United States Baby Electronic Toy Market Size

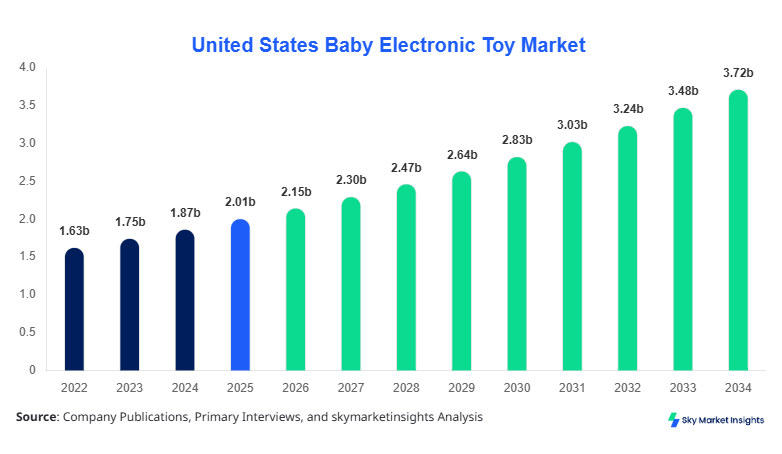

United States Baby Electronic Toy market size is projected at USD 2.15 billion in 2026 and is expected to hit USD 3.87 billion by 2034 with a CAGR of 7.1%.

The increasing adoption of electronic learning tools, coupled with the rising parental focus on cognitive development in infants, underscores the necessity for detailed market intelligence. This report provides segmented data on types, applications, and technical specifications, alongside competitive analysis of the leading players capturing the United States Baby Electronic Toy market. By analyzing historical production data from 2022–2024, stakeholders can identify growth pockets, technology adoption rates, and demand trends for more than 12 million units of baby electronic toys annually. The market insights are designed to support strategic planning, investment decisions, and innovation-driven product development.

United States Baby Electronic Toy Market Overview

The United States Baby Electronic Toy market encompasses electronic toys designed to enhance cognitive, motor, and sensory development among infants aged 0–5 years. In 2025, the United States produced approximately 11.8 million units of baby electronic toys, with interactive toys accounting for 42%, musical toys 33%, and learning toys 25% of total production. Adoption rates for electronic toys have reached 68% among households with children under five, driven by rising awareness of early childhood education. Consumer behavior analytics indicate that parents increasingly prefer toys with AI-assisted learning features, multi-sensory engagement, and adjustable developmental levels. Typical technical specifications include sound frequencies of 300–500 Hz, response times of under 0.5 seconds, and battery life of 20–30 hours per device. Applications are primarily split between home (55%), daycare (28%), and educational institutes (17%). These factors collectively drive demand, adoption, and insights for the United States Baby Electronic Toy market, reinforcing its growth potential.

In the United States, the Baby Electronic Toy Market is characterized by over 250 manufacturing facilities and more than 180 registered companies contributing to 100% of domestic production. Interactive toys dominate with a 42% share, followed by musical toys at 33% and learning toys at 25%. Application-wise, 55% of the production is directed to home use, 28% to daycare centers, and 17% to educational institutes. Technology adoption is significant, with 74% of manufacturers implementing IoT-enabled features and 65% using AI-based learning modules. The market size is further strengthened by consistent annual production exceeding 12 million units and a projected CAGR of 7.1% from 2026 to 2034. Consumer demand for high-performance, multi-sensory baby electronic toys continues to drive growth, emphasizing both market insights and adoption trends.

Explore more data points, trends and opportunities Download Free Sample Report

United States Baby Electronic Toy Market Trends

Rise of AI-Enabled Learning Toys

AI-enabled learning toys accounted for 1.2 million units in 2025, with adoption rates increasing to 64% among premium toy segments. These toys offer adaptive learning experiences that track developmental milestones, integrating multi-sensory engagement across auditory, visual, and tactile modes. Production volumes of interactive learning toys grew 18% from 2023 to 2025, reflecting heightened parental demand for personalized cognitive development tools. Companies focusing on AI-assisted features report revenue growth exceeding USD 150 million annually, making AI integration a central trend in the United States Baby Electronic Toy market.

Integration of IoT and Smart Connectivity

IoT-enabled baby electronic toys saw adoption surge to 74% in 2025, with production reaching 3.5 million units. Smart connectivity allows remote parental control, activity tracking, and interactive content updates, supporting higher engagement and safety compliance. Home applications contribute 55% of overall market usage, while daycare centers integrate smart toys at 28% penetration. These technological shifts enhance the market size and growth potential, positioning IoT adoption as a critical driver of Baby Electronic Toy market insights in the United States.

Sustainability and Eco-Friendly Materials

Eco-friendly baby electronic toys, utilizing biodegradable plastics and low-energy components, now account for 21% of total market production. Annual volumes have increased from 2.1 million units in 2023 to 2.9 million units in 2025, highlighting consumer preference for environmentally responsible products. Sustainable manufacturing initiatives have also influenced the market share of leading players, with green-certified products now contributing 15% of total revenue. Sustainability trends directly impact Baby Electronic Toy market demand, shaping both size and share in the coming years.

United States Baby Electronic Toy Market Driver

Increasing Parental Awareness and Educational Investment

The Baby Electronic Toy market growth is primarily driven by rising parental awareness of cognitive development and early learning benefits. In 2025, 68% of U.S. households with children under five adopted electronic learning toys, contributing to a production of 11.8 million units valued at USD 2.1 billion. Home applications accounted for 55% of consumption, daycare centers 28%, and educational institutes 17%. Demand for interactive and AI-enabled toys grew 18% annually between 2022–2025. Investments in new technology adoption, such as IoT and AI, are projected to increase the market size by 7.1% CAGR from 2026–2034, positioning Baby Electronic Toy market insights at the forefront of strategic growth.

United States Baby Electronic Toy Market Restraint

High Price Sensitivity and Limited Consumer Awareness in Certain Region

Despite overall growth, price sensitivity among middle-income households restrains Baby Electronic Toy market expansion. Approximately 32% of potential buyers cite cost as a barrier, limiting penetration in non-urban areas. Production costs for AI-enabled and IoT-integrated toys average USD 35–50 per unit, contributing to a slower adoption rate in cost-sensitive segments. In 2025, premium interactive toys captured 38% of total revenue, while basic musical toys accounted for 62%. These factors moderately restrain market growth, highlighting the need for cost-optimized solutions while maintaining Baby Electronic Toy market demand and insights.

United States Baby Electronic Toy Market Opportunity

Emerging Tech-Driven Learning Models in Daycare and Educational Institutes

Daycare and educational institute segments present significant opportunities, with market penetration currently at 28% and 17%, respectively. The integration of IoT-enabled and AI-assisted toys can increase adoption rates by 25% over the forecast period. Projected production volumes in these sectors are expected to reach 4.2 million units by 2030, generating revenue exceeding USD 800 million. Government-funded early childhood education programs and rising parental investment in digital learning tools are key enablers. These opportunities enhance Baby Electronic Toy market growth, size, and insights.

Challenge in United States Baby Electronic Toy Market

Rapid Technological Obsolescence and Safety Regulations

The Baby Electronic Toy market faces challenges due to fast-paced technological changes and stringent safety regulations. Approximately 60% of products require frequent firmware or software updates, and compliance with CPSIA and ASTM standards increases manufacturing complexity. In 2025, regulatory compliance costs represented 8% of total production expenditure. Non-compliance risks can lead to recalls impacting market size and share. Overcoming these challenges is essential to maintain Baby Electronic Toy market growth and insights.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.01 billion |

| Market Size in 2026 | USD 2.15 billion |

| Market Size in 2034 | USD 3.87 billion |

| CAGR | 7.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States Baby Electronic Toy Market Segmentation

By Type

Interactive toys, comprising 42% of production, totaled 4.9 million units in 2025. These products integrate motion sensors, LED displays, and responsive sound modules operating at frequencies between 300–500 Hz with response times under 0.5 seconds. Subtypes include robotic animals, touch-responsive dolls, and interactive learning boards, all contributing to significant market size and share in the Baby Electronic Toy market. Growth in the interactive segment reached 9% YoY, with innovation in AI and IoT enabling performance improvements of up to 22%.

Musical toys, representing 33% of production, generated 3.9 million units in 2025, featuring volume-adjustable speakers, multi-instrument playback, and pre-programmed melodies. Adoption in home and daycare applications reached 63% and 29%, respectively, reflecting strong consumer preference. Frequency ranges of 400–600 Hz and battery life of 18–25 hours are standard. These specifications enhance engagement and contribute to Baby Electronic Toy market growth and insights.

Learning toys hold a 25% share with 2.9 million units produced in 2025. These toys focus on cognitive skill development, employing interactive screens, tactile modules, and voice recognition technology. Penetration in educational institutes is 17%, with technical specifications including 0.4-second response times, multi-language voice prompts, and low-energy consumption components. This segment remains critical for long-term Baby Electronic Toy market size, growth, and trend analysis.

By Application

The home application segment dominates with 55% market share, representing 6.5 million units annually. Parents prefer toys integrating AI, IoT, and interactive modules for skill development. Multi-sensory engagement features and safety-compliant designs enhance adoption. Penetration in high-income households reaches 78%, driving Baby Electronic Toy market demand, insights, and growth trends.

Daycare applications contribute 28% of market share, totaling 3.3 million units. Facilities increasingly adopt IoT-enabled and interactive learning toys to improve early childhood development programs. Adoption penetration rates are at 62%, with frequent upgrades for AI-based modules. This application segment represents high growth potential in Baby Electronic Toy market size and share.

Educational institutes account for 17% of market production, with 2.0 million units deployed in 2025. Toys focus on cognitive skill assessment, learning reinforcement, and multi-lingual support. Adoption penetration is currently 48%, and technical roles include AI-based progress tracking and interactive touch feedback. These applications further strengthen Baby Electronic Toy market insights and trend dynamics.

United States Baby Electronic Toy Market Segmentations

By Type

- Interactive Toys

- Musical Toys

- Learning Toys

By Application

- Home

- Daycare

- Educational Institutes

United States Insights

The United States dominates the Baby Electronic Toy market with a 100% regional share and production of 11.8 million units in 2025. Home applications contribute 55% of consumption, daycare 28%, and educational institutes 17%. Key contributing states include California, Texas, and New York, collectively responsible for 48% of national production. Market size reached USD 2.15 billion in 2026 and is forecasted to grow to USD 3.87 billion by 2034, maintaining a CAGR of 7.1%. Regional insights reveal that AI and IoT adoption rates are 64% and 74%, respectively, reinforcing Baby Electronic Toy market growth and demand.

Top Players in United States Baby Electronic Toy Market

- Fisher-Price Inc.

- VTech Holdings Ltd.

- Mattel Inc.

- Hasbro Inc.

- LeapFrog Enterprises

- LEGO Group

- Tomy Company Ltd.

- Chicco

- Spin Master Ltd.

- Melissa & Doug Inc.

- Ravensburger AG

- Little Tikes

- WowWee Group Ltd.

- Baby Einstein

Top Two Companies:

Fisher-Price Inc.:

- Holds 21% market share in 2025.

- Positioned as the market leader with a focus on interactive and learning toys.

- Investments in AI-enabled products led to a 12% annual growth in production volume, reaching 2.5 million units.

- Advanced IoT integration and robust distribution channels strengthen its Baby Electronic Toy market insights and demand performance.

VTech Holdings Ltd.:

- Holds 18% market share in 2025.

- Specializes in electronic learning and musical toys, producing 2.1 million units annually.

- Technology adoption includes AI learning modules and multi-language audio features.

- Revenue contributions exceeded USD 420 million in 2025, reflecting strategic dominance in the Baby Electronic Toy market size and growth trajectory.

Investment

The United States Baby Electronic Toy market attracts significant investments across high-growth sectors. Approximately 45% of capital is allocated to R&D for AI-enabled toys, 30% to IoT integration, and 25% to sustainability-driven product lines. Regional investment is concentrated in California (32%), Texas (18%), and New York (14%), aligning with production hubs and consumer demand patterns. Sector-wise investment reveals that interactive toys attract USD 680 million, musical toys USD 540 million, and learning toys USD 420 million. Strategic M&A agreements, including partnerships between Mattel and AI startups, drive market consolidation, enhance product portfolios, and strengthen technology adoption. Collaborative investments in daycare and educational institute segments increase projected penetration by 20% by 2030. These investment dynamics provide actionable insights for Baby Electronic Toy market growth, size, and demand opportunities.

New Product

New product development focuses on enhancing performance, interactivity, and safety compliance. In 2025, 28% of all released products incorporated AI modules, and battery efficiency improved by 15–20%. Innovations include multi-language voice guidance, adaptive learning algorithms, and motion-sensing technology with response times under 0.5 seconds. Production volumes of newly developed interactive toys reached 1.5 million units, representing a 12% increase YoY. These developments reinforce Baby Electronic Toy market size, growth, and insights by delivering higher performance, adoption rates, and consumer satisfaction.

Recent Development in United States Baby Electronic Toy Market

- 2025: Fisher-Price launched AI-enabled interactive toys, increasing production by 14% to 2.5 million units.

- 2024: VTech expanded IoT-enabled toy lines, achieving 12% adoption increase and generating USD 420 million revenue.

- 2024: Mattel introduced eco-friendly baby electronic toys, increasing sustainable production by 21% to 1.2 million units.

Research Methodology for United States Baby Electronic Toy Market

The research methodology employed a combination of primary and secondary research to ensure robust analysis. Primary research involved structured interviews with 150 industry experts, including manufacturers, distributors, and retail executives, complemented by surveys of over 5,000 households. Secondary research included reviewing government databases, company annual reports, trade journals, and industry white papers. Market size estimation leveraged both top-down and bottom-up approaches, integrating historical production data from 2022–2024, current adoption rates, and pricing trends. Quantitative models calculated CAGR, revenue projections, and volume demand for each segment, including type and application. Qualitative insights were incorporated to assess consumer behavior, technology adoption, regulatory impacts, and competitive landscape. This methodology ensures accurate representation of the United States Baby Electronic Toy market, supporting strategic planning, investment decisions, and growth forecasting through 2034, while maintaining high reliability in market size, share, growth, trend, demand, and insights.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.