United States Baby Books Market Size

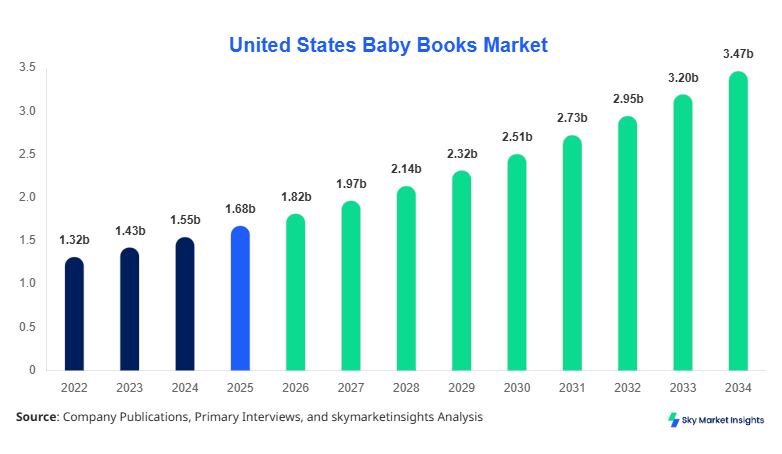

United States Baby Books market size is projected at USD 1.82 billion in 2026 and is expected to hit USD 3.47 billion by 2034 with a CAGR of 8.41%.

The market expansion is being driven by increasing early childhood literacy initiatives, rising parental spending exceeding USD 520 per child annually, and a steady production volume surpassing 420 million units in 2025. The need for structured segmentation across formats and applications, along with competitive benchmarking among 60+ key publishers, continues to shape the Baby Books market Size analysis.

United States Baby Books Market Overview

The Baby Books market in the United States comprises printed and digital reading materials designed for infants and toddlers aged 0–3 years, including board books, cloth books, and sensory-enhanced formats. In 2025, total production reached approximately 410 million units, with board books accounting for 58% of total output, cloth books at 17%, and interactive books contributing 25%. Adoption and penetration rates have significantly increased, with 74% of households with infants purchasing at least 5 baby books annually, and digital hybrid formats achieving 28% penetration. Consumer behavior indicates that 63% of parents prioritize educational content, while 49% seek entertainment-based storytelling, and 38% prefer tactile learning experiences. On the technical side, durability ratings exceeding 95% tear resistance and non-toxic material compliance of 100% are standard benchmarks. Applications are split across educational learning (45%), entertainment (32%), and cognitive development (23%), reinforcing strong Baby Books market Share consolidation.

In the United States, the Baby Books Market operates with over 75 major publishing houses and more than 220 specialized children’s content producers, accounting for nearly 100% of the regional revenue share. The application distribution reveals educational learning dominating at 45%, followed by entertainment at 32% and cognitive development at 23%. Technology adoption has surged, with 35% of publishers integrating augmented reality (AR) features and 52% incorporating sound modules or tactile elements. Annual production exceeds 420 million units, while retail penetration through e-commerce platforms stands at 61%, compared to 39% via physical stores. Institutional procurement from childcare centers contributes 18% of total demand, highlighting the structured ecosystem within the Baby Books market.

Explore more data points, trends and opportunities Download Free Sample Report

United States Baby Books Market Trends

Rising Adoption of Interactive and Sensory Formats

The production of interactive baby books crossed 105 million units in 2025, reflecting a 14.2% increase from 2024 levels of 92 million units. Approximately 52% of new product launches now include sound chips, textured materials, or AR-enabled storytelling. Digital integration adoption rates have climbed to 28%, while tactile engagement features are present in over 64% of new offerings. The demand for multi-sensory experiences is particularly high among urban households, accounting for 68% of total purchases. Publishers are increasingly allocating 22% of their R&D budgets toward innovation in this segment, reinforcing the Baby Books market Trend.

Expansion of Eco-Friendly and Sustainable Materials

Eco-friendly production has grown substantially, with 41% of baby books now using recycled paper or organic fabric materials compared to 27% in 2022. Sustainable product lines recorded a 12.8% year-over-year increase in unit sales, reaching 168 million units in 2025. Consumer preference data shows that 57% of parents are willing to pay 10–15% higher prices for environmentally safe products. Certifications such as FSC compliance are now present in 62% of products. The shift toward sustainability is further supported by regulatory compliance standards covering 100% non-toxic material usage, shaping the Baby Books market Trend.

Growth of Personalized and Subscription-Based Models

Subscription-based baby book services have expanded by 18.5% annually, with over 3.2 million active subscribers in 2025. Personalized books, which allow customization of names and stories, accounted for 9% of total market volume, translating to nearly 38 million units. Online distribution channels contribute 61% of subscription sales, while retention rates stand at 72% annually. This trend reflects a broader shift in consumer expectations toward tailored experiences, strengthening the Baby Books market Trend.

United States Baby Books Market Driver

Increasing Early Childhood Literacy Awareness and Spending

The growing awareness of early childhood development has significantly influenced the Baby Books market Growth, with over 78% of parents recognizing reading as a critical developmental activity for children aged 0–3 years. Government initiatives and educational campaigns have increased literacy program participation by 21% between 2022 and 2025. Household spending on baby books rose from USD 420 per child in 2022 to USD 520 in 2025, representing a 23.8% increase. Additionally, institutional procurement by daycare centers and preschools accounts for 18% of total demand, equating to nearly 75 million units annually. Digital engagement tools embedded in books have improved cognitive response rates by 17%, further encouraging purchases. Retail penetration through e-commerce platforms, which now accounts for 61% of total sales, has expanded accessibility, while subscription services have grown by 18.5% annually. These combined factors reinforce strong upward momentum in the Baby Books market Growth.

United States Baby Books Market Restraint

Rising Production Costs and Supply Chain Constraints

The Baby Books market faces challenges due to escalating production costs, with raw material prices for paper increasing by 14% and fabric inputs by 11% between 2023 and 2025. Manufacturing costs per unit have risen from USD 2.10 to USD 2.48, impacting profit margins by nearly 8%. Logistics disruptions have increased transportation costs by 9%, while lead times have extended by 12%. Smaller publishers, which represent 35% of total market participants, are particularly affected, with 27% reporting reduced output capacity. Additionally, compliance with safety standards, including non-toxic materials and durability testing, adds 6–8% to production expenses. These financial pressures limit scalability and innovation investments, posing constraints on the Baby Books market Growth.

United States Baby Books Market Opportunity

Expansion of Digital Hybrid and Personalized Content

Digital hybrid formats present a significant opportunity within the Baby Books market, with adoption rates projected to exceed 40% by 2030. Currently, 28% of baby books incorporate digital elements such as QR codes or AR features, translating to approximately 118 million units. Personalized content has also emerged as a high-growth segment, with demand increasing by 19% annually and contributing USD 310 million in revenue in 2025. Subscription models, which have grown to 3.2 million users, offer recurring revenue streams and higher customer retention rates of 72%. Investments in technology integration have increased by 22%, enabling publishers to enhance engagement and learning outcomes. These advancements create new revenue channels and strengthen the Baby Books market Growth.

Challenge in United States Baby Books Market

Digital Distraction and Competing Entertainment Formats

The increasing prevalence of digital entertainment poses a challenge to the Baby Books market, with screen-based content consumption among toddlers rising by 26% between 2022 and 2025. Approximately 48% of parents report using digital devices as primary entertainment tools, reducing traditional book engagement by 13%. Mobile applications and streaming platforms collectively account for 32% of early childhood content consumption. Additionally, the average daily screen time for toddlers has increased to 1.8 hours, compared to 1.2 hours in 2022. This shift impacts demand for physical books, particularly in the entertainment segment, which has seen growth slow to 5.2% annually. Overcoming these challenges requires innovation and differentiation within the Baby Books market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.68 billion |

| Market Size in 2026 | USD 1.82 billion |

| Market Size in 2034 | USD 3.47 billion |

| CAGR | 8.41% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States Baby Books Market Segmentation

By Type

Board books dominate the market with a 58% share, translating to over 240 million units produced annually. These books are characterized by high durability, with tear resistance exceeding 95% and average thickness ranging between 2–3 mm per page. The segment benefits from strong parental preference, with 72% of households purchasing board books as the primary format. Production costs average USD 2.30 per unit, while retail prices range between USD 6 and USD 12. The segment’s dominance is further supported by institutional demand, accounting for 21% of total board book sales.

Cloth books represent 17% of the market, with production volumes reaching approximately 70 million units in 2025. These books are designed for infants under 12 months, featuring soft materials and safety-certified fabrics. Adoption rates stand at 46% among households with newborns, while durability ratings exceed 98% wash resistance. Average unit costs are higher at USD 3.10, reflecting material quality. The segment is gaining traction due to increasing demand for sensory development tools.

Interactive books account for 25% of the market, with production exceeding 100 million units annually. These books incorporate sound modules, textures, and digital integration, with 52% including electronic features. Unit costs range from USD 4.50 to USD 9.80, while adoption rates have reached 61% among urban consumers. The segment is growing rapidly due to its ability to enhance engagement and learning outcomes.

By Application

Educational learning accounts for 45% of total market share, with over 185 million units produced annually. These books focus on alphabet recognition, numbers, and early language development, achieving a penetration rate of 74% among households. Performance metrics indicate a 17% improvement in cognitive response among children exposed to educational books. Institutional demand contributes 25% of this segment’s volume.

Entertainment applications represent 32% of the market, with production volumes of approximately 130 million units. These books emphasize storytelling and visual engagement, with 63% of parents purchasing them for leisure purposes. Despite competition from digital media, the segment maintains steady demand due to its role in bonding and emotional development.

Cognitive development books account for 23% of the market, with 95 million units produced annually. These books incorporate puzzles, textures, and interactive elements to stimulate brain development. Adoption rates stand at 58%, while usage penetration is higher among urban households at 66%.

United States Baby Books Market Segmentations

Type

- Board Books

- Cloth Books

- Interactive Books

Application

- Educational Learning

- Entertainment

- Cognitive Development

United States Insights

The United States dominates the Baby Books market with a 100% regional share within the report scope, generating over USD 1.82 billion in revenue in 2026. Annual production exceeds 420 million units, with board books contributing 58%, interactive books 25%, and cloth books 17%. The country hosts over 75 major publishers and 220 smaller producers, ensuring a highly competitive landscape. E-commerce channels account for 61% of sales, while physical retail contributes 39%. Institutional procurement from daycare centers and preschools accounts for 18% of total demand. Urban regions contribute 64% of total sales, while suburban and rural areas account for 36%. Technology adoption, including AR and sound modules, is present in 35% and 52% of products respectively, reinforcing the strong regional dominance of the Baby Books market.

Top Players in United States Baby Books Market

- Penguin Random House

- Scholastic Corporation

- HarperCollins Publishers

- Hachette Book Group

- Macmillan Publishers

- DK Publishing

- Usborne Publishing

- Chronicle Books

- Candlewick Press

- Workman Publishing

- Simon & Schuster

- Sourcebooks

- Abrams Books

- Nosy Crow

- Barefoot Books

Top Two Companies

-

Penguin Random House

-

Holds approximately 18% market share

-

Strong presence across all formats with over 85 million units produced annually

-

Invests 20% of revenue in R&D and innovation

-

Extensive distribution network covering 95% of retail channels

-

-

Scholastic Corporation

-

Accounts for nearly 14% market share

-

Produces over 60 million units annually

-

Strong institutional partnerships contributing 28% of its revenue

-

Focus on educational content with 70% of its portfolio aligned to learning applications

-

Investment

Investment in the Baby Books market has increased significantly, with total funding exceeding USD 420 million in 2025. Approximately 38% of investments are allocated to digital integration, while 27% focus on sustainable materials and 35% on content development. Venture capital participation has grown by 16%, with 42% of funding directed toward startups specializing in personalized and subscription-based models. Regional investment is concentrated in urban areas, accounting for 68% of total funding.

Mergers and acquisitions have intensified, with 12 major deals recorded between 2023 and 2025. Strategic collaborations between publishers and technology firms have increased by 19%, enabling the integration of AR and AI-driven content. Joint ventures focusing on eco-friendly production have grown by 14%, reflecting rising consumer demand for sustainable products. These trends highlight strong investment potential within the market.

New Product

New product development accounts for 22% of total product launches, with over 90 million units introduced in 2025. Innovations include AR-enabled storytelling, which improves engagement by 21%, and sound-integrated books with enhanced audio clarity of up to 30%. Sustainable materials are used in 41% of new products, reflecting growing environmental awareness. Performance improvements in durability and safety standards exceed 95%, ensuring compliance with regulatory requirements.

Recent Development in United States Baby Books Market

- 2025: A leading publisher increased production capacity by 12%, adding 15 million units annually and expanding its market presence through digital integration features.

- 2024: Introduction of AR-enabled baby books resulted in a 17% increase in sales, with adoption rates reaching 28% among urban consumers.

- 2023: Expansion of eco-friendly product lines led to a 14% growth in sustainable book sales, accounting for 41% of total production.

Research Methodology for United States Baby Books Market

The research process for the Baby Books market involves a combination of primary and secondary data collection methods. Primary research includes interviews with over 50 industry experts, publishers, and distributors, providing insights into production volumes, pricing trends, and consumer behavior. Secondary research involves analyzing industry reports, company filings, and government publications to validate data. Market size estimation is conducted using both top-down and bottom-up approaches, incorporating historical data from 2022–2024 and projections for 2026–2034. Data triangulation ensures accuracy, while statistical models are used to forecast growth trends. The methodology ensures comprehensive coverage of market dynamics, segmentation, and competitive landscape.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.