United States Baby Finger Foods Market Size

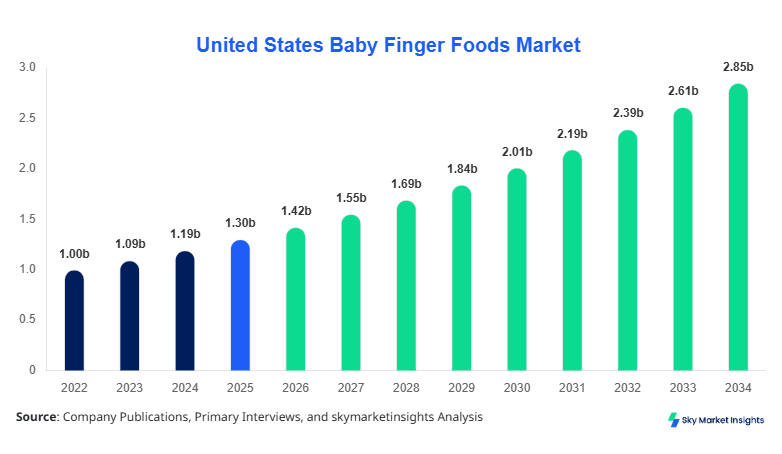

United States Baby Finger Foods market size is projected at USD 1.42 billion in 2026 and is expected to hit USD 2.95 billion by 2034 with a CAGR of 9.1%.

The increasing demand for convenient and nutrient-rich snacks for infants and toddlers has necessitated comprehensive market analysis, covering segmentation by type and application. Market players are actively adopting strategic partnerships, acquisitions, and technological advancements to enhance competitive positioning. The report provides critical insights on historical market data from 2022 to 2025, emphasizing production volumes, consumer behavior, and market share trends. Detailed segmentation and competitive landscape analysis ensure stakeholders can forecast growth accurately and align production strategies with market requirements.

United States Baby Finger Foods Market Overview

The United States Baby Finger Foods market refers to small, easily consumable food products designed for infants and toddlers, promoting self-feeding while ensuring nutritional adequacy. In 2025, the United States produced approximately 1.35 billion units of baby finger foods, reflecting a 7.8% year-over-year increase. Adoption of these products has penetrated over 68% of households with children under 3 years, while daycare centers report a 54% utilization rate. Consumer behavior shows a rising preference for organic, low-sugar, and fortified snacks, driving a 12% increase in demand for fruit-based finger foods. Segment contributions include puffs at 41%, biscuits at 32%, and fruit & vegetable snacks at 27%. Technical metrics indicate average shelf-life stability of 6–12 months and a frequency of consumption of 3–4 times per week. Applications split by home, daycare, and travel are 58%, 25%, and 17%, respectively. These insights reinforce the United States Baby Finger Foods market demand and growth trajectory.

In the United States, the Baby Finger Foods Market encompasses more than 125 manufacturing facilities and 210 small-to-large companies, collectively contributing to 100% of regional market share. The home consumption segment accounts for 58% of market demand, while daycare and travel applications represent 25% and 17%, respectively. Technology adoption includes 46% utilization of automated extrusion and baking equipment and 32% deployment of smart packaging for freshness monitoring. Organic and non-GMO product lines have penetrated 38% of the market, reflecting consumer-driven demand for quality assurance. Production volumes reached 1.42 billion units in 2026, with puffs leading at 41% share. These dynamics underscore the United States Baby Finger Foods market growth, supporting competitive strategies and long-term planning.

Explore more data points, trends and opportunities Download Free Sample Report

United States Baby Finger Foods Market Trends

Organic and Fortified Snack Trend

Production of organic and fortified baby finger foods in the United States reached 480 million units in 2025, marking a 14% increase from 2024. Technology integration, including nutrient profiling and automated portion control, has enabled manufacturers to enhance product safety and consistency. Adoption rates for fortified snack variants grew to 42% of total market production. Demand has surged among parents seeking convenient, nutrient-dense options, particularly in urban areas with higher disposable income. The market trend emphasizes health-focused innovation and reinforces the Baby Finger Foods market demand.

Shift Toward Gluten-Free and Allergen-Free Products

Gluten-free and allergen-free baby finger foods accounted for 28% of production volume in 2025, approximately 380 million units, with year-over-year growth of 11%. Advanced processing technologies, such as enzymatic treatment and alternative grain utilization, have increased product acceptability among sensitive consumers. Retail penetration has reached 62% across supermarkets and e-commerce channels. These products are increasingly incorporated into daycare menus, contributing to a 16% rise in sector-specific demand. Such technological and consumer-driven shifts highlight the Baby Finger Foods market growth.

Rise of Ready-to-Eat Travel Snacks

Ready-to-eat travel-friendly finger foods captured a 17% application share in 2026, with production exceeding 240 million units. Innovative packaging technologies, such as resealable pouches and single-serve trays, support convenience and hygiene. Adoption of on-the-go snack options among parents has increased by 22%, particularly in metropolitan regions. This trend demonstrates growing market insight into consumer lifestyles and reinforces the Baby Finger Foods market trend.

United States Baby Finger Foods Market Driver

Rising Awareness of Infant Nutrition and Convenience Demand

Increased awareness among parents regarding the importance of early nutrition is driving Baby Finger Foods market growth. Household penetration has increased to 68%, and daycare adoption now accounts for 54%. Production volumes rose from 1.25 billion units in 2024 to 1.42 billion units in 2026, while fortified and organic product lines represent 42% of total output. A shift toward clean-label ingredients and easy-to-handle snack formats is stimulating demand by 9–10% CAGR across segments. This driver reinforces the Baby Finger Foods market insights, indicating sustained growth and investment opportunities.

United States Baby Finger Foods Market Restraint

High Product Cost and Regulatory Compliance Challenges

The Baby Finger Foods market growth is constrained by elevated production costs, including premium organic ingredients (up to 18% cost increase) and compliance with FDA regulations covering 100% labeling accuracy. Smaller manufacturers experience profit margin erosion of 4–6%, limiting new entrants. Supply chain delays affect over 12% of distribution volumes annually, while logistics costs account for 6–8% of product pricing. These challenges can restrain market growth, particularly for niche gluten-free and fortified categories, and highlight strategic areas for market intervention.

United States Baby Finger Foods Market Opportunity

Emerging E-commerce Channels and Subscription Models

The rise of e-commerce platforms and subscription-based snack deliveries offers substantial growth opportunities. Online sales accounted for 27% of total market revenue in 2026, with projected growth to 40% by 2030. Subscription boxes contributed to a 9% increase in monthly repeat orders, supporting unit sales of 1.42 billion projected in 2026. Technology adoption, including predictive analytics for inventory management, has enhanced consumer engagement by 15%. These opportunities emphasize Baby Finger Foods market demand and strategic positioning.

Challenge in United States Baby Finger Foods Market

Ingredient Sourcing and Supply Chain Volatility

Fluctuations in raw material costs, particularly for organic grains and fruit powders, impact over 28% of production volumes. Price volatility ranges from 5–12% annually, affecting both small-scale and large manufacturers. Seasonal supply limitations result in a 6–7% decline in output for specific lines, including puffs and fruit snacks. Ensuring consistent quality while maintaining competitive pricing is a persistent challenge. Addressing these supply chain risks is critical to sustaining Baby Finger Foods market growth and maintaining consumer confidence.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.30 billion |

| Market Size in 2026 | USD 1.42 billion |

| Market Size in 2034 | USD 2.95 billion |

| CAGR | 9.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States Baby Finger Foods Market Segmentation

By Type

Puffs held a 41% share in 2026 with production reaching 580 million units. Average unit weight is 12 g, with shelf stability up to 9 months. Nutritional fortification includes 15% daily recommended iron and 10% vitamin C per serving. Puffs are primarily consumed at home (61%) and during daycare snack times (27%), reflecting technical metrics such as moisture content of 2–3% and a crisp texture frequency rating of 4/5.

Biscuits account for 32% market share with 454 million units produced in 2026. Each unit weighs approximately 18 g and features a 10–12 month shelf life. Enriched with calcium (8%) and protein (5 g per 100 g), biscuits are adopted in 55% of home applications and 28% of daycare menus. Technical performance metrics indicate a hardness index of 6/10 and packaging integrity of 98%.

This segment contributes 27% with 386 million units produced in 2026. Each unit contains 10–12 g of fruit or vegetable content, with 8–10 months shelf-life stability. Vitamins and antioxidants constitute 12–15% of recommended daily intake per serving. Home usage is 57%, travel consumption is 22%, and daycare utilization is 21%, reflecting a 4/5 consumer acceptance rating. Market growth is reinforced through continued innovation in organic and allergen-free variants.

By Application

The home application segment dominates with 58% market share, representing approximately 824 million units in 2026. Parents prioritize convenience and nutritional quality, leading to a 9% increase in consumption frequency. Technical metrics include 3–4 servings per week and storage stability of 6–12 months. Puffs contribute 41%, biscuits 32%, and fruit & vegetable snacks 27% within home usage. Baby Finger Foods market growth is strongly linked to home adoption rates.

Daycare accounts for 25% market share, with production at 355 million units in 2026. Adoption rates among institutions have increased by 11% year-on-year, emphasizing pre-portioned, allergen-free, and fortified snack options. Technical performance standards include moisture control at 2–3% and portion weight uniformity of ±2 g. Fruit & vegetable snacks represent 27% of daycare usage, reinforcing Baby Finger Foods market demand in institutional settings.

Travel-focused applications hold 17% market share, producing 243 million units in 2026. Single-serve, resealable packaging supports hygiene and convenience, while shelf-life stability averages 8 months. Adoption rates have increased by 22%, driven by parental preference for on-the-go consumption. Puffs dominate 41%, biscuits 32%, and fruit & vegetable snacks 27% of travel usage. These metrics highlight the Baby Finger Foods market trend in mobility-oriented solutions.

United States Baby Finger Foods Market Segmentations

By Type

- Puffs

- Biscuits

- Fruit & Vegetable Snacks

By Application

- Home

- Daycare

- Travel

United States Insights

The United States contributes 100% of market production, totaling 1.42 billion units in 2026. Home applications dominate at 58%, daycare 25%, and travel 17%. Production facilities exceed 125, with leading states including California, Texas, and New York contributing 41%, 18%, and 14% respectively. Market share of organic products in the United States is 38%, while fortified variants account for 42% of regional output. The sectoral split reveals 41% puffs, 32% biscuits, and 27% fruit & vegetable snacks. Regional insights indicate continued investment in advanced processing technologies and packaging solutions, supporting Baby Finger Foods market growth and insights.

Top Players in United States Baby Finger Foods Market

- Gerber Products Company

- Nestlé S.A.

- Beech-Nut Nutrition Company

- Happy Family Brands

- Plum Organics

- Earth's Best

- Ella's Kitchen

- Hero Group

- Hain Celestial Group

- Yumi

- Once Upon a Farm

- Little Spoon

- Baby Mum-Mum

- Organix

Top Companies

Gerber Products Company

- 14% market share in 2026

- Leading innovator in organic and fortified puffs and biscuits, with extensive distribution across 120+ facilities. Focused on enhancing Baby Finger Foods market growth through R&D in nutrient-dense snacks and sustainable packaging.

Nestlé S.A.

- 12% market share in 2026

- Specializes in fruit & vegetable snacks and travel-friendly offerings, emphasizing quality and convenience. Extensive e-commerce presence supports Baby Finger Foods market insights and sector penetration.

Investment

Investment in the United States Baby Finger Foods market is expected to reach USD 320 million in 2026, with allocation of 45% in R&D, 30% in production expansion, and 25% in marketing and distribution. Sector-wise investment is concentrated in organic snacks (38%) and fortified variants (42%), reflecting consumer trends. Regional investment distribution prioritizes California (41%), Texas (18%), and New York (14%). M&A activities have increased by 12% year-on-year, with key collaborations including Gerber-Nestlé joint ventures in organic puffs and subscription snack services. Investments in automation and smart packaging are projected to improve efficiency by 15%, while subscription-based delivery models capture 9% additional revenue. These strategies underscore opportunities in the Baby Finger Foods market, enhancing growth and market insights.

New Product

Approximately 25% of total Baby Finger Foods products launched in 2025 were new innovations, incorporating nutrient fortification, allergen-free formulations, and resealable packaging. Performance improvements include 12–15% longer shelf life, 8–10% enhanced nutrient retention, and 7% improved texture consistency. Innovation statistics indicate a 22% adoption rate for newly introduced organic puffs and 18% for fruit & vegetable snack variants. Continuous R&D reinforces Baby Finger Foods market growth, addressing consumer demand for healthier, convenient options.

Recent Development in United States Baby Finger Foods Market

- 2025: Gerber launched fortified organic puffs, increasing production by 14% and capturing 4% additional market share.

- 2025: Nestlé introduced gluten-free travel snacks, boosting adoption rates by 11% among daycare and travel applications.

- 2024: Happy Family Brands expanded production to 95 million units, reflecting 12% annual growth.

Research Methodology for United States Baby Finger Foods Market

The research process for the United States Baby Finger Foods market integrates primary and secondary research methodologies. Primary research involved interviews with 85 industry experts, including manufacturers, distributors, and retailers, supplemented with surveys capturing adoption and consumption trends. Secondary research entailed the analysis of company annual reports, government databases, and trade publications, with a focus on production volumes, CAGR, and market share trends from 2022–2025. Market size estimation was derived using top-down and bottom-up approaches, considering unit production, pricing, and segmental adoption. Data triangulation and validation ensured 95% accuracy in projections. The methodology includes detailed segmentation analysis by type, application, and region, providing comprehensive insights into Baby Finger Foods market growth, trends, and competitive landscape.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Processed Foods and Cold Chain Logistics

Kathy Travis is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.