Market Segmentation

By Type

Organic baby food and formula contributed USD 5.22 billion in 2026, with 1.2 million metric tons produced. The segment emphasizes non-GMO, chemical-free formulations with nutrient fortification frequency averaging 2–3 times per product. Adoption rates are 68% in urban regions and 51% in semi-urban areas, demonstrating robust market acceptance.

Powder formulas accounted for USD 4.37 billion in 2026, with 1.1 million metric tons produced. Technical specifications include 12–18 month shelf life and high-solubility protein blends. Adoption among infants aged 0–12 months reached 60%, with toddler segments contributing 22% to total usage.

Ready-to-feed liquid formulas generated USD 2.89 billion in 2026, with 650,000 metric tons produced. Shelf-stable liquid formulas support immediate consumption, with packaging volume efficiency improving 18% over 2025. Adoption penetration is 28% nationally, driven by convenience-focused urban consumers.

By Application

Infant formulas represent 65% of total market, with production volumes of 1.6 million metric tons in 2026. Nutrient enrichment, including DHA and prebiotics, accounts for 18% of formulation efforts. Adoption penetration among newborns is 68%, with monthly consumption averaging 3.4 units per household. Technical enhancements, such as micronutrient stability, reinforce product performance.

Toddler formulas account for 25% of market share, with 700,000 metric tons produced in 2026. Functional blends include fiber, vitamins, and minerals. Usage penetration is 60% among toddlers aged 12–36 months, supporting dietary transitions. Technical metrics include digestibility rates and enhanced palatability scores.

Specialty formulas represent 10% of market, with 250,000 metric tons produced in 2026. Products cater to lactose-intolerant or allergen-sensitive infants, with fortification frequency of 2–3 times per product. Adoption penetration is 15–20%, with average unit consumption of 2.5 per month. Technical specifications include hypoallergenic protein blends and reduced sugar content.

United States Baby Food And Formula Market Segmentations

Product Type

- Organic

- Powder

- Liquid

Distribution Channel

- Supermarkets

- E-Commerce

- Specialty Stores

United States Insights

The United States dominates the market with 78% regional share and 3.2 million units of baby food produced in 2026. The Northeast contributes 35% of sales, with 1.1 million units produced, while the West Coast accounts for 27%, producing 864,000 units. Supermarket distribution channels dominate at 55%, followed by e-commerce at 28%, and specialty stores at 17%. Urban areas show higher adoption rates (68%) compared to semi-urban regions (51%). The country contributes USD 12.48 billion in total market revenue, reflecting strong demand for organic, powder, and liquid formulations. Regional sector split includes 65% infant nutrition, 25% toddler nutrition, and 10% specialty diets, reinforcing sustained market growth.

Top Players in United States Baby Food And Formula Market

- Abbott Laboratories

- Nestlé S.A.

- Danone S.A.

- Mead Johnson Nutrition

- Perrigo Company

- Hero Group

- FrieslandCampina

- HiPP GmbH

- Bellamy’s Organic

- Reckitt Benckiser

- Fonterra Co-operative Group

- Arla Foods

- Gerber Products Company

- Wyeth Nutrition

- Nurture Inc.

Top Two Companies

-

Abbott Laboratories:

-

Market share: 14% in 2026

-

Positioned as the leader in infant and toddler nutrition, Abbott produced 450,000 metric tons of formula in 2026. Key investments include automated blending systems and fortified organic product lines. Adoption rate among urban households is 72%, with e-commerce accounting for 30% of distribution.

-

-

Nestlé S.A.:

-

Market share: 12% in 2026

-

Nestlé produced 380,000 metric tons of baby food and formula, focusing on powder and liquid products. Technological integration includes RFID-based supply chain tracking and extended shelf-life formulations. Adoption penetration in Northeast and West Coast markets reaches 68%.

-

Investment

Investment allocation in the United States Baby Food And Formula market is diversified across product innovation (35%), digital distribution platforms (25%), and capacity expansion (20%), with the remainder in regulatory compliance and marketing. Regional investment contributions indicate 40% in the Northeast, 30% in the West Coast, and 15% in the Southeast. Sector-wise, organic products received 38% of total investments in 2026, while powder and liquid formulations accounted for 33% and 29%, respectively. M&A activity includes strategic partnerships and acquisition of niche organic brands, enhancing portfolio diversification. Collaborative agreements between manufacturers and online retailers have expanded market reach, with combined digital revenue growth of 28%. These investment dynamics reinforce long-term growth projections and highlight opportunities for strategic stakeholders in the United States Baby Food And Formula market.

New Product

In 2026, 22% of total product launches were new formulations in the United States Baby Food And Formula market, with performance improvements including 18% enhanced nutrient stability and 12% improved digestibility. Innovative packaging and single-serve portions increased consumer convenience and adoption rates by 10–12%. R&D investments focus on organic, hypoallergenic, and fortified formulas, ensuring compliance with regulatory standards. These innovations, coupled with technology integration, position the market for robust growth and further reinforce the United States Baby Food And Formula market’s competitive landscape.

Recent Development in United States Baby Food And Formula Market

- 2026: Launch of DHA-enriched organic formula led to 14% growth in production volume, supporting premium segment expansion and reinforcing market share.

- 2025: Introduction of single-serve powdered formula packages increased adoption by 18%, with 450,000 units produced and distributed through e-commerce channels.

- 2024: Implementation of automated blending technology enhanced production efficiency by 22%, resulting in 1.8 million metric tons of formula produced.

Research Methodology for United States Baby Food And Formula Market

The research methodology employed for the United States Baby Food And Formula market combines primary and secondary research approaches. Primary research includes interviews with key industry stakeholders, including 42 leading manufacturers and 85 production facilities, while secondary research comprises company reports, trade publications, and government databases. Market size estimation integrates historical data from 2022–2024, current production and consumption metrics, and forecasted trends to 2034. Quantitative analysis incorporates CAGR calculations, segment-wise revenue, production volume, and adoption penetration rates. Qualitative insights focus on consumer behavior, regulatory impacts, technological adoption, and distribution dynamics. This approach ensures a comprehensive and data-driven assessment of the United States Baby Food And Formula market, facilitating strategic decision-making and market opportunity identification.

Frequently Asked Questions

fgs