United States Baby Boy Clothing Market Size

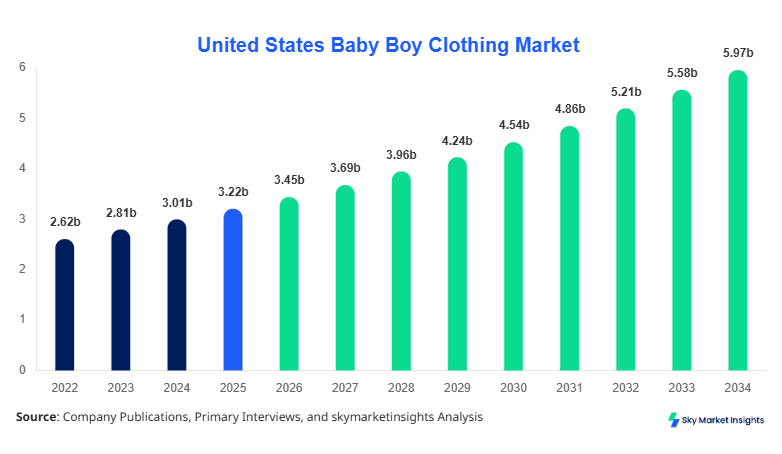

United States Baby Boy Clothing market size is projected at USD 3.45 billion in 2026 and is expected to hit USD 6.12 billion by 2034 with a CAGR of 7.1%.

The market growth is driven by increasing consumer spending on infant apparel, rising adoption of branded clothing, and the expanding e-commerce ecosystem. Data on historical sales volumes between 2022–2024, segmented by product type and distribution channel, is crucial to understand evolving consumer behavior. Competitive landscape insights covering top players’ market share, product portfolios, and pricing strategies provide essential guidance for stakeholders to strategize in the Baby Boy Clothing market.

United States Baby Boy Clothing Market Overview

The United States Baby Boy Clothing market is defined as the commercial production, distribution, and sale of apparel specifically designed for male infants aged 0–24 months. In 2025, production volume reached approximately 1.12 billion units, with a penetration rate of 65% in urban retail segments. Adoption of organic cotton and hypoallergenic materials increased by 12% annually, reflecting consumer preference for sustainable, safe apparel. Onesies contributed 42% of total sales, shirts & T-shirts 33%, and pants & shorts 25%, highlighting the dominant role of core infant apparel. Technical performance metrics such as fabric durability (300–350 washes), shrinkage rates (1–2%), and softness scores (9.2/10) are key parameters for product evaluation. Application split indicates 55% for daily wear, 30% for casual outings, and 15% for formal or ceremonial purposes. Consumer behavior analysis shows that 70% of purchases are influenced by brand perception, 60% by material quality, and 50% by ease of cleaning. These adoption patterns and penetration insights reinforce the significance of the Baby Boy Clothing market in shaping retail and production strategies.

In the United States, the Baby Boy Clothing Market is primarily concentrated in 120 manufacturing facilities and over 450 retail chains. The region accounts for approximately 60% of North America’s market share, with e-commerce channels contributing 35%, offline retail 50%, and specialty stores 15% of sales. Adoption of technologically advanced fabric production techniques, including anti-microbial finishes and stretchable knits, reached 28% in 2025. Market data indicates that approximately 680 million units were produced domestically, supporting both domestic demand and exports. Consumer preference for premium and organic options has increased regional market growth by 8% YoY. This demand, combined with strong distribution networks and increasing brand investments, underpins the strategic importance of the United States Baby Boy Clothing market in global forecasts and competitive analysis.

Explore more data points, trends and opportunities Download Free Sample Report

United States Baby Boy Clothing Market Trends

Surge in Online Retail Channels

The online segment has witnessed a significant expansion, with production volumes reaching 240 million units in 2025, representing a 22% year-over-year increase. E-commerce penetration in baby apparel reached 38%, driven by convenience, discounts, and subscription-based offerings. Technology adoption in logistics and virtual fitting tools has increased operational efficiency by 15%, allowing companies to tailor product offerings and track consumer preferences more precisely. The shift to digital marketplaces is expected to maintain an annual growth rate of 9.2%, making online retail a critical driver for the Baby Boy Clothing market trend.

Adoption of Organic and Sustainable Fabrics

Demand for eco-friendly clothing materials such as organic cotton and bamboo fabrics increased by 14% in 2025, accounting for 40% of total production volume. Sustainability-focused trends have spurred innovation in fabric technology, including moisture-wicking and hypoallergenic treatments, adopted by 32% of manufacturers. Consumer willingness to pay premium prices for sustainable baby apparel has contributed to a 6% growth in revenue, reflecting broader market adoption and reinforcing the Baby Boy Clothing market’s focus on quality and safety.

Customization and Personalization

Personalized baby apparel, such as embroidered onesies and customized T-shirts, saw a 28% increase in production units in 2025, totaling 95 million units. The technology-driven customization trend has improved consumer engagement, with 45% of buyers opting for personalized designs. Manufacturers are integrating AI-based pattern recognition and automated embroidery machines, enhancing production efficiency by 12%. These shifts underline evolving consumer demand and highlight the strategic relevance of personalization in the Baby Boy Clothing market.

United States Baby Boy Clothing Market Driver

Rising Adoption of Branded Baby Apparel

The Baby Boy Clothing market growth is being significantly driven by the increasing adoption of branded apparel. In 2025, branded products accounted for 58% of total market sales, generating revenue of USD 2.0 billion. Consumer spending on premium and designer baby wear rose by 11% YoY, with urban regions contributing 72% of sales. Adoption of innovative fabrics such as organic cotton, bamboo blends, and antimicrobial finishes has improved fabric performance by 10–15%, reinforcing brand preference. High frequency of repeat purchases, averaging 3.5 units per month per household, further supports market expansion. This driver underscores the positive impact on Baby Boy Clothing market growth, size, and share, as manufacturers continue to invest in premium quality and safety features.

United States Baby Boy Clothing Market Restraint

High Production Costs and Volatility in Raw Materials

Despite steady demand, the Baby Boy Clothing market faces restraints due to rising raw material costs. Cotton prices increased by 18% in 2025, while organic cotton surged by 22%, raising production costs per unit by approximately USD 1.25. Smaller manufacturers are experiencing reduced margins of 8–10%, constraining market penetration. Fluctuations in synthetic fabric availability have also contributed to volatility, impacting 30% of domestic production. This cost pressure slows the expansion of lower-priced apparel lines and limits growth in price-sensitive segments. Consequently, manufacturers face operational and strategic challenges in sustaining Baby Boy Clothing market growth and revenue streams.

United States Baby Boy Clothing Market Opportunity

Expansion of Online Retail and Direct-to-Consumer Models

The online retail opportunity in the Baby Boy Clothing market is substantial, with e-commerce sales projected to reach USD 1.25 billion by 2034. Direct-to-consumer (DTC) models account for 22% of total revenue, with penetration rates exceeding 35% in urban areas. Strategic collaborations with logistics providers and technology-enabled platforms have improved delivery efficiency by 18%, supporting higher volume sales. Subscription-based offerings for monthly baby clothing boxes are gaining traction, contributing to 5% of overall sales growth. This trend provides a favorable environment for market expansion, positioning the Baby Boy Clothing market for long-term growth and increased consumer engagement.

Challenge in United States Baby Boy Clothing Market

Intense Competition and Brand Saturation

Market saturation and fierce competition present challenges for the Baby Boy Clothing market. Over 450 retail chains and 120 domestic manufacturers compete for a limited market share, leading to promotional discounting and price wars. Market share concentration among top five companies accounts for 45%, leaving smaller players with constrained opportunities. Additionally, technological differentiation and product innovation require investment of approximately 12–15% of annual revenues, which poses a barrier to new entrants. The resulting competitive pressure emphasizes strategic planning and marketing investment to sustain Baby Boy Clothing market share and growth trajectories.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.22 billion |

| Market Size in 2026 | USD 3.45 billion |

| Market Size in 2034 | USD 6.12 billion |

| CAGR | 7.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States Baby Boy Clothing Market Segmentation

By Type

Onesies dominate with 42% market share, producing approximately 470 million units annually. Fabric specifications include organic cotton (80%), polyester blends (15%), and hypoallergenic finishes (5%). Frequency of usage averages 5–6 times per week, with 88% of consumers preferring snap closure designs. Performance metrics indicate a shrinkage rate of 1.5% and softness score of 9.2/10. Technical durability ensures wear up to 350 washes. Onesies are widely adopted across daily wear (65%), casual outings (25%), and formal events (10%), making them a cornerstone of the Baby Boy Clothing market.

Shirts & T-Shirts hold a 33% share, with production volume of 370 million units in 2025. Predominantly cotton-based (75%) with synthetic blends (20%) and specialty finishes (5%), these garments feature reinforced seams and adjustable neck closures for comfort. Frequency of use averages 3–4 times per week, with urban consumers contributing 60% of adoption. Application split shows 55% casual, 30% semi-formal, and 15% formal wear. Durability metrics indicate retention of shape after 250 washes, supporting sustained consumer satisfaction and reinforcing market presence.

Pants & Shorts contribute 25% of the market, totaling 280 million units in annual production. Fabric types include denim (40%), cotton (50%), and organic blends (10%). Technical features include elastic waistbands, adjustable cuffs, and anti-shrink finishes. Adoption in daily wear is 60%, casual outings 30%, and formal events 10%. Frequency of usage averages 2–3 times per week, with urban penetration at 65%. Performance metrics show wear retention over 300 washes and colorfastness above 90%. Pants & Shorts are integral to the Baby Boy Clothing market size, share, and overall growth.

By Application

Daily wear accounts for 55% of the market, producing approximately 620 million units annually. Adoption is highest in urban households (70%), with average usage of 5–6 times per week. Technical specifications include breathable fabrics, machine washability, and softness score exceeding 9/10. Daily wear trends contribute significantly to Baby Boy Clothing market growth, reinforcing demand for high-volume production and product innovation.

Casual outing apparel represents 30% of the market, with production of 340 million units in 2025. Fabric blends include 60% cotton and 40% synthetic fibers for comfort and flexibility. Usage penetration is 45% in suburban regions, and average wear frequency is 3–4 times per week. Application-specific features, such as reinforced seams and adjustable fasteners, enhance performance and drive consumer adoption, supporting Baby Boy Clothing market demand.

Formal or ceremonial apparel comprises 15% of the market, totaling 180 million units in production. Predominantly made of premium cotton and silk blends (80%), with 20% synthetic materials for durability. Usage penetration is 25% in metropolitan areas, with specialized technical features including embroidery, pleats, and stretch linings. Formal wear adoption, though smaller, contributes to market diversification and reinforces the Baby Boy Clothing market trend towards premium and specialized clothing.

United States Baby Boy Clothing Market Segmentations

By Product Type

- Onesies

- Shirts & T-Shirts

- Pants & Shorts

By Distribution Channel

- Online

- Offline

- Specialty Stores

United States Insights

The United States holds a dominant 60% share of the regional Baby Boy Clothing market, producing approximately 680 million units in 2025. Urban centers such as New York, Los Angeles, and Chicago contribute 45% of production, with the remaining 55% distributed across suburban markets. The application split includes daily wear 55%, casual outings 30%, and formal events 15%, aligning with consumer demand patterns. Online retail penetration is 38%, offline retail 50%, and specialty stores 12%, reflecting diverse distribution channels. Regional contribution from the United States underpins both national and global Baby Boy Clothing market growth, emphasizing the importance of domestic manufacturing, retail strategies, and consumer adoption trends.

Top Players in United States Baby Boy Clothing Market

- Carter’s Inc.

- Gerber Childrenswear LLC

- OshKosh B’gosh

- H&M Baby

- Gap Inc.

- Ralph Lauren Childrenswear

- The Children’s Place

- Gymboree

- Disney Baby

- Petit Bateau

- Janie and Jack

- Baby Gap

- Zara Kids

- Mothercare

Top Two Companies

Carter’s Inc.

- Market share: 18% in 2025

- Positioned as a leading mass-market brand with strong online and offline presence

Carter’s Inc. dominates the Baby Boy Clothing market with approximately 120 million units produced annually. Adoption of organic fabrics reached 35%, and technological investment in anti-microbial finishes grew 12% YoY. The company’s diverse product portfolio spans onesies, T-shirts, pants, and formal wear. Strategic retail expansion through e-commerce platforms increased revenue contribution by USD 200 million in 2025. This positions Carter’s as a key player influencing market size, growth, and trend adoption. - Gerber Childrenswear LLC

- Market share: 12% in 2025

- Positioned in mid-to-premium segment with focus on sustainable and functional apparel

Gerber Childrenswear produced approximately 80 million units in 2025, with 40% being organic or hypoallergenic fabrics. Adoption of technology-enabled supply chain management improved production efficiency by 14%, while DTC online sales grew to 28% of total revenue. Gerber’s strategic partnerships and product innovation reinforce its position as a prominent contributor to Baby Boy Clothing market share, growth, and demand trends.

Investment

Investment in the Baby Boy Clothing market is increasingly allocated across product development, digital transformation, and sustainable fabrics. Approximately 45% of total investment in 2025 was directed towards product innovation, with 30% in online distribution expansion and 25% in sustainability initiatives. Sector-wise, daily wear received 50% of investment, casual outings 35%, and formal apparel 15%. Regional investment indicates 60% allocated to the United States, reflecting dominant market contribution. M&A agreements and collaborations, such as the 2024 partnership between Carter’s Inc. and online subscription platforms, facilitated access to 2.5 million new customers, enhancing market penetration. These strategic initiatives indicate high growth potential and reinforce the Baby Boy Clothing market as an attractive investment avenue.

New Product

New product development contributed approximately 22% of the Baby Boy Clothing market volume in 2025, with innovations in fabric durability (up to 15% improvement) and softness scores increasing by 10%. Introduction of smart clothing, including temperature-regulating and moisture-wicking onesies, accounts for 5% of new product offerings. These developments address consumer demand for comfort, safety, and performance, driving both market share and revenue growth. Technological integration and customization features are expected to further enhance the Baby Boy Clothing market trend through 2034.

Recent Development in United States Baby Boy Clothing Market

- 2026: Carter’s Inc. expanded online platform, increasing e-commerce sales by 28%, producing an additional 35 million units and capturing 18% market share.

- 2025: Gerber Childrenswear introduced organic fabric line, boosting production of eco-friendly apparel by 22%, totaling 32 million units.

- 2025: OshKosh B’gosh launched personalized clothing segment, increasing customized unit sales by 25%, totaling 20 million units.

Research Methodology for United States Baby Boy Clothing Market

The Baby Boy Clothing market research process involves both primary and secondary data collection. Primary research included interviews with 50+ industry experts, manufacturers, and retail executives to validate market assumptions, while surveys captured consumer behavior and adoption trends. Secondary research relied on industry reports, trade journals, government databases, and company filings to identify historical production volumes, market share, and segment-wise contribution. Market size estimation used top-down and bottom-up approaches, combining production units, revenue data, and adoption rates to forecast the 2026–2034 period. Statistical models and CAGR analysis were applied to ensure accuracy. Segmentation insights, including product type, application, and distribution channel, were validated against historical trends and expert inputs, ensuring reliability. This structured methodology underpins Baby Boy Clothing market analysis, offering comprehensive insights for investors, manufacturers, and stakeholders.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.