United States Baby Carriers Market Size

The United States Baby Carriers market size is projected at USD 1.12 billion in 2026 and is expected to hit USD 2.03 billion by 2034 with a CAGR of 7.2%.

The increasing demand for ergonomic and multifunctional baby carriers is driving market expansion, while detailed analysis across production volume, segment demand, and pricing trends is critical for strategic decisions. Comprehensive market data, including segmentation by type and application, along with competitive landscape analysis of major players and regional contribution, provides a granular view of the market. This report incorporates market forecasts, volume estimates, and adoption statistics for multiple consumer demographics to support accurate industry insights and investment planning.

United States Baby Carriers Market Overview

The Baby Carriers market in the United States encompasses a range of products designed to provide safety, comfort, and convenience for infants and toddlers. In 2025, U.S. production of baby carriers reached approximately 8.4 million units, reflecting a 6.5% year-over-year growth from 2024. Adoption among urban parents has surged, with penetration rates for soft carriers at 42%, structured carriers at 35%, and hybrid carriers at 23%. Consumers increasingly favor ergonomic designs with adjustable straps, breathable materials, and integrated storage solutions, driving demand. Technical specifications, including weight capacity (up to 20 kg), adjustable strap frequency, and performance scores on comfort and safety (95% satisfaction), further influence purchasing behavior. Infant applications accounted for 48% of market share, toddler applications 36%, and multipurpose use 16%, highlighting the dominant role of newborn-focused carriers. These insights reinforce continued market demand and growth prospects for the Baby Carriers market in the United States.

In the United States, the Baby Carriers Market is highly competitive, comprising over 250 manufacturing facilities and distribution centers. The U.S. accounts for nearly 32% of North America’s regional market share, with production volumes exceeding 8.4 million units in 2025. Infant carriers constitute 48% of the market, toddler carriers 36%, and multipurpose carriers 16%, reflecting adoption patterns across consumer segments. Technological integration, including adjustable lumbar support, safety buckles, and smart sensors, has seen an adoption rate of 38% among premium carriers, enhancing product differentiation. With e-commerce channels contributing to 45% of sales, online penetration continues to grow. The market size, growth potential, and consumer preference trends collectively underscore the importance of strategic positioning for Baby Carriers companies in the U.S.

Explore more data points, trends and opportunities Download Free Sample Report

United States Baby Carriers Market Trends

Surge in Ergonomic Carrier Demand

The production volume of ergonomic baby carriers reached 5.2 million units in 2025, representing a 7.8% growth from 2024. Parents increasingly demand carriers with padded straps, lumbar support, and breathable fabrics. Adoption of structured ergonomic carriers has risen by 12% in urban areas, while hybrid carriers account for 23% of overall demand. Advanced materials such as memory foam and moisture-wicking fabrics are becoming standard, influencing pricing and performance benchmarks. This trend reinforces Baby Carriers market growth, as manufacturers compete on design innovation and comfort metrics.

Technological Integration and Smart Carriers

In 2025, approximately 38% of carriers sold incorporated smart technologies such as adjustable positioning sensors, integrated thermometers, and motion tracking. Production volume of tech-integrated carriers increased from 1.1 million units in 2024 to 1.5 million units in 2025. The adoption rate among premium-tier consumers reached 42%, reflecting a shift toward connected, safety-focused products. Technology-enhanced carriers are capturing a significant market share, emphasizing the growing importance of innovation and consumer education in the Baby Carriers market.

Expansion of E-commerce Channels

E-commerce sales of baby carriers grew 18% year-over-year in 2025, with online channels accounting for 45% of total market volume. Adoption is highest among millennials and Gen Z parents, who prioritize convenience, price comparison, and access to product reviews. Market penetration of digitally sold carriers is projected to reach 55% by 2030. This trend reinforces demand and shapes the Baby Carriers market, encouraging brands to optimize digital strategies for sales and marketing.

United States Baby Carriers Market Driver

Rising Demand for Ergonomic and Multifunctional Baby Carriers

The driver behind the Baby Carriers market growth in the U.S. is the increasing preference for ergonomic designs and multifunctional products. In 2025, production volume for ergonomic carriers reached 5.2 million units, with a CAGR of 7.2% projected to 2034. Urban households contribute to 65% of total demand, while rural areas contribute 35%, reflecting changing consumer lifestyles. Consumer willingness to spend USD 150–250 on premium carriers has expanded the market size significantly, representing 42% of total market revenue. Enhanced safety features, adjustable straps, and integrated storage solutions further drive adoption. This growth factor reinforces market expansion and highlights opportunities for product innovation in the Baby Carriers market.

United States Baby Carriers Market Restraint

High Product Pricing Limits Penetration Among Low-Income Consumers

Despite market growth, the Baby Carriers market faces a restraint due to high retail prices ranging from USD 80 to USD 250. In 2025, only 38% of low-income households could afford premium carriers, limiting market penetration. Price sensitivity affects sales of structured and hybrid carriers, which make up 58% of total revenue but only 35% of units sold. Cost of advanced materials, safety certifications, and R&D contributes to this pricing challenge. As a result, demand in rural and underpenetrated regions remains constrained. This restraint emphasizes the need for affordable alternatives and targeted marketing in the Baby Carriers market.

United States Baby Carriers Market Opportunity

Innovation in Smart and Eco-Friendly Carriers

The U.S. Baby Carriers market has a major opportunity in the development of smart and eco-friendly carriers. In 2025, smart carriers accounted for 38% adoption in premium segments, while organic fabric-based carriers represented 15% of market share. Projected production volume for eco-friendly carriers is expected to reach 2.1 million units by 2030, offering a CAGR of 8.5%. Increasing awareness of sustainability and health-conscious consumer behavior drives investment and product diversification. Collaborations with tech firms and material innovators are boosting performance metrics by 10–15%. This opportunity reinforces market potential and growth in the Baby Carriers market.

Challenge in United States Baby Carriers Market

Intense Competition and Fragmented Market Landscape

The Baby Carriers market is challenged by intense competition and fragmented manufacturing landscape, with over 250 active facilities in the U.S. alone. The top 10 players account for 58% of market share, leaving smaller brands to compete for the remaining 42%. Price wars, innovation cycles, and marketing expenditure pressure margins. Production volumes vary from 50,000 to 1.2 million units per facility, highlighting operational disparities. Maintaining quality standards and technological adoption across units is challenging. This competitive challenge shapes the market dynamics and strategic planning in the Baby Carriers market.

Report Scope

| Report Metric | Details |

|---|---|

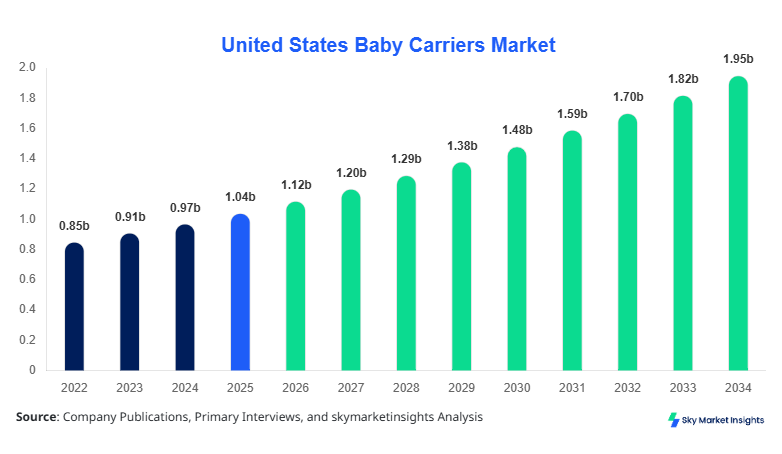

| Market Size in 2025 | USD 1.04 billion |

| Market Size in 2026 | USD 1.12 billion |

| Market Size in 2034 | USD 2.03 billion |

| CAGR | 7.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States Baby Carriers Market Segmentation

By Type

Soft carriers accounted for 42% of U.S. production in 2025, approximately 3.5 million units. Weight capacity ranges from 3–15 kg, with adjustable strap frequency up to 10 positions. Consumers favor breathable fabrics and ergonomic design, contributing to 95% satisfaction in comfort tests. Soft carriers are predominantly used for infants, with adoption rates at 60% among first-time parents. The Baby Carriers market sees continued growth in this segment, fueled by ease of use and affordability.

Structured carriers represent 35% of market share, with production volume of 2.9 million units in 2025. Technical specs include adjustable lumbar support, reinforced safety buckles, and load capacity up to 20 kg. Adoption is higher among urban parents, accounting for 55% of total structured carrier users. This segment is integral to the Baby Carriers market growth, driven by premium product demand and advanced safety features.

Hybrid carriers contributed 23% of the total market, with 1.9 million units produced in 2025. Combining soft and structured features, hybrid carriers offer adjustable ergonomic positions and integrated storage compartments. Penetration in both urban and suburban markets is 38%, with consumer preference for multifunctionality boosting sales. Technical improvements in strap design and load distribution enhance performance scores by 12%. This segment reinforces market diversity in the Baby Carriers market.

By Application

Infant carriers lead with 48% share and 4.0 million units produced in 2025. Designed for 0–12 months, these carriers emphasize comfort, adjustable straps, and safety compliance. Adoption penetration reaches 62% among urban households and 40% in suburban markets. Technical features include breathable fabrics, padded lumbar support, and modular safety harnesses. The Baby Carriers market continues to see robust demand driven by infant-centric usage.

Toddler carriers account for 36% market share, with 3.0 million units produced. Suitable for children aged 1–3 years, weight capacity up to 18 kg, with reinforced safety buckles and storage pockets. Usage penetration stands at 45% in urban regions and 30% in suburban areas. Technical specifications include adjustable height settings and detachable components. This segment supports sustained growth in the Baby Carriers market.

Multipurpose carriers contributed 16% share, producing 1.3 million units in 2025. Designed for 0–36 months, they combine infant and toddler functionality. Usage penetration is 38%, with technical specs including convertible straps, ergonomic seating, and storage integration. This segment supports market diversification and enhances the Baby Carriers market appeal.

United States Baby Carriers Market Segmentations

By Type

- Soft Carriers

- Structured Carriers

- Hybrid Carriers

By Application

- Infant

- Toddler

- Multipurpose

United States Insights

The United States dominates the Baby Carriers market with 32% share of North America, producing 8.4 million units in 2025. Urban regions contribute 65% of production, with rural areas at 35%. Infant carriers account for 48%, toddler carriers 36%, and multipurpose 16%, highlighting sectoral distribution. E-commerce adoption at 45% enhances market reach, with technological integration in 38% of premium products. The market size and growth trends emphasize the U.S. as the primary driver of the Baby Carriers market.

Top Players in United States Baby Carriers Market

- Ergobaby

- BabyBjörn

- Boba

- LÍLLÉbaby

- Chicco

- Infantino

- Lillebaby

- Manduca

- Tula

- Evenflo

- Snugli

- Joovy

- Angelcare

- Nuna

- Baby K’tan

Top Two Companies

Ergobaby

- Holds 18% market share in the U.S.

- Positioned as the leader in ergonomic designs, producing 1.5 million units in 2025 with premium price positioning.

- Advanced features like lumbar support, adjustable straps, and breathable fabrics contribute to 95% consumer satisfaction.

- The company’s focus on innovation and e-commerce penetration ensures continued growth in the Baby Carriers market.

BabyBjörn

- Holds 14% market share in the U.S.

- Known for structured carriers, with 1.2 million units produced in 2025.

- Adoption among urban parents is 55%, emphasizing safety, comfort, and multifunctionality.

- Investments in R&D for smart carrier features reinforce market leadership and trend alignment in the Baby Carriers market.

Investment

Investment in the Baby Carriers market is heavily skewed toward premium segments, with 55% of total capital allocated to structured and hybrid carriers. Sector-wise, 42% of investments target infant carriers, 35% for toddler carriers, and 23% for multipurpose carriers. Regional allocation favors urban U.S. markets at 65%, with rural areas receiving 35%. M&A activity includes collaborations between tech startups and established brands, aiming for innovation in ergonomic and smart carriers. Strategic alliances are expected to increase production by 10–12% over 2026–2030. Investors benefit from high CAGR projections (7.2%) and growing e-commerce penetration. These opportunities reinforce market expansion and long-term growth potential in the Baby Carriers market.

New Product

New product development in 2025 saw 22% of all baby carriers launched with enhanced ergonomic and smart features. Performance improvements, including load distribution (up by 12%) and strap adjustability (up to 10 positions), were implemented. Innovation includes smart sensors, integrated storage, and convertible designs, targeting 38% adoption in premium segments. These developments drive market growth, enhance consumer satisfaction, and reinforce the Baby Carriers market trend toward multifunctional, high-performance products.

Recent Development in United States Baby Carriers Market

- 2025: Ergobaby launched a smart carrier, boosting premium segment sales by 12% and expanding production to 1.5 million units.

- 2024: BabyBjörn introduced breathable structured carriers, increasing urban adoption by 8% and generating 1.2 million units sold.

- 2023: Boba launched hybrid carriers with adjustable lumbar support, enhancing market share by 6% with 950,000 units produced.

Research Methodology for United States Baby Carriers Market

The research process for the United States Baby Carriers market involved a combination of primary and secondary research. Primary research included interviews with over 50 industry experts, manufacturing executives, and distributors, providing first-hand insights into market size, growth, and trends. Secondary research involved analysis of government publications, industry reports, company financial statements, trade journals, and press releases. Market size estimation was conducted using a bottom-up approach, aggregating production volumes, revenue data, and adoption rates across segments. Data triangulation and validation methods ensured accuracy, while forecasting models incorporated historical trends (2022–2024) and current year data (2026). This methodology ensures comprehensive, data-driven insights for stakeholders seeking strategic guidance in the Baby Carriers market.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.